Concept explainers

Videos

Cost Accumulation: Service

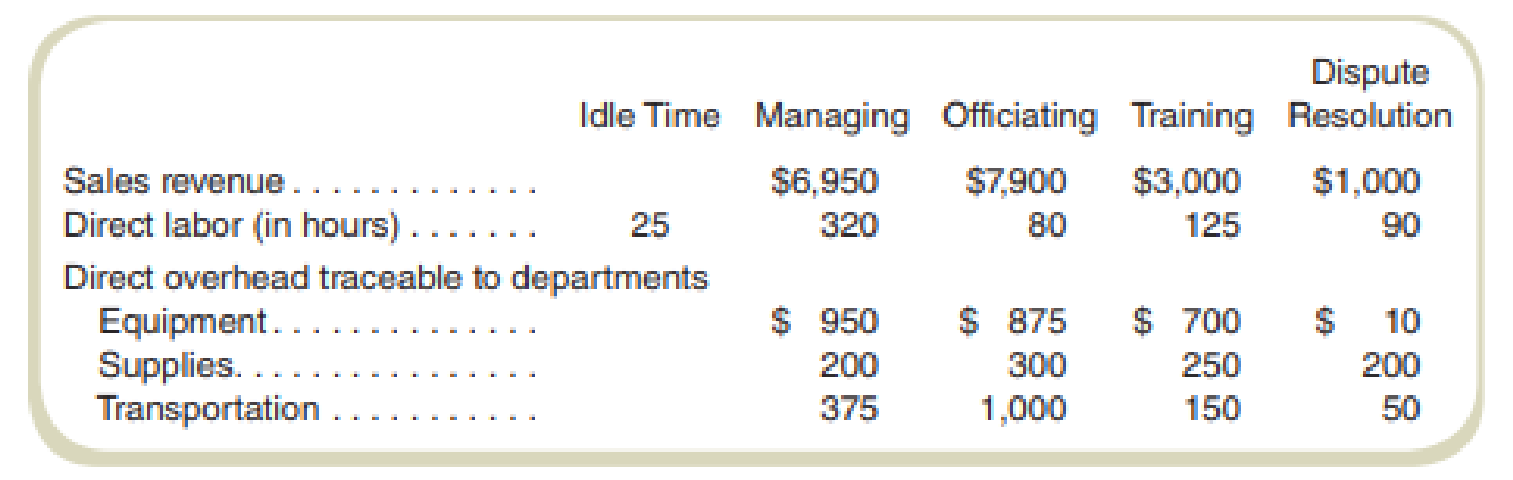

Youth Athletic Services (YAS) provides adult supervision for organized youth athletics. It has a president, William Mayes, and five employees. He and one of the other five employees manage all marketing and administrative duties. The remaining four employees work directly on operations. YAS has four

Some of the July operating data are as follows:

Other Data

- The four employees working in the operating departments all make $15 per hour.

- The fifth employee, who helps manage marketing and administrative duties, earns $2,250 per month, and William earns $3,000 per month.

- Indirect overhead amounted to $768 and is assigned to departments based on the number of direct labor-hours used. Because there are idle hours, some overhead will not be assigned to a department.

- In addition to salaries paid, marketing costs for items such as advertising and special promotions totaled $600.

- In addition to salaries paid, other administrative costs were $225.

- All revenue transactions are cash; all others are on account.

Required

Management wants to know whether each department is contributing to the company’s profit. Prepare an income statement for July that shows the revenue and cost of services for each department. Write a short report to management about departmental profitability. No inventories are kept.

Prepare an income statement for July that shows the revenue and cost of services for each department also write a short report to management about departmental profitability.

Explanation of Solution

Job costing: Job costing is a method of tracking and allocating costs to different jobs in the manufacturing process. This method of costing is used in entities where different jobs are incurred in each period.

Income statement for July that shows the revenue and cost of services:

| Income statement for the month ending July 31. | |||||

| Particulars | Managing | Officiating | Training | Dispute Resolution | Total |

| Revenue | $ 6,950 | $ 7,900 | $ 3,000 | $ 1,000 | $ 18,850 |

| Cost of services | |||||

| Labor | $ 4,800 (1) | $ 1,200 (2) | $ 1,875 (3) | $ 1,350 (4) | |

| Add: direct overhead | $ 1,525 (5) | $ 2,175 (6) | $ 1,100 (7) | $ 260 (8) | |

| Add: indirect overhead | $ 384 (9) | $ 96 (10) | $ 150 (11) | $ 108 (12) | |

| Total costs of services | $ 6,709 | $ 3,471 | $ 3,125 | $ 1,718 | $ 15,023 |

| Department margin | $ 241 | $ 4,429 | ($ 125) | ($ 718) | $ 3,827 |

| Less other costs | |||||

| Unassigned labor costs (idle time) | $ 375 (14) | ||||

| Unassigned overhead, indirect costs | $ 30 | ||||

| Marketing and administrative costs | $ 6,075 | ||||

| Operating profit | ($ 2,653) | ||||

Table: (1)

Managing and Officiating are the departments that are making any profits. Managing among the two is still making very less profit. For Training and Dispute Resolution the management should consider pricing policies of the two. The highest loss was earned by Dispute Resolution.

Thus, the value of operating loss is $2,653 for July.

Working note 1:

Compute the labor:

Working note 2:

Compute the labor:

Working note 3:

Compute the labor:

Working note 4:

Compute the labor:

Working note 5:

Compute the direct overhead:

Working note 6:

Compute the direct overhead:

Working note 7:

Compute the direct overhead:

Working note 8:

Compute the direct overhead:

Working note 9:

Compute the indirect overhead:

Working note 10:

Compute the indirect overhead:

Working note 11:

Compute the indirect overhead:

Working note 12:

Compute the indirect overhead:

Working note 13:

Compute the application rate:

Working note 14:

Compute the unassigned labor cost:

Working note 15:

Compute the indirect labor cost:

Want to see more full solutions like this?

Chapter 7 Solutions

FUNDAMENTALS OF COST ACCOUNTING BUNDLE

- A manufacturing company has two service and two production departments. Building Maintenance and Factory Office are the service departments. The production departments are Assembly and Machining. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The building maintenance department services all departments of the company, and its costs are allocated using floor space occupied, while factory office costs are allocable to Assembly and Machining on the basis of direct labor hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardThayne Company has 30 clerks that work in its Accounts Payable Department. A study revealed the following activities and the relative time demanded by each activity: Required: Classify the four activities as value-added or non-value-added, and calculate the clerical cost of each activity. For non-value-added activities, indicate why they are non-value-added.arrow_forwardJoseph Fox, controller of Thorpe Company, has been in charge of a project to install an activity-based cost management system. This new system is designed to support the companys efforts to become more competitive. For the past six weeks, he and the project committee members have been identifying and defining activities, associating workers with activities, and assessing the time and resources consumed by individual activities. Now, he and the project committee are focusing on three additional implementation issues: (1) identifying activity drivers, (2) assessing value content, and (3) identifying cost drivers (root causes). Joseph has assigned a committee member the responsibilities of assessing the value content of five activities, choosing a suitable activity driver for each activity, and identifying the possible root causes of the activities. Following are the five activities with possible activity drivers: The committee member ran a regression analysis for each potential activity driver, using the method of least squares to estimate the variable and fixed cost components. In all five cases, costs were highly correlated with the potential drivers. Thus, all drivers appeared to be good candidates for assigning costs to products. The company plans to reward production managers for reducing product costs. Required: 1. What is the difference between an activity driver and a cost driver? In answering the question, describe the purpose of each type of driver. 2. For each activity, assess the value content and classify each activity as value-added or non-value-added (justify the classification). Identify some possible root causes of each activity, and describe how this knowledge can be used to improve activity performance. For purposes of discussion, assume that the value-added activities are not performed with perfect efficiency. 3. Describe the behavior that each activity driver will encourage, and evaluate the suitability of that behavior for the companys objective of becoming more competitive.arrow_forward

- Vargas, Inc., produces industrial machinery. Vargas has a machining department and a group of direct laborers called machinists. Each machinist is paid 25,000 and can machine up to 500 units per year. Vargas also hires supervisors to develop machine specification plans and to oversee production within the machining department. Given the planning and supervisory work, a supervisor can oversee three machinists, at most. Vargass accounting and production history reveal the following relationships between units produced and the costs of direct labor and supervision (measured on an annual basis): Required: 1. Prepare two graphs: one that illustrates the relationship between direct labor cost and units produced, and one that illustrates the relationship between the cost of supervision and units produced. Let cost be the vertical axis and units produced the horizontal axis. 2. How would you classify each cost? Why? 3. Suppose that the normal range of activity is between 2,400 and 2,450 units and that the exact number of machinists is currently hired to support this level of activity. Further suppose that production for the next year is expected to increase by an additional 400 units. How much will the cost of direct labor increase (and how will this increase be realized)? Cost of supervision?arrow_forwardMiddler Corporation, a manufacturer of electronics and communications systems, uses a service department charge system to charge profit centers with Computing and Communications Services (CCS) service department costs. The following table identifies an abbreviated list of service categories and activity bases used by the CCS department. The table also includes some assumed cost and activity base quantity information for each service for October. CCS ServiceCategory Activity Base Budgeted Cost Budgeted ActivityBase Quantity Help desk Number of calls $82,350 2,700 Network center Number of devices monitored 631,125 9,350 Electronic mail Number of user accounts 63,500 6,350 Handheld technology support Number of handheld devices issued 140,800 8,800 One of the profit centers for Middler Corporation is the Communication Systems (COMM) sector. Assume the following information for the COMM sector: The sector has 1,000 employees, of whom 30% are office employees.…arrow_forwardMiddler Corporation, a manufacturer of electronics and communications systems, uses a service department charge system to charge profit centers with Computing and Communications Services (CCS) service department costs. The following table identifies an abbreviated list of service categories and activity bases used by the CCS department. The table also includes some assumed cost and activity base quantity information for each service for October. CCS ServiceCategory Activity Base Budgeted Cost Budgeted ActivityBase Quantity Help desk Number of calls $82,350 2,700 Network center Number of devices monitored 631,125 9,350 Electronic mail Number of user accounts 63,500 6,350 Handheld technology support Number of handheld devices issued 140,800 8,800 One of the profit centers for Middler Corporation is the Communication Systems (COMM) sector. Assume the following information for the COMM sector: The sector has 1,000 employees, of whom 30% are office employees.…arrow_forward

- Classification of costs, service sector. Market Focus is a marketing research firm that organizes focus groups for consumer-product companies. Each focus group has eight individuals who are paid $60 per session to provide comments on new products. These focus groups meet in hotels and are led by a trained, independent marketing specialist hired by Market Focus. Each specialist is paid a fixed retainer to conduct a minimum number of sessions and a per session fee of $2,200. A Market Focus staff member attends each session to ensure that all the logistical aspects run smoothly. Direct or indirect (D or I) costs of each individual focus group. Variable or fixed (V or F) costs of how the total costs of Market Focus change as the number of focus groups conducted changes. (If in doubt, select on the basis of whether the total costs will change substantially if there is a large change in the number of groups conducted.) You will have two answers (D or I; V or F) for each of the following…arrow_forwardSalado Inc. provides cleaning services through its Residential and Commercial divisions. Support services of the company are provided by Personnel and Administration areas. Costs of these two areas are allocated to the revenue producing departments. Personnel costs are allocated using number of employees; administration costs are allocated using direct department costs. The following annual budgeted information (presented in a benefits-provided ranking) is available: Personnel Administration Residential Commercial Direct costs $196,000 $252,000 $672,000 $1,120,000 Number of employess 17 42 101 67 Direct labor hours 84,000 126,000 Square feet cleaned 630,000 798,000 a. Using the direct method, allocate the costs of Personnel and Administration to the Residential and Commercial divisions. Total support costs allocated to Residential = $ Total support costs allocated to Commercial = $ b. Using the step method, allocate the costs of Personnel and…arrow_forwardManagement at C. Pier Press has decided to allocate costs of the paper’s two support departments (administration and human resources) to the two revenue-generating departments (advertising and circulation). Administration costs are to be allocated on the basis of dollars of assets employed; human resources costs are to be allocated on the basis of number of employees. The following costs and allocation bases are available: Department Direct Costs Number of Employees Assets Employeed Administration $1,094,100 14 $541,940 Human resources 689,780 11 408,380 Advertising 1,340,920 17 1,067,360 Circulation 1,893,640 36 2,618,420 Totals $5,018,440 78 $4,636,100 a. Using the direct method, allocate the support department costs to the revenue-generating departments. Amount allocated to Advertising: $______ Amount allocated to Circulation: $______ b. Using your answer to (a), what are the total costs of the revenue-generating departments after the allocations? Advertising total…arrow_forward

- Ethics Case. At Symond Company, production workers in the Painting Department are paid on the basis of productivity. The labor time standard for a unit of production is established through periodic time studies conducted by Douglas Management Consultants. In a time actual time required to complete a specific task by a worker is observed. Allowances are then made for preparation time, rest periods, and cleanup time. Bill Carson is one of several veterans in the Painting Department .Bill is informed by Douglas that he will be used in the time study for the beginning of a new product . The findings will be the basis for establishing the labor time standard of the next 6 months.During the test, Bill deliberately slows his normal work pace in an effort to obtain a labor time standard that will be easy to meet. Because it is a new product, the Douglas representatives who conducted the test is unaware that Bill did not give the test his best effort.arrow_forwardFollowing items belong to the revenue, expenditure, human resources/payroll, production, or financing cycle. Classify each item based on the cycle it belongs to. a. Pay pay-as-you-earn (PAYE) payroll taxes b. Send material requisition to inventory c. Issue stock to investors d. Borrow money from the bank to purchase a new factory e. Complete receiving report f. Appoint replacement purchasing clerk g. Measure employee performance using a performance management system h. Choose suitable supplier of raw materials i. Ensure employees are up to date with the latest tax provisions j. Record personal and tax information for new employeesarrow_forwardThe manager of the Personnel Department at City Enterprises has been reading about time-driven ABC and wants to apply it to her department. She has identified four basic activities her employees spend most of the their time on: Interviewing, Hiring, Assessment, and Separation Processing. The department employs five staff who perform these activities. The manager provides the following estimates for the amount of time it takes to complete each of these activities: Interviewing: 45 minutes. Hiring: 60 minutes. Assessment: 75 minutes. Separation Processing: 90 minutes. Employees in Personnel work 35-hour weeks with four weeks for vacation. Of the 35 hours, five are reserved for administrative tasks, training, and so on. The costs of the Personnel Department, including any allocated costs from other staff functions, are $972,000. During the year, Personnel conducted 1,200 interviews, made 375 hires, made 3,000 assessments, and had 250 separations. Required: a. What is the…arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub