Concept explainers

Videos

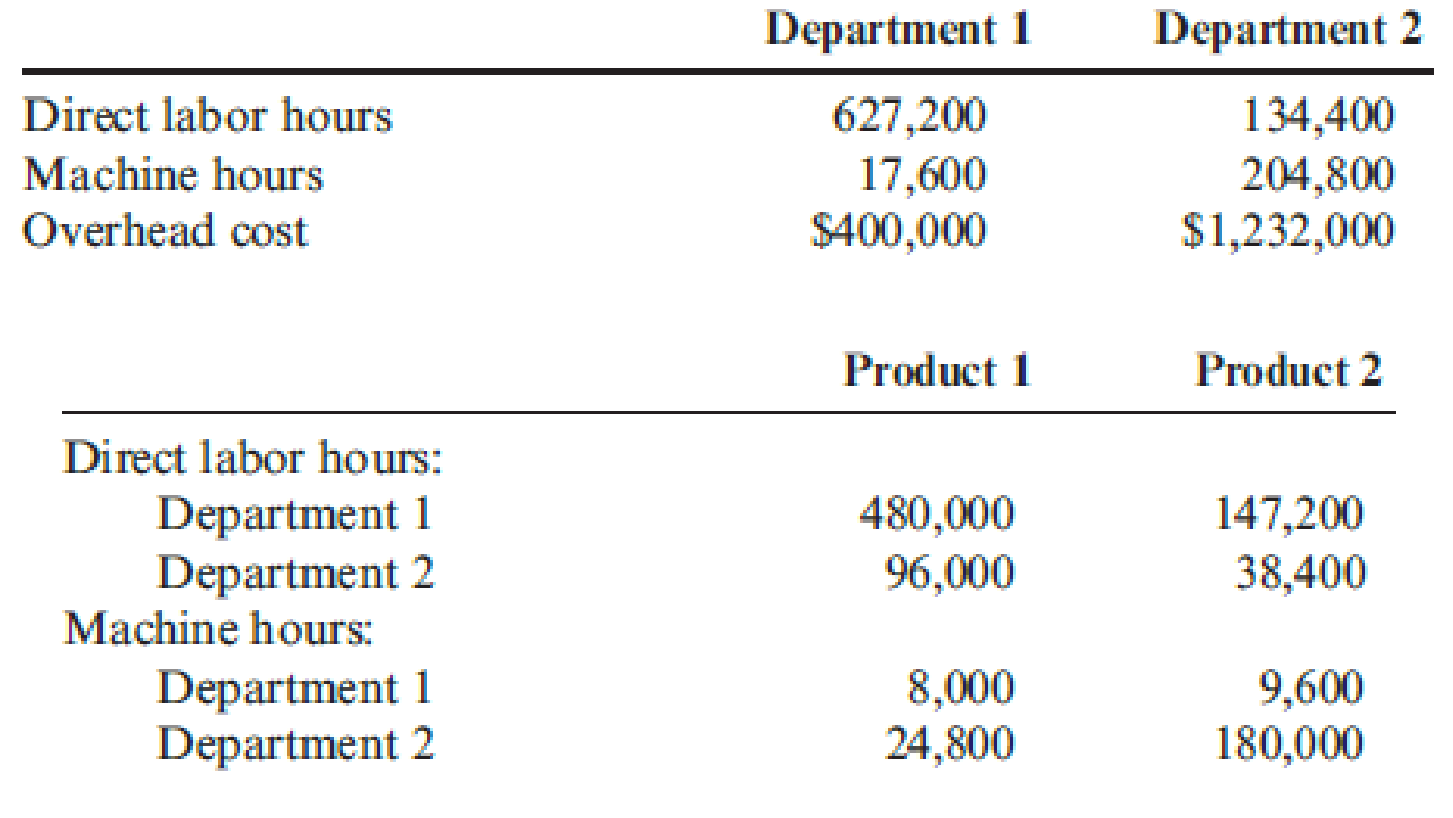

Primera Company produces two products and uses a predetermined

Actual results reported by department and product during the year are as follows:

Required:

- 1. Compute the plantwide predetermined overhead rate and calculate the overhead assigned to each product.

- 2. Calculate the predetermined departmental overhead rates and calculate the overhead assigned to each product.

- 3. Using departmental rates, compute the applied overhead for the year. What is the under- or overapplied overhead for the firm?

- 4. Prepare the

journal entry that disposes of the overhead variance calculated in Requirement 3, assuming it is not material in amount. What additional information would you need if the variance is material to make the appropriate journal entry?

1.

Determine the plantwide predetermined overhead rate and identify the overhead assigned to each products of Company P.

Explanation of Solution

Plantwide predetermined overhead rate: Plantwide overhead rate is the rate a company uses to allocate its manufacturing overhead costs to products and cost centres. Predetermined overhead rate is a measure used to allocate the estimated manufacturing overhead cost to the products or job orders during a particular period. This is generally evaluated at the beginning of each reporting period. The evaluation takes into account the estimated manufacturing overhead cost and the estimated allocation base which can be direct labor hours, direct labor in dollars, machine hours or direct materials.

Compute plantwide predetermined overhead rate:

Thus, the predetermined overhead rate for Company P is $2 per direct labor hour.

Ascertain the overhead assigned to each product:

Thus, the overhead assigned to product 1 and product 2 are $1,152,000 and $371,200 respectively.

2.

Compute the predetermined departmental overhead rates and ascertain the overhead assigned to each product.

Explanation of Solution

Compute predetermined departmental overhead rate:

Therefore, the predetermined departmental overhead rate of department 1 and department 2 is $0.60 per direct labor hour and $6.00 per machine hour respectively.

Ascertain the overhead assigned to each product:

Thus, the overhead assigned to product 1 and product 2 is $436,800 and $1,168,320 respectively.

3.

Calculate the applied overhead for the year and determine the under-or-overapplied overhead for the Company P.

Explanation of Solution

Applied overhead: The total overhead charged to actual production at any point of time is termed as applied overhead.

Overapplied overhead: The difference between actual and applied overheads is known as overhead variances. If the applied overhead is more than the actual overhead, then the variance is known as overapplied overhead.

Underapplied overhead: The difference between actual and applied overheads is known as overhead variances. If the applied overhead is less than the actual overhead, then the variance is known as underapplied overhead

Compute total applied overhead rate:

Therefore, the total applied overhead is $1,605,120.

Determine the under-or-overapplied overhead:

Since, the applied overhead is less than the actual overhead, the variance of $26,880 is underapplied overhead.

4.

Record the journal entry to dispose the overhead variance by assuming that it is not material in amount and identify the required additional information if the variance is material to make the appropriate journal entry.

Explanation of Solution

Prepare the journal entry to dispose the overhead variance:

| Date | Account title and explanation | Debit ($) | Credit ($) |

| Cost of goods sold | 26,880 | ||

| Overhead control | 26,880 | ||

| (To record the entry to dispose of the variance at the end of the year) |

Table (1)

Therefore, if the variance is material, we would need to know the balances of following Accounts

- Work-in-progress account

- Finished goods account

- Cost of goods sold account.

Want to see more full solutions like this?

Chapter 4 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Lansing. Inc., provided the following data for its two producing departments: Machine hours are used to assign the overhead of the Molding Department, and direct labor hours are used to assign the overhead of the Polishing Department. There are 30,000 units of Form A produced and sold and 50,000 of Form B. Required: 1. Calculate the overhead rates for each department. 2. Using departmental rates, assign overhead to live two products and calculate the overhead cost per unit. How does this compare with the plantwide rate unit cost, using direct labor hours? 3. What if the machine hours in Molding were 1,200 for Form A and 3,800 for Form B and the direct labor hours used in Polishing were 5,000 and 15,000, respectively? Calculate the overhead cost per unit for each product using departmental rates, and compare with the plantwide rate unit costs calculated in Requirement 2. What can you conclude from this outcome?arrow_forwardA manufacturing company has two service and two production departments. Building Maintenance and Factory Office are the service departments. The production departments are Assembly and Machining. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The building maintenance department services all departments of the company, and its costs are allocated using floor space occupied, while factory office costs are allocable to Assembly and Machining on the basis of direct labor hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardRockford Company has four departmental accounts: Building Maintenance, General Factory Overhead, Machining, and Assembly. The direct labor hour method is used to apply factory overhead to the jobs being worked on in Machining and Assembly. The company expects each production department to use 30,000 direct labor hours during the year. The estimated overhead rates for the year include the following: During the year, both Machining and Assembly used 28,000 direct labor hours. Factory overhead costs incurred during the year follow: In determining application rates at the beginning of the year, cost allocations were made as follows, using the sequential distribution method: Building Maintenance to: General Factory Overhead, 10%; Machining, 50%; Assembly, 40%. General factory overhead was distributed according to direct labor hours. Required: Determine the under- or overapplied overhead for each production department. (Hint: First you must distribute the service department costs.)arrow_forward

- Units of production data for the two departments of Atlantic Cable and Wire Company for July of the current fiscal year are as follows: Each department uses the weighted average method. For each department, assume that direct Materials are placed in process during production. a. Determine the number of whole units to be accounted for and to be assigned costs and the equivalent units of production for the Drawing Department. b. Determine the number of whole units to be accounted for and to be assigned costs and the equivalent units of production for the Winding Department.arrow_forwardJohn Sheng, a cost accountant at Starlet Company, is developing departmental factory overhead application rates for the companys Tooling and Fabricating departments. The budgeted overhead for each department and the data for one job are as follows: Using the departmental overhead application rates, total overhead applied to Job 231 in the Tooling and Fabricating departments will be: a. 225. b. 303. c. 537. d. 671.arrow_forwardSan Mateo Optics, Inc., specializes in manufacturing lenses for large telescopes and cameras used in space exploration. As the specifications for the lenses are determined by the customer and vary considerably, the company uses a job-order costing system. Manufacturing overhead is applied to jobs on the basis of direct labor hours, utilizing the absorption- or full-costing method. San Mateos predetermined overhead rates for 20x1 and 20x2 were based on the following estimates. Jim Cimino, San Mateos controller, would like to use variable (direct) costing for internal reporting purposes as he believes statements prepared using variable costing are more appropriate for making product decisions. In order to explain the benefits of variable costing to the other members of San Mateos management team, Cimino plans to convert the companys income statement from absorption costing to variable costing. He has gathered the following information for this purpose, along with a copy of San Mateos 20x1 and 20x2 comparative income statement. San Mateo Optics, Inc. Comparative Income Statement For the Years 20x1 and 20x2 San Mateos actual manufacturing data for the two years are as follows: The companys actual inventory balances were as follows: For both years, all administrative expenses were fixed, while a portion of the selling expenses resulting from an 8 percent commission on net sales was variable. San Mateo reports any over-or underapplied overhead as an adjustment to the cost of goods sold. Required: 1. For the year ended December 31, 20x2, prepare the revised income statement for San Mateo Optics, Inc., utilizing the variable-costing method. Be sure to include the contribution margin on the revised income statement. 2. Describe two advantages of using variable costing rather than absorption costing. (CMA adapted)arrow_forward

- Geneva, Inc., makes two products, X and Y, that require allocation of indirect manufacturing costs. The following data were compiled by the accountants before making any allocations: The total cost of purchasing and receiving parts used in manufacturing is 60,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were 48,000 and 12,000 for X and Y, respectively. If an activity-based system is used, what would be the allocated costs for each product?arrow_forwardCynthia Rogers, the cost accountant for Sanford Manufacturing, is preparing a management report that must include an allocation of overhead. The budgeted overhead for each department and the data for one job are as follows: Using the departmental overhead application rates, and allocating overhead on the basis of direct labor hours, overhead applied to Job 231 in the Tooling Department would be: a. 44.00. b. 197.50. c. 241.50. d. 501.00.arrow_forwardChester Company provided information on overhead for its three producing departments as follows: Overhead is applied on the basis of machine hours in Fabricating and direct labor hours in Assembly and in Finishing. Job #13-198 had total prime cost of 6,700. The job took 40 machine hours in Fabricating, 100 direct labor hours in Assembly, and 20 direct labor hours in Finishing. What is the total cost of Job# 13-198? a. 6,700.00 b. 1,523.20 c. 8,223.20 d. 7,383.20arrow_forward

- Abbey Products Company is studying the results of applying factory overhead to production. The following data have been used: estimated factory overhead, 60,000; estimated materials costs, 50,000; estimated direct labor costs, 60,000; estimated direct labor hours, 10,000; estimated machine hours, 20,000; work in process at the beginning of the month, none. The actual factory overhead incurred for November was 80,000, and the production statistics on November 30 are as follows: Required: 1. Compute the predetermined rate, based on the following: a. Direct labor cost b. Direct labor hours c. Machine hours 2. Using each of the methods, compute the estimated total cost of each job at the end of the month. 3. Determine the under-or overapplied factory overhead, in total, at the end of the month under each of the methods. 4. Which method would you recommend? Why?arrow_forwardPatterson Company produces wafers for integrated circuits. Data for the most recent year are provided: aCalculated using number of dies as the single unit-level driver. bCalculated by multiplying the consumption ratio of each product by the cost of each activity. Required: 1. Using the five most expensive activities, calculate the overhead cost assigned to each product. Assume that the costs of the other activities are assigned in proportion to the cost of the five activities. 2. Calculate the error relative to the fully specified ABC product cost and comment on the outcome. 3. What if activities 1, 2, 5, and 8 each had a cost of 650,000 and the remaining activities had a cost of 50,000? Calculate the cost assigned to Wafer A by a fully specified ABC system and then by an approximately relevant ABC approach. Comment on the implications for the approximately relevant approach.arrow_forwardUsing the same data found in Exercise 6.22, assume the company uses the FIFO method. Required: Prepare a schedule of equivalent units, and compute the unit cost for the month of December. Fordman Company has a product that passes through two processes: Grinding and Polishing. During December, the Grinding Department transferred 20,000 units to the Polishing Department. The cost of the units transferred into the second department was 40,000. Direct materials are added uniformly in the second process. Units are measured the same way in both departments. The second department (Polishing) had the following physical flow schedule for December: Costs in beginning work in process for the Polishing Department were direct materials, 5,000; conversion costs, 6,000; and transferred in, 8,000. Costs added during the month: direct materials, 32,000; conversion costs, 50,000; and transferred in, 40,000.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,