Videos

Make or Buy

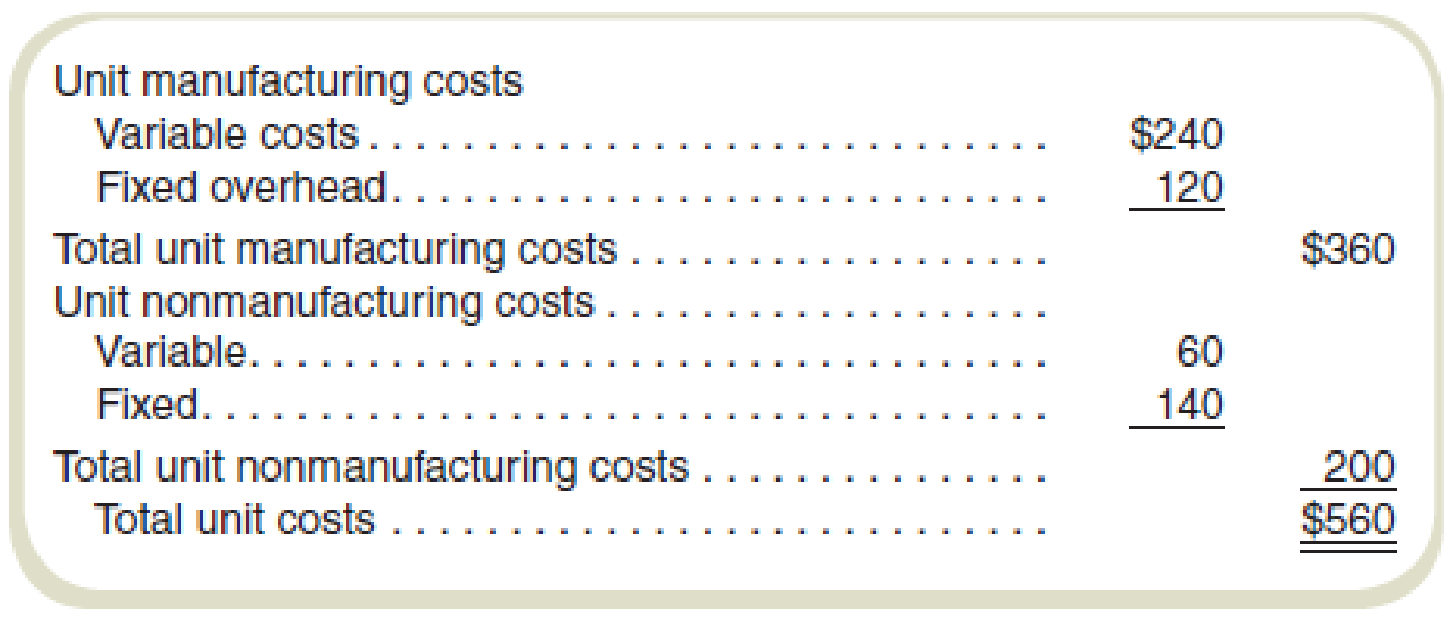

King City Specialty Bikes (KCSB) produces high-end bicycles. The costs to manufacture and market the bicycles at the company’s volume of 2,000 units per month are shown in the following table:

The company has the capacity to produce 2,000 units per month and always operates at full capacity. The bicycles sell for $600 per unit.

Required

- a. KCSB receives a proposal from an outside contractor who will assemble 800 of the 2,000 bicycles per month and ship them directly to KCSB’s customers as orders are received from KCSB’s sales force. KCSB would provide the materials for each bicycle, but the outside contractor would assemble, box, and ship the bicycles. The variable

manufacturing costs would be reduced by 40 percent for the 800 bicycles assembled by the outside contractor. KCSB’s fixed nonmanufacturing costs would be unaffected, but its variable nonmanufacturing costs would be cut by 60 percent for these 800 units produced by the outside contractor. KCSB’s plant would operate at 60 percent of its normal level, and total fixed manufacturing costs would be cut by 20 percent. What in-house unit cost should be compared with the quotation received from the outside contractor? Should the proposal be accepted for a price (that is, payment to the contractor) of $140 per unit? - b. Assume the same facts as in requirement (a) but assume that the idle facilities would be used to produce 80 specialty racing bicycles per month. These racing bicycles could be sold for $8,000 each, while the costs of production would be $5,600 per unit variable manufacturing cost. Variable marketing costs would be $200 per unit. Fixed nonmanufacturing and manufacturing costs would be unchanged whether the original 2,000 regular bicycles were manufactured or the mix of 1,200 regular bicycles plus 80 racing bicycles was produced. Considering this opportunity to use the freed-up space, what is the maximum purchase price per unit that KCSB should be willing to pay the outside contractor to assemble regular bicycles? Should the contractor’s proposal of $140 per unit be accepted?

a.

Calculate the in-house unit cost that should be compared with the quotation received from the outside contractor. Recommend Company K whether it should accept the offer or not.

Answer to Problem 58P

The cost that should be compared with the supplier’s proposal is $192. Yes, Company K should accept the offer.

Explanation of Solution

Acceptance of the offer:

An offer should be accepted when the profit after accepting the offer will increase the profitability of the company. An offer should be accepted in the scenario when the cost of the product is reduced after accepting the offer.

Calculate the cost that should be compared to the supplier’s proposal:

Thus, the cost that should be compared with the supplier’s proposal is $192.

Working note 1:

Calculate the cost of in-house production:

| Particulars |

Number of bicycles (a) |

Per unit cost (b) |

Total cost |

| Variable costs: | |||

| Manufacturing costs | 2,000 | $240 | $480,000 |

| Non-manufacturing costs | 2,000 | $60 | $120,000 |

| Total variable costs(a) | $300 | $600,000 | |

| Fixed costs: | |||

| Manufacturing costs | 2,000 | $120 | $240,000 |

| Non-manufacturing costs | 2,000 | $140 | $280,000 |

| Total fixed costs(b) | 2,000 | $260 | $520,000 |

| Total costs | $1,120,000 |

Table: (1)

Working note 2:

Calculate the cost of the contract:

| Particulars |

Number of bicycles (a) |

Per unit cost (b) |

Total cost |

| Variable costs: | |||

| In-house assembly | 1,200 | $300 | $360,000 |

| Outside contract | 800 | $168(3) | $134,400 |

| Total variable costs(a) | $468 | $494,400 | |

| Fixed costs: | |||

| Manufacturing costs (80% of $240,000) | $192,000 | ||

| Non-manufacturing costs | $280,000 | ||

| Total fixed costs(b) | $472,000 | ||

| Total costs | $966,400 |

Table: (2)

Working note 3:

Calculate the in-house assembly cost per unit:

Recommend Company K should accept the offer or not.

The total cost without accepting the offer is $1,120,000, and the total cost after accepting the offer is $966,400. Company K is saving $153,600

The supplier is offering a price of $14 per unit. The management of Company K should accept the offer because it is saving $192 and only paying $140 per unit.

Thus, Company K should accept the offer.

b.

Calculate the maximum amount that the Company K should pay to the outside contractor. Suggest whether the management should accept the offer not.

Answer to Problem 58P

Company K should accept the offer because the profit is increased by $169,600 when it accepts the offer.

Explanation of Solution

Acceptance of the offer:

An offer should be accepted when the profit after accepting the offer will increase the profitability of the company. An offer should be accepted in the scenario when the cost of the product is reduced after accepting the offer.

| Particulars |

Status quo (a) |

Alternate proposal: assemble 80 units (b) |

Difference |

| Revenue: | |||

| Regular bicycle (5) | $1,200,000 | $1,200,000 | No change |

| Racing bicycle (5) | $640,000 | $640,000 higher | |

| Total revenue(a) | $1,200,000 | $1,840,000 | $640,000 higher |

| Variable costs: | |||

| Regular cycle (variable costs) (4) | $600,000 | $494,400 | $105,600 lower |

| Racing bicycle (manufacturing)(4) | $112,000 | $112,000 higher | |

| Racing bicycle (marketing) (4) | $448,000 | $448,000 higher | |

| Supplier payment | $16,000 | $16,000 higher | |

| Total variable costs(b) | $600,000 | $1,070,400 | $470,400 higher |

| Fixed costs: | |||

| Total fixed costs [c] | $520,000 | $520,000 | No change |

| Total costs | $1,120,000 | $1,590,400 | $470,400 higher |

| Operating profit | $80,000 | $249,600 | $169,600 higher |

Table: (3)

Thus, Company K should accept the offer because the profit is increased by $169,600 when it accepts the offer.

Working note 4:

| Particulars |

Units (a) |

Cost per unit (b) |

Amount |

| Variable costs regular bicycle | $2,000 | $300 | $600,000 |

| Supplier payment | $800 | $140 | $112,000 |

| Racing bicycle (manufacturing) | $80 | $5,600 | $448,000 |

| Racing bicycle (marketing) | $80 | $200 | $16,000 |

Table: (4)

Working note 5:

Calculate the revenue:

| Particulars | Units | Price per unit | Amount |

| Regular cycle | 2000 | $600 | $1,200,000 |

| Racing cycle | 80 | $8,000 | $640,000 |

Table: (5)

Want to see more full solutions like this?

Chapter 4 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Power Corp. makes 2 products: blades for table saws and blades for handsaws. Each product passes through the sharpening machine area, which is the chief constraint during production. Handsaw blades take 15 minutes on the sharpening machine and have a contribution margin per blade of $15. Table saw blades take 20 minutes on the sharpening machine and have a contribution margin per blade of $35. If it is assumed that Power Corp. has 5,000 hours available on the sharpening machine to service a minimum demand for each product of 4,000 units, how much will profits increase if 200 more hours of machine time can be obtained?arrow_forwardPower Corp. makes 2 products: blades for table saws and blades for handsaws. Each product passes through the sharpening machine area, which is the chief constraint during production. Handsaw blades take 15 minutes on the sharpening machine and have a contribution margin per blade of $15. Table saw blades take 20 minutes on the sharpening machine and have a contribution margin per blade of $35. If it is assumed that Power Corp. has 5,000 hours available on the sharpening machine to service a minimum demand for each product of 4,000 units, how many of each product should be made?arrow_forwardRolertyme Company manufactures roller skates. With the exception of the rollers, all parts of the skates are produced internally. Neeta Booth, president of Rolertyme, has decided to make the rollers instead of buying them from external suppliers. The company needs 100,000 sets per year (currently it pays 1.90 per set of rollers). The rollers can be produced using an available area within the plant. However, equipment for production of the rollers would need to be leased (30,000 per year lease payment). Additionally, it would cost 0.50 per machine hour for power, oil, and other operating expenses. The equipment will provide 60,000 machine hours per year. Direct material costs will average 0.75 per set, and direct labor will average 0.25 per set. Since only one type of roller would be produced, no additional demands would be made on the setup activity. Other overhead activities (besides machining and setups), however, would be affected. The companys cost management system provides the following information about the current status of the overhead activities that would be affected. (The supply and demand figures do not include the effect of roller production on these activities.) The lumpy quantity indicates how much capacity must be purchased should any expansion of activity supply be needed. The purchase price is the cost of acquiring the capacity represented by the lumpy quantity. This price also represents the cost of current spending on existing activity supply (for each block of activity). Production of rollers would place the following demands on the overhead activities: Producing the rollers also means that the purchase of outside rollers will cease. Thus, purchase orders associated with the outside acquisition of rollers will drop by 5,000. Similarly, the moves for the handling of incoming orders will decrease by 200. The company has not inspected the rollers purchased from outside suppliers. Required: 1. Classify all resources associated with the production of rollers as flexible resources and committed resources. Label each committed resource as a short- or long-term commitment. How should we describe the cost behavior of these short- and long-term resource commitments? Explain. 2. Calculate the total annual resource spending (for all activities except for setups) that the company will incur after production of the rollers begins. Break this cost into fixed and variable activity costs. In calculating these figures, assume that the company will spend no more than necessary. What is the effect on resource spending caused by production of the rollers? 3. Refer to Requirement 2. For each activity, break down the cost of activity supplied into the cost of activity output and the cost of unused activity.arrow_forward

- Dimitri Designs has capacity to produce 30,000 desk chairs per year and is currently selling all 30,000 for $240 each. Country Enterprises has approached Dimitri to buy 800 chairs for $210 each. Dimitris normal variable cost is $165 per chair, including $50 per unit in direct labor per chair. Dimitri can produce the special order on an overtime shift, which means that direct labor would be paid overtime at 150% of the normal pay rate. The annual fixed costs will be unaffected by the special order and the contract will not disrupt any of Dimitris other operations. What will be the impact on profits of accepting the order?arrow_forwardRemarkable Enterprises requires four units of part A for every unit of Al that it produces. Currently, part A is made by Remarkable, with these per-unit costs in a month when 4,000 units were produced: Variable manufacturing overhead is applied at $1.60 per unit. The other $0.50 of overhead consists of allocated fixed costs. Remarkable will need 8,000 units of part A for the next years production. Altoona Corporation has offered to supply 8,000 units of part A at a price of $8.00 per unit. If Remarkable accepts the offer, all of the variable costs and $2,000 of the fixed costs will be avoided. Should Remarkable accept the offer from Altoona Corporation?arrow_forwardGent Designs requires three units of part A for every unit of Al that it produces. Currently, part A is made by Gent, with these per-unit costs in a month when 4.000 units were produced: Variable manufacturing overhead is applied at $1.00 per unit. The other $0.30 of overhead consists of allocated fixed costs. Gent will need 6,000 units of part A for the next years production. Cory Corporation has offered to supply 6,000 units of part A at a price of $7.00 per unit. It Gent accepts the offer, all of the variable costs and $1,200 of the fixed costs will be avoided. Should Gent Designs accept the offer from Cory Corporation?arrow_forward

- Jansen Crafters has the capacity to produce 50,000 oak shelves per year and is currently selling 44,000 shelves for $32 each. Cutrate Furniture approached Jansen about buying 1,200 shelves for bookcases it is building and is willing to pay $26 for each shelf. No packaging will be required for the bulk order. Jansen usually packages shelves for Home Depot at a price of $1.50 per shell. The $1.50 per-shelf cost is included in the unit variable cost of $27, with annual fixed costs of $320.000. However, the $130 packaging cost will not apply in this case. The fixed costs will be unaffected by the special order and the company has the capacity to accept the order. Based on this information, what would be the profit if Jansen accepts the special order? A. Profits will decrease by $1,200. B. Profits will increase by $31,200. C. Profits will increase by $600. D. Profits will increase by $7,200.arrow_forwardOlin Company manufactures and distributes carpentry tools. Production of the tools is in the mature portion of the product life cycle. Olin has a sales force of 20. Salespeople are paid a commission of 7 percent of sales, plus expenses of 35 per day for days spent on the road away from home, plus 0.50 per mile. They deliver products in addition to making the sales, and each salesperson is required to own a truck suitable for making deliveries. For the coming quarter, Olin estimates the following: On average, a salesperson travels 6,000 miles per quarter and spends 38 days on the road. The fixed marketing and administrative expenses total 400,000 per quarter. Required: 1. Prepare an income statement for Olin Company for the next quarter. 2. Suppose that a large hardware chain, MegaHardware, Inc., wants Olin Company to produce its new SuperTool line. This would require Olin Company to sell 80 percent of total output to the chain. The tools will be imprinted with the SuperTool brand, requiring Olin to purchase new equipment, use somewhat different materials, and reconfigure the production line. Olins industrial engineers estimate that cost of goods sold for the SuperTool line would increase by 15 percent. No sales commission would be incurred, and MegaHardware would link Olin to its EDI system. This would require an annual cost of 100,000 on the part of Olin. MegaHardware would pay shipping. As a result, the sales force would shrink by 80 percent. Should Olin accept MegaHardwares offer? Support your answer with appropriate calculations.arrow_forwardIngles Corporation is a manufacturer of tables sold to schools, restaurants, hotels, and other institutions. The table tops are manufactured by Ingles, but the table legs are purchased from an outside supplier. The Assembly Department takes a manufactured table top and attaches the four purchased table legs. It takes 16 minutes of labor to assemble a table. The company follows a policy of producing enough tables to ensure that 40 percent of next months sales are in the finished goods inventory. Ingles also purchases sufficient materials to ensure that materials inventory is 60 percent of the following months scheduled production. Ingless sales budget in units for the next quarter is as follows: Ingless ending inventories in units for July 31 are as follows: Required: 1. Calculate the number of tables to be produced during August. 2. Disregarding your response to Requirement 1, assume the required production units for August and September are 2,100 and 1,900, respectively, and the July 31 materials inventory is 4,000 units. Compute the number of table legs to be purchased in August. 3. Assume that Ingles Corporation will produce 2,340 units in September. How many employees will be required for the Assembly Department in September? (Fractional employees are acceptable since employees can be hired on a part-time basis. Assume a 40-hour week and a 4-week month.) (CMA adapted)arrow_forward

- The Calhoun Textile Mill is in the process of deciding on a production schedule. It wishes to know how to weave the various fabrics it will produce during the coming quarter. The sales department has continued orders for each of the 15 fabrics produced by Calhoun. These demands are given in the following table. Also given in this table is the variable cost for each fabric. The mill operates continuously during the quarter: 13 weeks, 7 days a week, and 24 hours a day. There are two types of looms: dobbie and regular. Dobbie looms can be used to make all fabrics and are the only looms that can weave certain fabrics, such as plaids. The rate of production for each fabric on each type of loom is also given in the table. Note that if the production rate is zero, the fabric cannot be woven on that type of loom. Also, if a fabric can be woven on each type of loom, then the production rates are equal. Calhoun has 90 regular looms and 15 dobbie looms. For this problem, assume that the time requirement to change over a loom from one fabric to another is negligible. Management would like to know how to allocate the looms to the fabrics and which fabrics to buy on the market so as to minimize the cost of meeting demand.arrow_forwardAndalus Furniture Company has two manufacturing plants, one at Aynor and another at Spartanburg. The cost in dollars of producing a kitchen chair at each of the two plants is given here. The cost of producing Q1 chairs at Aynor is: 75Q1+5Q12+100 and the cost of producing Q2 kitchen chairs at Spartanburg is: 25Q2+2.5Q22+150. Andalus needs to manufacture a total of 40 kitchen chairs to meet an order just received. How many chairs should be made at Aynor, and how many should be made at Spartanburg in order to minimize total production cost?arrow_forwardHawkins Manufacturing Company produces connecting rods for 4- and 6-cylindcr automobile engines using the same production line. The cost required to set up the production line to produce the 4-cylinder connecting rods is 2,000, and the cost required to set up the production line for the 6-cylinder connecting rods is 3,500. Manufacturing costs are 15 for each 4-cylinder connecting rod and 18 for each 6-cylinder connecting rod. There is no production on weekends, so on Friday the line is disassembled and cleaned. On Monday, the line must be set up to run whichever product will be produced that week. Once the line has been set up, the weekly production capacities are 6,000 6-cylinder connecting rods and 8,000 4-cylinder connecting rods. Let x4 = the number of 4-cylinder connecting rods produced next week x6 = the number of 6-cylinder connecting rods produced next week s4 = 1 if the production line is set up to produce the 4-cylinder connecting rods; 0 if otherwise s6 = 1 if the production line is set up to produce the 6-cylinder connecting rods; 0 if otherwise a. Using the decision variables x4 and s4, write a constraint that sets next weeks maximum production of the 4-cylinder connecting rods to either 0 or 8,000 units. b. Using the decision variables x6 and s6, write a constraint that sets next weeks maximum production of the 6-cylinder connecting rods to either 0 or 6,000 units. c. Write a constraint that requires that production be set up for exactly one of the two rods. d. Write the cost function to be minimized.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT