Concept explainers

Videos

Optima Company is a high-technology organization that produces a mass-storage system. The design of Optima’s system is unique and represents a breakthrough in the industry. The units Optima produces combine positive features of both compact and hard disks. The company is completing its fifth year of operations and is preparing to build its

- a. Fourth-quarter sales for 20X0 are 55,000 units.

- b. Unit sales by quarter (for 20X1) are projected as follows:

The selling price is $400 per unit. All sales are credit sales. Optima collects 85% of all sales within the quarter in which they are realized; the other 15% is collected in the following quarter. There are no

- c. There is no beginning inventory of finished goods. Optima is planning the following ending finished goods inventories for each quarter:

- d. Each mass-storage unit uses 5 hours of direct labor and three units of direct materials. Laborers are paid $10 per hour, and one unit of direct materials costs $80.

- e. There are 65,700 units of direct materials in beginning inventory as of January 1, 20X1. At the end of each quarter, Optima plans to have 30% of the direct materials needed for next quarter’s unit sales. Optima will end the year with the same amount of direct materials found in this year’s beginning inventory.

- f. Optima buys direct materials on account. Half of the purchases are paid for in the quarter of acquisition, and the remaining half are paid for in the following quarter. Wages and salaries are paid on the 15th and 30th of each month.

- g. Fixed

overhead totals $1 million each quarter. Of this total, $350,000 representsdepreciation . All other fixed expenses are paid for in cash in the quarter incurred. The fixed overhead rate is computed by dividing the year’s total fixed overhead by the year’s budgeted production in units. - h. Variable overhead is budgeted at $6 per direct labor hour. All variable overhead expenses are paid for in the quarter incurred.

- i. Fixed selling and administrative expenses total $250,000 per quarter, including $50,000 depreciation.

- j. Variable selling and administrative expenses are budgeted at $10 per unit sold. All selling and administrative expenses are paid for in the quarter incurred.

- k. The balance sheet as of December 31, 20X0, is as follows:

- l. Optima will pay quarterly dividends of $300,000. At the end of the fourth quarter, $2 million of equipment will be purchased.

Required:

Prepare a master budget for Optima Company for each quarter of 20X1 and for the year in total. The following component budgets must be included:

- 1. Sales budget

- 2. Production budget

- 3. Direct materials purchases budget

- 4. Direct labor budget

- 5. Overhead budget

- 6. Selling and administrative expenses budget

- 7. Ending finished goods inventory budget

- 8. Cost of goods sold budget (Note: Assume that there is no change in work-in-process inventories.)

- 9.

Cash budget - 10. Pro forma income statement (using absorption costing) (Note: Ignore income taxes.)

- 11. Pro forma balance sheet (Note: Ignore income taxes.)

1.

Construct sales budget.

Explanation of Solution

Budgets:

Budgets are prepared for the planning and controlling purposes. Budgets facilitate planning and making decisions to achieve the desired objectives and are prepared to enable comparison between actual and expected outcomes.

Sales budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Sales units (A) | 65,000 | 70,000 | 75,000 | 90,000 | 300,000 |

| Selling price (B) | 400 | 400 | 400 | 400 | |

| Sales | 26,000,000 | 28,000,000 | 30,000,000 | 36,000,000 | 120,000,000 |

Table (1)

2.

Construct production budget.

Explanation of Solution

Production budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Expected sales | 65,000 | 70,000 | 75,000 | 90,000 | 300,000 |

| Add: Closing units. | 13,000 | 15,000 | 20,000 | 10,000 | 58,000 |

| Less: Opening units. | 0 | 13,000 | 15,000 | 20,000 | 48,000 |

| Production units | 78,000 | 72,000 | 80,000 | 80,000 | 310,000 |

Table (2)

Working Notes:

- Opening units are closing units of previous quarter.

- Production units are computed by adding closing units and subtracting opening units from the expected sales.

3.

Construct direct material purchases budget.

Explanation of Solution

Materials purchases budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Expected material required for production | 234,000 | 216,000 | 240,000 | 240,000 | 930,000 |

| Add: Closing units. 30% of sales units of next month | 63,000 | 67,500 | 81,000 | 65,700 | 65,700 |

| Less: Opening units. | 65,700 | 63,000 | 67,500 | 81,000 | 65,700 |

| Material units expected to be purchased (A) | 231,300 | 220,500 | 253,500 | 224,700 | 930,000 |

|

Material cost: $80 per unit | 18,504,000 | 17,640,000 | 20,280,000 | 17,976,000 | 74,400,000 |

Table (3)

4.

Construct direct labor budget.

Explanation of Solution

Direct labor budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Expected production (A) | 78,000 | 72,000 | 80,000 | 80,000 | 310,000 |

| Hours per unit (B) | 5 | 5 | 5 | 5 | 5 |

|

Number of hours | 390,000 | 360,000 | 400,000 | 400,000 | 1,550,000 |

| Rate per hour | 10 | 10 | 10 | 10 | 10 |

| Labor cost | 3,900,000 | 3,600,000 | 4,000,000 | 4,000,000 | 15,500,000 |

Table (4)

5.

Construct overhead budget.

Explanation of Solution

Overhead budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Number of hours (sub-part 4) (A) | 390,000 | 360,000 | 400,000 | 400,000 | 1,550,000 |

| Variable overhead | 2,340,000 | 2,160,000 | 2,400,000 | 2,400,000 | 9,300,000 |

| Fixed overhead (C) | 1,000,000 | 1,000,000 | 1,000,000 | 1,000,000 | 4,000,000 |

|

Total overhead | 3,340,000 | 3,160,000 | 3,400,000 | 3,400,000 | 13,300,000 |

Table (5)

6.

Construct selling and administrative expenses budget.

Explanation of Solution

Selling and administrative expenses budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Number of sales units (A) | 65,000 | 70,000 | 75,000 | 90,000 | 300,000 |

| Variable expense | 650,000 | 700,000 | 750,000 | 900,000 | 3,000,000 |

| Fixed expense(C) | 250,000 | 250,000 | 250,000 | 250,000 | 1,000,000 |

|

Total overhead | 900,000 | 950,000 | 1,000,000 | 1,150,000 | 4,000,000 |

Table (6)

7.

Construct ending finished goods inventory budget.

Explanation of Solution

Ending goods inventory budget:

| Particulars |

Amount ($) |

| Material cost | 240 |

| Add: Labor cost | 50 |

| Add: Variable overheads | 30 |

| Add: Fixed overheads | 12.90 |

| Unit cost | 332.90 |

| Cost of ending goods | 3,329,000 |

Table (7)

8.

Construct COGS budget.

Explanation of Solution

Cost of goods sold budget:

| Particulars |

Amount ($) |

| Material cost | 74,400,000 |

| Add: Labor cost | 15,500,000 |

| Add: Variable overheads | 9,300,000 |

| Add: Fixed overheads | 4,000,000 |

| Manufacturing cost (A) | 103,200,000 |

| Add: Beginning finished goods | 0 |

| Cost of goods available for sale (A) | 103,200,000 |

| Less: Ending goods (sub-part 7) (B) | 3,329,000 |

| COGS | 99,871,000 |

Table (8)

9.

Construct cash budget.

Explanation of Solution

Cash Budget:

| Particulars |

Q1 ($) |

Q2 ($) |

Q3 ($) |

Q4 ($) |

Total ($) |

| Opening balance | 250,000 | 1,110,000 | 3,128,000 | 5,568,000 | 250,000 |

| Receipt from sales of current quarter |

22,100,000 |

25,500,000 | 102,000,000 | ||

| Receipts from sales of previous quarter | 3,300,000 |

3,900,000 |

4,200,000 |

4,500,000 | 15,900,000 |

| Less: Payment for material purchased in preceding quarter1 | 7,248,000 | 9,252,000 | 8,820,000 | 10,140,000 | 35,460,000 |

| Less: Payment for material purchased in current quarter |

9,252,000 |

8,820,000 |

10,140,000 |

8,988,000 | 37,200,000 |

| Less: labor cost | 3,900,000 | 3,600,000 | 4,000,000 | 4,000,000 | 15,500,000 |

| Less: Variable manufacturing Overhead cost | 2,340,000 | 2,160,000 | 2,400,000 | 2,400,000 | 9,300,000 |

| Less: Fixed manufacturing Overhead cost | 650,000 | 650,000 | 650,000 | 650,000 | 2,600,000 |

| Less: Variable Selling and administrative expense | 650,000 | 700,000 | 750,000 | 900,000 | 3,000,000 |

| Less: Fixed Selling and administrative expense | 200,000 | 200,000 | 200,000 | 200,000 | 800,000 |

| Less: Dividends | 300,000 | 300,000 | 300,000 | 300,000 | 1,200,000 |

| Less: acquisition of equipment | 2,000,000 | 2,000,000 | |||

| Closing balance | 1,110,000 | 3,128,000 | 5,568,000 | 11,090,000 | 11,090,000 |

Table (9)

Working Notes:

1. Computation of payment for material purchased in quarter 4 of the last year:

10.

Construct pro forma income statement.

Explanation of Solution

Budgeted income statement:

| Particulars |

Amount ($) |

| Sales | 120,000,000 |

| Less: COGS (sub-part 8) | 99,871,000 |

| Operating profit | 20,129,000 |

| Less: Selling and administrative expenses | 4,000,000 |

| Income | 16,129,000 |

Table (10)

11.

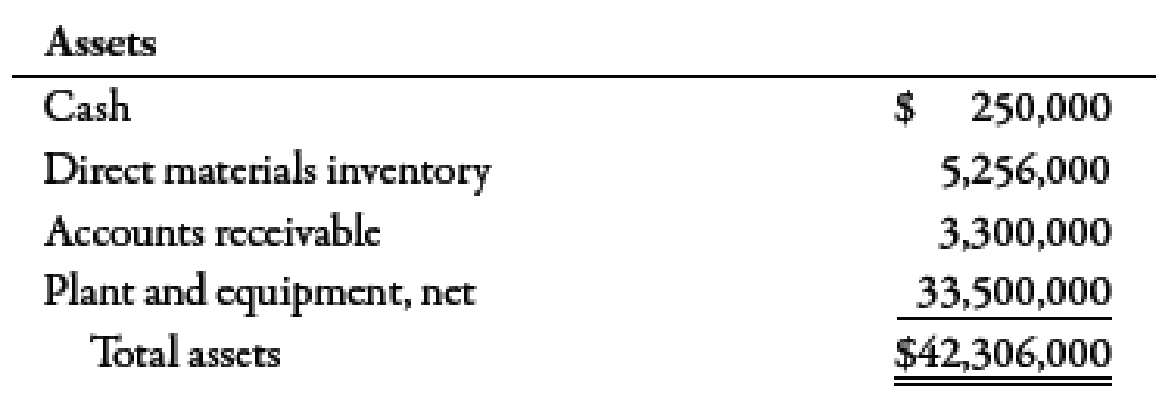

Construct pro forma balance sheet.

Explanation of Solution

Budgeted Balance Sheet:

| Particulars |

Amount ($) |

| Assets: | |

| Cash | 11,090,000 |

| Direct material inventory | 5,256,000 |

| Accounts receivable | 5,400,000 |

| Finished goods inventory | 3,329,000 |

| Plant and equipment | 33,900,000 |

| Total Assets | 58,975,000 |

| Liabilities and Equity: | |

| Accounts payable | 8,988,000 |

| Capital stock | 27,000,000 |

| Retained Earnings | 22,987,000 |

| Total liabilities and equity | 58,975,000 |

Table (11)

Working Notes:

1.

Computation of opening retained earnings:

Capital stock of $27,000,000 has been assumed.

Want to see more full solutions like this?

Chapter 9 Solutions

Managerial Accounting

- Iona Company, a large printing company, is in its fourth year of a five-year, quality improvement program. The program began in 20x0 with an internal study that revealed the quality costs being incurred. In that year, a five-year plan was developed to lower quality costs to 10 percent of sales by the end of 20x5. Sales and quality costs for each year are as follows: Budgeted figures. Quality costs by category are expressed as a percentage of sales as follows: The detail of the 20x5 budget for quality costs is also provided. All prevention costs are fixed; all other quality costs are variable. During 20x5, the company had 12 million in sales. Actual quality costs for 20x4 and 20x5 are as follows: Required: 1. Prepare an interim quality cost performance report for 20x5 that compares actual quality costs with budgeted quality costs. Comment on the firms ability to achieve its quality goals for the year. 2. Prepare a one-period quality performance report for 20x5 that compares the actual quality costs of 20x4 with the actual costs of 20x5. How much did profits change because of improved quality? 3. Prepare a graph that shows the trend in total quality costs as a percentage of sales since the inception of the quality improvement program. 4. Prepare a graph that shows the trend for all four quality cost categories for 20x1 through 20x5. How does this graph help management know that the reduction in total quality costs is attributable to quality improvements? 5. Assume that the company is preparing a second five-year plan to reduce quality costs to 2.5 percent of sales. Prepare a long-range quality cost performance report assuming sales of 15 million at the end of five years. Assume that the final planned relative distribution of quality costs is as follows: proofreading, 50 percent; other inspection, 13 percent; quality training, 30 percent; and quality reporting, 7 percent.arrow_forwardNorton Company, a manufacturer of infant furniture and carriages, is in the initial stages of preparing the annual budget for the coming year. Scott Ford has recently joined Nortons accounting staff and is interested in learning as much as possible about the companys budgeting process. During a recent lunch with Marge Atkins, sales manager, and Pete Granger, production manager, Ford initiated the following conversation. FORD: Since Im new around here and am going to be involved with the preparation of the annual budget, Id be interested in learning how the two of you estimate sales and production numbers. ATKINS: We start out very methodically by looking at recent history, discussing what we know about current accounts, potential customers, and the general state of consumer spending. Then, we add that usual dose of intuition to come up with the best forecast we can. GRANGER: I usually take the sales projections as the basis for my projections. Of course, we have to make an estimate of what this years closing inventories will be, which is sometimes difficult. FORD: Why does that present a problem? There must have been an estimate of closing inventories in the budget for the current year. GRANGER: Those numbers arent always reliable since Marge makes some adjustments to the sales numbers before passing them on to me. FORD: What kind of adjustments? ATKINS: Well, we dont want to fall short of the sales projections so we generally give ourselves a little breathing room by lowering the initial sales projection anywhere from 5 to 10 percent. GRANGER: So, you can see why this years budget is not a very reliable starting point. We always have to adjust the projected production rates as the year progresses, and of course, this changes the ending inventory estimates. By the way, we make similar adjustments to expenses by adding at least 10 percent to the estimates; I think everyone around here does the same thing. Required: 1. Marge Atkins and Pete Granger have described the use of budgetary slack. a. Explain why Atkins and Granger behave in this manner, and describe the benefits they expect to realize from the use of budgetary slack. b. Explain how the use of budgetary slack can adversely affect Atkins and Granger. 2. As a management accountant, Scott Ford believes that the behavior described by Marge Atkins and Pete Granger may be unethical and that he may have an obligation not to support this behavior. By citing the specific standards of competence, confidentiality, integrity, and/or credibility from the Statement of Ethical Professional Practice (in Chapter 1), explain why the use of budgetary slack may be unethical. (CMA adapted)arrow_forwardShalimar Company manufactures and sells industrial products. For next year, Shalimar has budgeted the follow sales: In Shalimars experience, 10 percent of sales are paid in cash. Of the sales on account, 65 percent are collected in the quarter of sale, 25 percent are collected in the quarter following the sale, and 7 percent are collected in the second quarter after the sale. The remaining 3 percent are never collected. Total sales for the third quarter of the current year are 4,900,000 and for the fourth quarter of the current year are 6,850,000. Required: 1. Calculate cash sales and credit sales expected in the last two quarters of the current year, and in each quarter of next year. 2. Construct a cash receipts budget for Shalimar Company for each quarter of the next year, showing the cash sales and the cash collections from credit sales. 3. What if the recession led Shalimars top management to assume that in the next year 10 percent of credit sales would never be collected? The expected payment percentages in the quarter of sale and the quarter after sale are assumed to be the same. How would that affect cash received in each quarter? Construct a revised cash budget using the new assumption.arrow_forward

- Foy Company has a welding activity and wants to develop a flexible budget formula for the activity. The following resources are used by the activity: Four welding units, with a lease cost of 12,000 per year per unit Six welding employees each paid a salary of 50,000 per year (A total of 9,000 welding hours are supplied by the six workers.) Welding supplies: 300 per job Welding hours: Three hours used per job During the year, the activity operated at 90 percent of capacity and incurred the actual activity and resource costs, shown on page 676. Lease cost: 48,000 Salaries: 315,000 Parts and supplies: 805,000 Required: 1. Prepare a flexible budget formula for the welding activity using welding hours as the driver. 2. Prepare a performance report for the welding activity. 3. What if welders were hired through outsourcing and paid 30 per hour (the welding equipment is provided by Foy)? Repeat Requirement 1 for the outsourcing case.arrow_forwardNovo, Inc., wants to develop an activity flexible budget for the activity of moving materials. Novo uses eight forklifts to move materials from receiving to stores. The forklifts are also used to move materials from stores to the production area. The forklifts are obtained through an operating lease that costs 18,000 per year per forklift. Novo employs 25 forklift operators who receive an average salary of 50,000 per year, including benefits. Each move requires the use of a crate. The crates are used to store the parts and are emptied only when used in production. Crates are disposed of after one cycle (two moves), where a cycle is defined as a move from receiving to stores to production. Each crate costs 1.80. Fuel for a forklift costs 3.60 per gallon. A gallon of gas is used every 20 moves. Forklifts can make three moves per hour and are available for 280 days per year, 24 hours per day (the remaining time is downtime for various reasons). Each operator works 40 hours per week and 50 weeks per year. Required: 1. Prepare a flexible budget for the activity of moving materials, using the number of cycles as the activity driver. 2. Calculate the activity capacity for moving materials. Suppose Novo works at 80 percent of activity capacity and incurs the following costs: Prepare the budget for the 80 percent level and then prepare a performance report for the moving materials activity. 3. Calculate and interpret the volume variance for moving materials. 4. Suppose that a redesign of the plant layout reduces the demand for moving materials to one-third of the original capacity. What would be the budget formula for this new activity level? What is the budgeted cost for this new activity level? Has activity performance improved? How does this activity performance evaluation differ from that described in Requirement 2? Explain.arrow_forwardOptima Company is a high-technology organization that produces a mass-storage system. Thedesign of Optima’s system is unique and represents a breakthrough in the industry. The unitsOptima produces combine positive features of both compact and hard disks. The company iscompleting its fifth year of operations and is preparing to build its master budget for the comingyear (20X1). The budget will detail each quarter’s activity and the activity for the year in total.The master budget will be based on the following information:a. Fourth-quarter sales for 20X0 are 55,000 units.b. Unit sales by quarter (for 20X1) are projected as follows:First quarter 65,000Second quarter 70,000Third quarter 75,000Fourth quarter 90,000The selling price is $400 per unit. All sales are credit sales. Optima collects 85% of all saleswithin the quarter in which they are realized; the other 15% is collected in the followingquarter. There are no bad debts.c. There is no beginning inventory of finished goods. Optima…arrow_forward

- Optima Company is a high-technology organization that produces a mass-storage system. The design of Optima’s system is unique and represents a breakthrough in the industry. The units Optima produces combine positive features of both compact and hard disks. The company is completing its fifth year of operations and is preparing to build its master budget for the coming year (2019). The budget will detail each quarter’s activity and the activity for the year in total. The master budget will be based on the following information: a. Fourth-quarter sales for 2018 are 55,000 units. b. Unit sales by quarter (for 2018) are projected as follows: First quarter 65,000 Second quarter 70,000 Third quarter 75,000 Fourth quarter 90,000 The selling price is $400 per unit. All sales are credit sales. Optima collects 85 percent of all sales within the quarter in which they are realized; the other 15 percent is collected in the following quarter. There are no bad debts. c. There is no beginning…arrow_forwardOptima Company is a high-technology organization that produces a mass-storage system. The design of Optima’s system is unique and represents a breakthrough in the industry. The units Optima produces combine positive features of both compact and hard disks. The company is completing its fifth year of operations and is preparing to build its master budget for the coming year (2019). The budget will detail each quarter’s activity and the activity for the year in total. The master budget will be based on the following information: a. Fourth-quarter sales for 2018 are 55,000 units. b. Unit sales by quarter (for 2018) are projected as follows: First quarter 65,000 Second quarter 70,000 Third quarter 75,000 Fourth quarter 90,000 The selling price is $400 per unit. All sales are credit sales. Optima collects 85 percent of all sales within the quarter in which they are realized; the other 15 percent is collected in the following quarter. There are no bad debts. c. There is no beginning…arrow_forwardOptima Company is a high-technology organization that produces a mass-storage system. The design of Optima’s system is unique and represents a breakthrough in the industry. The units Optima produces combine positive features of both compact and hard disks. The company is completing its fifth year of operations and is preparing to build its master budget for the coming year (2019). The budget will detail each quarter’s activity and the activity for the year in total. The master budget will be based on the following information: a. Fourth-quarter sales for 2018 are 55,000 units. b. Unit sales by quarter (for 2018) are projected as follows: First quarter 65,000 Second quarter 70,000 Third quarter 75,000 Fourth quarter 90,000 The selling price is $400 per unit. All sales are credit sales. Optima collects 85 percent of all sales within the quarter in which they are realized; the other 15 percent is collected in the following quarter. There are no bad debts. c. There is no beginning…arrow_forward

- The management team at Rawlins Corporation is capitalizing on the trend for live-edge cedar fireplace mantels- beautiful, simple, organic. In fact, sales are so strong they are running out of inventory. This means that budgeting for next year will be extremely important, to ensure sure that Rawlins can source enough cedar. With budgeted sales as the starting point for the entire process, the management team agrees that the following levels present the most likely scenario for the first five months of the upcoming year. Budgeted number of materials to be sold, Jan-400, Feb- 425, March- 440, April- 430, May- 450. In addition to sales volume, many other specifics are required in order to complete the company's operating budgets. Key details associated with prices, costs, and usage are as follows: Budgeted selling price is 500/per mantel. Each mantel measures 3inches x 12inches x 4ft. Target ending inventory of finished mantels is 20% of next month's budgeted sales. However, beginning…arrow_forwardThe management team at Nash Corporation is capitalizing on the trend for live-edge cedar fireplace mantels—beautiful, simple, organic. In fact, sales are so strong they are running out of inventory. This means that budgeting for next year will be extremely important, to ensure sure that Nash can source enough cedar.With budgeted sales as the starting point for the entire process, the management team agrees that the following levels present the most likely scenario for the first five months of the upcoming year. January February March April May Budgeted number of mantels to be sold 380 420 430 410 460 In addition to sales volume, many other specifics are required in order to complete the company’s operating budgets. Key details associated with prices, costs, and usage are as follows. ● Budgeted selling price is $500 per mantel. Each mantel measures 3 inches × 12 inches × 4 feet. ● Target ending inventory of finished mantels is 20% of…arrow_forwardJay Rexford, president of Photo Artistry Company, was just concluding a budget meeting with his senior staff. It was November of 20x1, and the group was discussing preparation of the firm’s master budget for 20x2. “I've decided to go ahead and purchase the industrial robot we’ve been talking about. We’ll make the acquisition on January 2 of next year, and I expect it will take most of the year to train the personnel and reorganize the production process to take full advantage of the new equipment.” In response to a question about financing the acquisition, Rexford replied as follows: “The robot will cost $950,000. There will also be an additional $50,000 in ancillary equipment to be purchased. We’ll finance these purchases with a one‑year $1,000,000 loan from Shark Bank and Trust Company. I’ve negotiated a repayment schedule of four equal installments on the last day of each quarter. The interest rate will be 10 percent, and interest payments will be quarterly as well.” With…arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning