Videos

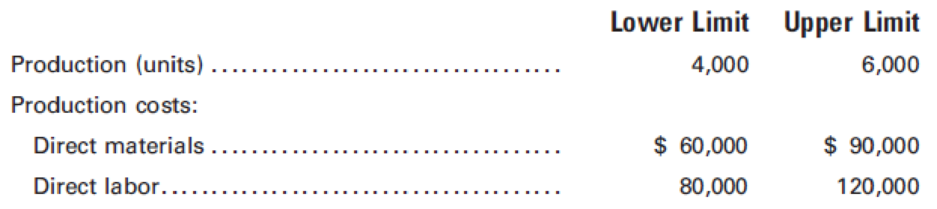

Grand Canyon Manufacturing Inc. produces and sells a product with a price of $100 per unit. The following cost data have been prepared for its estimated upper and lower limits of activity:

Overhead:

Selling and administrative expenses:

Required:

- 1. Classify each cost element as either variable, fixed, or semi-variable. (Hint: Recall that variable expenses must go up in direct proportion to changes in the volume of activity.)

- 2. Calculate the break-even point in units and dollars. (Hint: First use the high-low method illustrated in Chapter 4 to separate costs into their fixed and variable components.)

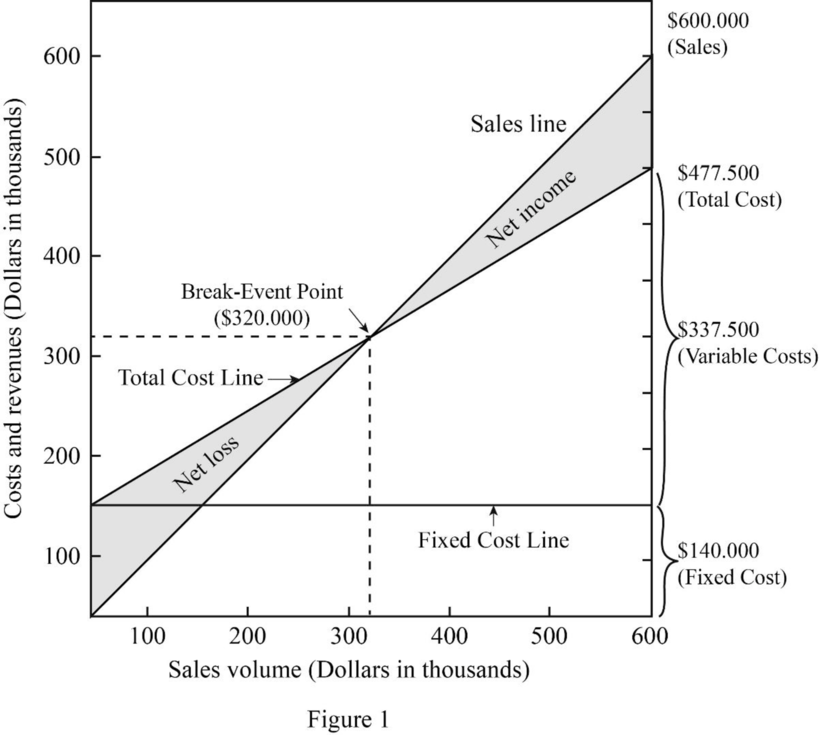

- 3. Prepare a break-even chart.

- 4. Prepare a contribution income statement, similar in format to the statement appearing on page 540, assuming sales of 5,000 units.

- 5. Recompute the break-even point in units, assuming that variable costs increase by 20% and fixed costs are reduced by $50,000.

1.

Classify the each cost element as either variable, fixed or semi-variable.

Explanation of Solution

Classify the each cost element as either variable, fixed or semi-variable as follows:

- Variable costs vary with the number of units produced or for the services provided. For example, the labor costs increase if the number of labor hours is increased, and the labor costs decrease if the number of labor hours is decreased. Direct material, direct labor and indirect material are considered as the variable costs.

- Fixed Cost is a cost which is constant in the short run, it is not related to any change in the production of goods or service, it will be fixed disregarding of increase or decrease in output. Fixed cost is generally incurred on fixed assets in long run. Depreciation, office salary and advertising are considered as the fixed cost.

- Semi variable costs are the cost that changes based on the changes in the production, but it is not proportionately. Indirect labor, sales salaries and other expense are considered as semi-variable cost.

2.

Calcualte the break even point in units and dollars.

Explanation of Solution

Calcualte the break even point in units and dollars as follows:

Working note (1):

Calcualte the vairable cost per unit:

Working note (2):

Calculate the variable cost for 4,000 units.

Working note (3):

Calcualte the fixed cost:

3.

Prepare a break-even chart.

Explanation of Solution

Prepare a break-even chart as follows:

4.

Prepare a contribution income statement of company G.

Explanation of Solution

Prepare a contribution income statement of company G as follows:

| Company G | |

| Income statement | |

| For the year ended --- | |

| Particulars | Amount ($) |

| Sales | $ 500,000 |

| Less: Variable cost | $281,250 |

| Contribution margin | $218,250 |

| Less: Fixed costs (3) | $140,000 |

| Net operating income | $ 78,750 |

Table (1)

5.

Calculate the break-even point in units, assume that the variable costs is increased by 20% and fixed cost is decreased by $50,000.

Explanation of Solution

Calculate the break-even point in units, assume that the variable costs is increased by 20% and fixed cost is decreased by $50,000 as follows:

Working note (4):

Calcualte the decrase in fixed cost:

Working note (5):

Calcualte the increase in variable cost:

Want to see more full solutions like this?

Chapter 10 Solutions

PRINCIPLES OF COST ACCOUNTING

Additional Business Textbook Solutions

INTERMEDIATE ACCOUNTING

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Cost Accounting (15th Edition)

Managerial Accounting: Tools for Business Decision Making

Intermediate Accounting

Introduction To Managerial Accounting

- Baxter Company has a relevant range of production between 15,000 and 30,000 units. The following cost data represents average variable costs per unit for 25,000 units of production. Using the costs data from Rose Company, answer the following questions: A. If 15,000 units are produced, what is the variable cost per unit? B. If 28,000 units are produced, what is the variable cost per unit? C. If 21,000 units are produced, what are the total variable costs? D. If 29,000 units are produced, what are the total variable costs? E. If 17,000 units are produced, what are the total manufacturing overhead costs incurred? F. If 23,000 units are produced, what are the total manufacturing overhead costs incurred? G. If 30,000 units are produced, what are the per unit manufacturing overhead costs incurred? H. If 15,000 units are produced, what are the per unit manufacturing overhead costs incurred?arrow_forwardRose Company has a relevant range of production between 10,000 and 25.000 units. The following cost data represents average cost per unit for 15,000 units of production. Using the cost data from Rose Company, answer the following questions: If 10,000 units are produced, what is the variable cost per unit? If 18,000 units are produced, what is the variable cost per unit? If 21,000 units are produced, what are the total variable costs? If 11,000 units are produced, what are the total variable costs? If 19,000 units are produced, what are the total manufacturing overhead costs incurred? If 23,000 units are produced, what are the total manufacturing overhead costs incurred? If 19,000 units are produced, what are the per unit manufacturing overhead costs incurred? If 25,000 units are produced, what are the per unit manufacturing overhead costs incurred?arrow_forwardA company has prepared the following statistics regarding its production and sales at different capacity levels. Total costs: 1. At what point is break-even reached in sales dollars? In units? (Hint: Use the capacity level to determine the number of units.) 2. If the company is operating at 60% capacity, should it accept an offer from a customer to buy 10,000 units at 3 per unit?arrow_forward

- Flaherty, Inc., has just completed its first year of operations. The unit costs on a normal costing basis are as follows: During the year, the company had the following activity: Actual fixed overhead was 12,000 less than budgeted fixed overhead. Budgeted variable overhead was 5,000 less than the actual variable overhead. The company used an expected actual activity level of 12,000 direct labor hours to compute the predetermined overhead rates. Any overhead variances are closed to Cost of Goods Sold. Required: 1. Compute the unit cost using (a) absorption costing and (b) variable costing. 2. Prepare an absorption-costing income statement. 3. Prepare a variable-costing income statement. 4. Reconcile the difference between the two income statements.arrow_forwardThe management of Hartman Company is trying to determine the amount of each of two products to produce over the coming planning period. The following information concerns labor availability, labor utilization, and product profitability: a. Develop a linear programming model of the Hartman Company problem. Solve the model to determine the optimal production quantities of products 1 and 2. b. In computing the profit contribution per unit, management does not deduct labor costs because they are considered fixed for the upcoming planning period. However, suppose that overtime can be scheduled in some of the departments. Which departments would you recommend scheduling for overtime? How much would you be willing to pay per hour of overtime in each department? c. Suppose that 10, 6, and 8 hours of overtime may be scheduled in departments A, B, and C, respectively. The cost per hour of overtime is 18 in department A, 22.50 in department B, and 12 in department C. Formulate a linear programming model that can be used to determine the optimal production quantities if overtime is made available. What are the optimal production quantities, and what is the revised total contribution to profit? How much overtime do you recommend using in each department? What is the increase in the total contribution to profit if overtime is used?arrow_forwardCool Pool has these costs associated with production of 20,000 units of accessory products: direct materials, $70; direct labor, $110; variable manufacturing overhead, $45; total fixed manufacturing overhead, $800,000. What is the cost per unit under both the variable and absorption methods?arrow_forward

- The profit function for two products is: Profit3x12+42x13x22+48x2+700, where x1 represents units of production of product 1, and x2 represents units of production of product 2. Producing one unit of product 1 requires 4 labor-hours, and producing one unit of product 2 requires 6 labor-hours. Currently, 24 labor-hours are available. The cost of labor-hours is already factored into the profit function, but it is possible to schedule overtime at a premium of 5 per hour. a. Formulate an optimization problem that can be used to find the optimal production quantity of products 1 and 2 and the optimal number of overtime hours to schedule. b. Solve the optimization model you formulated in part (a). How much should be produced and how many overtime hours should be scheduled?arrow_forwardIdentify cost graphs The following cost graphs illustrate various types of cost behavior: For each of the following costs, identify the cost graph that best illustrates its cost behavior as the number of units produced increases: A. Total direct materials cost B. Electricity costs of 1,000 per month plus 0.10 per kilowatt-hour C. Per-unit cost of straight-line depreciation on factory equipment D. Salary of quality control supervisor, 20,000 per month E. Per-unit direct labor costarrow_forwardTotal costs for ABC Distributing are $250,000 when the activity level is 10,000 units. If variable costs are $5 per unit, what are their fixed costs? $240,000 $200,000 $260,000 Their fixed costs cannot be determined from the information presented.arrow_forward

- The following information pertains to Vladamir, Inc., for last year: There are no work-in-process inventories. Normal activity is 100,000 units. Expected and actual overhead costs are the same. Costs have not changed from one year to the next. Required: 1. How many units are in ending inventory? 2. Without preparing an income statement, indicate what the difference will be between variable-costing income and absorption-costing income. 3. Assume the selling price per unit is 29. Prepare an income statement using (a) variable costing and (b) absorption costing.arrow_forwardManatoah Manufacturing produces 3 models of window air conditioners: model 101, model 201, and model 301. The sales price and variable costs for these three models are as follows: The current product mix is 4:3:2. The three models share total fixed costs of $430,000. Calculate the sales price per composite unit. What is the contribution margin per composite unit? Calculate Manatoahs break-even point in both dollars and units. Using an income statement format, prove that this is the break-even point.arrow_forwardThe total cost for monthly supervisory cost in a factory is 4,500 regardless of how many hours the supervisor works or the quantity of output achieved. This cost a. is strictly variable. b. is strictly fixed. c. is a mixed cost. d. is a step cost. e. cannot be determined from this information.arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning