Videos

AKL Foundry manufactures metal components for different kinds of equipment used by the aerospace, commercial aircraft, medical equipment, and electronic industries. The company uses investment casting to produce the required components. Investment casting consists of creating, in wax, a replica of the final product and pouring a hard shell around it. After removing the wax, molten metal is poured into the resulting cavity. What remains after the shell is broken is the desired metal object ready to be put to its designated use.

Metal components pass through eight processes: gating, shell creating, foundry work, cutoff, grinding, finishing, welding, and strengthening. Gating creates the wax mold and clusters the wax pattern around a sprue (a hole through which the molten metal will be poured through the gates into the mold in the foundry process), which is joined and supported by gates (flow channels) to form a tree of patterns. In the shell-creating process, the wax molds are alternately dipped in a ceramic slurry and a fluidized bed of progressively coarser refractory grain until a sufficiently thick shell (or mold) completely encases the wax pattern. After drying, the mold is sent to the foundry process. Here, the wax is melted out of the mold, and the shell is fired, strengthened, and brought to the proper temperature. Molten metal is then poured into the dewaxed shell. Finally, the ceramic shell is removed, and the finished product is sent to the cutoff process, where the parts are separated from the tree by the use of a band saw. The parts are then sent to the grinding process, where the gates that allowed the molten metal to flow into the ceramic cavities are ground off using large abrasive grinders. In the finishing process, rough edges caused by the grinders are removed by small handheld pneumatic tools. Parts that are flawed at this point are sent to welding for corrective treatment. The last process uses heat to treat the parts to bring them to the desired strength.

In 20X1, the two partners who owned AKL Foundry decided to split up and divide the business. In dissolving their business relationship, they were faced with the problem of dividing the business assets equitably. Since the company had two plants—one in Arizona and one in New Mexico—a suggestion was made to split the business on the basis of geographic location. One partner would assume ownership of the plant in New Mexico, and the other would assume ownership of the plant in Arizona. However, this arrangement had one major complication: the amount of WIP inventory located in the Arizona plant.

The Arizona facilities had been in operation for more than a decade and were full of WIP. The New Mexico facility had been operational for only 2 years and had much smaller WIP inventories. The partner located in New Mexico argued that to disregard the unequal value of the WIP inventories would be grossly unfair.

Unfortunately, during the entire business history of AKL Foundry, WIP inventories had never been assigned any value. In computing the cost of goods sold each year, the company had followed the policy of adding

During 20X1, the Arizona plant had sales of $2,028,670. The cost of goods sold is itemized as follows:

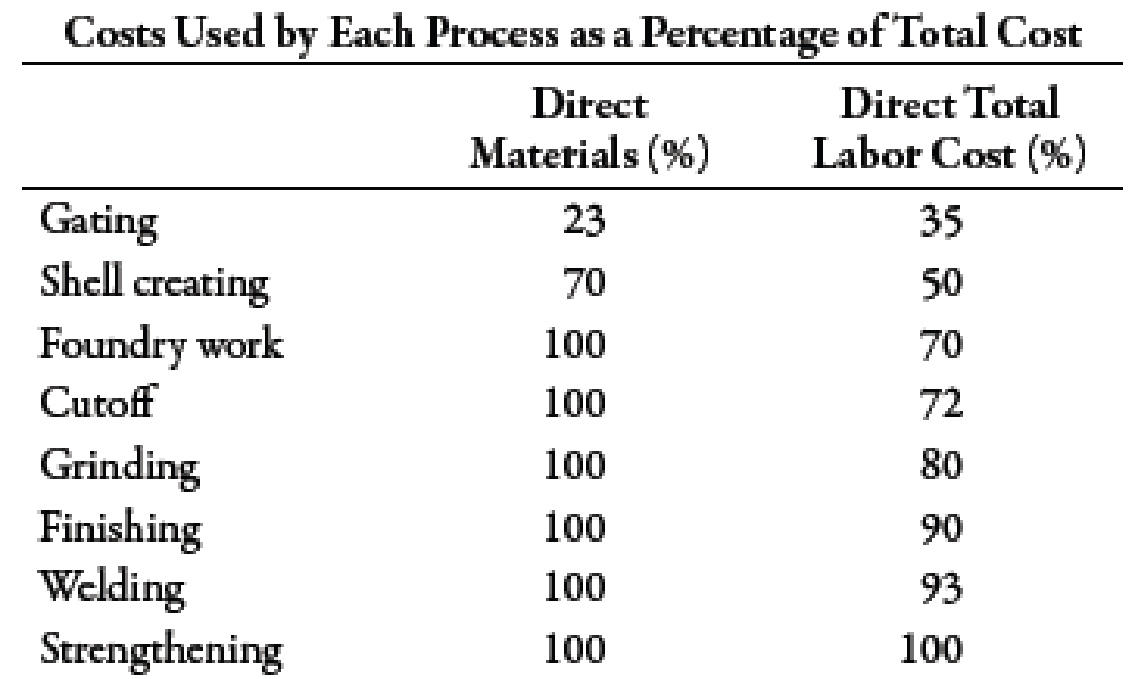

Upon request, the owners of AKL provided the following supplementary information (percentages are cumulative):

Gating had 10,000 units in BWIP, 60% complete. Assume that all materials are added at the beginning of each process. During the year, 50,000 units were completed and transferred out. The ending inventory had 11,000 unfinished units, 60% complete.

Required:

- 1. The partners of AKL want a reasonable estimate of the cost of WIP inventories. Using the gating department’s inventory as an example, prepare an estimate of the cost of the EWIP. What assumptions did you make? Did you use the FIFO or weighted average method? Why? (Note: Round unit cost to two decimal places.)

- 2. Assume that the shell-creating process has 8,000 units in BWIP, 20% complete. During the year, 50,000 units were completed and transferred out. (Note: All 50,000 units were sold; no other units were sold.) The EWIP inventory had 8,000 units, 30% complete. Compute the value of the shell-creating department’s EWIP. What additional assumptions had to be made?

1.

Provide an estimate of the ending WIP of gating process. Also, explain the method used to measure WIP and reason for such selection.

Explanation of Solution

Process Costing:

Process costing is a system in which an organization ascertains costs associated which specific processes undertaken within the company.

Step 1: Physical flow analysis:

| Particulars | Units |

| Units to account for: | |

| Units in beginning WIP | 10,000 |

| Add: Units started during the period1 | 51,000 |

| Units to account for | 61,000 |

| Units accounted for: | |

| Units completed and transferred | 50,000 |

| Add: Units in ending WIP | 11,000 |

| Units accounted for | 61,000 |

Table (1)

Step 2: Computation of equivalent units:

| Particulars | Material | Conversion |

| Units started and completed | 40,000 | 40,000 |

|

Equivalent units of beginning WIP | 4,000 | |

|

Equivalent units of ending WIP | 11,000 | 6,600 |

| Equivalent units | 51,000 | 50,600 |

Table (2)

Step 3: Computation of unit cost:

| Particulars | Material ($) | Conversion ($) |

| Material cost | 86,940 | |

| Labor cost | 185,605 | |

| Overhead cost | 225,231 | |

| Total cost | 86,940 | 410,836 |

| Equivalent units | 51,000 | 50,600 |

| Unit cost | 1.70 | 8.12 |

Table (3)

Step 4: Valuation of ending inventory:

| Particulars | Amount ($) |

| Equivalent units of material | 18,700 |

| Equivalent units for conversion | 53,592 |

| Total value | 72,292 |

Table (4)

FIFO method has been used since, costs associated with beginning inventory is to be removed from the equivalent units so that current period’s cost can be correctly allocated amongst the equivalent units for computation of unit cost.

Working Notes:

1. Computation of units started during the period:

2.

Provide an estimate of the ending WIP of shell-creating process.

Explanation of Solution

Step 1: Physical flow analysis:

| Particulars | Units |

| Units to account for: | |

| Units in beginning WIP | 8,000 |

| Add: Units started during the period1 | 50,000 |

| Units to account for | 58,000 |

| Units accounted for: | |

| Units completed and transferred | 50,000 |

| Add: Units in ending WIP | 8,000 |

| Units accounted for | 58,000 |

Table (5)

Step 2: Computation of equivalent units:

| Particulars | Material | Conversion |

| Units started and completed | 42,000 | 42,000 |

|

Equivalent units of beginning WIP | 6,400 | |

|

Equivalent units of ending WIP | 8,000 | 2,400 |

| Equivalent units | 50,000 | 50,800 |

Table (6)

Step 3: Computation of unit cost:

| Particulars | Material ($) | Conversion ($) |

| Material cost | 177,660 | |

| Labor cost | 79,545 | |

| Overhead cost | 96,528 | |

| Total cost | 177,660 | 176,073 |

| Equivalent units | 50,000 | 50,800 |

| Unit cost | 3.55 | 3.47 |

Table (7)

Step 4: Valuation of ending inventory:

| Particulars | Amount ($) |

| Equivalent units of material | 28,400 |

| Equivalent units for conversion | 8,328 |

| Transferred in | 78,560 |

| Total value | 115,288 |

Table (8)

Working Notes:

1.

Computation of units started during the period:

Want to see more full solutions like this?

Chapter 6 Solutions

Bundle: Managerial Accounting: The Cornerstone of Business Decision-Making, Loose-Leaf Version, 7th + CengageNOWv2, 1 term (6 months) Printed Access Card

- Reducir, Inc., produces two different types of hydraulic cylinders. Reducir produces a major subassembly for the cylinders in the Cutting and Welding Department. Other parts and the subassembly are then assembled in the Assembly Department. The activities, expected costs, and drivers associated with these two manufacturing processes are given below. Note: In the assembly process, the materials-handling activity is a function of product characteristics rather than batch activity. Other overhead activities, their costs, and drivers are listed below. Other production information concerning the two hydraulic cylinders is also provided: Required: 1. Using a plantwide rate based on machine hours, calculate the total overhead cost assigned to each product and the unit overhead cost. 2. Using activity rates, calculate the total overhead cost assigned to each product and the unit overhead cost. Comment on the accuracy of the plantwide rate. 3. Calculate the global consumption ratios. 4. Calculate the consumption ratios for welding and materials handling (Assembly) and show that two drivers, welding hours and number of parts, can be used to achieve the same ABC product costs calculated in Requirement 2. Explain the value of this simplification. 5. Calculate the consumption ratios for inspection and engineering, and show that the drivers for these two activities also duplicate the ABC product costs calculated in Requirement 2.arrow_forwardThe Sedona Company is dedicated to making products that meet the needs of customers in a sustainable manner. Sedona is best known for its KLN water bottle, which is a BPA-free, dishwasher-safe, bubbly glass bottle in a soft silicone sleeve. The production process consists of three basic operations. In the first operation, the glass is formed by remelting cullets (broken or refuse glass). In the second operation, the glass is assembled with the silicone gasket and sleeve. The resulting product is finished in the final operation with the addition of the polypropylene cap. Consulting studies have indicated that of the total conversion costs required to complete a finished unit, the forming operation requires 60%, the assembly 30%, and the finishing 10%. Cullets purchased $67,500 Silicone purchased $24,000 Polypropylene used $ 6,000 Total conversion costs incurred $68,850 Ending inventory, cullets $ 4,500 Ending inventory, silicone $ 3,000 Number of bottles completed and transferred…arrow_forwardThe Sedona Company is dedicated to making products that meet the needs of customers in a sustainable manner. Sedona is best known for its KLN water bottle, which is a BPA-free, dishwasher-safe, bubbly glass bottle in a soft silicone sleeve. The production process consists of three basic operations. In the first operation, the glass is formed by remelting cullets (broken or refuse glass). In the second operation, the glass is assembled with the silicone gasket and sleeve. The resulting product is finished in the final operation with the addition of the polypropylene cap. Consulting studies have indicated that of the total conversion costs required to complete a finished unit, the forming operation requires 60%, the assembly 30%, and the finishing 10%. Cullets purchased $67,500 Silicone purchased $24,000 Polypropylene used $ 6,000 Total conversion costs incurred $68,850 Ending inventory, cullets $ 4,500 Ending inventory, silicone $ 3,000 Number of bottles completed and transferred…arrow_forward

- The Sedona Company is dedicated to making products that meet the needs of customers in a sustainable manner. Sedona is best known for its KLN water bottle, which is a BPA-free, dishwasher-safe, bubbly glass bottle in a soft silicone sleeve. The production process consists of three basic operations. In the first operation, the glass is formed by remelting cullets (broken or refuse glass). In the second operation, the glass is assembled with the silicone gasket and sleeve. The resulting product is finished in the final operation with the addition of the polypropylene cap. Consulting studies have indicated that of the total conversion costs required to complete a finished unit, the forming operation requires 60%, the assembly 30%, and the finishing 10%. Cullets purchased $67,500 Silicone purchased $24,000 Polypropylene used $ 6,000 Total conversion costs incurred $68,850 Ending inventory, cullets $ 4,500 Ending inventory, silicone $ 3,000 Number of bottles completed and transferred…arrow_forwardScribners Corporation produces fine papers in three production departments—Pulping, Drying, and Finishing. In the Pulping Department, raw materials such as wood fiber and rag cotton are mechanically and chemically treated to separate their fibers. The result is a thick slurry of fibers. In the Drying Department, the wet fibers transferred from the Pulping Department are laid down on porous webs, pressed to remove excess liquid, and dried in ovens. In the Finishing Department, the dried paper is coated, cut, and spooled onto reels. The company uses the weighted-average method in its process costing system. Data for March for the Drying Department follow: Percent Completed Units Pulping Conversion Work in process inventory, March 1 3,800 100 % 80 % Work in process inventory, March 31 5,000 100 % 75 % Pulping cost in work in process inventory, March 1 $ 1,349 Conversion cost in work in process inventory, March 1 $ 684 Units transferred to the…arrow_forwardScribners Corporation produces fine papers in three production departments—Pulping, Drying, and Finishing. In the Pulping Department, raw materials such as wood fiber and rag cotton are mechanically and chemically treated to separate their fibers. The result is a thick slurry of fibers. In the Drying Department, the wet fibers transferred from the Pulping Department are laid down on porous webs, pressed to remove excess liquid, and dried in ovens. In the Finishing Department, the dried paper is coated, cut, and spooled onto reels. The company uses the weighted-average method in its process costing system. Data for March for the Drying Department follow: Percent Completed Units Pulping Conversion Work in process inventory, March 1 3,100 100 % 80 % Work in process inventory, March 31 5,000 100 % 70 % Pulping cost in work in process inventory, March 1 $ 1,674 Conversion cost in work in process inventory, March 1 $ 1,147 Units transferred to the…arrow_forward

- Golding Manufacturing, a division of Farnsworth Sporting, Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handle. The limbs pass through four sequential processes before reaching final assembly: lay-up, molding, fabricating, and finishing. In the Lay-Up Department, limbs are created by laminating layers of wood. In Molding, the limbs are heat treated, under pressure, to form a strong resilient limb. In the Fabricating Department, any protruding glue or other processing residue is removed. Finally, in Finishing, the limbs are cleaned with acetone, dried, and sprayed with the final finishes. The handles pass through two processes before reaching final assembly: pattern and finishing. In the Pattern Department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machines setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the Finishing Department where they are sprayed with the final finishes. In Final Assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight adjustment bolts, side plates, and string. Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80 percent of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation: KAREN: Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in direct material input. AARON: Your predecessor is responsible. He believed that tracking the difference in direct material cost wasnt worth the effort. He simply didnt believe that it would make much difference in the unit cost of either model. KAREN: Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isnt very stringent. All we have to worry about is the Pattern Department. The other departments fit what I view as a process-costing pattern. AARON: Why dont you look into it? If there is a significant difference, go ahead and adjust the costing system. After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the Pattern Department: a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models. b. There was no beginning work in process; however, there were 300 units in ending work in process: 200 Deluxe and 100 Econo models. Both models were 80 percent complete with respect to conversion costs and 100 percent complete with respect to direct materials. c. The Pattern Department experienced the following costs: d. On an experimental basis, the requisition forms for direct materials were modified to identify the dollar value of the direct materials used by the Econo and Deluxe models: Required: 1. Compute the unit cost for the handles produced by the Pattern Department, assuming that process costing is totally appropriate. 2. Compute the unit cost of each handle, using the separate cost information provided on materials. 3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend. 4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this products advertising budget because its per-unit profit (selling price less manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?arrow_forwardHales Company produces a product that requires two processes. In the first process, a subassembly is produced (subassembly A). In the second process, this subassembly and a subassembly purchased from outside the company (subassembly B) are assembled to produce the final product. For simplicity, assume that the assembly of one final unit takes the same time as the production of subassembly A. Subassembly A is placed in a container and sent to an area called the subassembly stores (SB stores) area. A production Kanban is attached to this container. A second container, also with one subassembly, is located near the assembly line (called the withdrawal store). This container has attached to it a withdrawal Kanban. Required: 1. Explain how withdrawal and production Kanban cards are used to control the work flow between the two processes. How does this approach minimize inventories? 2. Explain how vendor Kanban cards can be used to control the flow of the purchased subassembly. What implications does this have for supplier relationships? What role, if any, do continuous replenishment and EDI play in this process?arrow_forwardGolding Manufacturing, a division of Farnsworth Sporting Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handles. The limbs pass through four sequential processes before reaching final assembly: layup, molding, fabricating, and finishing. In the layup department, limbs are created by laminating layers of wood. In the molding department, the limbs are heat-treated, under pressure, to form strong resilient limbs. In the fabricating department, any protruding glue or other processing residue is removed. Finally, in the finishing department, the limbs are cleaned with acetone, dried, and sprayed with the final finishes. The handles pass through two processes before reaching final assembly: pattern and finishing. In the pattern department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machines setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the finishing department, where they are sprayed with the final finishes. In final assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight-adjustment bolts, side plates, and string. Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80% of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product-costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation: Karen: Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in material input. Aaron: Your predecessor is responsible. He believed that tracking the difference in material cost wasnt worth the effort. He simply didnt believe that it would make much difference in the unit cost of either model. Karen: Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isnt very stringent. All we have to worry about is the pattern department. The other departments fit what I view as a process-costing pattern. Aaron: Why dont you look into it? If there is a significant difference, go ahead and adjust the costing system. After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the pattern department: a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models. b. There was no BWIP; however, there were 300 units in EWIP: 200 Deluxe and 100 Econo models. Both models were 80% complete with respect to conversion costs and 100% complete with respect to materials. c. The pattern department experienced the following costs: d. On an experimental basis, the requisition forms for materials were modified to identify the dollar value of the materials used by the Econo and Deluxe models: Required: 1. Compute the unit cost for the handles produced by the pattern department, assuming that process costing is totally appropriate. Round unit cost to two decimal places. 2. Compute the unit cost of each handle, using the separate cost information provided on materials. Round unit cost to two decimal places. 3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend. 4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this products advertising budget because its per-unit profit (selling price minus manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?arrow_forward

- Hepworth Communications produces cell phones. One of the four major electronic components is produced internally. The other three components are purchased from external suppliers. The electronic components and other parts are assembled (by the Assembly Department) and then tested (by the Testing Department). Any units that fail the test are sent to the Rework Department where the unit is taken apart and the failed component is replaced. Data from the Testing Department reveal that the internally produced component (made by the Component Department) is the most frequent cause of product failure. One out of every 50 phones fails because of a faulty internally produced component. Barry Norton is the manager of the Component Department. In a recent performance evaluation, the plant manager told Barry that he needed to be more sensitive to the needs of the departments customers. This charge puzzled Barry somewhatafter all, the component is not sold to anyone but is used in producing the plants cell phones. Required: 1. Who are Barrys customers? 2. Explain the plant managers charge to Barry to be more sensitive to his customers. Explain also how this increased sensitivity could improve the companys time-based competitive ability. 3. What role would cost management play in helping Barry be more sensitive to his customers?arrow_forwardConfer Company produces two different metal components used in medical equipment (Component X and Component Y). The company has three processes: molding, grinding, and finishing. In molding, molds are created, and molten metal is poured into the shell. Grinding removes the gates that allowed the molten metal to flow into the molds cavities. In finishing, rough edges caused by the grinders are removed by small, handheld pneumatic tools. In molding, the setup time is one hour. The other two processes have no setup time required. The demand for Component X is 600 units per day, and the demand for Component Y is 1,000 units per day. The minutes required per unit for each product are as follows: The company operates one eight-hour shift. The molding process employs 24 workers (who each work eight hours). Two hours of their time, however, are used for setups (assuming both products are produced). The grinding process has sufficient equipment and workers to provide 400 grinding hours per shift. The Finishing Department is labor intensive and employs 70 workers, who each work eight hours per day. The only significant unit-level variable costs are materials and power. For Component X, the variable cost per unit is 40, and for Component Y, it is 50. Selling prices for X and Y are 90 and 110, respectively. Confers policy is to use two setups per day: an initial setup to produce all that is scheduled for Component X and a second setup (changeover) to produce all that is scheduled for Component Y. The amount scheduled does not necessarily correspond to each products daily demand. Required: 1. Calculate the time (in minutes) needed each day to meet the daily market demand for Component X and Component Y. What is the major internal constraint facing Confer Company? 2. Describe how Confer should exploit its major binding constraint. Specifically, identify the product mix that will maximize daily throughput. 3. Assume that manufacturing engineering has found a way to reduce the molding setup time from one hour to 10 minutes. Explain how this affects the product mix and daily throughput.arrow_forwardLacy, Inc., produces a subassembly used in the production of hydraulic cylinders. The subassemblies are produced in three departments: Plate Cutting, Rod Cutting, and Welding. Materials are added at the beginning of the process. Overhead is applied using the following drivers and activity rates: Other data for the Plate Cutting Department are as follows: Required: 1. Prepare a physical flow schedule. 2. Calculate equivalent units of production for: a. Direct materials b. Conversion costs 3. Calculate unit costs for: a. Direct materials b. Conversion costs c. Total manufacturing 4. Provide the following information: a. The total cost of units transferred out b. The journal entry for transferring costs from Plate Cutting to Welding c. The cost assigned to units in ending inventoryarrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning