Concept explainers

Videos

Recording Daily and

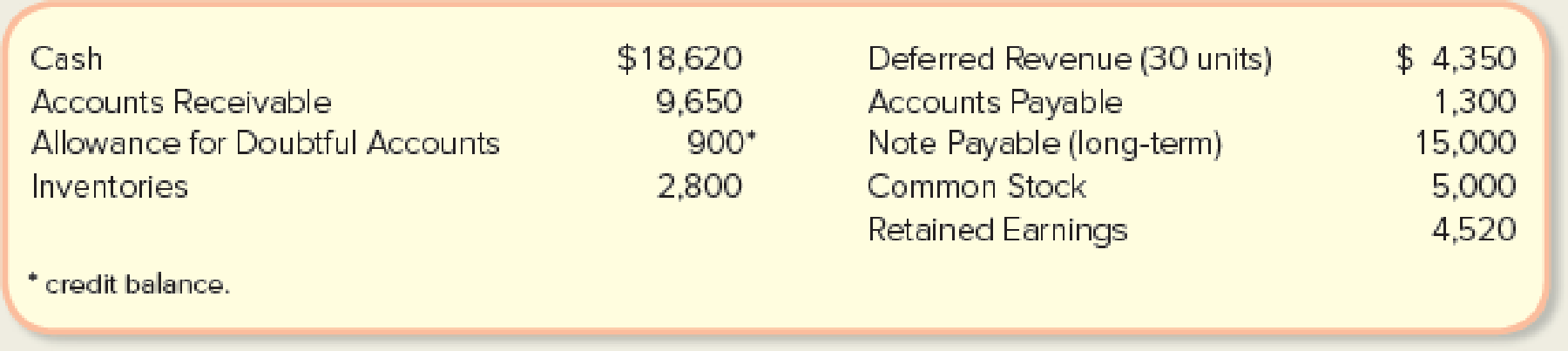

One Trick Pony (OTP) incorporated and began operations near the end of the year, resulting in the following post-closing balances at December 31:

The following information is relevant to the first month of operations in the following year:

- • OTP will sell inventory at $145 per unit. OTP’s January 1 inventory balance consists of 35 units at a total cost of $2,800. OTP’s policy is to use the FIFO method, recorded using a perpetual inventory system.

- • In December, OTP received a $4,350 payment for 30 units OTP is to deliver in January; this obligation was recorded in Deferred Revenue. Rent of $1,300 was unpaid and recorded in Accounts Payable at December 31.

- • OTP’s note payable matures in three years, and accrues interest at a 10% annual rate.

January Transactions

- a. Included in OTP’s January 1 Accounts Receivable balance is a $1,500 balance due from Jeff Letrotski. Jeff is having cash flow problems and cannot pay the $1,500 balance at this time. On 01/01, OTP arranges with Jeff to convert the $1,500 balance to a six-month note, at 12% annual interest. Jeff signs the promissory note, which indicates the principal and all interest will be due and payable to OTP on July 1 of this year.

- b. OTP paid a $500 insurance premium on 01/02, covering the month of January; the payment is recorded directly as an expense.

- c. OTP purchased an additional 150 units of inventory from a supplier on account on 01/05 at a total cost of $9,000, with terms n/30.

- d. OTP paid a courier $300 cash on 01/05 for same-day delivery of the 150 units of inventory.

- e. The 30 units that OTP’s customer paid for in advance in December are delivered to the customer on 01/06.

- f. On 01/07, OTP received a purchase allowance of $1,350 on account, and then paid the amount necessary to settle the balance owed to the supplier for the 1/05 purchase of inventory (in c).

- g. Sales of 40 units of inventory occurring during the period of 01/07–01/10 are recorded on 01/10. The sales terms are n/30.

- h. Collected payments on 01/14 from sales to customers recorded on 01/10.

- i. OTP paid the first 2 weeks’ wages to the employees on 01/16. The total paid is $2,200.

- j. Wrote off a $1,000 customer’s account balance on 01/18. OTP uses the allowance method, not the direct write-off method.

- k. Paid $2,600 on 01/19 for December and January rent. See the earlier bullets regarding the December portion. The January portion will expire soon, so it is charged directly to expense.

- l. OTP recovered $400 cash on 01/26 from the customer whose account had previously been written off on 01/18.

- m. An unrecorded $400 utility bill for January arrived on 01/27. It is due on 02/15 and will be paid then.

- n. Sales of 65 units of inventory during the period of 01/10–01/28, with terms n/30, are recorded on 01/28.

- o. Of the sales recorded on 01/28, 15 units are returned to OTP on 01/30. The inventory is not damaged and can be resold. OTP charges sales returns directly against Sales Revenue.

- p. On 01/31, OTP records the $2,200 employee salary that is owed but will be paid February 1.

- q. OTP uses the aging method to estimate and adjust for uncollectible accounts on 01/31. All of OTP’s accounts receivable fall into a single aging category, for which 8% is estimated to be uncollectible. (Update the balances of both relevant accounts prior to determining the appropriate adjustment, and round your calculation to the nearest dollar.)

- r. Accrue interest for January on the note payable on 01/31.

- s. Accrue interest for January on Jeff Letrotski’s note on 0 1/3 1 (see a).

Required:

- 1. Prepare all January

journal entries and adjusting entries for items (a)–(s). - 2. If you are completing this problem manually, set up T-accounts using the December 31 balances as the beginning balances,

post the journal entries from requirement 1, and prepare an adjustedtrial balance at January 31. If you are completing this problem in Connect using the general ledger tool, this requirement will be completed automatically using your previous answers. - 3. Prepare an income statement, statement of

retained earnings , and classified balance sheet at the end of January. - 4. For the month ended January 31, indicate the (i) gross profit percentage (rounded to one decimal place), (ii) number of units in ending inventory, and (iii) cost per unit of ending inventory (include dollars and cents).

- 5. If OTP had used the percentage of sales method (using 2% of Net Sales) rather than the aging method, what amounts would OTC’s January financial statements have reported for (i)

Bad Debt Expense and (ii) Accounts Receivable, net? - 6. If OTP had used LIFO rather than FIFO, what amount would OTC have reported for Cost of Goods Sold on 01/10?

1.

Prepare the journal entries and adjusting entries for items (a) to (s).

Explanation of Solution

Accounts receivable: Accounts receivable refers to the amounts to be received within a short period from customers upon the sale of goods and services on account. In other words, accounts receivable are amounts customers owe to the business. Accounts receivable is an asset of a business.

Prepare the journal entries and adjusting entries for items (a) to (s).

| Date | Account Title and Explanation | Debit | Credit | |

| a. | January 1 | Note receivable | $1,500 | |

| Account receivable | $1,500 | |||

| (To record the acceptance of note) | ||||

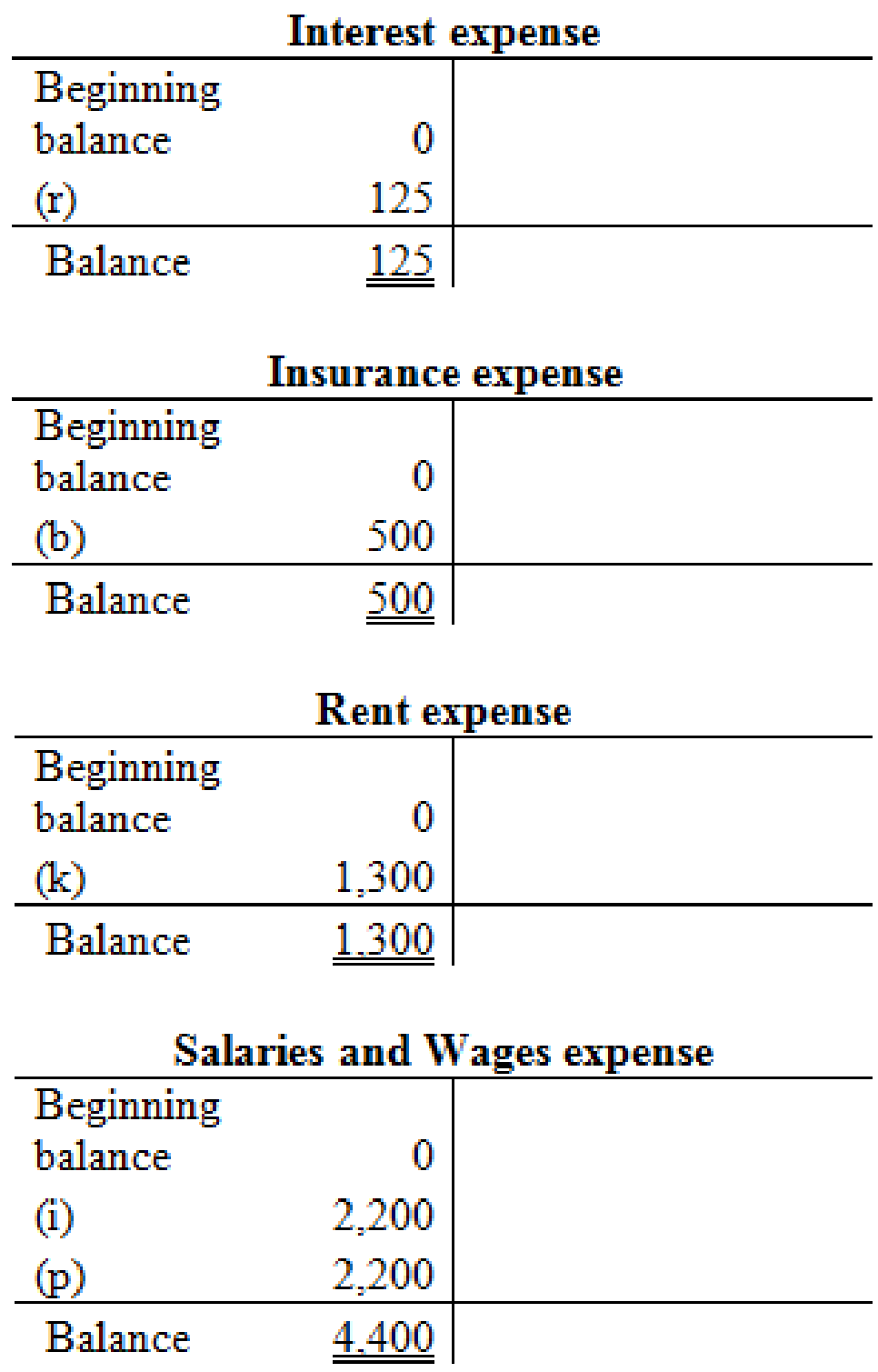

| b. | January 2 | Insurance expense | $500 | |

| Cash | $500 | |||

| (To record the insurance expense ) | ||||

| c. | January 5 | Inventory | $9,000 | |

| Accounts payable | $9,000 | |||

| (To record the purchase of inventory on account) | ||||

| d. | January 5 | Inventory | $300 | |

| Cash | $300 | |||

| (To record the purchase of inventory for cash) | ||||

| e. | January 6 | Deferred revenue | $4,350 | |

| Sales revenue | $4,350 | |||

| (To record the earned deferred revenue) | ||||

| January 6 |

Cost of goods sold | $2,400 | ||

| Sales revenue | $2,400 | |||

| (To record the cost of goods sold) | ||||

| f. | January 7 | Accounts payable | $9,000 | |

| Cash | $7,650 | |||

| Inventory | $1350 | |||

| (To record the settlement of payables) | ||||

| g. |

January 10 | Accounts receivable | $5,800 | |

|

Sales revenue | $5,800 | |||

| (To record the sales provided on account) | ||||

| January 10 |

Cost of goods sold | $2,255 | ||

| Sales revenue | $2,255 | |||

| (To record the cost of goods sold) | ||||

| h. | January 14 | Cash | $5,800 | |

| Accounts receivable | $5,800 | |||

| (To record the collection of cash on account) | ||||

| i. | January 16 | Salaries and Wages expense | $2,200 | |

| Cash | $2,200 | |||

| (To record the salaries and wages expense) | ||||

| j. | January 18 | Allowance for doubtful accounts | $1,000 | |

| Accounts receivable | $1,000 | |||

| (To record the write off) | ||||

| k. | January 19 | Accounts payable | $1,300 | |

| Rent expense | $1,300 | |||

| Cash | $2,600 | |||

| (To record the payment of rent expense and accounts payable) | ||||

| l. | January 26 | Accounts receivable | $400 | |

| Allowance for doubtful accounts | $400 | |||

| (To reverse the written off bad debt) | ||||

| January 26 | Cash | $400 | ||

| Accounts receivable | $400 | |||

| (To record the collection of cash on account) | ||||

| m. | January 27 | Utilities expense | $400 | |

| Accounts payable | $400 | |||

| (To record the accrued utilities expense) | ||||

| n. |

January 28 | Accounts receivable | $9,425 | |

|

Sales revenue | $9,425 | |||

| (To record the sales provided on account) | ||||

| January 28 |

Cost of goods sold | $3,445 | ||

| Sales revenue | $3,445 | |||

| (To record the cost of goods sold) | ||||

| o. | January 30 | Sales returns and allowances | $2,175 | |

| Accounts receivable | $2,175 | |||

| (To record the sales returns) | ||||

| January 30 | Inventory | $795 | ||

| Cost of goods sold | $795 | |||

| (To record the cost of goods sold) | ||||

| p. | January 31 | Salaries and Wages expense | $2,200 | |

| Salaries and Wages payable | $2,200 | |||

| (To record the salaries and wages expense) | ||||

| q. | January 31 | Bad debt expense (1) | $852 | |

| Allowance for doubtful accounts | $852 | |||

| (To record the bad debt expense) | ||||

| r. | January 31 | Interest expense | $125 | |

| Interest payable | $125 | |||

| (To record the interest expense) | ||||

| s. | January 31 | Interest receivable | $15 | |

| Interest revenue | $15 | |||

| (To record the interest revenue) | ||||

Table (1)

Working note (1):

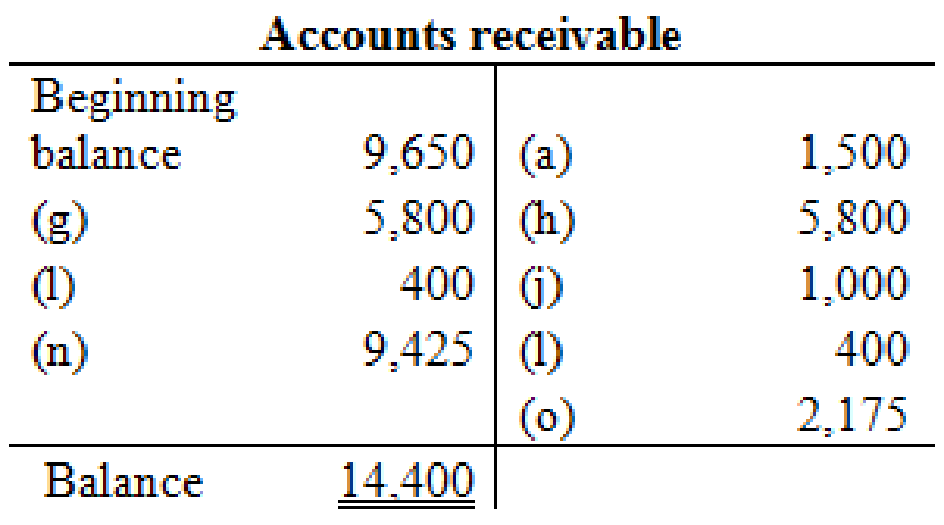

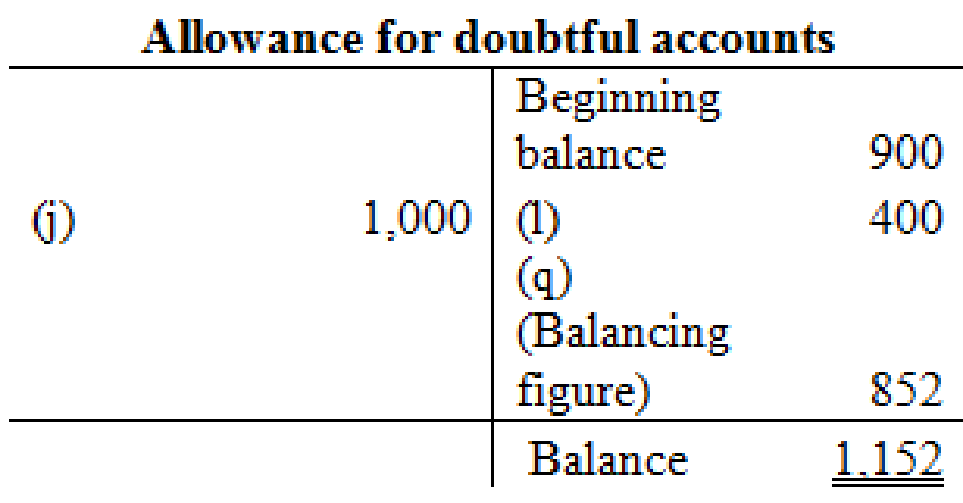

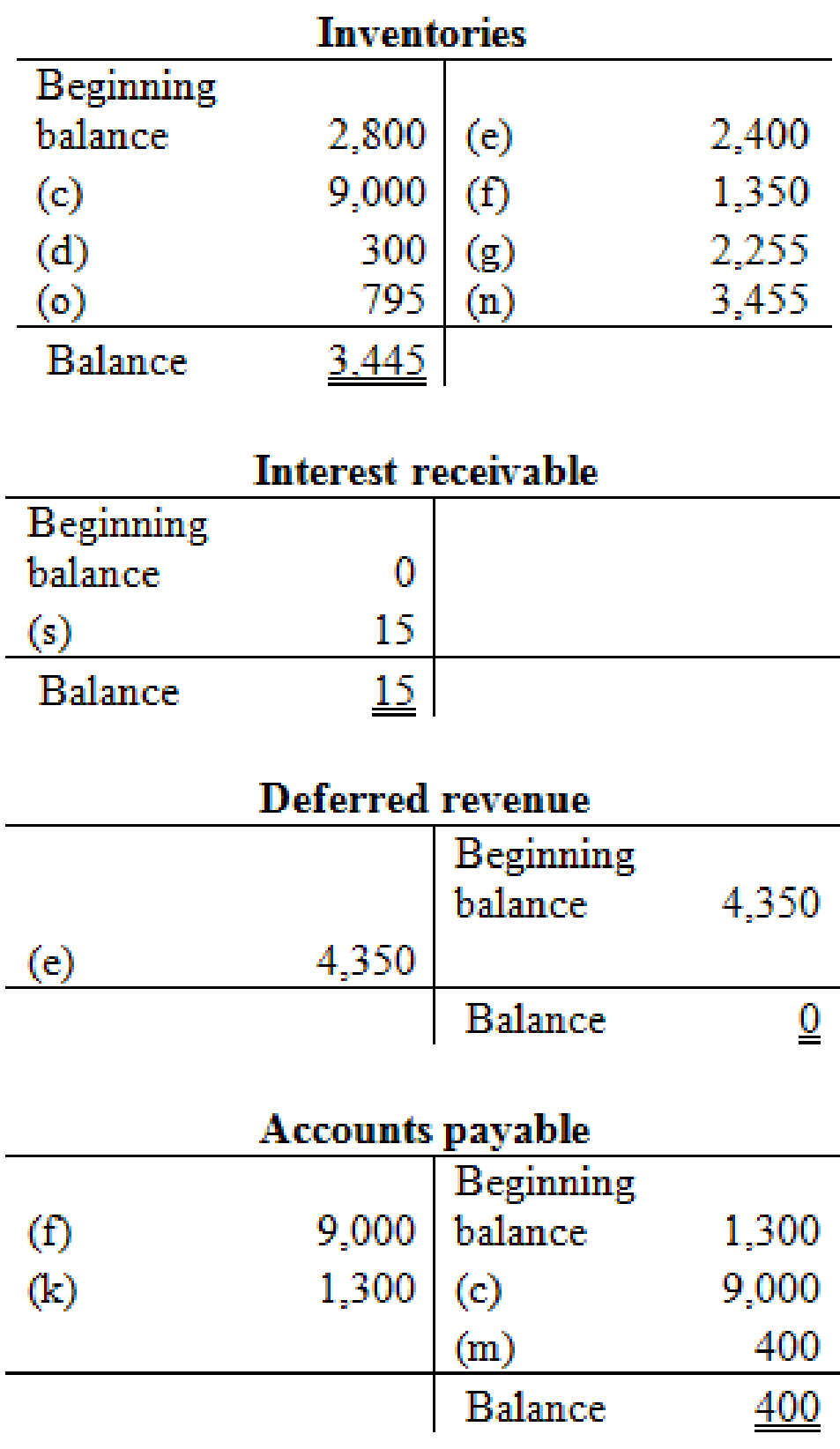

Step 1: Prepare T-account for accounts receivable.

Step 2: Determine the desired ending balance for allowance for doubtful accounts.

Step 3: Now, determine the bad debt expense to be reported on January 31 using T-account for allowance for doubtful accounts.

2.

Set up T-account and post the journal entries, and prepare adjusted trial balance.

Explanation of Solution

Adjusted trial balance: Adjusted trial balance is that statement which contains complete list of accounts with their adjusted balances, after all relevant adjustments have been made. This statement is prepared at the end of every financial period.

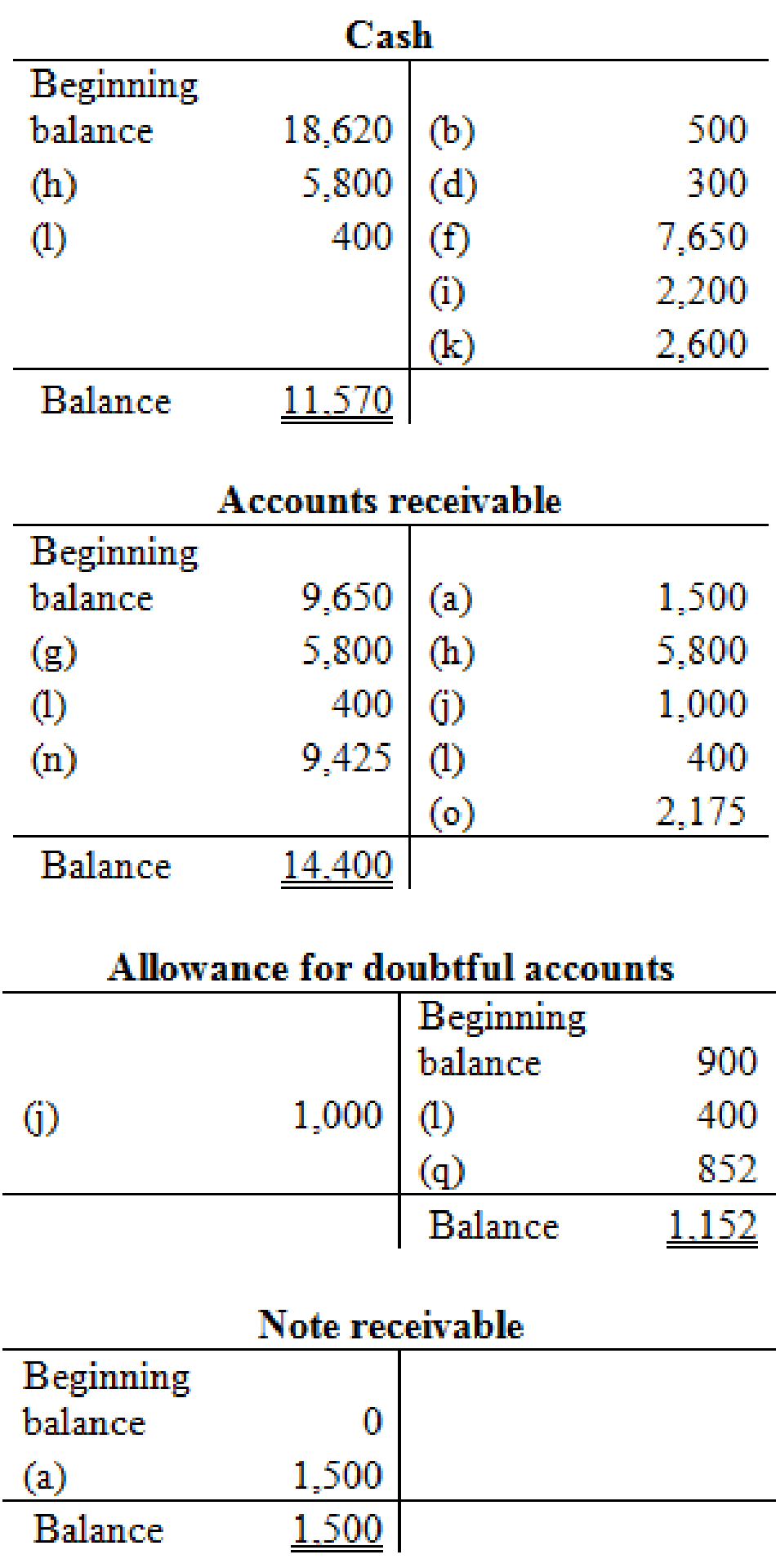

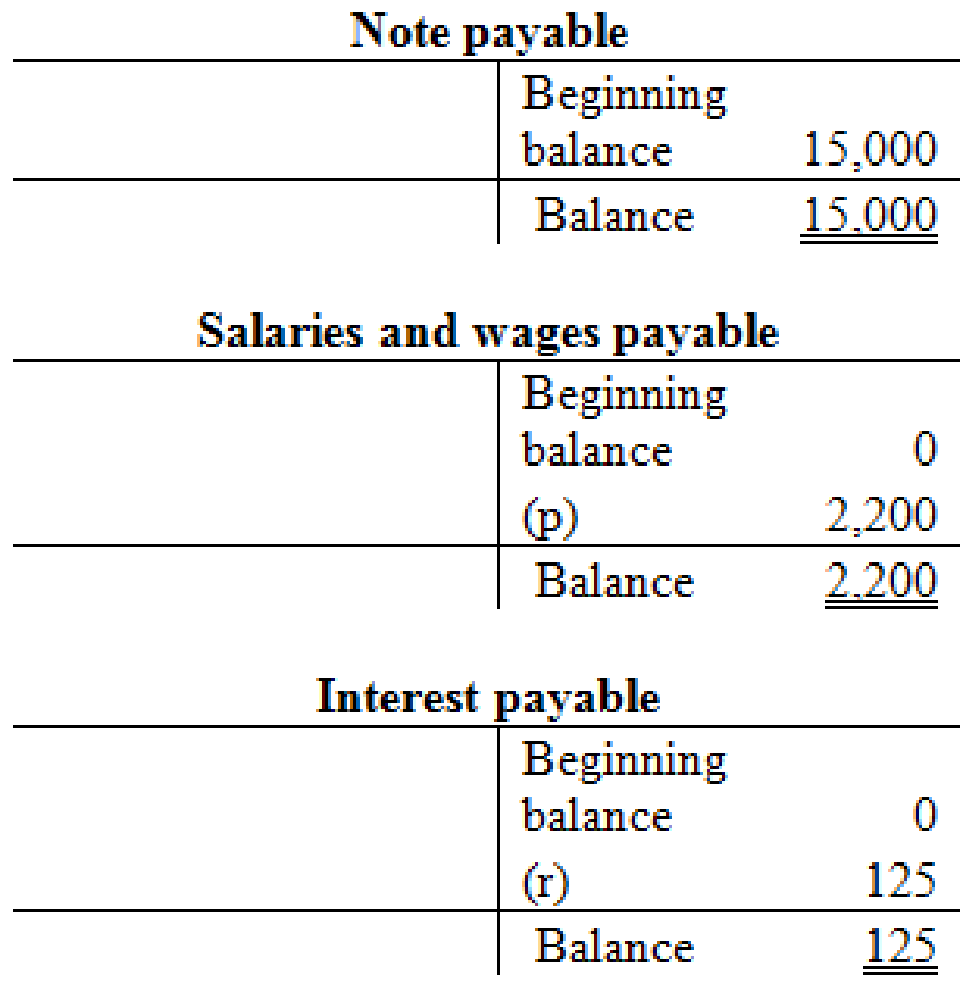

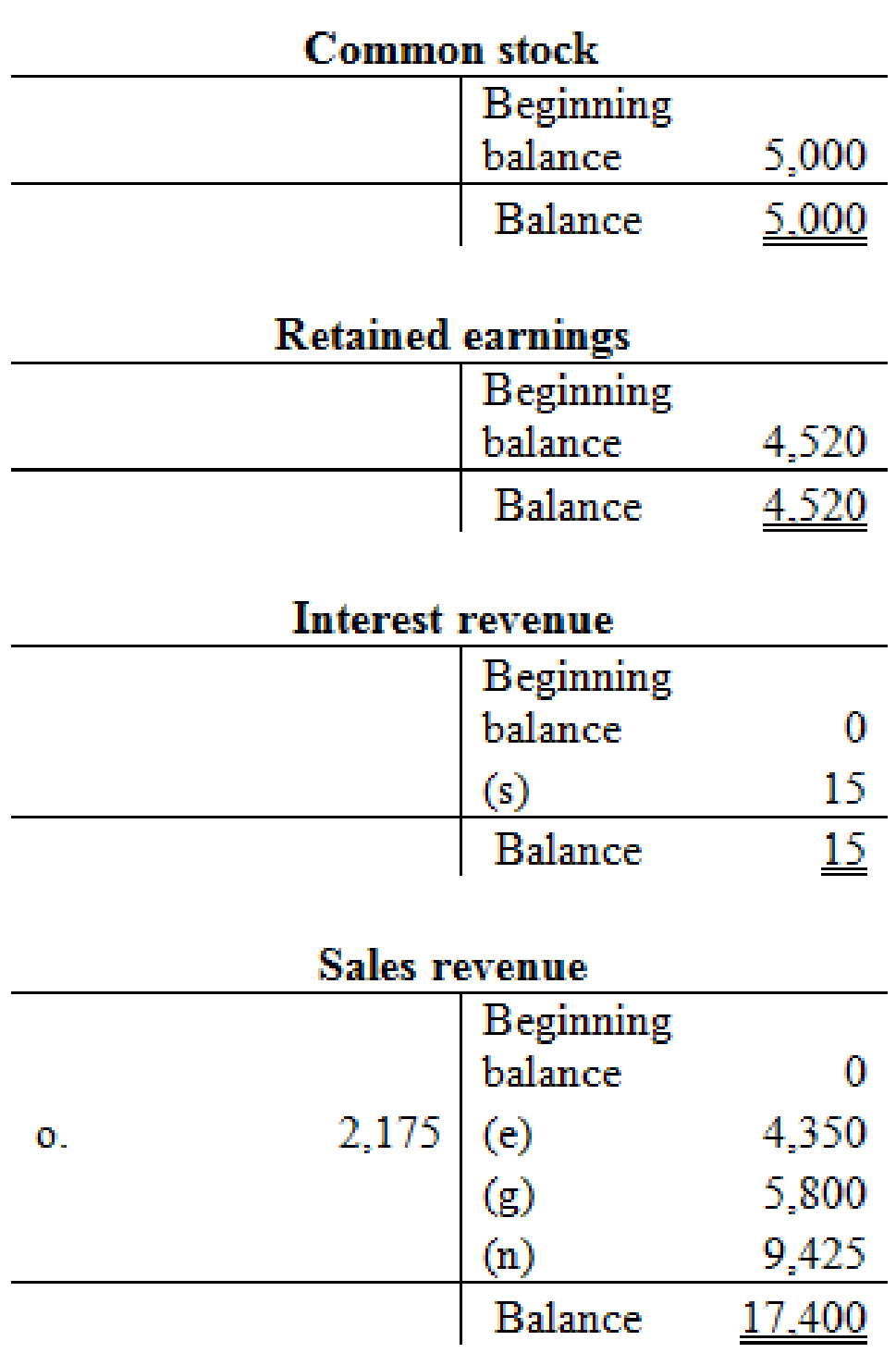

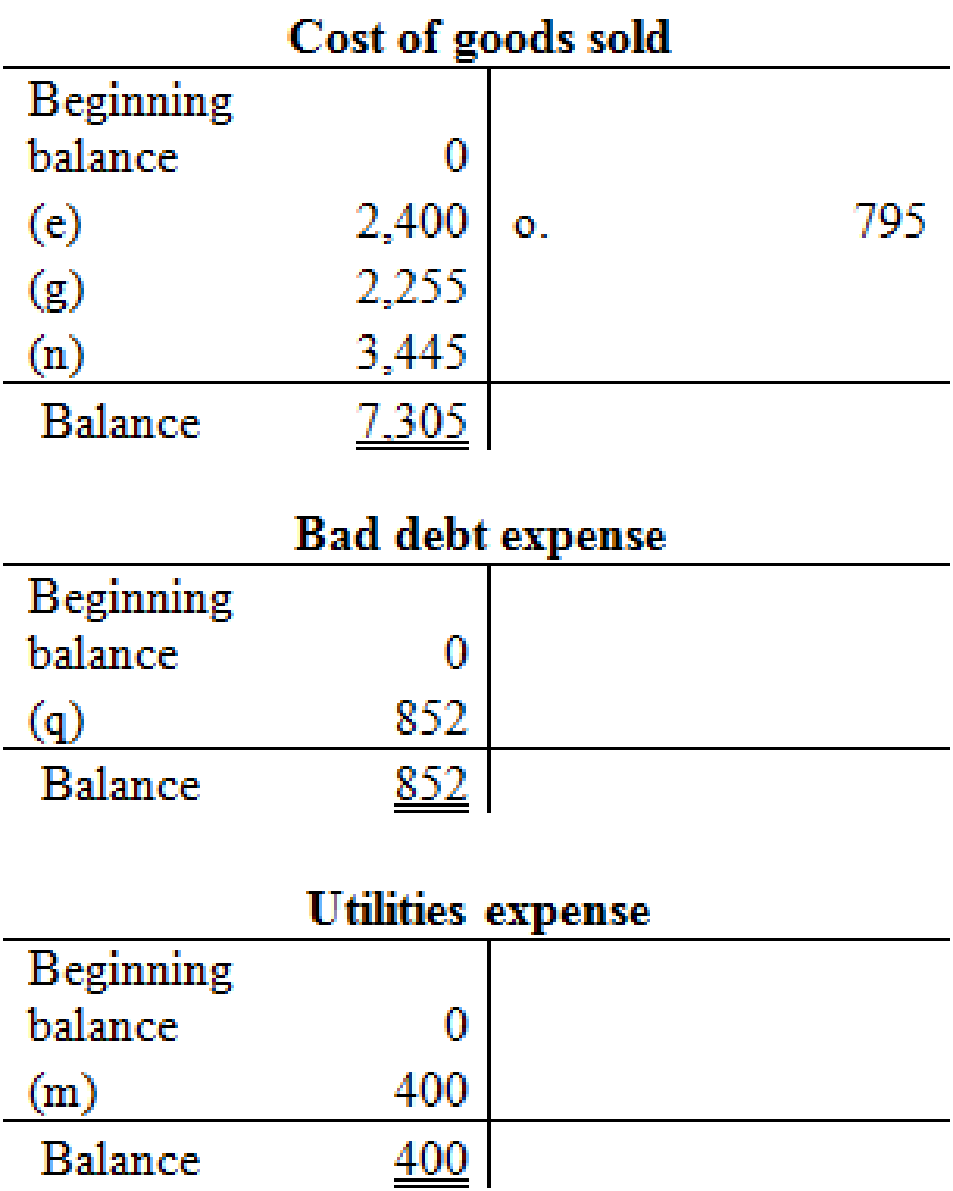

Set up T-account and post the journal entries as follows:

Prepare adjusted trial balance for Company OTP as follows:

| Company OTP | ||

| Adjusted trial balance | ||

| January 31 | ||

| Account Titles | Debit | Credit |

| Cash | $11,570 | |

| Accounts Receivable | 14,400 | |

| Allowance for Doubtful Accounts | $1,152 | |

| Inventory | 3,445 | |

| Note Receivable | 1,500 | |

| Interest Receivable | 15 | |

| Deferred Revenue | 0 | |

| Accounts Payable | 400 | |

| Salaries and Wages Payable | 2,200 | |

| Interest Payable | 125 | |

| Note Payable | 15,000 | |

| Common Stock | 5,000 | |

| Retained Earnings | 4,520 | |

| Sales Revenue | 17,400 | |

| Cost of Goods Sold | 7,305 | |

| Salaries and Wages Expense | 4,400 | |

| Rent Expense | 1,300 | |

| Bad Debt Expense | 852 | |

| Insurance Expense | 500 | |

| Utilities Expense | 400 | |

| Interest Expense | 125 | |

| Interest Revenue | 15 | |

| Totals | $45,812 | $45,812 |

Table (2)

3.

Prepare an income statement, retained earnings statement and classified balance sheet for the month ended January 31.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare an income statement for Company OTP as follows:

| Company OTP | |

| Income Statement | |

| For the Month Ended January 31 | |

| Particulars | Amount |

| Sales Revenue | $17,400 |

| Less: Cost of Goods Sold | 7,305 |

| Gross Profit | 10,095 |

| Less: Salaries and Wages Expense | 4,400 |

| Rent Expense | 1,300 |

| Bad Debt Expense | 852 |

| Insurance Expense | 500 |

| Utilities Expense | 400 |

| Income from Operations | 2,643 |

| Less: Interest Revenue (Expense), net | 110 |

| Net Income | $2,533 |

Table (3)

Statement of Retained Earnings: Statement of retained earnings shows, the changes in the retained earnings, and the income left in the company after payment of the dividends, for the accounting period.

Prepare the statement of retained earnings for Company OTP as follows:

| Company OTP | |

| Statement of Retained Earnings | |

| For the Month Ended January 31 | |

| Particulars | Amount |

| Balance, January 1 | $ 4,520 |

| Add: Net Income | 2,533 |

| Less: Dividends | 0 |

| Balance, December 31 | $ 7,053 |

Table (4)

Classified balance sheet: The main elements of balance sheet assets, liabilities, and stockholders’ equity are categorized or classified further into sections, and sub-sections in a classified balance sheet. Assets are further classified as current assets, long-term investments, property, plant, and equipment (PPE), and intangible assets. Liabilities are classified into two sections current and long-term. Stockholders’ equity comprises of common stock and retained earnings. Thus, the classified balance sheet includes all the elements under different sections.

Prepare classified balance sheet for Company OTP as follows:

| Company OTP | |

| Balance Sheet | |

| At December 31 | |

| Assets | Amount |

| Current Assets: | |

| Cash | $11,570 |

| Accounts Receivable | 14,400 |

| Less: Allowance for Doubtful Accounts | -1,152 |

| Inventory | 3,445 |

| Note Receivable | 1,500 |

| Interest Receivable | 15 |

| Total Assets | $29,778 |

| Liabilities and Stockholders’ Equity | Amount |

| Liabilities | |

| Current Liabilities: | |

| Accounts Payable | $400 |

| Salaries and Wages Payable | 2,200 |

| Interest Payable | 125 |

| Total Current Liabilities | 2,725 |

| Note Payable | 15,000 |

| Total Liabilities (a) | 17,725 |

| Stockholders’ Equity | |

| Common Stock | 5,000 |

| Retained Earnings | 7,053 |

| Total Stockholders’ Equity (b) | 12,053 |

| Total Liabilities and Stockholders’ Equity | $29,778 |

Table (5)

4.

Calculate the following:

- i. The gross profit percentage.

- ii. The number of units in ending inventory.

- iii. Cost per unit of ending inventory.

Explanation of Solution

Gross margin percentage: The percentage of gross profit generated by every dollar of net sales is referred to as gross profit percentage. This ratio measures the profitability of a company by quantifying the amount of income earned from sales revenue generated after cost of goods sold are paid. The higher the ratio, the more ability to cover operating expenses.

- i. Calculate the gross profit percentage as follows:

Thus, the gross profit percentage is 58.01%.

- ii. Calculate the number of units in ending inventory as follows:

| Particulars | Number of units |

| Inventory as of January 1 | 35 |

| Add: Inventory purchased on January 5 | 150 |

| Less: Inventory sold on January 6 | -30 |

| Less: Inventory sold on January 10 | -40 |

| Less: Inventory sold on January 28 | -65 |

| Add: Inventory returned on January 30 | 15 |

| Number of units on hand as of January 31 | 65 |

Table (6)

Thus, the number of units in ending inventory as of January 31 is 65 units.

- iii. Calculate the cost per unit of ending inventory as follows:

Hence, the cost per unit of ending inventory is $53 per unit.

5.

Calculate the net amount that would be reported by Company OTC for (i) bad debt expense, and (ii) accounts receivable, if it uses percentage of sale method.

Explanation of Solution

Bad debt expense: Bad debt expense is an expense account. The amounts of loss incurred from extending credit to the customers are recorded as bad debt expense. In other words, the estimated uncollectible accounts receivable are known as bad debt expense.

- i. Calculate the amount of bad debt expense.

Therefore, Company OTP would have reported $348 as bad debt expense if it uses percentage of sales method.

- ii. Calculate the amount of accounts receivable, net.

Step 1: Prepare T-account for allowance for doubtful accounts according calculated bad debts based on percentage of credit sales method.

| Allowance for doubtful accounts | ||||

| Beginning balance | 900 | |||

| (j) | 1,000 | (l) | 400 | |

| Bad debt expense | 348 | |||

| Balance | 648 | |||

Step 2: Calculate the accounts receivable, net.

Therefore, Company OTP would have reported $13,752 as accounts receivable, net, if it uses percentage of sales method.

6.

Calculate the amount of cost of goods sold that would be reported by Company OTC on January 10, if it uses LIFO instead of FIFO.

Explanation of Solution

First-in-First-Out (FIFO): In this method, items purchased initially are sold first. So, the value of the ending inventory consists the recent cost for the remaining unsold items.

Last-in-First-Out (LIFO): In this method, items purchased recently are sold first. So, the value of the ending inventory consists the initial cost for the remaining unsold items.

If Company OTP uses LIFO (Last-In First Out) instead of FIFO (First-In First Out), then it would have used the cost of goods that was acquired in recent times to calculate the cost of goods sold.

For January 10, the most recently purchased goods is $9,000 of 150 units on January 5, however the cost of goods sold is changed later due to the cost of freight and purchase discount, which is calculated as follows:

| Cost of goods sold | |

| Particulars | $ |

| Purchase value of goods | $9,000 |

| Add: Freight-in | $300 |

| Less: Purchase discount | –$1,350 |

| Cost of goods sold | $7,950 |

Table (7)

These 150 units cost is $7,950, and whose cost per unit is

Thus, at a LIFO unit cost of $53, the 40 units sold on January 10 would have produced a cost of goods sold of

Thus, at a LIFO unit cost of $53, the 40 units sold on January 10 would have produced a cost of goods sold of $2,120.

Want to see more full solutions like this?

Chapter 8 Solutions

Fundamentals Of Financial Accounting

Additional Business Textbook Solutions

Auditing and Assurance Services (16th Edition)

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Fundamentals of Financial Accounting

INTERMEDIATE ACCOUNTING

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Construction Accounting And Financial Management (4th Edition)

- Rescue Sequences LLC purchased inventory by issuing a 30,000, 10%, 60-day note on October 1. Prepare the journal entries for Rescue Sequences to record the purchase and payment assuming it uses a perpetual inventory system and a 360-day calendar fiscal year. Rescue Sequences LLC uses a perpetual inventory system.arrow_forwardJohn Neff owns and operates Waikiki Surf Shop. A year-end trial balance is provided on page 561. Year-end adjustment data for the Waikiki Surf Shop are shown below. Neff uses the periodic inventory system. Year-end adjustment data are as follows: (a, b)A physical count shows that merchandise inventory costing 51,800 is on hand as of December 31, 20--. (c, d, e)Neff estimates that customers will be granted 2,000 in refunds of this years sales next year and the merchandise expected to be returned will have a cost of 1,200. (f)Supplies remaining at the end of the year, 600. (g)Unexpired insurance on December 31, 2,600. (h)Depreciation expense on the building for 20--, 5,000. (i)Depreciation expense on the store equipment for 20--, 3,000. (j)Wages earned but not paid as of December 31, 1,800. (k)Neff also offers boat rentals which clients pay for in advance. Unearned boat rental revenue as of December 31 is 3,000. Required 1. Prepare a year-end spreadsheet. 2. Journalize the adjusting entries. 3. Compute cost of goods sold using the spreadsheet prepared for part (1).arrow_forwardCarla Company uses the perpetual inventory system. The following information is available for January of the current year when Carla sold 1,600 units of inventory on January 14. Using the FIFO method, calculate Carlas cost of goods sold for January and its January 31 inventory.arrow_forward

- Reid Company uses the periodic inventory system. On January 1, it had an inventory balance of 250,000. During the year, it made 613,000 of net purchases. At the end of the year, a physical inventory showed it had ending inventory of 140,000. Calculate Reid Companys cost of goods sold for the year.arrow_forwardFIFO perpetual inventory The beginning inventory at Dunne Co. and data on purchases and sales for a three-month period ending June 30 are as follows: Instructions 1. Record the inventory, purchases, and cost of goods sold data in a perpetual inventory record similar to the one illustrated in Exhibit 3, using the first-in, first-out method. 2. Determine the total sales and the total cost of goods sold for the period. Journalize the entries in the sales and cost of goods sold accounts. Assume that all sales were on account. 3. Determine the gross profit from sales for the period. 4. Determine the ending inventory cost on June 30. 5. Based upon the preceding data, would you expect the ending inventory using the last-in, first-out method to be higher or lower?arrow_forwardJessie Stores uses the periodic system of calculating inventory. The following information is available for December of the current year when Jessie sold 500 units of inventory. Using the FIFO method, calculate Jessies inventory on December 31 and its cost of goods sold for December.arrow_forward

- PERPETUAL: LIFO AND MOVING-AVERAGE Kelley Company began business on January 1, 20-1. Purchases and sales during the month of January follow. REQUIRED Calculate the total amount to be assigned to cost of goods sold for January and the ending inventory on January 31, under each of the following methods: 1. Perpetual LIFO inventory method. 2. Perpetual moving-average inventory method.arrow_forwardPalisade Creek Co. is a retail business that uses the perpetual inventory system. The account balances for Palisade Creek as of May 1, 20Y6 (unless otherwise indicated), are as follows: During May, the last month of the fiscal year, the following transactions were completed: Record the following transactions on Page 21 of the journal: Instructions 1. Enter the balances of each of the accounts in the appropriate balance column of a four-column account. Write Balance in the item section, and place a check mark () in the Posting Reference column. Journalize the transactions for May, starting on Page 20 of the journal. 2. Post the journal to the general ledger, extending the month-end balances to the appropriate balance columns after all posting is completed. In this problem, you are not required to update or post to the accounts receivable and accounts payable subsidiary ledgers. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete (5) and (6). 5. (Optional) Enter the unadjusted trial balance on a 10-column end-of-period spreadsheet (work sheet), and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 22 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of stockholders equity, and a balance sheet. Assume that additional common stock of 10,000 was issued in January 20Y6. 9. Prepare and post the closing entries. Record the closing entries on Page 23 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. Insert the new balance in the retained earnings account. 10. Prepare a post-closing trial balance.arrow_forwardOn September 30, 2013, the general ledger of Leons Golf Shop, which uses the calendar year as its accounting period, showed the following year-to-date account balances: The merchandise inventory account had a 48,000 balance on January 1, 2013. The historical gross profit percentage is 40%. Leon prepares quarterly financial statements and takes physical inventory once a yearat the end of the accounting period. In order to prepare the financial statements for the third quarter, the store needs to have an estimate of ending inventory. You have been asked to use the gross profit method to estimate the ending inventory. Review the worksheet called GP. Study it carefully because it may have a solution format somewhat different from the one shown in your textbook.arrow_forward

- WORK SHEET EXTENSIONS FOR MERCHANDISE INVENTORY ADJUSTMENTS: PERIODIC INVENTORY SYSTEM The following partial work sheet is taken from Kevins Gift Shop for the year ended December 31, 20--. The ending merchandise inventory is 50,000. 1. Complete the Adjustments columns for the merchandise inventory. 2. Extend the merchandise inventory to the Adjusted Trial Balance and Balance Sheet columns. 3. Extend the remaining accounts to the Adjusted Trial Balance and Income Statement columns. 4. Prepare a cost of goods sold section from the partial work sheet.arrow_forwardOn June 30, 2019, the balances of the accounts appearing in the ledger of Simkins Company are as follows: Instructions 1. Does Simkins Company use a periodic or perpetual inventory system? Explain. 2. Prepare a multiple-step income statement for Simkins Company for the year ended June 30, 2019. The merchandise inventory as of June 30, 2019, was 508,000. The adjustment for estimated returns inventory for sales for the year ending December 31, 2019, was 33,000. 3. Prepare the closing entries for Simkins Company as of June 30, 2019. 4. What would the net income have been if the perpetual inventory system had been used?arrow_forwardDymac Appliances uses the periodic inventory system. Details regarding the inventory of appliances at January 1, purchases invoices during the next 12 months, and the inventory count at December 31 are summarized as follows: Instructions 1. Determine the cost of the inventory on December 31 by the first-in, first-out method. Present data in columnar form, using the following headings: If the inventory of a particular model comprises one entire purchase plus a portion of another purchase acquired at a different unit cost, use a separate line for each purchase. 2. Determine the cost of the inventory on December 31 by the last-in, first-out method, following the procedures indicated in (1). 3. Determine the cost of the inventory on December 31 by the weighted average cost method, using the columnar headings indicated in (1). 4. Discuss which method (FIFO or LIFO) would be preferred for income tax purposes in periods of (a) rising prices and (b) declining prices.arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,