Concept explainers

Videos

Finlon Upholstery, Inc. uses a

Finlon applies manufacturing

Job no. 2077 was completed in January 20x2; there was no work in process at year-end. All jobs produced during 20x2 were sold with the exception of job no. 2143, which contained direct-material costs of $156,000 and direct-labor charges of $85,000. The company charges any under- or overapplied overhead to Cost of Goods Sold.

Required:

- 1. Determine the company’s predetermined overhead application rate.

- 2. Determine the additions to the Work-in-Process Inventory account for direct material used, direct labor, and manufacturing overhead.

- 3. Compute the amount that the company would disclose as finished-goods inventory on the December 31, 20x2, balance sheet.

- 4. Prepare the

journal entry needed to record the year’s completed production. - 5. Compute the amount of under- or overapplied overhead at year-end, and prepare the necessary journal entry to record its disposition.

- 6. Determine the company’s 20x2 cost of goods sold.

- 7. Would it be appropriate to include selling and administrative expenses in either manufacturing overhead or cost of goods sold? Briefly explain.

1.

Calculate the amount of Company F’s predetermined overhead application rate.

Explanation of Solution

Predetermined Overhead Rate: Predetermined overhead rate is a measure used to allocate the estimated manufacturing overhead cost to the products or job orders during a particular period. This is generally evaluated at the beginning of each reporting period. The evaluation takes into account the estimated manufacturing overhead cost and the estimated allocation base that includes direct labor hours, direct labor in dollars, machine hours and direct materials.

Calculate the amount of Company F’s predetermined overhead application rate.

Thus, the amount of Company F’s predetermined overhead application rate is 130% of direct labor cost.

2.

Calculate the additions that are made to the work-in-process inventory account for direct materials used, direct labor, and manufacturing overhead.

Explanation of Solution

Work-in-process is the middle part of raw materials and finished goods. This inventory is the portion of the manufactured inventory for which the process has been started but not yet completed.

Calculate the additions that are made to the work-in-process inventory account for direct materials used, direct labor, and manufacturing overhead.

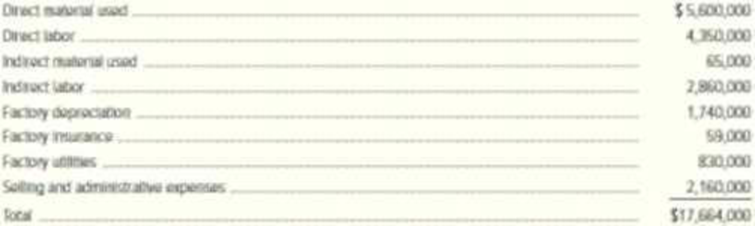

| Particulars | Amount ($) |

| Direct materials used | $5,600,000 |

| Direct labor | $4,350,000 |

| Manufacturing overhead | $5,655,000 |

| Total | $15,605,000 |

Table (1)

Thus, the total addition (debits) made to work-in process inventory account is $15,605,000.

3.

Identify the amount that would be disclosed by the company as finished goods inventory on the balance sheet as of December 31, 20x2.

Explanation of Solution

Finished goods inventory are completely ready for sale after completing the production process.

The amount that would be disclosed by the company as finished goods inventory on the balance sheet as of December 31, 20x2 is $351,500

4.

Prepare the journal entry in the books of Company F to record the year’s completed production.

Explanation of Solution

Prepare the journal entry in the books of Company F to record the year’s completed production.

| Date | Account title and explanation | Debit ($) | Credit ($) |

| Finished-goods inventory | 15,761,800 | ||

| Work-in-process inventory | 15,761,800 | ||

| (To record the company’s completed production) |

Table (2)

5.

Calculate the amount of under-applied or over-applied at year end and record its disposition.

Explanation of Solution

Under-applied overhead:

When there is a debit balance in the manufacturing overhead account during the month end, it indicates that overheads applied to jobs are less than the actual overhead cost incurred by the business. Therefore, the debit balance in the manufacturing overhead account is referred to as under-applied overhead.

Over-applied overhead:

When there is a credit balance in the manufacturing overhead account during the month end, indicates that overheads applied to jobs is more than the actual overhead cost incurred by the business. Therefore, the credit balance in the manufacturing overhead account is referred to as over- applied overhead.

Step 1: calculate the amount of actual overhead.

| Particulars | Amount ($) |

| Indirect materials used | $65,000 |

| Indirect labor | $2,860,000 |

| Factory depreciation | $1,740,000 |

| Factory insurance | $59,000 |

| Factory utilities | $830,000 |

| Total | $5,554,000 |

Table (3)

Step 2: Calculate the amount of under-applied or over-applied overhead.

Working note (1):

Calculate the amount of applied overhead.

Thus, the overhead is over-applied by $101,000.

Prepare the journal entry.

| Date | Account title and explanation | Debit ($) | Credit ($) |

| Manufacturing overhead | 101,000 | ||

| Cost of goods sold | 101,000 | ||

| (To record the company’s completed production) |

Table (4)

6.

Calculate the cost of goods sold of Company F for the year 20x2.

Explanation of Solution

Cost of goods sold: Cost of goods sold is the total of all the expenses incurred by a company to sell the goods during the given period.

Calculate the cost of goods sold of Company F for the year 20x2.

| Particulars | Amount ($) |

| Finished-goods inventory, January 1 | $0 |

| Add: Cost of goods manufactured | $15,761,800 |

| Cost of goods available for sale | $15,761,800 |

| Less: Finished-goods inventory, December 31 | $351,500 |

| Unadjusted cost of goods sold | $15,410,300 |

| Less: Over applied overhead | $101,000 |

| Cost of goods sold | $15,309,300 |

Table (5)

Thus, the amount of cost of goods sold is $15,309,300.

7.

Explain whether it would be appropriate to include selling and administrative expenses in either manufacturing overhead or cost of goods sold.

Explanation of Solution

Selling and administrative expenses are the operating expenses of the company. These costs are considered as the period cost rather than the product costs. Hence, these costs are unrelated to manufacturing overhead and cost of goods sold. Thus, it cannot be included.

Want to see more full solutions like this?

Chapter 3 Solutions

Loose-Leaf for Managerial Accounting: Creating Value in a Dynamic Business Environment

- Abbey Products Company is studying the results of applying factory overhead to production. The following data have been used: estimated factory overhead, 60,000; estimated materials costs, 50,000; estimated direct labor costs, 60,000; estimated direct labor hours, 10,000; estimated machine hours, 20,000; work in process at the beginning of the month, none. The actual factory overhead incurred for November was 80,000, and the production statistics on November 30 are as follows: Required: 1. Compute the predetermined rate, based on the following: a. Direct labor cost b. Direct labor hours c. Machine hours 2. Using each of the methods, compute the estimated total cost of each job at the end of the month. 3. Determine the under-or overapplied factory overhead, in total, at the end of the month under each of the methods. 4. Which method would you recommend? Why?arrow_forwardChannel Products Inc. uses the job order cost system of accounting. The following is a list of the jobs completed during March, showing the charges for materials issued to production and for direct labor. Assume that factory overhead is applied on the basis of direct labor costs and that the predetermined rate is 200%. Required: Compute the amount of overhead to be added to the cost of each job completed during the month. Compute the total cost of each job completed during the month. Compute the total cost of producing all the jobs finished during the month.arrow_forwardLuna Manufacturing Inc. completed Job 2525 on May 31, and there were no jobs in process in the plant. Prior to June 1, the predetermined overhead application rate for June was computed from the following data, based on an estimate of 5,000 direct labor hours: The factory has one production department and uses the direct labor hour method to apply factory overhead. Three jobs are started during the month, and postings are made daily to the job cost sheets from the materials requisitions and labor-time records. The following schedule shows the jobs and amounts posted to the job cost sheets: The factory overhead control account was debited during the month for actual factory overhead expenses of 27,000. On June 11, Job 2526 was completed and delivered to the customer using a mark-on percentage of 50% on manufacturing cost. On June 24, Job 2527 was completed and transferred to Finished Goods. On June 30, Job 2528 was still in process. Required: 1. Prepare job cost sheets for Jobs 2526, 2527, and 2528, including factory overhead applied when the job was completed or at the end of the month for partially completed jobs. 2. Prepare journal entries as of June 30 for the following: a. Applying factory overhead to production. b. Closing the applied factory overhead account. c. Closing the factory overhead account. d. Transferring the cost of the completed jobs to finished goods. e. Recording the cost of the sale and the sale of Job 2526.arrow_forward

- The cost accountant for River Rock Beverage Co. estimated that total factory overhead cost for the Blending Department for the coming fiscal year beginning February 1 would be 3,150,000, and total direct labor costs would be 1,800,000. During February, the actual direct labor cost totalled 160,000, and factory overhead cost incurred totaled 283,900. a. What is the predetermined factory overhead rate based on direct labor cost? b. Journalize the entry to apply factory overhead to production for February. c. What is the February 28 balance of the account Factory OverheadBlending Department? d. Does the balance in part (c) represent over- or underapplied factory overhead?arrow_forwardPotomac Automotive Co. manufactures engines that are made only on customers orders and to their specifications. During January, the company worked on Jobs 007, 008, 009, and 010. The following figures summarize the cost records for the month: Jobs 007 and 008 have been completed and delivered to the customer at a total selling price of 426,000, on account. Job 009 is finished but has not yet been delivered. Job 010 is still in process. There were no materials or work in process inventories at the beginning of the month. Material purchases were 115,000, and there were no indirect materials used during the month. Required: 1. Prepare a summary showing the total cost of each job completed during the month or in process at the end of the month. 2. Prepare the summary journal entries for the month to record the distribution of materials, labor, and overhead costs. 3. Determine the cost of the inventories of completed engines and engines in process at the end of the month. 4. Prepare the journal entries to record the completion of the jobs and the sale of the jobs. 5. Prepare a statement of cost of goods manufactured.arrow_forwardNutt Products manufactures screws and bolts made to customer specifications. During August, Nutt incurred the following manufacturing costs: direct materials, 28,019.00; direct labor, 15,276.75; and applied factory overhead, 9,854.50. The following data pertain to these costs: The overhead application rates are 4 per direct labor hour for Dept. 1 and 175% of direct labor cost for Dept. 2. Nutt had no beginning work in process for August. Job 8958, which cost 14,190.18 to manufacture, was completed in July and was sold on account in August for 19,000. The job cost sheet for this job is shown on page 103. Of the jobs begun in August, Job 8961 was completed and sold on account for 24,000, Jobs 8962 and 8964 were completed but not sold, and Job 8963 was still in process. As cost accountant for this company, you have been asked to prepare job cost sheets for each of the four jobs started in August. Review the printed worksheet called JOB that follows these requirements.arrow_forward

- OReilly Manufacturing Co.s cost of goods sold for the month ended July 31 was 345,000. The ending work in process inventory was 90% of the beginning work in process inventory. Factory overhead was 50% of the direct labor cost. No indirect materials were used during the period. Other information pertaining to OReillys inventories and production for July is as follows: Required: 1. Prepare a statement of cost of goods manufactured for the month of July. (Hint: Set up a statement of cost of goods manufactured, putting the given information in the appropriate spaces and solving for the unknown information. Start by using cost of goods sold to solve for the cost of goods manufactured.) 2. Prepare a schedule to compute the prime cost incurred during July. 3. Prepare a schedule to compute the conversion cost charged to Work in Process during July.arrow_forwardCycle Specialists manufactures goods on a job order basis. During the month of June, three jobs were started in process. (There was no work in process at the beginning of the month.) Jobs Sprinters and Trekkers were completed and sold, on account, during the month (selling prices: Sprinters, 22,000; Trekkers, 27,000); Job Roadsters was still in process at the end of June. The following data came from the job cost sheets for each job. The factory overhead includes a total of 1,200 of indirect materials and 900 of indirect labor. Prepare journal entries to record the following: a. Materials used. b. Factory wages and salaries earned. c. Factory Overhead transferred to Work in Process d. Jobs completed. e. Jobs sold.arrow_forwardOn August 1, Cairle Companys work-in-process inventory consisted of three jobs with the following costs: During August, four more jobs were started. Information on costs added to the seven jobs during the month is as follows: Before the end of August, Jobs 70, 72, 73, and 75 were completed. On August 31, Jobs 72 and 75 were sold. Required: 1. Calculate the predetermined overhead rate based on direct labor cost. 2. Calculate the ending balance for each job as of August 31. 3. Calculate the ending balance of Work in Process as of August 31. 4. Calculate the cost of goods sold for August. 5. Assuming that Cairle prices its jobs at cost plus 20 percent, calculate Cairles sales revenue for August.arrow_forward

- Terrills Transmissions uses a job order cost system. A partial list of the accounts being maintained by the company, with their balances as of November 1, follows: The following transactions were completed during November: a. Materials purchases on account during the month, 74,000. b. Materials requisitioned during the month: 1. Direct materials, 57,000. 2. Indirect materials, 11,000. c. Direct materials returned by factory to storeroom during the month, 1,100. d. Materials returned to vendors during the month prior to payment, 2,500. e. Payments to vendors during the month, 68,500. Required: 1. Prepare general journal entries for each of the transactions. 2. Post the general journal entries to T-accounts. 3. Balance the accounts and report the balances of November 30 for the following: a. Cash b. Materials c. Accounts Payablearrow_forwardLorrimer Company has a job-order cost system. The following debits (credits) appeared in the Work-in-Process account for the month of June. During the month of June, direct labor totaled 30,000 and 24,000 of overhead was applied to production. Finished Goods was debited 100,000 during June. Lorrimer Company applies overhead at a predetermined rate of 80% of direct labor cost. Job number 83, the only job still in process at the end of June, has been charged with manufacturing overhead of 3,400. What was the amount of direct materials charged to Job number 83? a. 3,400 b. 4,250 c. 8,350 d. 7,580arrow_forwardHigh-End Products Inc. uses a standard cost system in accounting for the cost of production of its only product, Swank. The standards for the production of one unit of Swank follow: Direct materials: 10 feet of Class at $.75 per foot and 3 feet of Chic at $1.00 per foot. Direct labor: 4 hours at $12.00 per hour. Factory overhead: applied at 150% of standard direct labor costs. There was no beginning inventory on hand at July 1. Following is a summary of costs and related data for the production of Swank during the following year ended June 30: 100,000 feet of Class were purchased at $.72 per foot. 30,000 feet of Chic were purchased at $1.05 per foot. 8,000 units of Swank were produced that required 78,000 feet of Class, 26,000 feet of Chic, and 31,000 hours of direct labor at $11.80 per hour. 6,000 units of product Swank were sold. On June 30, there are 22,000 feet of Class, 4,000 feet of Chic, and 2,000 completed units of Swank on hand. All purchases and transfers are “charged in” at standard. Required: Calculate the following, using the formulas on pages 421–422 and 424 and compute the materials variances for both Class and Chic: Materials quantity variance. Materials purchase price variance. Labor efficiency variance. Labor rate variance.arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,