Concept explainers

Videos

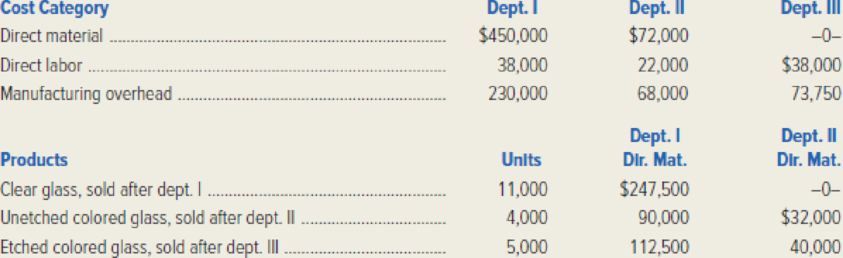

(Contributed by Roland Minch.) Glass Glow Company manufactures a variety of glass windows in its Egalton plant. In department I, clear glass sheets are produced, and some of these sheets are sold as finished goods. Other sheets made in department I have metallic oxides added in department II to form colored glass sheets. Some of these colored sheets are sold; others are moved to department III for etching and then are sold. The company uses operation costing.

Glass Glow Company’s production costs applied to products in May are given in the following table. There was no beginning or ending inventory of work in process for May.

Each sheet of glass requires the same steps within each operation.

Required: Compute each of the following amounts.

- 1. The conversion cost per unit in department I.

- 2. The conversion cost per unit in department II.

- 3. The cost of a clear glass sheet.

- 4. The cost of an unetched colored glass sheet.

- 5. The cost of an etched colored glass sheet.

Want to see the full answer?

Check out a sample textbook solution

Chapter 4 Solutions

Managerial Accounting: Creating Value in a Dynamic Business Environment

- Reducir, Inc., produces two different types of hydraulic cylinders. Reducir produces a major subassembly for the cylinders in the Cutting and Welding Department. Other parts and the subassembly are then assembled in the Assembly Department. The activities, expected costs, and drivers associated with these two manufacturing processes are given below. Note: In the assembly process, the materials-handling activity is a function of product characteristics rather than batch activity. Other overhead activities, their costs, and drivers are listed below. Other production information concerning the two hydraulic cylinders is also provided: Required: 1. Using a plantwide rate based on machine hours, calculate the total overhead cost assigned to each product and the unit overhead cost. 2. Using activity rates, calculate the total overhead cost assigned to each product and the unit overhead cost. Comment on the accuracy of the plantwide rate. 3. Calculate the global consumption ratios. 4. Calculate the consumption ratios for welding and materials handling (Assembly) and show that two drivers, welding hours and number of parts, can be used to achieve the same ABC product costs calculated in Requirement 2. Explain the value of this simplification. 5. Calculate the consumption ratios for inspection and engineering, and show that the drivers for these two activities also duplicate the ABC product costs calculated in Requirement 2.arrow_forwardHales Company produces a product that requires two processes. In the first process, a subassembly is produced (subassembly A). In the second process, this subassembly and a subassembly purchased from outside the company (subassembly B) are assembled to produce the final product. For simplicity, assume that the assembly of one final unit takes the same time as the production of subassembly A. Subassembly A is placed in a container and sent to an area called the subassembly stores (SB stores) area. A production Kanban is attached to this container. A second container, also with one subassembly, is located near the assembly line (called the withdrawal store). This container has attached to it a withdrawal Kanban. Required: 1. Explain how withdrawal and production Kanban cards are used to control the work flow between the two processes. How does this approach minimize inventories? 2. Explain how vendor Kanban cards can be used to control the flow of the purchased subassembly. What implications does this have for supplier relationships? What role, if any, do continuous replenishment and EDI play in this process?arrow_forwardBenson Pharmaceuticals uses a process-costing system to compute the unit costs of the over-the-counter cold remedies that it produces. It has three departments: mixing, encapsulating, and bottling. In mixing, the ingredients for the cold capsules are measured, sifted, and blended (with materials assumed to be uniformly added throughout the process). The mix is transferred out in gallon containers. The encapsulating department takes the powdered mix and places it in capsules (which are necessarily added at the beginning of the process). One gallon of powdered mix converts into 1,500 capsules. After the capsules are filled and polished, they are transferred to bottling, where they are placed in bottles that are then affixed with a safety seal, lid, and label. Each bottle receives 50 capsules. During March, the following results are available for the first two departments: Overhead in both departments is applied as a percentage of direct labor costs. In the mixing department, overhead is 200% of direct labor. In the encapsulating department, the overhead rate is 150% of direct labor. Required: 1. Prepare a production report for the mixing department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to two decimal places for the unit cost.) 2. Prepare a production report for the encapsulating department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to four decimal places for the unit cost.) 3. CONCEPTUAL CONNECTION Explain why the weighted average method is easier to use than FIFO. Explain when weighted average will give about the same results as FIFO.arrow_forward

- Healthway uses a process-costing system to compute the unit costs of the minerals that it produces. It has three departments: Mixing, Tableting, and Bottling. In Mixing, at the beginning of the process all materials are added and the ingredients for the minerals are measured, sifted, and blended together. The mix is transferred out in gallon containers. The Tableting Department takes the powdered mix and places it in capsules. One gallon of powdered mix converts to 1,600 capsules. After the capsules are filled and polished, they are transferred to Bottling where they are placed in bottles, which are then affixed with a safety seal and a lid and labeled. Each bottle receives 50 capsules. During July, the following results are available for the first two departments (direct materials are added at the beginning in both departments): Overhead in both departments is applied as a percentage of direct labor costs. In the Mixing Department, overhead is 200 percent of direct labor. In the Tableting Department, the overhead rate is 150 percent of direct labor. Required: 1. Prepare a production report for the Mixing Department using the weighted average method. Follow the five steps outlined in the chapter. Round unit cost to three decimal places. 2. Prepare a production report for the Tableting Department. Materials are added at the beginning of the process. Follow the five steps outlined in the chapter. Round unit cost to four decimal places.arrow_forwardGreystone Corporation manufactures windows for the home building industry. The window frames are produced in the Frame Division. The frames are then transferred to the Glass Division, where the glass and hardware are installed. The company’s best selling product is a three-by-four-foot, double-paned operable-windows. The standard cost of the window is detailed below: Frame Division Glass Division Direct Material P15 P30 Direct Labor 20 15 Variable overhead 30 30 Total 65 75 *Not including the transfer price for the frame. The Frame Division can also sell frames directly to custom home builders, who install the glass and hardware at P80. The markets for both frames and finished…arrow_forwardPBB Company manufactures high end product. Because of the high volume of this type of product, the company employs a process cost system using the weighted average method to determine costs. Product Parts are manufactured in the Molding Department and transferred to the assembly Department were they are partially assembled. After assembly, the product is sent to packaging department. Cost per unit data for the high end product has been completed through the Molding department. Annual cost and production figures for the assembly Department are presented below: Production Data Beg. Inventory 50% Complete as to Assembly materials; 20% complete 3,000 as to Conversion units 45,000 Transferred In during the year units 40,000 Transferred to Packaging Department units 4,000 Ending Inventory 80% complete units Cost Data: Transferred-In Materials Conversion Current Period P 1,240,800 P 97,020 P 236,470 Work in Process, beginning 82,200 6,660 11,930 Damage product are identified on inspection…arrow_forward

- Bristol Fabricators, Inc., produces air purifiers in batches. To manufacture a batch of the purifiers, Bristol Fabricators, Inc., must set up the machines and assembly line tooling. Setup costs are batch-level costs because they are associated with batches rather than individual units of products. A separate Setup Department is responsible for setting up machines and tooling for different models of the air purifiers. Setup overhead costs consist of some costs that are variable and some costs that are fixed with respect to the number of setup-hours. The following information pertains to June 2020: E (Click the icon to view the information for June 2020.) Calculate the production-volume variance for fixed overhead setup costs. (Round all intermediary calculations to two decimal places and your final answer to the nearest whole number.) O A. $2,478 unfavorable O B. $2,478 favorable i Data Table C. $363 favorable O D. $363 unfavorable Budget Amounts Actual Amounts Units produced and sold…arrow_forwardAlcoa Inc. is the world’s largest producer of aluminum products. One product that Alcoa manufactures is aluminum sheet products for the aerospace industry. The entire output of the Smelting Department is transferred to the Rolling Department. Part of the fully processedgoods from the Rolling Department are sold as rolled sheet, and the remainder of the goods are transferred to the Converting Department for further processing into sheared sheet. Prepare a diagram using T accounts showing the flow of costs from the processing department accounts into the finished goods accounts and then into the cost of goods sold account. The relevant accounts are as follows:Attachmentarrow_forwardMakani Handcraft is a manufacturer of picture frames for large retailers. Every picture frame passes through two departments: the assembly department and the finishing department. This problem focuses on the assembly department. The process-costing system at Makani has a single direct-cost category (direct materials) and a single indirect-cost category (conversion costs). Direct materials are added at the beginning of the process. Conversion costs are added evenly during the assembly department's process. Consider the following data for the assembly department in June 2020: Physical units (Frames) Direct materials Direct labour Work in progress (June 1) 80 $1,500 $150 Completed during June 500 Work in progress June 30 200 Total costs added during June $17,800 $11,500 Degree of completion is as follows: Work in progress (June 1): 100% 60% Work in progress June 30 100% 25% Required: Compute the costs assigned to products using two methods: 1. Weighted average method (WAM); | 2. First in…arrow_forward

- Oakland Precision Products (OPP) manufactures and sells a variety of scales for the kitchen and office. OPP sells primarily to kitchenware stores, discount stores, and so on. Two of the scales it produces for kitchen use are the Cook and Baker. The Cook is a basic food scale. The Baker has a greater capacity and special features that facilitate adjusting baking recipes for more or fewer people. The following information is available: Costs per unit Direct materials Direct labor Variable overhead Fixed overhead Total cost per unit Price Units produced and sold Cook $ 1.90 0.80 0.60 8.30 Baker $14.70 3.20 2.40 15.60 $11.60 $ 35.90 $15.60 $46.80 230,000 120,000 The average wage rate is $32 per hour. Variable overhead varies with the quantity of direct labor-hours. The plant has a capacity of 20,000 direct labor-hours, but current production uses only 17,750 direct labor-hours. Required: a. A nationwide kitchenware chain has offered to buy 30,000 Cook models and 15,000 Baker models if the…arrow_forwardGroFast Company manufactures a high-quality fertilizer, which is used primarily by commercial veg-etable growers. Two departments are involved in the production process. In the Mixing Department, various chemicals are entered into production. After processing, the Mixing Department transfers a chemical called Chemgro to the Finishing Department. There the product is completed, packaged, and shipped under the brand name Vegegro. Various chemicals --> Mixing Dept (Chemgro)-->Finishing Dept (Vegegro) ---> In the Mixing Department, the raw material is added at the beginning of the process. Labor and overhead are applied continuously throughout the process. All direct departmental overhead is traced to the departments, and plant overhead is allocated to the departments on the basis of direct-labor. The plant overhead rate for 20x2 is $.40 per direct-labor dollar. The following information relates to production during November 20x2 in the Mixing Department. a. Work in process,…arrow_forwardRich company produces a variety of stationery products. One product, sealing wax sticks,passes through two processes: blending and molding. The weighted average method is used toaccount for the cost of production. Two ingredients, paraffin and pigment are added at thebeginning of the process and heated and mixed for several hours. After blending, the resultingproduct is sent to the Molding department, where it is poured into molds and cooled. Thefollowing information relates to the blending process for November:a) Work in process, November 1, had 20,000 pounds, 20% complete with respect toconversion costs. Costs associated with partially completed units withParaffin $ 120,000Pigment $ 100,000Direct Labor $ 30,000Overhead applied $ 10,000b) Work in process, August 31, had 30,000 pounds, 70% complete with respect toconversion costs.c) Units completed and transferred out totaled 500,000 pounds. Costs added during themonth were:Paraffin $ 3,060,000Pigment $ 2,550,000Direct Labor $…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning