Concept explainers

Videos

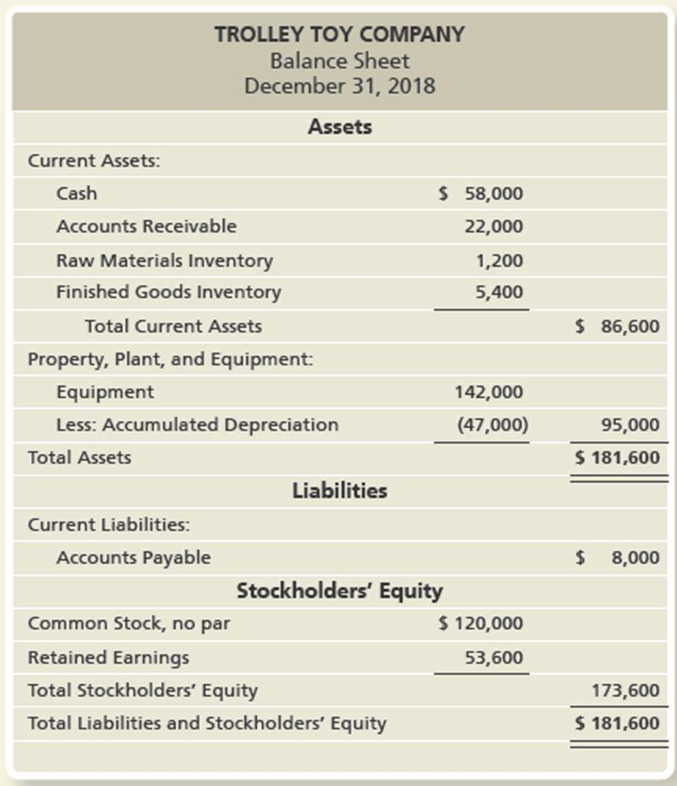

The Trolley Toy Company manufactures toy building block sets for children. Trolley is planning for 2019 by developing a

Other budget data for Trolley Toy Company:

- a. Budgeted sales are 1,400 sets for the first quarter and expected to increase by 150 sets per quarter. Cash sales are expected to be 30% of total sales, with the remaining 70% of sales on account. Sets are budgeted to sell for $90 per set.

- b. Finished Goods Inventory on December 31, 2018, consists of 200 sets at $27 each.

- c. Desired ending Finished Goods Inventory is 40% of the next quarter’s sales; first quarter sales for 2020 are expected to be 2,000 sets. FIFO inventory costing method is used.

- d. Raw Materials Inventory on December 31, 2018, consists of 600 pounds. Direct materials requirement is 3 pounds per set. The cost is $2 per pound.

- e. Desired ending Raw Materials Inventory is 10% of the next quarter’s direct materials needed for production; desired ending inventory for December 31, 2019, is 600 pounds; indirect materials are insignificant and not considered for budgeting purposes.

- f. Each set requires 0.30 hours of direct labor; direct labor costs average $12 per hour.

- g. Variable manufacturing overhead is $3.60 per set.

- h. Fixed manufacturing overhead includes $7,000 per quarter in

depreciation and $2,585 per quarter for other costs, such as utilities, insurance, and property taxes. - i. Fixed selling and administrative expenses include $11,000 per quarter for salaries; $1,500 per quarter for rent; $1,350 per quarter for insurance; and $1,500 per quarter for depreciation.

- j. Variable selling and administrative expenses include supplies at 2% of sales.

- k. Capital expenditures include $45,000 for new manufacturing equipment, to be purchased and paid for in the first quarter.

- l. Cash receipts for sales on account are 40% in the quarter of the sale and 60% in the quarter following the sale; Accounts Receivable balance on December 31, 2018, is expected to be received in the first quarter of 2019; uncollectible accounts are considered insignificant and not considered for budgeting purposes.

- m. Direct materials purchases are paid 90% in the quarter purchased and 10% in the following quarter; Accounts Payable balance on December 31, 2018, is expected to be paid in the first quarter of 2019.

- n. Direct labor, manufacturing overhead, and selling and administrative costs are paid in the quarter incurred.

- o. Income tax expense is projected at $3,500 per quarter and is paid in the quarter incurred.

- p. Trolley desires to maintain a minimum cash balance of $55,000 and borrows from the local bank as needed in increments of $1,000 at the beginning of the quarter; principal repayments are made at the beginning of the quarter when excess funds are available and in increments of $1,000; interest is 10% per year and paid at the beginning of the quarter based on the amount outstanding from the previous quarter.

Requirements

- 1. Prepare Trolley’s operating budget and

cash budget for 2019 by quarter. Required schedules and budgets include: sales budget, production budget, direct materials budget, direct labor budget, manufacturing overhead budget, cost of goods sold budget, selling and administrative expense budget, schedule of cash receipts, schedule of cash payments, and cash budget.Manufacturing overhead costs are allocated based on direct labor hours. - 2. Prepare Trolley’s annual financial budget for 2019, including

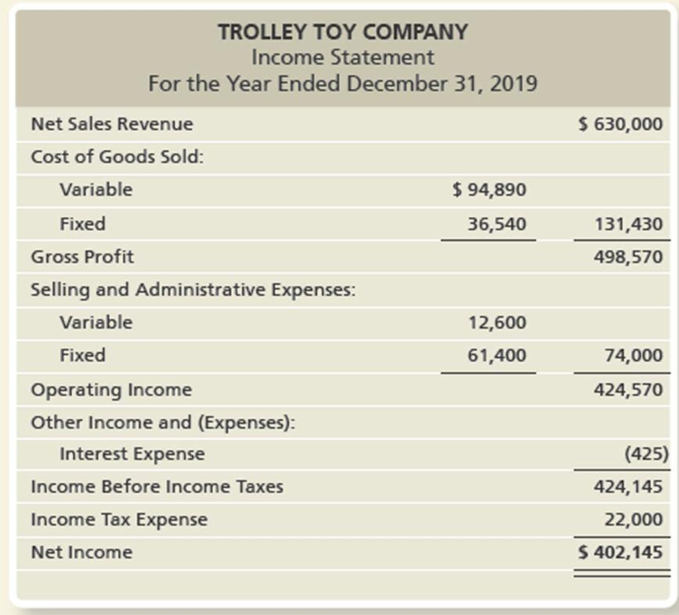

budgeted income statement and budgeted balance sheet. - 3. Trolley sold 7,000 sets in 2019, and its actual operating income was as follows:

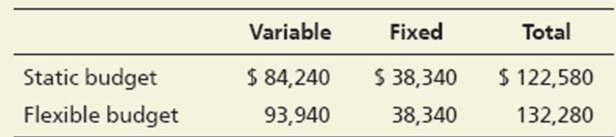

Prepare a flexible budget performance report through operating income for 2019. Show product costs separately from selling and administrative costs. To simplify the calculations due to sets in beginning inventory having a different cost than those produced and sold in 2019, assume the following product costs:

- 4. What was the effect on Trolley’s operating income of selling 500 sets more than the static budget level of sales?

- 5. What is Trolley’s static

budget variance for operating income? - 6. Explain why the flexible budget performance report provides more useful information to Trolley’s managers than the static budget performance report. What insights can Trolley’s managers draw from this performance report?

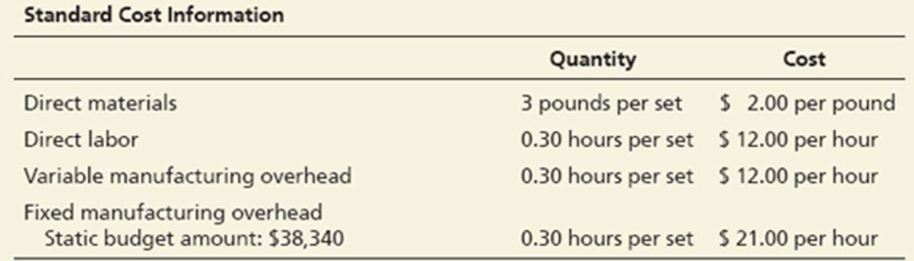

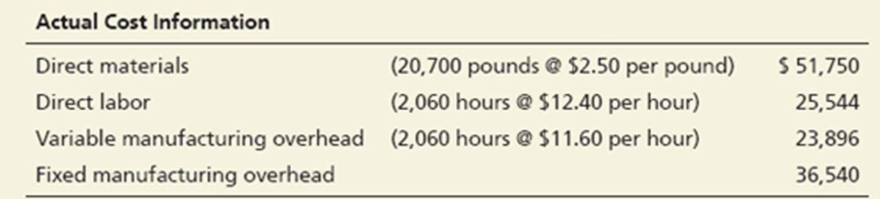

- 7. During 2019, Trolley recorded the following cost data:

Compute the cost and efficiency variances for direct materials and direct labor.

- 8. For manufacturing overhead, compute the variable overhead cost and efficiency variances and the fixed overhead cost and volume variances.

- 9. Prepare the

standard cost income statement for 2019. - 10. Calculate Trolley’s ROI for 2019. To calculate average total assets, use the December 31, 2018, balance sheet for the beginning balance and the budgeted balance sheet for December 31, 2019, for the ending balance. Round all of your answers to four decimal places.

- 11. Calculate Trolley’s profit margin ratio for 2019. Interpret your results.

- 12. Calculate Trolley’s asset turnover ratio for 2019. Interpret your results.

- 13. Use the expanded ROI formula to confirm your results from Requirement 10. Interpret your results.

- 14. Trolley’s management has specified a 30% target

rate of return . Calculate Trolley’s RI for 2019. Interpret your results.

Want to see the full answer?

Check out a sample textbook solution

Chapter 24 Solutions

EP FINANCIAL+MANAGERIAL ACCT. >CUSTOM<

Additional Business Textbook Solutions

Principles of Accounting Volume 2

Intermediate Accounting

Managerial Accounting (4th Edition)

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

Financial Accounting (12th Edition) (What's New in Accounting)

Financial Accounting, Student Value Edition (5th Edition)

- CASH BUDGETING Helen Bowers, owner of Helens Fashion Designs, is planning to request a line of credit from her bank. She has estimated the following sales forecasts for the firm for parts of 2019 and 2020: Estimates regarding payments obtained from the credit department are as follows: collected within the month of sale, 10%; collected the month following the sale, 75%; collected the second month following the sale, 15%. Payments for labor and raw materials are made the month after these services were provided. Here are the estimated costs of labor plus raw materials: General and administrative salaries are approximately 27,000 a month. Lease payments under long-term leases are 9,000 a month. Depreciation charges are 36,000 a month. Miscellaneous expenses are 2,700 a month. Income tax payments of 63,000 are due in September and December. A progress payment of 180,000 on a new design studio must be paid in October. Cash on hand on July 1 will be 132,000, and a minimum cash balance of 90,000 should be maintained throughout the cash budget period. a. Prepare a monthly cash budget for the last 6 months of 2019. b. Prepare monthly estimates of the required financing or excess fundsthat is, the amount of money Bowers will need to borrow or will have available to invest. c. Now suppose receipts from sales come in uniformly during the month (that is, cash receipts come in at the rate of 1/30 each day), but all outflows must be paid on the 5th. Will this affect the cash budget? That is, will the cash budget you prepared be valid under these assumptions? If not, what could be done to make a valid estimate of the peak financing requirements? No calculations are required, although if you prefer, you can use calculations to illustrate the effects. d. Bowers sales are seasonal, and her company produces on a seasonal basis, just ahead of sales. Without making any calculations, discuss how the companys current and debt ratios would vary during the year if all financial requirements were met with short-term bank loans. Could changes in these ratios affect the firms ability to obtain bank credit? Explain.arrow_forwardThe sales department of Macro Manufacturing Co. has forecast sales for its single product to be 20,000 units for June, with three-quarters of the sales expected in the East region and one-fourth in the West region. The budgeted selling price is 25 per unit. The desired ending inventory on June 30 is 2,000 units, and the expected beginning inventory on June 1 is 3,000 units. Prepare the following: a. A sales budget for June. b. A production budget for June.arrow_forwardNorton Company, a manufacturer of infant furniture and carriages, is in the initial stages of preparing the annual budget for the coming year. Scott Ford has recently joined Nortons accounting staff and is interested in learning as much as possible about the companys budgeting process. During a recent lunch with Marge Atkins, sales manager, and Pete Granger, production manager, Ford initiated the following conversation. FORD: Since Im new around here and am going to be involved with the preparation of the annual budget, Id be interested in learning how the two of you estimate sales and production numbers. ATKINS: We start out very methodically by looking at recent history, discussing what we know about current accounts, potential customers, and the general state of consumer spending. Then, we add that usual dose of intuition to come up with the best forecast we can. GRANGER: I usually take the sales projections as the basis for my projections. Of course, we have to make an estimate of what this years closing inventories will be, which is sometimes difficult. FORD: Why does that present a problem? There must have been an estimate of closing inventories in the budget for the current year. GRANGER: Those numbers arent always reliable since Marge makes some adjustments to the sales numbers before passing them on to me. FORD: What kind of adjustments? ATKINS: Well, we dont want to fall short of the sales projections so we generally give ourselves a little breathing room by lowering the initial sales projection anywhere from 5 to 10 percent. GRANGER: So, you can see why this years budget is not a very reliable starting point. We always have to adjust the projected production rates as the year progresses, and of course, this changes the ending inventory estimates. By the way, we make similar adjustments to expenses by adding at least 10 percent to the estimates; I think everyone around here does the same thing. Required: 1. Marge Atkins and Pete Granger have described the use of budgetary slack. a. Explain why Atkins and Granger behave in this manner, and describe the benefits they expect to realize from the use of budgetary slack. b. Explain how the use of budgetary slack can adversely affect Atkins and Granger. 2. As a management accountant, Scott Ford believes that the behavior described by Marge Atkins and Pete Granger may be unethical and that he may have an obligation not to support this behavior. By citing the specific standards of competence, confidentiality, integrity, and/or credibility from the Statement of Ethical Professional Practice (in Chapter 1), explain why the use of budgetary slack may be unethical. (CMA adapted)arrow_forward

- Shalimar Company manufactures and sells industrial products. For next year, Shalimar has budgeted the follow sales: In Shalimars experience, 10 percent of sales are paid in cash. Of the sales on account, 65 percent are collected in the quarter of sale, 25 percent are collected in the quarter following the sale, and 7 percent are collected in the second quarter after the sale. The remaining 3 percent are never collected. Total sales for the third quarter of the current year are 4,900,000 and for the fourth quarter of the current year are 6,850,000. Required: 1. Calculate cash sales and credit sales expected in the last two quarters of the current year, and in each quarter of next year. 2. Construct a cash receipts budget for Shalimar Company for each quarter of the next year, showing the cash sales and the cash collections from credit sales. 3. What if the recession led Shalimars top management to assume that in the next year 10 percent of credit sales would never be collected? The expected payment percentages in the quarter of sale and the quarter after sale are assumed to be the same. How would that affect cash received in each quarter? Construct a revised cash budget using the new assumption.arrow_forwardBefore the year began, the following static budget was developed for the estimated sales of 50,000. Sales are higher than expected and management needs to revise its budget. Prepare a flexible budget for 100,000 and 110,000 units of sales.arrow_forwardReview the completed master budget and answer the following questions: Is Ranger Industries expecting to earn a profit during the next quarter? If so, how much? Does the company need to borrow cash during the quarter? Can it make any repayments? Explain. (Carefully review rows 74 through 80.)arrow_forward

- Before the year began, the following static budget was developed for the estimated sales of 100,000. Sales are sluggish and management needs to revise its budget. Use this information to prepare a flexible budget for 80,000 and 90,000 units of sales.arrow_forwardStarburst Inc. has the following items and amounts as part of its master budget at the 10,000-unit level of sales and production: Determine the total dollar amounts for the above items that would appear in a flexible budget at the following volume levels, assuming that both levels are within the relevant range: a. 8,000-unit level of sales and production b. 12,000-unit level of sales and production (Hint: You must first determine the unit selling price and certain unit costs.)arrow_forwardCash budget The controller of Bridgeport Housewares Inc. instructs you to prepare a monthly cash budget for the next three months. You are presented with the following budget information: The company expects to sell about 10% of its merchandise for cash. Of sales on account, 70% are expected to be collected in the month following the sale and the remainder the following month (second month following sale). Depreciation, insurance, and property tax expense represent 50,000 of the estimated monthly manufacturing costs. The annual insurance premium is paid in January, and the annual property taxes are paid in December. Of the remainder of the manufacturing costs, 80% are expected to be paid in the month in which they are incurred and the balance in the following month. Current assets as of September 1 include cash of 40,000, marketable securities of 75,000, and accounts receivable of 300,000 (60,000 from July sales and 240,000 from August sales). Sales on account for July and August were 200,000 and 240,000, respectively. Current liabilities as of September 1 include 40,000 of accounts payable incurred in August for manufacturing costs. All selling and administrative expenses are paid in cash in the period they are incurred. An estimated income tax payment of 55,000 will be made in October. Bridgeports regular quarterly dividend of 25,000 is expected to be declared in October and paid in November. Management desires to maintain a minimum cash balance of 50,000. Instructions Prepare a monthly cash budget and supporting schedules for September, October, and November. On the basis of the cash budget prepared in part (1), what recommendation should be made to the controller?arrow_forward

- Digital Solutions Inc. uses flexible budgets that are based on the following data: Prepare a flexible selling and administrative expenses budget for October for sales volumes of 500,000, 750,000, and 1,000,000.arrow_forwardLovely Wedding printing is budgeting sales of 32,000 units and already has 4,000 in beginning inventory. How many units must be produced to also meet the 6,000 units required in ending inventory?arrow_forwardPilsner Inc. purchases raw materials on account for use in production. The direct materials purchases budget shows the following expected purchases on account: Pilsner typically pays 25% on account in the month of billing and 75% the next month. Required: 1. How much cash is required for payments on account in May? 2. How much cash is expected for payments on account in June?arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT