Concept explainers

Videos

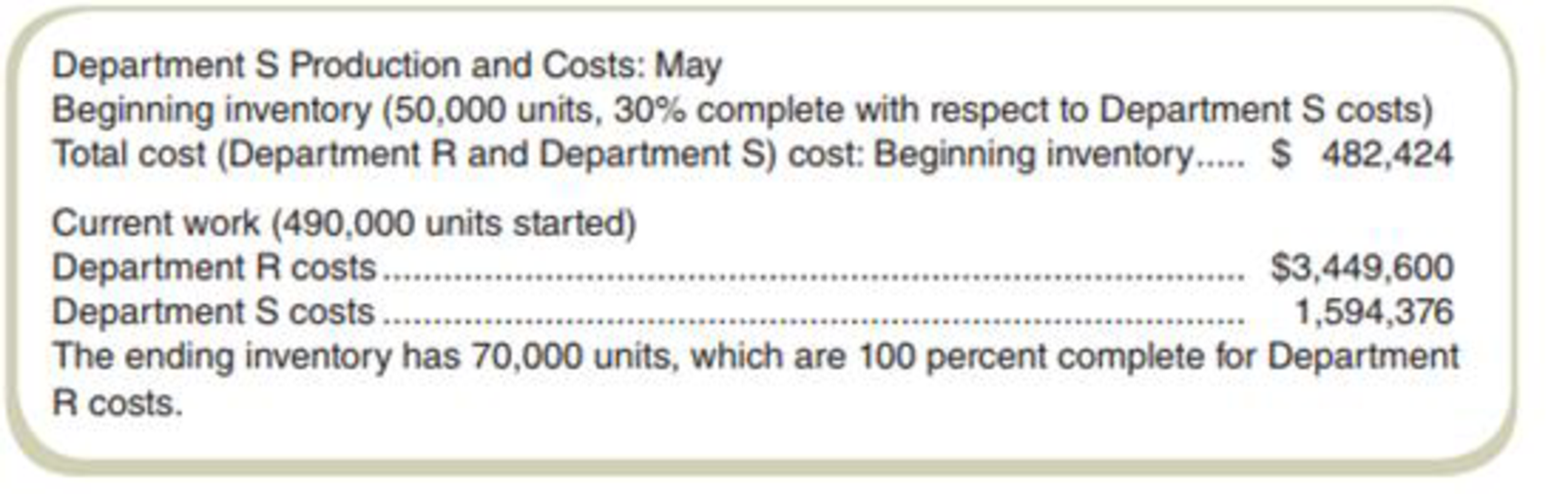

Prepare a Production Cost Report: Weighted-Average Method, Missing Data Saline Solutions uses

Required

- a. Assume that Saline Solutions used weighted-average process costing and that the cost per equivalent unit for May for materials in Department S is $7.20 and for conversion costs it is $3.20. How complete is ending inventory with respect to conversion costs?

- b. What is the cost of product transferred out of Department S for May?

- c. What is the cost of ending inventory in Department S for May?

Want to see the full answer?

Check out a sample textbook solution

Chapter 8 Solutions

FUNDAMENTALS OF COST ACCT.(LL) >CUSTOM<

- Benson Pharmaceuticals uses a process-costing system to compute the unit costs of the over-the-counter cold remedies that it produces. It has three departments: mixing, encapsulating, and bottling. In mixing, the ingredients for the cold capsules are measured, sifted, and blended (with materials assumed to be uniformly added throughout the process). The mix is transferred out in gallon containers. The encapsulating department takes the powdered mix and places it in capsules (which are necessarily added at the beginning of the process). One gallon of powdered mix converts into 1,500 capsules. After the capsules are filled and polished, they are transferred to bottling, where they are placed in bottles that are then affixed with a safety seal, lid, and label. Each bottle receives 50 capsules. During March, the following results are available for the first two departments: Overhead in both departments is applied as a percentage of direct labor costs. In the mixing department, overhead is 200% of direct labor. In the encapsulating department, the overhead rate is 150% of direct labor. Required: 1. Prepare a production report for the mixing department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to two decimal places for the unit cost.) 2. Prepare a production report for the encapsulating department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to four decimal places for the unit cost.) 3. CONCEPTUAL CONNECTION Explain why the weighted average method is easier to use than FIFO. Explain when weighted average will give about the same results as FIFO.arrow_forwardThe Converting Department of Tender Soft Tissue Company uses the weighted average method and had 1,900 units in work in process that were 60% complete at the beginning of the period. During the period, 15,800 units were completed and transferred to the Packing Department. There were 1,200 units in process that were 30% complete at the end of the period. a. Determine the number of whole units to be accounted for and to be assigned costs for the period. b. Determine the number of equivalent units of production for the period. Assume that direct materials are placed in process during production.arrow_forwardK-Briggs Company uses the FIFO method to account for the costs of production. For Crushing, the first processing department, the following equivalent units schedule has been prepared: The cost per equivalent unit for the period was as follows: The cost of beginning work in process was direct materials, 40,000; conversion costs, 30,000. Required: 1. Determine the cost of ending work in process and the cost of goods transferred out. 2. Prepare a physical flow schedule.arrow_forward

- Victory Company uses weighted average process costing. The company has two production processes. Conversion cost is added evenly throughout each process. Direct materials are added at the beginning of the first process. Additional information for the first process follows. Beginning work in process inventory Units started this period Units completed and transferred out Ending work in process inventory Beginning work in process inventory Direct materials Conversion Costs added this period Direct materials Conversion Total costs to account for Total units Units 79,000 891,000 790,000 180,000 Units $ 189, 150 179,600 1,265,850 3,412,400 Direct Materials Percent Complete 100% 100% Percent Complete Required: 1. Compute equivalent units of production for both direct materials and conversion. Conversion Percent Complete 80% $368,750 4,678, 250 $ 5,047,000 Equivalent Units of Production (EUP) - Weighted Average Method Direct Materials EUP 60% Percent Complete Conversion EUParrow_forwardThe Bottling Department of Mountain Springs Water Company had 4,100 liters in beginning work in process that were 30% complete. During the period, 56,800 liters were completed. The ending work in process inventory had 2,800 liters that were 60% complete. Assume that Mountain Springs uses the FIFO cost flow method and that materials are added at the beginning of the process. What are the conversion equivalent units of production for the period?arrow_forwardFIFO Method, Two-Department Analysis Muskoge Company uses a process-costing system. The company manufactures a product that is processed in two departments: Molding and Assembly. In the Molding Department, direct materials are added at the beginning of the process; in the Assembly Department, additional direct materials are added at the end of the process. In both departments, conversion costs are incurred uniformly throughout the process. As work is completed, it is transferred out. The following table summarizes the production activity and costs for February: Molding Assembly Beginning inventories: Physical units 10,000 8,000 Costs: Transferred in — $45,300 Direct materials $22,000 — Conversion costs $13,800 $16,900 Current production: Units started 25,000 ? Units transferred out 30,000 35,000 Costs: Transferred in — ? Direct materials…arrow_forward

- FIFO Method, Two-Department Analysis Muskoge Company uses a process-costing system. The company manufactures a product that is processed in two departments: Molding and Assembly. In the Molding Department, direct materials are added at the beginning of the process; in the Assembly Department, additional direct materials are added at the end of the process. In both departments, conversion costs are incurred uniformly throughout the process. As work is completed, it is transferred out. The following table summarizes the production activity and costs for February: Molding Assembly Beginning inventories: Physical units 10,000 8,000 Costs: Transferred in — $45,300 Direct materials $22,000 — Conversion costs $13,800 $16,700 Current production: Units started 25,000 ? Units transferred out 30,000 35,000 Costs: Transferred in — ? Direct materials…arrow_forwardFIFO Method, Two-Department Analysis Muskoge Company uses a process-costing system. The company manufactures a product that is processed in two departments: Molding and Assembly. In the Molding Department, direct materials are added at the beginning of the process; in the Assembly Department, additional direct materials are added at the end of the process. In both departments, conversion costs are incurred uniformly throughout the process. As work is completed, it is transferred out. The following table summarizes the production activity and costs for February: Molding Assembly Beginning inventories: Physical units 10,000 8,000 Costs: Transferred in — $45,300 Direct materials $22,000 — Conversion costs $13,800 $16,900 Current production: Units started 25,000 ? Units transferred out 30,000 35,000 Costs: Transferred in — ? Direct materials…arrow_forwardVictory Company uses weighted average process costing. The company has two production processes. Conversion cost is added evenly throughout each process. Direct materials are added at the beginning of the first process. Additional information for the first process follows. Beginning work in process inventory Units started this period Total units Units completed and transferred out Ending work in process inventory Beginning work in process inventory Direct materials Conversion Costs added this period Direct materials Conversion Total costs to account for Units Units 79,000 894,000 795,000 178,000 $ 632,450 180, 360 Percent Complete 4,232,550 3,426,840 Direct Materials Percent Complete 100% 100% Required: 1. Compute equivalent units of production for both direct materials and conversion. Conversion Percent Complete 80% $ 812,810 Equivalent Units of Production (EUP) - Weighted Average Method Direct Materials EUP 7,659,390 $ 8,472,200 60% Percent Complete Conversion EUParrow_forward

- The Converting Department of Tender Soft Tissue Company uses the average cost method and had 1,900 units in work in process that were 60% complete at the beginning of the period. During the period, 15,800 units were completed and transferred to the Packing Department.There were 1,200 units in process that were 30% complete at the end of the period.a. Determine the number of whole units to be accounted for and to be assigned costs for the period.b. Determine the number of equivalent units of production for the period.arrow_forwardGladden Dock Company manufactures boat docks on an assembly line. Its costing system uses two cost categories, direct materials and conversion costs. Each product must pass through the Assembly Department and the Finishing Department. This problem focuses on the Assembly Department. Direct materials are added at the beginning of the production process. Conversion costs are allocated evenly throughout production. The firm uses FIFO method and the controller prepared the following (correct) equivalent unit calculation. Unitscompleted Physical Units Direct Materials Conversion WIP, beginning 70 0 52.5 Started and completed 30 30 30 WIP, ending 10 10 5 Totals 110 40 87.5 Cost per Equiv Unit $4,000 $16,000 Work in process, beginning inventory: Current Costs:Direct materials $140,000 Direct materials $ 160,000Conversion costs $260,000 Conversion…arrow_forwardMuskoge Company uses a process-costing system. The company manufactures a product that isprocessed in two departments: Molding and Assembly. In the Molding Department, directmaterials are added at the beginning of the process; in the Assembly Department, additionaldirect materials are added at the end of the process. In both departments, conversion costs areincurred uniformly throughout the process. As work is completed, it is transferred out. Thefollowing table summarizes the production activity and costs for February: Molding AssemblyBeginning inventories: Physical units 10,000 8,000 Costs: Transferred in — $ 45,400 Direct materials $22,000 — Conversion costs $13,800 $ 16,700Current production: Units started 25,000 ? Units transferred out 30,000 35,000 Costs: Transferred in — ? Direct materials $ 56,250 $ 40,250 Conversion costs $103,500 $142,845 Percentage of completion: Beginning inventory 40% 55% Ending inventory 80 50Required:3. Using the FIFO method, prepare the following for…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub