Concept explainers

Videos

Cost Data for Managerial Purposes

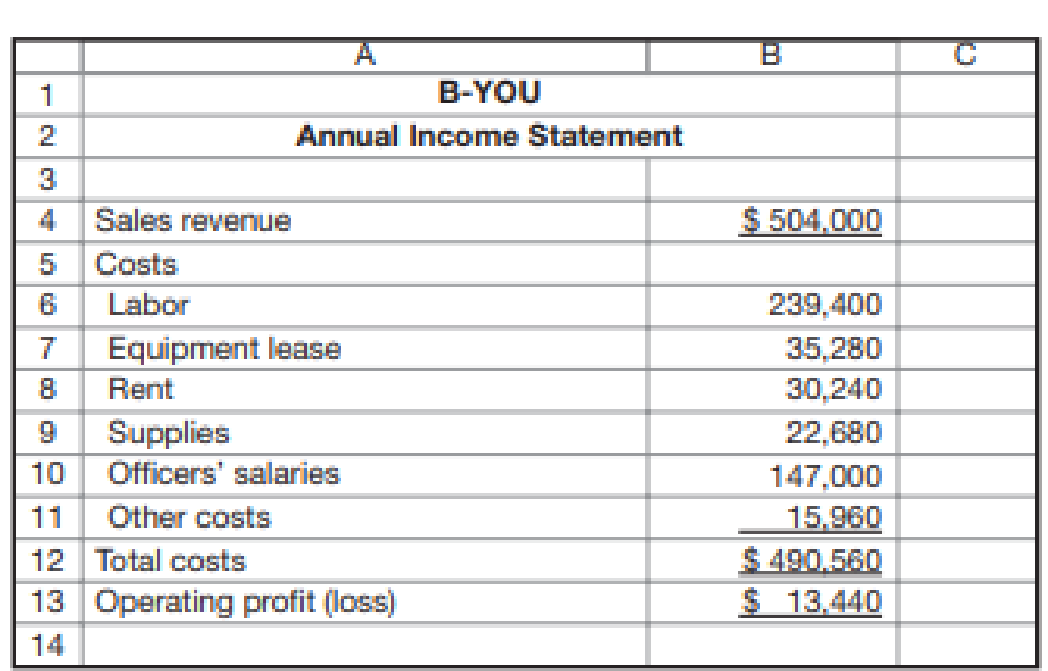

B-You is a consulting firm that works with managers to improve their interpersonal skills. Recently, a representative of a high-tech research firm approached B-You’s owner with an offer to contract for one year with B-You to improve the interpersonal skills of a newly hired manager. B-You reported the following costs and revenues during the past year:

If B-You decides to take the contract to help the manager, it will hire a full-time consultant at $85,000. Equipment lease will increase by 5 percent. Supplies will increase by an estimated 10 percent and other costs by 15 percent. The existing building has space for the new consultant. No new offices will be necessary for this work.

Required

- a. What are the differential costs that would be incurred as a result of taking the contract?

- b. If the contract will pay $90,000, should B-You accept it?

- c. What considerations, other than costs, do you think are necessary before making this decision?

Want to see the full answer?

Check out a sample textbook solution

Chapter 1 Solutions

FUNDAMENTALS OF COST ACCOUNTING BUNDLE

Additional Business Textbook Solutions

Financial Accounting, Student Value Edition (5th Edition)

Managerial Accounting: Tools for Business Decision Making

Horngren's Accounting (11th Edition)

Fundamentals of Financial Accounting

INTERMEDIATE ACCOUNTING

Financial Accounting: Tools for Business Decision Making, 8th Edition

- Cost Classification, Income Statement Gateway Construction Company, run by Jack Gateway, employs 25 to 30 people as subcontractors for laying gas, water, and sewage pipelines. Most of Gateways work comes from contracts with city and state agencies in Nebraska. The companys sales volume averages 3 million, and profits vary between 0 and 10% of sales. Sales and profits have been somewhat below average for the past 3 years due to a recession and intense competition. Because of this competition, Jack constantly reviews the prices that other companies bid for jobs. When a bid is lost, he analyzes the reasons for the differences between his bid and that of his competitors and uses this information to increase the competitiveness of future bids. Jack believes that Gateways current accounting system is deficient. Currently, all expenses are simply deducted from revenues to arrive at operating income. No effort is made to distinguish among the costs of laying pipe, obtaining contracts, and administering the company. Yet all bids are based on the costs of laying pipe. With these thoughts in mind, Jack looked more carefully at the income statement for the previous year (see below). First, he noted that jobs were priced on the basis of equipment hours, with an average price of 165 per equipment hour. However, when it came to classifying and assigning costs, he needed some help. One thing that really puzzled him was how to classify his own 114,000 salary. About half of his time was spent in bidding and securing contracts, and the other half was spent in general administrative matters. Required: 1. Classify the costs in the income statement as (1) costs of laying pipe (production costs), (2) costs of securing contracts (selling costs), or (3) costs of general administration. For production costs, identify direct materials, direct labor, and overhead costs. The company never has significant work in process (most jobs are started and completed within a day). 2. Assume that a significant driver is equipment hours. Identify the expenses that would likely be traced to jobs using this driver. Explain why you feel these costs are traceable using equipment hours. What is the cost per equipment hour for these traceable costs?arrow_forwardCommunication The controller of New Wave Sounds Inc. prepared the following product profitability report for management, using activity-based costing methods for allocating both the factory overhead and the marketing expenses. As such, the controller has confidence in the accuracy of this report. In addition, the controller interviewed the vice president of marketing, who provided the following insight into the companys three products: The home theater speakers are an older product that is highly recognized in the marketplace. The wireless speakers are a new product that was just recently launched. The wireless headphones are a new technology that has no competition in the marketplace, and it is hoped that they will become an important future addition to the companys product portfolio. Initial indications are that the product is well received by customers. The controller believes that the manufacturing costs for all three products are in line with expectations. Based on the information provided: 1. Calculate the ratio of gross profit to sales and the ratio of operating income to sales for each product. 2. Write a brief (one-page) memo using the product profitability report and the calculations in (a) to make recommendations to management with respect to strategies for the three products.arrow_forwardProduct costing and decision analysis for a service company Blue Star Airline provides passenger airline service, using small jets. The airline connects four major cities: Charlotte, Pittsburgh, Detroit, and San Francisco. The company expects to fly 170,000 miles during a month. The following costs are budgeted for a month: Blue Star management wishes to assign these costs to individual flights in order to gauge the profitability of its service offerings. The following activity bases were identified with the budgeted costs: The size of the companys ground operation in each city is determined by the size of the workforce. The following monthly data are available from corporate records for each terminal operation: Three recent representative flights have been selected for the profitability study. Their characteristics are as follows: Instructions Determine the fuel, crew, and depreciation cost per mile flown. Determine the cost per arrival or departure by terminal city. Use the information in (1) and (2) to construct a profitability report for the three flights. Each flight has a single arrival and departure to its origin and destination city pairs.arrow_forward

- Ventana Window and Wall Treatments Company provides draperies, shades, and various window treatments. Ventana works with the customer to design the appropriate window treatment, places the order, and installs the finished product. Direct materials and direct labor costs are easy to trace to the jobs. Ventanas income statement for last year is as follows: Ventana wants to find a markup on cost of goods sold that will allow them to earn about the same amount of profit on each job as was earned last year. Required: 1. What is the markup on cost of goods sold (COGS) that will maintain the same profit as last year? (Round the percentage to two significant digits.) 2. A customer orders draperies and shades for a remodeling job. The job will have the following costs: What is the price that Ventana will quote given the markup percentage calculated in Requirement 1? (Round the price to the nearest dollar.) 3. What if Ventana wants to calculate a markup on direct materials cost, since it is the largest cost of doing business? What is the markup on direct materials cost that will maintain the same profit as last year? (Round the percentage to two significant digits.) What is the bid price Ventana will use for the job given in Requirement 2 if the markup percentage is calculated on the basis of direct materials cost? (Round to the nearest dollar.)arrow_forwardFrom the following list of performance measures, label each one as Financial, Customer, Internal Business Processes, or Learning and Growth: Percentage of on-time deliveries Employee turnover ratio Revenue from new products Number of new customers Percentage of compensation based on team performance Percentage of products returned Operating income Time taken to replace defective productsarrow_forwardEthics and professional conduct in business Erin Haywood was recently hired as a cost analyst by Wind River Medical Supplies Inc. Oneof Erin’s first assignments was to perform a net present value analysis for a new warehouse.Et-in performed the analysis and calculated a present value index of 0.8. The plant manager.ZuhairBarbat, is very intent on purchasing the warehouse because he believes that more storage space is needed. Zuhair asks Erín into his office and the following conversation takes place: ZubairErín, you’re new here, aren’t you? EHii: Yes, sir. Zubair: V.dl, Erin, let me tell you something. ¡m not at all pleased with the capital investment analysis that you performed on this new warehouse. T need that warehouse for my production. If I dont get it, where am I going to place our output? Erín: Hopefully with the customer, sir. Zithair: Now don’t get smart with me. Erín: No, really. I was being serious. My analysis does not support constructing a new ware- house. The numbers don’t lie: the warehouse does not meet our investment return targets. In fact, it seems to me that purchasing a warehouse dots not add much value to the business. We need to be producing product to satisfy customer orders, not to fill a warehouse. Zubair Listen, you need to understand sonwthing. The headquarters people will not allow mv to build the warehouse if the numbers dont add up. You know as well as I that many assump tions go into your net present value analysis. Why don’t you relax some of your assumptions so that the f́nancial savings will offset the cost? Erín: I’m willing to discuss my assumptions with you. Maybe I overlooked something. Zubafr Good. Here’s what I want you to do. 1 see in your analysis tha you don’t project greater sales as a result of the warehouse. It seems to me, if we can store more goxLs, then will have more to sell. Thus, logically, a larger warehouse translates into more sales. If you incorporate this into your analysis, I think you’ll see that the numbers will work out. Why don’t you work it through and come back with a new analysis? I’m really counting on you on this one. Let’s get off to a good start together and see if we can get this project accepted. What is your advice to Erin?arrow_forward

- Suspicious Acquisition of Data, Ethical Issues Bill Lewis, manager of the Thomas Electronics Division, called a meeting with his controller, Brindon Peterson, and his marketing manager, Patty Fritz. The following is a transcript of the conversation that took place during the meeting: Bill: Brindon, the variable costing system that you developed has proved to be a big plus for our division. Our success in winning bids has increased, and as a result our revenues have increased by 25%. However, if we intend to meet this years profit targets, we are going to need something extraam I right, Patty? Patty: Absolutely. While we have been able to win more bids, we still are losing too many, particularly to our major competitor, Kilborn Electronics. If we knew more about their bidding strategy, we could be more successful at competing with them. Brindon: Would knowing their variable costs help? Patty: Certainly. It would give me their minimum price. With that knowledge, Im sure that we could find a way to beat them on several jobs, particularly on those jobs where we are at least as efficient. It would also help us to identify where we are not cost competitive. With this information, we might be able to find ways to increase our efficiency. Brindon: Well, I have good news. Ive been talking with Carl Penobscot, Kilborns assistant controller. Carl doesnt feel appreciated by Kilborn and wants to make a change. He could easily fit into our team here. Plus, Carl has been preparing for a job switch by quietly copying Kilborns accounting files and records. Hes already given me some data that reveal bids that Kilborn made on several jobs. If we can come to a satisfactory agreement with Carl, hell bring the rest of the information with him. Well easily be able to figure out Kilborns prospective bids and find ways to beat them. Besides, I could use another accountant on my staff. Bill, would you authorize my immediate hiring of Carl with a favorable compensation package? Bill: I know that you need more staff, Brindon, but is this the right thing to do? It sounds like Carl is stealing those files, and surely Kilborn considers this information confidential. I have real ethical and legal concerns about this. Why dont we meet with Laurie, our attorney, and determine any legal problems? Required: 1. Is Carls behavior ethical? What would Kilborn think? 2. Is Bill correct in supposing that there are ethical and/or legal problems involved with the hiring of Carl? (Reread the section on corporate codes of conduct in Chapter 1.) What would you do if you were Bill? Explain.arrow_forwardTypes of Responsibility Centers Consider each of the following independent scenarios: a. Terrin Belson, plant manager for the laser printer factory of Compugear Inc., brushed his hair back and sighed. December had been a bad month. Two machines had broken down, and some factory production workers (all on salary) were idled for part of the month. Materials prices increased, and insurance premiums on the factory increased. No way out of it; costs were going up. He hoped that the marketing vice president would be able to push through some price increases, but that really wasnt his department. b. Joanna Pauly was delighted to see that her ROI figures had increased for the third straight year. She was sure that her campaign to lower costs and use machinery more efficiently (enabling her factories to sell several older machines) was the reason why. Joanna planned to take full credit for the improvements at her semiannual performance review. c. Gil Rodriguez, sales manager for ComputerWorks, was not pleased with a memo from headquarters detailing the recent cost increases for the laser printer line. Headquarters suggested raising prices. Great, thought Gil, an increase in price will kill sales and revenue will go down. Why cant the plant shape up and cut costs like every other company in America is doing? Why turn this into my problem? d. Susan Whitehorse looked at the quarterly profit and loss statement with disgust. Revenue was down, and cost was upwhat a combination! Then she had an idea. If she cut back on maintenance of equipment and let a product engineer go, expenses would decreaseperhaps enough to reverse the trend in income. e. Shonna Lowry had just been hired to improve the fortunes of the Southern Division of ABC Inc. She met with top staff and hammered out a 3-year plan to improve the situation. A centerpiece of the plan is the retiring of obsolete equipment and the purchasing of state-of-the-art, computer-assisted machinery. The new machinery would take time for the workers to learn to use, but once that was done, waste would be virtually eliminated. Required: For each of the above independent scenarios, indicate the type of responsibility center involved (cost, revenue, profit, or investment).arrow_forwardThe controller of Emery, Inc. has computed quality costs as a percentage of sales for the past 5 years (20X1 was the first year the company implemented a quality improvement program). This information is as follows: Required: 1. Prepare a trend graph for total quality costs. Comment on what the graph has to say about the success of the quality improvement program. 2. Prepare a graph that shows the trend for each quality cost category. What does the graph have to say about the success of the quality improvement program? Does this graph supply more insight than the total cost trend graph does? 3. Prepare a graph that compares the trend in relative control costs versus relative failure costs. Comment on the significance of this trend.arrow_forward

- Analyze Horsepower Hookup, Inc. Horsepower Hookup, Inc., is a large automobile company that specializes in the production of high-powered trucks. The company is determining cost allocations for purposes of performance evaluation. A portion of company bonuses depends on divisions achieving cost management goals. This necessitates highly accurate support department cost allocation. Management has also stated that it has the means to implement as complex a method as necessary. The general manager over the Mid-Size D wants to get a good idea of what factors are driving the costs of the support departments in order to make accurate cost allocations, so finding accurate support department cost drivers is important. Support department costs include Janitorial (163,100) and Security (285,400). The Janitorial costs vary depending on the number of vehicles produced, increasing with larger production volumes. Security costs are fixed based on the size of the lot, and do not change with respect to how many vehicles are in the lot or warehouse. Joint costs involved in producing the trucks before the split-off point where the various makes, models, and colors are produced are 946,000 for the period. All makes, models, and colors sell at relatively similar margins, but the sports models and metallic colors are normally more difficult to produce during the joint production process. a. Which support department cost allocation method (direct, sequential, or reciprocal services) should be used to allocate support department cost? b. What driver would be best for allocating Janitorial costs? c. What driver would be best for allocating Security costs? d. If Janitorial costs were to be allocated based on square footage, and Security costs based on asset value, what percentage of each support departments costs would be allocated to each production department using the sequential method (allocating Security costs first) given the following: e. Should Janitorial and Security costs be considered when evaluating the performance of cost management employees? f. What joint cost allocation method should be used for performance evaluation purposes?arrow_forwardEthics in Action Danielle Hastings was recently hired as a cost analyst by CareNet Medical Supplies Inc. One of Danielles first assignments was to perform a net present value analysis for a new warehouse. Danielle performed the analysis and determined a present value index of 0.75. The plant manager, Jerrod Moore, is very intent on purchasing the warehouse because he believes that more storage space is needed. Jerrod asks Danielle into his office and the following conversation takes place: Jerrod: Danielle, youre new here, arent you? Danielle: Yes, I am. Jerrod: Well, Danielle, Im not at all pleased with the capital investment analysis that you performed on this new warehouse. I need that warehouse for my production. If I dont get it, where am I going to place our output? Danielle: Well, we need to get product into our customers hands. Jerrod: I agree, and we need a warehouse to do that. Danielle: My analysis does not support constructing a new warehouse. The numbers dont lie; the warehouse does not meet our investment return targets. In fact, it seems to me that purchasing a warehouse does not add much value to the business. We need to be producing product to satisfy customer orders, not to fill a warehouse. Jerrod: The headquarters people will not allow me to build the warehouse if the numbers dont add up. You know as well as I that many assumptions go into your net present value analysis. Why dont you relax some of your assumptions so that the financial savings will offset the cost? Danielle: Im willing to discuss my assumptions with you. Maybe I overlooked something. Jerrod: Good. Heres what I want you to do. I see in your analysis that you dont project greater sales as a result of the warehouse. It seems to me that if we can store more goods, then we will have more to sell. Thus, logically, a larger warehouse translates into more sales. If you incorporate this into your analysis, I think youll see that the numbers will work out. Why dont you work it through and come back with a new analysis. Im really counting on you on this one. Lets get off to a good start together and see if we can get this project accepted. What is your advice to Danielle?arrow_forwardCost Separation About 8 years ago, Kicker faced the problem of rapidly increasing costs associated with workplace accidents. The costs included the following: A safety program was implemented with the following features: hiring a safety director, new employee orientation, stretching required four times a day, and systematic monitoring of adherence to the program by directors and supervisors. A year later, the indicators were as follows: Required: 1. CONCEPTUAL CONNECTION Discuss the safety-related costs listed. Are they variable or fixed with respect to speakers sold? With respect to other independent variables (describe)? 2. CONCEPTUAL CONNECTION Did the safety program pay for itself? Discuss your reasoning.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning