Concept explainers

Videos

Support department cost allocation —comparison

Refer to your answers to Exercises 7-9. Compare the total support department costs allocated to each production department under each cost allocation method. Which production department is allocated the most support department costs (a) under the direct method, (b) under the sequential method, and (c) under the reciprocal services method?

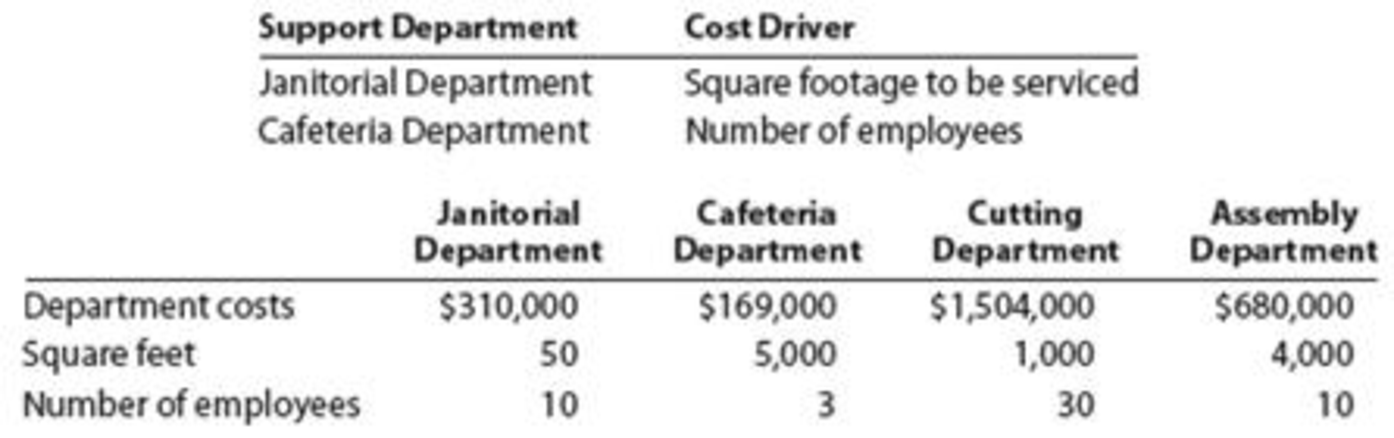

EX 19-7 Support department cost allocation—direct method

Becker Tabletops has two support departments (Janitorial and Cafeteria) and two production departments (Cutting and Assembly). Relevant details for these departments are as follows:

Allocate the support department costs to the production departments using the direct method.

EX 19-8 Support department cost allocation—sequential method

Refer to the information provided for Becker Tabletops in Exercise 7. Allocate the support department costs to the production departments using the sequential method. Allocate the support department with the highest department cost first.

EX 19-9 Support department cost allocation —reciprocal services method

Refer to the information provided for Becker Tabletops in Exercise 7. Allocate the support department costs to the production departments using the reciprocal services method.

Identify the production department with greater department cost allocation under each method.

Explanation of Solution

Cost allocation:

The cost allocation refers to the process of allocating the costs associated with the production of the products mainly indirectly and are generally ignored. The main objective of cost allocation is to ensure proper pricing of the products. This can be done by several methods.

(a) The direct method:

Compute the costs allocated from the support departments.

Cutting Department Total Cost:

Assembly Department Total Cost:

Under the direct method the Assembly department has been allocated the greater costs from the support departments.

Working Notes:

Janitorial Department Cost Allocation:

Compute the allocation of costs from Janitorial Department to Cutting Department:

The costs from Janitorial Department that should be allocated to Cutting department is $62,000.

Compute the allocation of costs from Janitorial Department to Assembly Department:

The cost allocated from Janitorial Department to Assembly department is $248,000.

Cafeteria Department Cost Allocation:

Compute the allocation of costs from Cafeteria Department to Cutting Department:

The costs allocated from Cafeteria Department to Cutting department is $126,750.

Compute the allocation of costs from Cafeteria Department to Assembly Department:

The cost allocated from Cafeteria Department to Assembly department is $42,250.

(b) The sequential method:

Compute the costs allocated from the support departments.

Cutting Department Total Cost:

Assembly Department Total Cost:

Under the sequential method the Cutting department has been allocated the greater costs from the support departments.

Working Notes:

Janitorial Department Cost Allocation:

Compute the allocation of costs from Janitorial Department to Cafeteria Department:

The cost allocated from Janitorial Department to Cafeteria department is $155,000.

Compute the allocation of costs from Janitorial Department to Cutting Department:

The costs allocated from Janitorial Department to Cutting department is $31,000.

Compute the allocation of costs from Janitorial Department to Assembly Department:

The cost allocated from Janitorial Department to Assembly department is $124,000.

Cafeteria Department Total Cost:

The total costs of Cafeteria Department are $324,000.

Compute the allocation of costs from Cafeteria Department to Cutting Department:

The costs allocated from Cafeteria Department to Cutting department is $243,000.

Compute the allocation of costs from Cafeteria Department to Assembly Department:

The cost allocated from Cafeteria Department to Assembly department is $81,000.

(c) The reciprocal services method:

Compute the costs allocated from the support departments.

Cutting Department Total Cost:

Assembly Department Total Cost:

Under the reciprocal services method the Cutting department has been allocated the greater costs from the support departments.

Working Notes:

Janitorial Department Cost to be allocated:

The total Janitorial Department costs include 20% of the Cafeteria department costs as,

Therefore, the Cafeteria Department cost is,

Cafeteria Department Cost to be allocated:

The total Cafeteria Department costs include 50% of the Janitorial department costs as,

Therefore, the Cafeteria Department cost is,

Substitute the equation for J into the C equation:

Substitute the value of C into the J equation:

Janitorial Department Cost Allocation:

Compute the allocation of costs from Janitorial Department to Cafeteria Department:

The cost allocated from Janitorial Department to Cafeteria Department is $191,000.

Compute the allocation of costs from Janitorial Department to Cutting Department:

The cost allocated from Janitorial Department to Cutting Department is $38,200.

Compute the allocation of costs from Janitorial Department to Assembly Department:

The cost allocated from Janitorial Department to Assembly Department is $152,800.

Cafeteria Department Cost Allocation:

Compute the allocation of costs from Cafeteria Department to Janitorial Department:

The cost allocated from Cafeteria Department to Janitorial Department is $72,000.

Compute the allocation of costs from Cafeteria Department to Cutting Department:

The cost allocated from Cafeteria Department to Cutting Department is $216,000.

Compute the allocation of costs from Cafeteria Department to Assembly Department:

The cost allocated from Cafeteria Department to Assembly Department is $72,000.

Want to see more full solutions like this?

Chapter 5 Solutions

MANAGERIAL ACCOUNTING (LL) W/ CENGAGENO

- (Appendix 4B) Sequential Method of Support Department Cost Allocation Refer to Exercise 4-51 for data. Now assume that Stevenson uses the sequential method to allocate support department costs to the operating divisions. General Factory is allocated first in the sequential method for the company. Required: 1. Calculate the allocation ratios for Power and General Factory. (Note: Carry these calculations out to four decimal places.) 2. Allocate the support service costs to the operating divisions. (Note: Round all amounts to the nearest dollar.) 3. Assume divisional overhead rates are based on direct labor hours. Calculate the overhead rate for the Battery Division and for the Small Motors Division. (Note: Round overhead rates to the nearest cent.)arrow_forwardRefer to Cornerstone Exercise 7.3. Now assume that Valron Company uses the sequential method to allocate support department costs. The support departments are ranked in order of highest cost to lowest cost. Required: 1. Calculate the allocation ratios (rounded to four significant digits) for the four departments using the sequential method. 2. Using the sequential method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments. (Round all allocated costs to the nearest dollar.) 3. What if the allocation ratios in Requirement 1 were rounded to six significant digits rather than four? How would that affect any rounding error in the allocation of costs?arrow_forwardRefer to the data in Exercise 7.22. The support departments are ranked in order of highest cost to lowest cost. Required: 1. Allocate the costs of the support departments using the sequential method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.) 2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)arrow_forward

- Distribution of service department costs to production departments using the sequential distribution method Required: Using the information in P4-6, prepare a schedule showing the distribution of the service departments’ expenses using the sequential distribution method in the order of number of other departments served. (Hint: First distribute the service department that services the greater number of other departments.)arrow_forwardRefer to Cornerstone Exercise 7.3. Now assume that Valron Company uses the reciprocal method to allocate support department costs. Required: 1. Calculate the allocation ratios (rounded to four significant digits) for the four departments using the reciprocal method. 2. Develop a simultaneous equations system of total costs for the support departments. Solve for the total reciprocated costs of each support department. (Round reciprocated total costs to the nearest dollar.) 3. Using the reciprocal method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments. (Round all allocated costs to the nearest dollar.) 4. What if the square footage in Fabricating were 13,300 and the square footage in Assembly were 5,700. How would that affect the allocation of support department costs?arrow_forwardRefer to the data in Exercise 7.22. The company has decided to simplify its method of allocating support service costs by switching to the direct method. Required: 1. Allocate the costs of the support departments to the producing departments using the direct method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.) 2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)arrow_forward

- Refer to the data in Exercise 7.20. The company has decided to use the sequential method of allocation instead of the direct method. The support departments are ranked in order of highest cost to lowest cost. Required: 1. Allocate the overhead costs to the producing departments using the sequential method. (Take allocation ratios out to four significant digits. Round allocated costs to the nearest dollar.) 2. Using machine hours, compute departmental overhead rates. (Round the overhead rates to the nearest cent.)arrow_forwardActivity cost pools, activity rates, and product costs using activity-based costing Caldwell Home Appliances Inc. is estimating the activity cost associated with producing ovens and refrigerators. The indirect labor can be traced into four separate activity pools, based on time records provided by the employees. The budgeted activity cost and activity-base information are provided as follows: The estimated activity-base usage and unit information for two product lines was determined as follows: A. Determine the activity rate for each activity cost pool. B. Determine the activity-based cost per unit of each product.arrow_forwardActivity-based department rate product costing and product cost distortions Big Sound Inc. manufactures two products: receivers and loudspeakers. The factory overhead incurred is as follows: The activity base associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: The activity-base usage quantities and units produced for the two products follow: Instructions Determine the factory overhead rates under the multiple production department rate method. Assume that indirect labor is associated with the production departments, so that the total factory overhead is 420,000 and 294,000 for the Subassembly and Final Assembly departments, respectively. Determine the total and per-unit factory overhead costs allocated to each product, using the multiple production department overhead rates in (1). Determine the activity rates, assuming that the indirect labor is associated with activities rather than with the production departments. Determine the total and per-unit cost assigned to each product under activity-based costing. Explain the difference in the per-unit overhead allocated to each product under the multiple production department factory overhead rate and activity-based costing methods. production department factory overhead rate and activity-based costing methods.arrow_forward

- Support department cost allocation Blue Mountain Masterpieces produces pictures, paintings, and other home decor. The Printing and Framing production departments are supported by the Janitorial and Security departments. Janitorial costs are allocated to the production departments based on square feet, and security costs are allocated based on asset value. Information about these departments is detailed in the following table: Management has experimented with different support department cost allocation methods in the past. The different allocation methods did not yield large differences of cost allocation to the production departments. Instructions 1. Determine which support department cost allocation method Blue Mountain Masterpieces would most likely use to allocate its support department costs to the production departments. 2. Determine the total costs allocated from each support department to each production department using the method you determined in part (1). 3. Without doing calculations, consider and answer the following: If Blue Mountain Masterpieces decided to use square feet instead of asset value as the cost driver for security services, how would this change the allocation of Security Department costs?arrow_forwardFIFO Method, Single Department Analysis, One Cost Category Refer to the data in Problem 6.33. Required: Prepare a cost of production report for the Fabrication Department for December using the FIFO method of costing.arrow_forwardOverhead Rates, Unit Costs Folsom Company manufactures specialty tools to customer order. There are three producing departments. Departmental information on budgeted overhead and various activity measures for the coming year is as follows: Currently, overhead is applied on the basis of machine hours using a plantwide rate. However, Janine, the controller, has been wondering whether it might be worthwhile to use departmental overhead rates. She has analyzed the overhead costs and drivers for the various departments and decided that Welding and Finishing should base their overhead rates on machine hours and that Assembly should base its overhead rate on direct labor hours. Janine has been asked to prepare bids for two jobs with the following information: The typical bid price includes a 35% markup over full manufacturing cost. Round all overhead rates to the nearest cent. Round all bid prices to the nearest dollar. Required: 1. Calculate a plantwide rate for Folsom Company based on machine hours. What is the bid price of each job using this rate? 2. Calculate departmental overhead rates for the producing departments. What is the bid price of each job using these rates?arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning