Concept explainers

Videos

Prepare comparative income statement and comparative schedule of cost of goods sold for each month under (1) absorption costing method and (2) variable costing method.

Explanation of Solution

Absorption costing: It refers to the method of product costing in which the price of the product is calculated considering all fixed as well as the variable or direct costs. The

Variable costing: It refers to the method of product costing in which the price of the product is calculated considering only the variable or direct costs or the cost that happened to occurred due to the product only. It also called as marginal costing as it takes marginal costs while calculating the product cost.

Prepare comparative income statement and comparative schedule of cost of goods sold for each month under (1) absorption costing method and (2) variable costing method as follows:

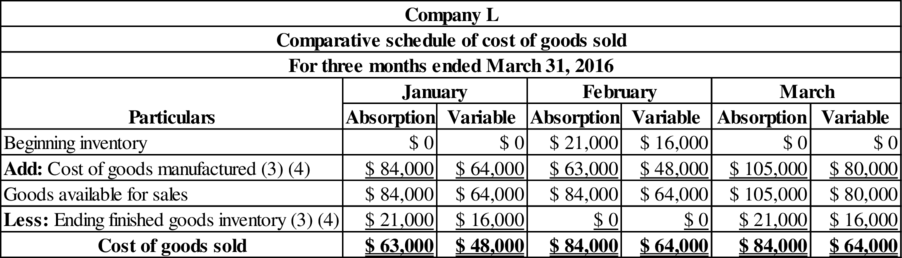

Comparative schedule of cost of goods sold for each month:

Table (1)

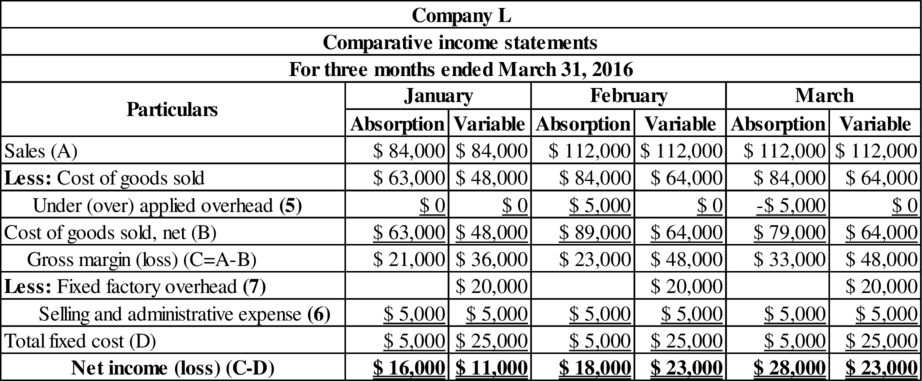

Comparative income statement for each month:

Table (2)

Working note (1):

Calculate the absorption costing per unit.

Working note (2):

Calculate the ending inventory units for each month.

| Particulars | January | February | March |

| Beginning inventory | 0 | 1,000 | 0 |

| Add: Number of units produced | 4,000 | 3,000 | 5,000 |

| Less: Number of units sold | 3,000 | 4,000 | 4,000 |

| Ending inventory | 1,000 | 0 | 1,000 |

Table (3)

Working note (3):

Calculate the cost of goods sold and ending inventory under absorption costing for each month.

| Particulars | January | February | March |

| Number of units produced (A) | 4,000 | 3,000 | 5,000 |

| Absorption cost per unit (B) (1) | $ 21 | $ 21 | $ 21 |

| Cost of goods manufactured | $ 84,000 | $ 63,000 | $ 105,000 |

| Ending inventories units (C) (2) | 1,000 | 0 | 1,000 |

| Absorption cost per unit (D) | $ 21 | $ 21 | $ 21 |

| Ending inventory | $ 21,000 | $ 0 | $ 21,000 |

| Beginning inventory units (E) (2) | 0 | 1,000 | 0 |

| Absorption cost per unit (F) | $ 21 | $ 21 | $ 21 |

| Beginning inventory | $ 0 | $ 21,000 | $ 0 |

Table (4)

Working note (4):

Calculate the cost of goods sold and ending inventory under variable costing for each month.

| Particulars | January | February | March |

| Number of units produced (A) | 4,000 | 3,000 | 5,000 |

| Variable cost per unit (B) | $ 16 | $ 16 | $ 16 |

| Cost of goods manufactured | $ 64,000 | $ 48,000 | $ 80,000 |

| Ending inventories units (C) (2) | 1,000 | 0 | 1,000 |

| Variable cost per unit (D) | $ 16 | $ 16 | $ 16 |

| Ending inventory | $ 16,000 | $ 0 | $ 16,000 |

| Beginning inventory units (E) (2) | 0 | 1,000 | 0 |

| Variable cost per unit (F) | $ 16 | $ 16 | $ 16 |

| Beginning inventory | $ 0 | $ 16,000 | $ 0 |

Table (5)

Working note (5):

Calculate the under or over applied fixed overhead.

January:

February:

March:

Working note (6):

Calculate the fixed selling and administrative expense per month.

Working note (7):

Calculate the fixed factory overhead per month.

Want to see more full solutions like this?

Chapter 10 Solutions

PRINCIPLES OF COST ACCOUNTING

- Using the information in the previous exercises about Marleys Manufacturing, determine the operating income for department B, assuming department A sold department B 1,000 units during the month and department A reduces the selling price to the market price.arrow_forwardThe following data were adapted from a recent income statement of Caterpillar Inc. (CAT) for the year ended December 31: Assume that 8,500 million of cost of goods sold and 4,000 million of selling, administrative, and other expenses were fixed costs. Inventories at the beginning and end of the year were as follows: Also, assume that 30% of the beginning and ending inventories were fixed costs. a. Prepare an income statement according to the variable costing concept for Caterpillar Inc. Round numbers to nearest million. b. Explain the difference between the amount of operating income reported under the absorption costing and variable costing concepts. Round numbers to nearest million.arrow_forwardThe following production data came from the records of Olympic Enterprises for the year ended December 31, 2016: During the year, 40,000 units were manufactured but only 35,000 units were sold. Determine the effect on inventory valuation by computing the following: 1. Total inventoriable costs and the cost of the 35,000 units sold and of the 5,000 units in the ending inventory, using variable costing. 2. Total inventoriable costs and the cost of the 35,000 units sold and of the 5,000 units in the ending inventory, using absorption costing.arrow_forward

- At the end of the first year of operations, 21,500 units remained in the finished goods inventory. The unit manufacturing costs during the year were as follows: Determine the cost of the finished goods inventory reported on the balance sheet under (a) the absorption costing concept and (b) the variable costing concept.arrow_forwardPattison Products, Inc., began operations in October and manufactured 40,000 units during the month with the following unit costs: Fixed overhead per unit = 280,000/40,000 units produced = 7. Total fixed factory overhead is 280,000 per month. During October, 38,400 units were sold at a price of 24, and fixed marketing and administrative expenses were 130,500. Required: 1. Calculate the cost of each unit using absorption costing. 2. How many units remain in ending inventory? What is the cost of ending inventory using absorption costing? 3. Prepare an absorption-costing income statement for Pattison Products, Inc., for the month of October. 4. What if November production was 40,000 units, costs were stable, and sales were 41,000 units? What is the cost of ending inventory? What is operating income for November?arrow_forwardIncome Statements under Absorption and Variable Costing In the coming year, Kalling Company expects to sell 28,700 units at 32 each. Kallings controller provided the following information for the coming year: Required: 1. Calculate the cost of one unit of product under absorption costing. 2. Calculate the cost of one unit of product under variable costing. 3. Calculate operating income under absorption costing for next year. 4. Calculate operating income under variable costing for next year.arrow_forward

- Click the Chart sheet tab. On the screen is a column chart showing ending inventory costs. During a deflationary period, which bar (A, B, or C) represents FIFO costing, which represents LIFO costing, and which represents weighted average? Explain your reasoning. On January 4 following year-end, Rio Enterprises received a shipment of 60 units of product costing 580 each. These units had been ordered by Del in December and had been shipped to him on December 27. They were shipped FOB shipping point. Revise the FIFOLIFO3 worksheet to include this shipment. Preview the printout to make sure that the worksheet will print neatly on one page, and then print the worksheet. Save the completed file as FIFOLIFOT. Using the FIFOLIFO3 file, prepare a 3-D bar (stacked) chart showing the cost of goods sold and ending inventory under each of the four inventory cost flow assumptions. No Chart Data Table is needed. Use the values in the Calculations Section of the worksheet for your chart. Enter your name somewhere on the chart. Save the file again as FIFOLIFO3. Print the chart.arrow_forwardLast year, Orsen Company produced 25,000 juicers and sold 26,500 juicers for 60 each. The actual variable unit cost is as follows: Fixed overhead was 320,000. Fixed selling expenses consisted of advertising copayments totaling 110,000. Fixed administrative expenses were 236,000. There were no beginning and ending work-in-process inventories. Beginning finished goods inventory was 148,000 for 4,000 juicers. The value of ending inventory reported on the financial statements was Refer to the information in 2.24. The gross margin percentage for last year was a. 12.57% b. 55.67% c. 28.95% d. 38.33%arrow_forwardEstimated income statements, using absorption and variable costing Prior to the first month of operations ending October 31, Marshall Inc. estimated the following operating results: The company is evaluating a proposal to manufacture 50,000 units instead of 40,000 units, thus creating an ending inventory of 10,000 units. Manufacturing the additional units will not change sales, unit variable factory overhead costs, total fixed factory overhead cost, or total selling and administrative expenses. a. Prepare an estimated income statement, comparing operating results if 40,000 and 50,000 units are manufactured in (1) the absorption costing format and (2) the variable costing format. b. What is the reason for the difference in operating income reported for the two levels of production by the absorption costing income statement?arrow_forward

- The following information pertains to Vladamir, Inc., for last year: There are no work-in-process inventories. Normal activity is 100,000 units. Expected and actual overhead costs are the same. Costs have not changed from one year to the next. Required: 1. How many units are in ending inventory? 2. Without preparing an income statement, indicate what the difference will be between variable-costing income and absorption-costing income. 3. Assume the selling price per unit is 29. Prepare an income statement using (a) variable costing and (b) absorption costing.arrow_forwardPotter Company has installed a JIT purchasing and manufacturing system and is using back-flush accounting for its cost flows. It currently uses a two-trigger approach with the purchase of materials as the first trigger point and the completion of goods as the second trigger point. During the month of June, Potter had the following transactions: 40,500 labor plus 222,750 overhead. There were no beginning or ending inventories. All goods produced were sold with a 60 percent markup. Any variance is closed to Cost of Goods Sold. (Variances are recognized monthly.) Required: Prepare the journal entries for the month of June using backflush costing, assuming that Potter uses the sale of goods as the second trigger point instead of the completion of goods.arrow_forwardFlaherty, Inc., has just completed its first year of operations. The unit costs on a normal costing basis are as follows: During the year, the company had the following activity: Actual fixed overhead was 12,000 less than budgeted fixed overhead. Budgeted variable overhead was 5,000 less than the actual variable overhead. The company used an expected actual activity level of 12,000 direct labor hours to compute the predetermined overhead rates. Any overhead variances are closed to Cost of Goods Sold. Required: 1. Compute the unit cost using (a) absorption costing and (b) variable costing. 2. Prepare an absorption-costing income statement. 3. Prepare a variable-costing income statement. 4. Reconcile the difference between the two income statements.arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College