Videos

Financial and nonfinancial performance measures, goal congruence. (CMA, adapted) Precision Equipment specializes in the manufacture of medical equipment, a field that has become increasingly competitive. Approximately 2 years ago, Pedro Mendez, president of Precision, decided to revise the bonus plan (based, at the time, entirely on operating income) to encourage division managers to focus on areas that were important to customers and that added value without increasing cost. In addition to a profitability incentive, the revised plan includes incentives for reduced rework costs, reduced sales returns, and on-time deliveries. The company calculates and rewards bonuses semiannually on the following basis: A base bonus is calculated at 2% of operating income; this amount is then adjusted as follows:

- i. Reduced by excess of rework costs over and above 2% of operating income

- ii. No adjustment if rework costs are less than or equal to 2% of operating income

- i. Increased by $4,000 if more than 98% of deliveries are on time and by $1,500 if 96–98% of deliveries are on time

- ii. No adjustment if on-time deliveries are below 96%

- i. Increased by $2,500 if sales returns are less than or equal to 1.5% of sales

- ii. Decreased by 50% of excess of sales returns over 1.5% of sales

If the calculation of the bonus results in a negative amount for a particular period, the manager simply receives no bonus, and the negative amount is not carried forward to the next period.

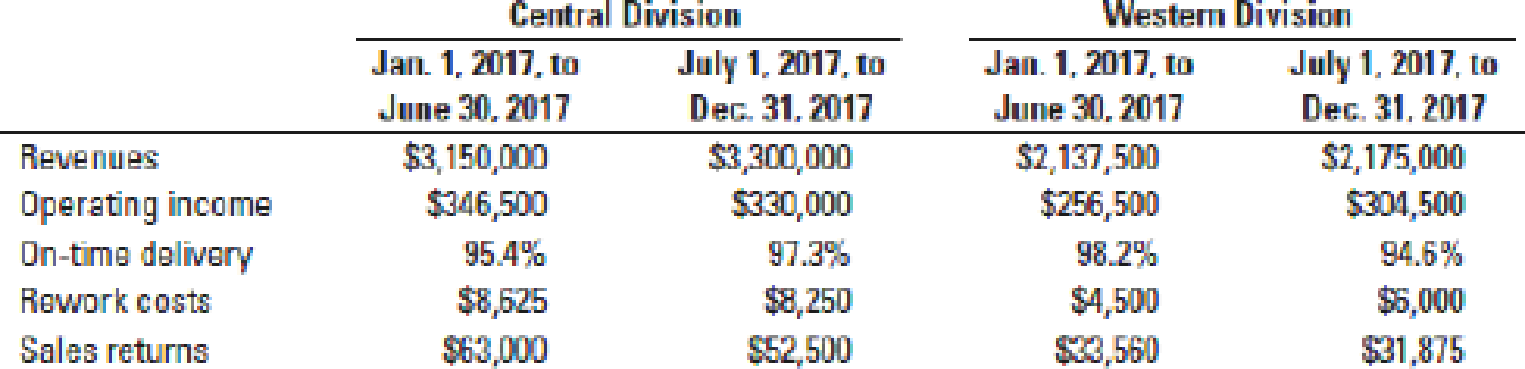

Results for Precision’s Central division and Western division for 2017, the first year under the new bonus plan, follow. In 2016, under the old bonus plan, the Central division manager earned a bonus of $20,295 and the Western division manager received a bonus of $15,830.

- 1. Why did Mendez need to introduce these new performance measures? That is, why does Mendez need to use these performance measures in addition to the operating-income numbers for the period?

- 2. Calculate the bonus earned by each manager for each 6-month period and for 2017 overall.

- 3. What effect did the change in the bonus plan have on each manager’s behavior? Did the new bonus plan achieve what Mendez wanted? What changes, if any, would you make to the new bonus plan?

Want to see the full answer?

Check out a sample textbook solution

Chapter 23 Solutions

COST ACCT

- Suspicious Acquisition of Data, Ethical Issues Bill Lewis, manager of the Thomas Electronics Division, called a meeting with his controller, Brindon Peterson, and his marketing manager, Patty Fritz. The following is a transcript of the conversation that took place during the meeting: Bill: Brindon, the variable costing system that you developed has proved to be a big plus for our division. Our success in winning bids has increased, and as a result our revenues have increased by 25%. However, if we intend to meet this years profit targets, we are going to need something extraam I right, Patty? Patty: Absolutely. While we have been able to win more bids, we still are losing too many, particularly to our major competitor, Kilborn Electronics. If we knew more about their bidding strategy, we could be more successful at competing with them. Brindon: Would knowing their variable costs help? Patty: Certainly. It would give me their minimum price. With that knowledge, Im sure that we could find a way to beat them on several jobs, particularly on those jobs where we are at least as efficient. It would also help us to identify where we are not cost competitive. With this information, we might be able to find ways to increase our efficiency. Brindon: Well, I have good news. Ive been talking with Carl Penobscot, Kilborns assistant controller. Carl doesnt feel appreciated by Kilborn and wants to make a change. He could easily fit into our team here. Plus, Carl has been preparing for a job switch by quietly copying Kilborns accounting files and records. Hes already given me some data that reveal bids that Kilborn made on several jobs. If we can come to a satisfactory agreement with Carl, hell bring the rest of the information with him. Well easily be able to figure out Kilborns prospective bids and find ways to beat them. Besides, I could use another accountant on my staff. Bill, would you authorize my immediate hiring of Carl with a favorable compensation package? Bill: I know that you need more staff, Brindon, but is this the right thing to do? It sounds like Carl is stealing those files, and surely Kilborn considers this information confidential. I have real ethical and legal concerns about this. Why dont we meet with Laurie, our attorney, and determine any legal problems? Required: 1. Is Carls behavior ethical? What would Kilborn think? 2. Is Bill correct in supposing that there are ethical and/or legal problems involved with the hiring of Carl? (Reread the section on corporate codes of conduct in Chapter 1.) What would you do if you were Bill? Explain.arrow_forwardIn 20x5, Major Company initiated a full-scale, quality improvement program. At the end of the year, Jack Aldredge, the president, noted with some satisfaction that the defects per unit of product had dropped significantly compared to the prior year. He was also pleased that relationships with suppliers had improved and defective materials had declined. The new quality training program was also well accepted by employees. Of most interest to the president, however, was the impact of the quality improvements on profitability. To help assess the dollar impact of the quality improvements, the actual sales and the actual quality costs for 20x4 and 20x5 are as follows by quality category: All prevention costs are fixed (by discretion). Assume all other quality costs are unit-level variable. Required: 1. Compute the relative distribution of quality costs for each year and prepare a pie chart. Do you believe that the company is moving in the right direction in terms of the balance among the quality cost categories? Explain. 2. Prepare a one-year trend performance report for 20x5 (compare the actual costs of 20x5 with those of 20x4, adjusted for differences in sales volume). How much have profits increased because of the quality improvements made by Major Company? 3. Estimate the additional improvement in profits if Major Company ultimately reduces its quality costs to 2.5 percent of sales revenues (assume sales of 10 million).arrow_forwardIn 20X1, Don Blackburn, president of Price Electronics, received a report indicating that quality costs were 31% of sales. Faced with increasing pressures from imported goods. Don resolved to take measures to improve the overall quality of the companys products. After hiring a consultant in 20X1, the company began an aggressive program of total quality control. At the end of 20X5, Don requested an analysis of the progress the company had made in reducing and controlling quality costs. The accounting department assembled the following data: Required: 1. Compute the quality costs as a percentage of sales by category and in total for each year. 2. Prepare a multiple-year trend graph for quality costs, both by total costs and by category. Using the graph, assess the progress made in reducing and controlling quality costs. Does the graph provide evidence that quality has improved? Explain. 3. Using the 20X1 quality cost relationships (assume all costs are variable), calculate the quality costs that would have prevailed in 20X4. By how much did profits increase in 20X4 because of the quality improvement program? Repeat for 20X5.arrow_forward

- At the beginning of the last quarter of 20x1, Youngston, Inc., a consumer products firm, hired Maria Carrillo to take over one of its divisions. The division manufactured small home appliances and was struggling to survive in a very competitive market. Maria immediately requested a projected income statement for 20x1. In response, the controller provided the following statement: After some investigation, Maria soon realized that the products being produced had a serious problem with quality. She once again requested a special study by the controllers office to supply a report on the level of quality costs. By the middle of November, Maria received the following report from the controller: Maria was surprised at the level of quality costs. They represented 30 percent of sales, which was certainly excessive. She knew that the division had to produce high-quality products to survive. The number of defective units produced needed to be reduced dramatically. Thus, Maria decided to pursue a quality-driven turnaround strategy. Revenue growth and cost reduction could both be achieved if quality could be improved. By growing revenues and decreasing costs, profitability could be increased. After meeting with the managers of production, marketing, purchasing, and human resources, Maria made the following decisions, effective immediately (end of November 20x1): a. More will be invested in employee training. Workers will be trained to detect quality problems and empowered to make improvements. Workers will be allowed a bonus of 10 percent of any cost savings produced by their suggested improvements. b. Two design engineers will be hired immediately, with expectations of hiring one or two more within a year. These engineers will be in charge of redesigning processes and products with the objective of improving quality. They will also be given the responsibility of working with selected suppliers to help improve the quality of their products and processes. Design engineers were considered a strategic necessity. c. Implement a new process: evaluation and selection of suppliers. This new process has the objective of selecting a group of suppliers that are willing and capable of providing nondefective components. d. Effective immediately, the division will begin inspecting purchased components. According to production, many of the quality problems are caused by defective components purchased from outside suppliers. Incoming inspection is viewed as a transitional activity. Once the division has developed a group of suppliers capable of delivering nondefective components, this activity will be eliminated. e. Within three years, the goal is to produce products with a defect rate less than 0.10 percent. By reducing the defect rate to this level, marketing is confident that market share will increase by at least 50 percent (as a consequence of increased customer satisfaction). Products with better quality will help establish an improved product image and reputation, allowing the division to capture new customers and increase market share. f. Accounting will be given the charge to install a quality information reporting system. Daily reports on operational quality data (e.g., percentage of defective units), weekly updates of trend graphs (posted throughout the division), and quarterly cost reports are the types of information required. g. To help direct the improvements in quality activities, kaizen costing is to be implemented. For example, for the year 20x1, a kaizen standard of 6 percent of the selling price per unit was set for rework costs, a 25 percent reduction from the current actual cost. To ensure that the quality improvements were directed and translated into concrete financial outcomes, Maria also began to implement a Balanced Scorecard for the division. By the end of 20x2, progress was being made. Sales had increased to 26,000,000, and the kaizen improvements were meeting or beating expectations. For example, rework costs had dropped to 1,500,000. At the end of 20x3, two years after the turnaround quality strategy was implemented, Maria received the following quality cost report: Maria also received an income statement for 20x3: Maria was pleased with the outcomes. Revenues had grown, and costs had been reduced by at least as much as she had projected for the two-year period. Growth next year should be even greater as she was beginning to observe a favorable effect from the higher-quality products. Also, further quality cost reductions should materialize as incoming inspections were showing much higher-quality purchased components. Required: 1. Identify the strategic objectives, classified by the Balanced Scorecard perspective. Next, suggest measures for each objective. 2. Using the results from Requirement 1, describe Marias strategy using a series of if-then statements. Next, prepare a strategy map. 3. Explain how you would evaluate the success of the quality-driven turnaround strategy. What additional information would you like to have for this evaluation? 4. Explain why Maria felt that the Balanced Scorecard would increase the likelihood that the turnaround strategy would actually produce good financial outcomes. 5. Advise Maria on how to encourage her employees to align their actions and behavior with the turnaround strategy.arrow_forwardAt the end of 2021, Mejorar Company implemented a low-cost strategy to improve its competitive position. Its objective was to become the low-cost producer in its industry. A Balanced Scorecard was developed to guide the company toward this objective. To lower costs, Mejorar undertook a number of improvement activities such as JIT production, total quality management, and activity-based management. Now, after two years of operation, the president of Mejorar wants some assessment of the achievements. To help provide this assessment, the following information on one product has been gathered: 1. Compute the following measures for 2021 and 2023: a. actual velocity and cycle time (2021 and 2023) (My question: In the book it stated that Actual Velocity (# units produced/time) and Cycle Time (time/# units produced) However, which one is per hour and per minute Or maybe I wrong let me know?) b. Percentage of total revenue from new customers (2021 and 2023) (assume one unit per customer) c.…arrow_forwardInternal and External Linkages, Strategic Cost Management Maxwell Company produces a variety of kitchen appliances, including cooking ranges and dishwashers. Over the past several years, competition has intensified. In order to maintain—and perhaps increase—its market share, Maxwell’s management decided that the overall quality of its products had to be increased. Furthermore, costs needed to be reduced so that the selling prices of its products could be reduced. After some investigation, Maxwell concluded that many of its problems could be traced to the unreliability of the parts that were purchased from outside suppliers. Many of these components failed to work as intended, causing performance problems. Over the years, the company had increased its inspection activity of the final products. If a problem could be detected internally, then it was usually possible to rework the appliance so that the desired performance was achieved. Management also had increased its warranty coverage;…arrow_forward

- Blue is the controller at the Acme Shoe Company, a large manufacturing companylocated in Franklin, Pennsylvania. Acme has many divisions, and the performance ofeach division has typically been evaluated using a retum on investment (ROI)formula. The return on investment is caleulated by dividing profit by the book value of total assets.In a meeting yesterday with Bob Burn, the compuny president, Blue warned that thisreturn on investment measure might not be accurately rellecting how well thedivisions are doing. Blue is concerned that by using profits and the book value ofussets, division managers might be engaging in some short-term finagling to show the highest possible return. Bob concurred and asked what other numbers they could use to evaluate division performance.Blue said,T'm not sure, Bob. Net income isn't a good number for evaluationpurposes. Becuse we allocate a lot of overhead costs to the divisions on what somemanagers consider an arbitrary basis, net income won't work as a…arrow_forwardFaced with headquarters’ desire to add a new product line, Stefan Grenier, manager of Bilti Products’ East Division, felt that he had to see the numbers before he made a move. His division’s ROI has led the company for three years, and he doesn’t want any letdown. Bilti Products is a decentralized wholesaler with four autonomous divisions. The divisions are evaluated on the basis of ROI, with year-end bonuses given to divisional managers who have the highest ROI. Operating results for the company’s East Division for last year are given below: Sales $ 28,700,000 Variable expenses 14,390,000 Contribution margin 14,310,000 Fixed expenses 12,301,000 Operating income $ 2,009,000 Divisional operating assets $ 7,175,000 The company had an overall ROI of 16% last year (considering all divisions). The new product line that headquarters wants Grenier’s East Division to add would require an investment of $4,100,000. The cost and revenue characteristics…arrow_forwardFaced with headquarters’ desire to add a new product line, Stefan Grenier, manager of Bilti Products’ East Division, felt that he had to see the numbers before he made a move. His division’s ROI has led the company for three years, and he doesn’t want any letdown. Bilti Products is a decentralized wholesaler with four autonomous divisions. The divisions are evaluated on the basis of ROI, with year-end bonuses given to divisional managers who have the highest ROI. Operating results for the company’s East Division for last year are given below: Sales $ 23,800,000 Variable expenses 13,760,000 Contribution margin 10,040,000 Fixed expenses 8,374,000 Operating income $ 1,666,000 Divisional operating assets $ 5,950,000 The company had an overall ROI of 16% last year (considering all divisions). The new product line that headquarters wants Grenier’s East Division to add would require an investment of $3,400,000. The cost and revenue characteristics of…arrow_forward

- Lindell Manufacturing embarked on an ambitious quality program that is centered on continual improvement. This improvement is operationalized by declining quality costs from year toyear. Lindell rewards plant managers, production supervisors, and workers with bonuses ranging from $1,000 to $10,000 if their factory meets its annual quality cost goals.Len Smith, manager of Lindell’s Boise plant, felt obligated to do everything he could toprovide this increase to his employees. Accordingly, he has decided to take the following actionsduring the last quarter of the year to meet the plant’s budgeted quality cost targets:a. Decrease inspections of the process and final product by 50% and transfer inspectorstemporarily to quality training programs. Len believes this move will increase theinspectors’ awareness of the importance of quality; also, decreasing inspection willproduce significantly less downtime and less rework. By increasing the output anddecreasing the costs of internal failure,…arrow_forwardMindspin Labs Inc. is a manufacturing firm that has experienced strong competition in its traditional business. Management is considering joining the trend to the "service economy" by eliminating its manufacturing operations and concentrating on providing specialized maintenance services to other manufacturers. Management of Mindspin Labs has had a target ROI of 16% on an asset base that has averaged $8 million. To achieve this ROI, average total asset turnover of 2 was required. If the company shifts its operations from manufacturing to providing maintenance services, it is estimated that average total assets will decrease to $5 million.Required: Calculate net income, margin, and sales required for Mindspin Labs to achieve its target ROI as a manufacturing firm. Assume that the average margin of maintenance service firms is 2.50%, and that the average ROI for such firms is also 17%. Calculate the net income, sales, and total asset turnover that Mindspin Labs will have if the change…arrow_forwardStrategy, balanced scorecard, service company. Compton Associates is an architectural firm that has been in practice only a few years. Because it is a relatively new firm, the market for the firm’s services is very competitive. To compete successfully, Compton must deliver quality services at a low cost. Compton presents the following data for 2016 and 2017. Architect labor-hour costs are variable costs. Architect support costs for each year depend on the Architect support capacity that Compton chooses to maintain each year (that is, the number of jobs it can do each year). Architect support costs do not vary with the actual number of jobs done that year. 1. Is Compton Associate’s strategy one of product differentiation or cost leadership? Explain briefly. 2. Describe key measures you would include in Compton’s balanced scorecard and your reasons for doing so.arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College