Concept explainers

Videos

(This serial problem began in Chapter 1 and continues through most of the book if previous chapter segment were not completed the serial problem can begin at this point. It is helpful but not necessary to use the working papers that accompany the book.)

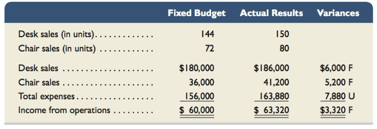

Business Solutions’s second quarter 2016 fixed budget performance report for its computer furniture operations follows. The $156,000 budgeted expenses include $108,000 in variable expenses for desks and $18,000 in variable expenses for chairs, as well as $30,000 fixed expenses. The actual expenses include $31,000 fixed expenses. Prepare a flexible budget performance report that shows any variances between budgeted results and actual results. List fixed and variable expenses separately.

Want to see the full answer?

Check out a sample textbook solution

Chapter 8 Solutions

MANAGERIAL ACCOUNTING ACCT 2302 >IC<

- Listed below are the budgeted factory overhead costs for 2011 for Moss Industries at a projected level of 2,000 units: Required: Prepare flexible budgets for factory overhead at the 1,000, 2,000, and 4,000 unit levels. (Hint: You must first decide which of the listed costs should be considered variable and which should be fixed.)arrow_forwardAdam Corporation manufactures computer tables and has the following budgeted indirect manufacturing cost information for the next year: If Adam uses the step-down (sequential) method, beginning with the Maintenance Department, to allocate support department costs to production departments, the total overhead (rounded to the nearest dollar) for the Machining Department to allocate to its products would be: a. 407,500. b. 422,750. c. 442,053. d. 445,000.arrow_forwardCassara, Inc., had the following quality costs for the years ended December 31, 20X1 and 20X2: At the end of 20X1, management decided to increase its investment in control costs by 40% for each categorys items, with the expectation that failure costs would decrease by 25% for each item of the failure categories. Sales were 12,000,000 for both 20X1 and 20X2. Required: 1. Calculate the budgeted costs for 20X2, and prepare an interim quality performance report. 2. Comment on the significance of the report. How much progress has Cassara made?arrow_forward

- Kelly Gray, production manager, was upset with the latest performance report, which indicated that she was 100,000 over budget. Given the efforts that she and her workers had made, she was confident that they had met or beat the budget. Now, she was not only upset but also genuinely puzzled over the results. Three itemsdirect labor, power, and setupswere over budget. The actual costs for these three items follow: Kelly knew that her operation had produced more units than originally had been budgeted, so more power and labor had naturally been used. She also knew that the uncertainty in scheduling had led to more setups than planned. When she pointed this out to John Huang, the controller, he assured her that the budgeted costs had been adjusted for the increase in productive activity. Curious, Kelly questioned John about the methods used to make the adjustment. JOHN: If the actual level of activity differs from the original planned level, we adjust the budget by using budget formulasformulas that allow us to predict what the costs will be for different levels of activity. KELLY: The approach sounds reasonable. However, Im sure something is wrong here. Tell me exactly how you adjusted the costs of labor, power, and setups. JOHN: First, we obtain formulas for the individual items in the budget by using the method of least squares. We assume that cost variations can be explained by variations in productive activity where activity is measured by direct labor hours. Here is a list of the cost formulas for the three items you mentioned. The variable X is the number of direct labor hours: Labor cost = 10X Power cost = 5,000 + 4X Setup cost = 100,000 KELLY: I think I see the problem. Power costs dont have a lot to do with direct labor hours. They have more to do with machine hours. As production increases, machine hours increase more rapidly than direct labor hours. Also, ... JOHN: You know, you have a point. The coefficient of determination for power cost is only about 50 percent. That leaves a lot of unexplained cost variation. The coefficient for labor, however, is much betterit explains about 96 percent of the cost variation. Setup costs, of course, are fixed. KELLY: Well, as I was about to say, setup costs also have very little to do with direct labor hours. And I might add that they certainly are not fixedat least not all of them. We had to do more setups than our original plan called for because of the scheduling changes. And we have to pay our people when they work extra hours. It seems as if we are always paying overtime. I wonder if we simply do not have enough people for the setup activity. Supplies are used for each setup, and these are not cheap. Did you build these extra costs of increased setup activity into your budget? JOHN: No, we assumed that setup costs were fixed. I see now that some of them could vary as the number of setups increases. Kelly, let me see if I can develop some cost formulas based on better explanatory variables. Ill get back with you in a few days. Assume that after a few days work, John developed the following cost formulas, all with a coefficient of determination greater than 90 percent: Labor cost = 10X; where X = Direct labor hours Power cost = 68,000 + 0.9Y; where Y = Machine hours Setup cost = 98,000 + 400Z; where Z = Number of setups The actual measures of each of the activity drivers are as follows: Required: 1. Prepare a performance report for direct labor, power, and setups using the direct-labor-based formulas. 2. Prepare a performance report for direct labor, power, and setups using the multiple cost driver formulas that John developed. 3. Of the two approaches, which provides the most accurate picture of Kellys performance? Why? 4. After reviewing the approach to performance measurement, a consultant remarked that non-value-added cost trend reports would be a much better performance measurement approach than comparing actual costs with budgeted costseven if activity flexible budgets were used. Do you agree or disagree? Explain.arrow_forwardThe controller for Muir Companys Salem plant is analyzing overhead in order to determine appropriate drivers for use in flexible budgeting. She decided to concentrate on the past 12 months since that time period was one in which there was little important change in technology, product lines, and so on. Data on overhead costs, number of machine hours, number of setups, and number of purchase orders are in the following table. Required: 1. Calculate an overhead rate based on machine hours using the total overhead cost and total machine hours. (Round the overhead rate to the nearest cent and predicted overhead to the nearest dollar.) Use this rate to predict overhead for each of the 12 months. 2. Run a regression equation using only machine hours as the independent variable. Prepare a flexible budget for overhead for the 12 months using the results of this regression equation. (Round the intercept and x-coefficient to the nearest cent and predicted overhead to the nearest dollar.) Is this flexible budget better than the budget in Requirement 1? Why or why not?arrow_forwardDouglas Davis, controller for Marston, Inc., prepared the following budget for manufacturing costs at two different levels of activity for 20X1: During 20X1, Marston worked a total of 80,000 direct labor hours, used 250,000 machine hours, made 32,000 moves, and performed 120 batch inspections. The following actual costs were incurred: Marston applies overhead using rates based on direct labor hours, machine hours, number of moves, and number of batches. The second level of activity (the right column in the preceding table) is the practical level of activity (the available activity for resources acquired in advance of usage) and is used to compute predetermined overhead pool rates. Required: 1. Prepare a performance report for Marstons manufacturing costs in the current year. 2. Assume that one of the products produced by Marston is budgeted to use 10,000 direct labor hours, 15,000 machine hours, and 500 moves and will be produced in five batches. A total of 10,000 units will be produced during the year. Calculate the budgeted unit manufacturing cost. 3. One of Marstons managers said the following: Budgeting at the activity level makes a lot of sense. It really helps us manage costs better. But the previous budget really needs to provide more detailed information. For example, I know that the moving materials activity involves the use of forklifts and operators, and this information is lost when only the total cost of the activity for various levels of output is reported. We have four forklifts, each capable of providing 10,000 moves per year. We lease these forklifts for five years, at 10,000 per year. Furthermore, for our two shifts, we need up to eight operators if we run all four forklifts. Each operator is paid a salary of 30,000 per year. Also, I know that fuel costs about 0.25 per move. Assuming that these are the only three items, expand the detail of the flexible budget for moving materials to reveal the cost of these three resource items for 20,000 moves and 40,000 moves, respectively. Based on these comments, explain how this additional information can help Marston better manage its costs. (Especially consider how activity-based budgeting may provide useful information for non-value-added activities.)arrow_forward

- The Fantasy Gifts Company, a maker of Holiday novelties, needs your help immediately. The company's accountant resigned without leaving adequate records or explanations for what she did. In reviewing the records, you find the following information for May: Materials Purchased 23,000 units Materials Used 16,500 units You find a copy of the budget which shows that materials were budgeted at $0.50/unit. You know that the material price variance is recorded at the time of purchase and you find some handwritten notes among the accountant's work papers, which indicate the following: Material price variance $ 230 F Material efficiency variance $ 750 F What was the total standard cost of direct materials purchased during May? Multiple Choice $11,730. $11,270. $8,365. $11,500.arrow_forwardThe Fantasy Gifts Company, a maker of Holiday novelties, needs your help immediately. The company's accountant resigned without leaving adequate records or explanations for what she did. In reviewing the records, you find the following information for May: Materials Purchased Materials Used 36,000 units 23,000 units You find a copy of the budget which shows that materials were budgeted at $0.60 per unit. You know that the materials price variance is recorded at the time of purchase and you find some handwritten notes among the accountants work papers, which indicate the following: Materials price variance Materials efficiency variance $ 360 F $ 1,400 F What was the total actual cost of the direct materials purchased during May? Multiple Cholce $13,800 $21,240 $21.600arrow_forwardThe Fantasy Gifts Company, a maker of Holiday novelties, needs your help immediately. The company's accountant resigned without leaving adequate records or explanations for what she did. In reviewing the records, you find the following information for May: Materials Purchased 29,000 units Materials Used 19,500 units You find a copy of the budget which shows that materials were budgeted at $0.50/unit. You know that the material price variance is recorded at the time of purchase and you find some handwritten notes among the accountant's work papers, which indicate the following: Material price variance $ 290 F Material efficiency variance $ 1,050 F What was the total standard cost of direct materials allowed during May? Multiple Choice $8,526. $10,800. $8,700. $10,584.arrow_forward

- The Fantasy Gifts Company, a maker of Holiday novelties, needs your help immediately. The company's accountant resigned without leaving adequate records or explanations for what they did. In reviewing the records, you find the following information for May: Materials Purchased Materials Used 38,000 units 24,000 units You find a copy of the budget which shows that materials were budgeted at $0.60 per unit. You know that the materials price variance is recorded at the time of purchase and you find some handwritten notes among the accountants work papers. which indicate the following: Materials price variance Materials efficiency variance $ 380 F $ 1,500 F What was the total standard cost of direct materials purchased during May? Multiple Cholce $22.420 $22,800 $14.628 $23,180arrow_forwardI am struggling to find a few of the answers. Flexible Budget ApplicationThe cutting department of Liberty Manufacturing Company operated during September 2016 with the following manufacturing overhead cost budget based on 6,000 hours of monthly productive capacity: Liberty Manufacturing CompanyCutting DepartmentOverhead Budget (6,000 Hours)For the Month of September 2016 Variable costs: Factory supplies $48,000 Indirect labor 72,000 Utilities (usage charge) 36,000 Patent royalties on secret process 144,000 Total variable overhead $300,000 Fixed costs: Supervisory salaries 96,000 Depreciation on factory equipment 140,000 Factory taxes 40,000 Factory insurance 24,000 Utilities (base charge) 32,000 Total fixed overhead 332,000 Total manufacturing overhead $632,000 The cutting department was operated for 5,460 hours during September…arrow_forwardRoyal Ltd has a varied client base that includes schools, hospitals, and the hospitality sector and has experienced fluctuating consumer demands since the beginning of the Covid-19 pandemic. One of their products is a fresh produce box, consisting of local seasonal produce, and which is ordered in units. The following information is available for the year ending 30th September. Due to these fluctuating demands, you have been asked to use Excel to prepare a flexible sales budget for quantities of 200,000 units and 300,000 units. Sales revenue is fully variable. Budget Sales (units) 250,000 £/unit £000s Sales revenue 3,250 Variable produce costs (875) Variable production overheads (150) Fixed production costs (700) Fixed administration costs (1,160) Profit 365arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning