Concept explainers

Videos

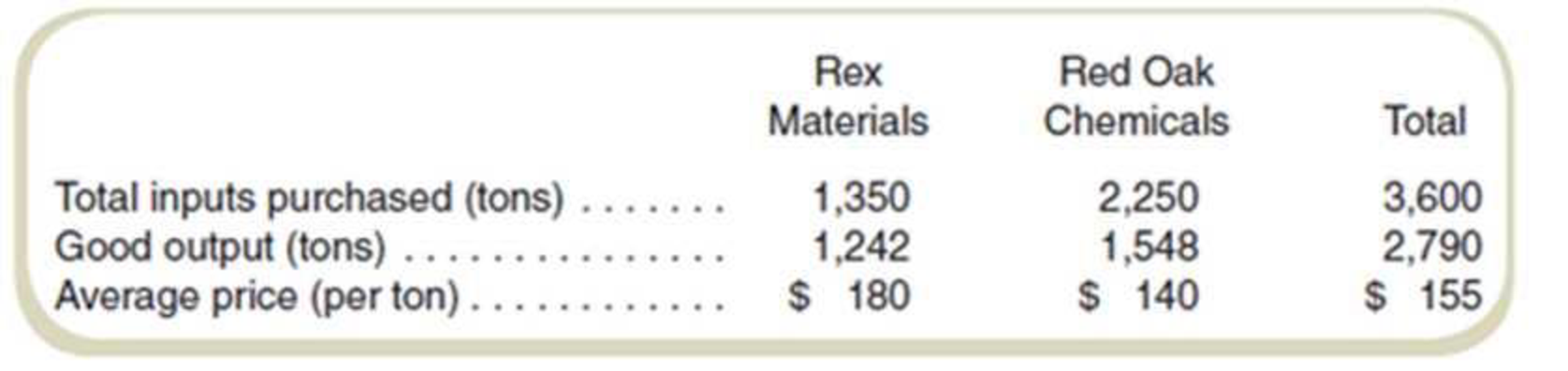

Activity-Based Costing of Suppliers

JFI Foods produces processed foods. Its basic ingredient is a feedstock that is mixed with other ingredients to produce the final packaged product. JFI purchases the feedstock from two suppliers, Rex Materials and Red Oak Chemicals. The quality of the final product depends directly on the quality of the feedstock. If the feedstock is not correct, JFI has to dispose of the entire batch. All feedstock in this business is occasionally “bad.” so JFI measures what it calls the “yield,” which is measured as

Yield = Good output ÷ Input

where the output and inputs are both measured in tons. As a benchmark. JFI expects to get 8 tons of good output for every 10 tons of feedstock purchased for a yield of 80 percent (= 8 tons of output ÷ 10 tons of feedstock).

Data on the two suppliers for the past year follow:

Required

Assume that the average quality, measured by the yield, and prices from the two companies will continue as in the past. What is the effective price for feedstock from the two companies when quality is considered?

Want to see the full answer?

Check out a sample textbook solution

Chapter 10 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Determining cost relationships Midst ate Containers Inc. manufactures cans for the canned food industry. The operations manager of a can manufacturing operation wants to conduct a cost study investigating the relationship of tin content in the material (can stock) to the energy cost for enameling the cans. The enameling was necessary to prepare the cans for labeling. A higher percentage of tin content in the can stock increases the cost of material. The operations manager believed that a higher tin content in the can stock would reduce the amount of energy used in enameling. During the analysis period, the amount of tin content in the steel can stock was increased for every month, from April to September. The following operating reports were available from the controller: Differences in materials unit costs were entirely related to the amount of tin content. In addition, inventory changes are negligible and are ignored in the analysis. Interpret this information and report to the operations manager your recommendations with respect to tin content.arrow_forwardProducts versus Services, Cost Assignment Holmes Company produces wooden playhouses. When a customer orders a playhouse, it is delivered in pieces with detailed instructions on how to put it together. Some customers prefer that Holmes put the playhouse together. Therefore, these customers purchase the playhouse, as well as pay an additional fee for Holmes to install the playhouse. Holmes then pulls two workers off the production line and sends them to construct the playhouse on site. Required: 1. What two products does Holmes sell? Classify each one as a product or a service. 2. CONCEPTUAL CONNECTION Do you think Holmes assigns costs individually to each product or service? Why or why not? 3. CONCEPTUAL CONNECTION Describe the opportunity cost of the installation process.arrow_forwardActivity-based costing and product cost distortion The management of Four Finger Appliance Company in Exercise 14 has asked you to use activity-based costing instead of direct labor hours to allocate factory overhead costs to the two products. You have determined that 81,000 of factory overhead from each of the production departments can be associated with setup activity (162,000 in total). Company records indicate that blenders required 135 setups, while the toaster ovens required only 45 setups. Each product has a production volume of 7,500 units. Determine the three activity rates (assembly, test and pack, and setup). Determine the total factory overhead and factory overhead per unit allocated to each product using the activity rates in (A).arrow_forward

- Analyzing process cost elements across product types Mystic Bottling Company bottles popular beverages in the Bottling Department. The beverages are produced by blending concentrate with water and sugar. The concentrate is purchased from a concentrate producer. The concentrate producer sets higher prices for the more popular concentrate flavors. A simplified Bottling Department cost of production report separating the cost of bottling the four flavors follows: Beginning and ending work in process inventories are negligible, so they are omitted from the cost of production report. The flavor changeover cost represents the cost of cleaning the bottling machines between production runs of different flavors. A production ran of a new flavor is produced after a flavor changeover from the previous flavor. Higher-demand flavors are produced in larger production runs, while smaller-demand flavors are produced in smaller production runs. Prepare a memo to the production manager, analyzing this comparative cost information. In your memo, provide recommendations for further action, along with supporting schedules showing the total cost per case and cost per case by cost element. Round supporting calculations to the nearest cent.arrow_forwardSouthward Company has implemented a JIT flexible manufacturing system. John Richins, controller of the company, has decided to reduce the accounting requirements given the expectation of lower inventories. For one thing, he has decided to treat direct labor cost as a part of overhead and to discontinue the detailed direct labor accounting of the past. The company has created two manufacturing cells, each capable of producing a family of products: the radiator cell and the water pump cell. The output of both cells is sold to a sister division and to customers who use the radiators and water pumps for repair activity. Product-level overhead costs outside the cells are assigned to each cell using appropriate drivers. Facility-level costs are allocated to each cell on the basis of square footage. The budgeted direct labor and overhead costs are as follows: The predetermined conversion cost rate is based on available production hours in each cell. The radiator cell has 45,000 hours available for production, and the water pump cell has 27,000 hours. Conversion costs are applied to the units produced by multiplying the conversion rate by the actual time required to produce the units. The radiator cell produced 81,000 units, taking 0.5 hour to produce one unit of product (on average). The water pump cell produced 90,000 units, taking 0.25 hour to produce one unit of product (on average). Other actual results for the year are as follows: All units produced were sold. Any conversion cost variance is closed to Cost of Goods Sold. Required: 1. Calculate the predetermined conversion cost rates for each cell. 2. Prepare journal entries using backflush accounting. Assume two trigger points, with completion of goods as the second trigger point. 3. Repeat Requirement 2, assuming that the second trigger point is the sale of the goods. 4. Explain why there is no need to have a work-in-process inventory account. 5. Two variants of backflush costing were presented in which each used two trigger points, with the second trigger point differing. Suppose that the only trigger point for recognizing manufacturing costs occurs when the goods are sold. How would the entries be listed here? When would this backflush variant be considered appropriate?arrow_forwardFunctional-Based versus Activity-Based Costing For years, Tamarindo Company produced only one product: backpacks. Recently, Tamarindo added a line of duffel bags. With this addition, the company began assigning overhead costs by using departmental rates. (Prior to this, the company used a predetermined plantwide rate based on units produced.) Surprisingly, after the addition of the duffel-bag line and the switch to departmental rates, the costs to produce the backpacks increased, and their profitability dropped. Josie, the marketing manager, and Steve, the production manager, both complained about the increase in the production cost of backpacks. Josie was concerned because the increase in unit costs led to pressure to increase the unit price of backpacks. She was resisting this pressure because she was certain that the increase would harm the companys market share. Steve was receiving pressure to cut costs also, yet he was convinced that nothing different was being done in the way the backpacks were produced. After some discussion, the two managers decided that the problem had to be connected to the addition of the duffel-bag line. Upon investigation, they were informed that the only real change in product-costing procedures was in the way overhead costs are assigned. A two-stage procedure was now in use. First, overhead costs are assigned to the two producing departments, Patterns and Finishing. Second, the costs accumulated in the producing departments are assigned to the two products by using direct labor hours as a driver (the rate in each department is based on direct labor hours). The managers were assured that great care was taken to associate overhead costs with individual products. So that they could construct their own example of overhead cost assignment, the controller provided them with the information necessary to show how accounting costs are assigned to products: The controller remarked that the cost of operating the accounting department had doubled with the addition of the new product line. The increase came because of the need to process additional transactions, which had also doubled in number. During the first year of producing duffel bags, the company produced and sold 100,000 backpacks and 25,000 duffel bags. The 100,000 backpacks matched the prior years output for that product. Required: (Note: Round rates and unit cost to the nearest cent.) 1. CONCEPTUAL CONNECTION Compute the amount of accounting cost assigned to a backpack before the duffel-bag line was added by using a plantwide rate approach based on units produced. Is this assignment accurate? Explain. 2. Suppose that the company decided to assign the accounting costs directly to the product lines by using the number of transactions as the activity driver. What is the accounting cost per unit of backpacks? Per unit of duffel bags? 3. Compute the amount of accounting cost assigned to each backpack and duffel bag by using departmental rates based on direct labor hours. 4. CONCEPTUAL CONNECTION Which way of assigning overhead does the best jobthe functional-based approach by using departmental rates or the activity-based approach by using transactions processed for each product? Explain. Discuss the value of ABC before the duffel-bag line was added.arrow_forward

- Variable and Fixed Costs What follows are a number of resources that are used by a manufacturer of futons. Assume that the output measure or cost driver is the number of futons produced. All direct labor is paid on an hourly basis, and hours worked can be easily changed by management. All other factory workers are salaried. a. Power to operate a drill (to drill holes in the wooden frames of the futons) b. Cloth to cover the futon mattress c. Salary of the factory receptionist d. Cost of food and decorations for the annual Fourth of July party for all factory employees e. Fuel for a forklift used to move materials in a factory f. Depreciation on the factory g. Depreciation on a forklift used to move partially completed goods h. Wages paid to workers who assemble the futon frame i. Wages paid to workers who maintain the factory equipment j. Cloth rags used to wipe the excess stain off the wooden frames Required: Classify the resource costs as variable or fixed.arrow_forwardActivity-Based Supplier Costing Bowman Company manufactures cooling systems. Bowman produces all the parts necessary for its product except for one electronic component, which is purchased from two local suppliers: Manzer Inc. and Buckner Company. Both suppliers are reliable and seldom deliver late; however, Manzer sells the component for $89 per unit, while Buckner sells the same component for $86. Bowman purchases 80% of its components from Buckner because of its lower price. The total annual demand is 4,000,000 components. To help assess the cost effect of the two components, the following data were collected for supplier-related activities and suppliers: I. Activity Data Activity Cost Inspecting components (sampling only) $605,000 Reworking products (due to failed component) 7,570,000 Warranty work (due to failed component) 10,270,000 II. Supplier Data Manzer Inc. Buckner Company Unit purchase price $89 $86 Units purchased 800,000 3,200,000 Sampling hours*…arrow_forwardSupport Activity Cost Allocation Kizzle’s Crepes Co. produces world famous crepes. The company’s crepes are produced via its Mixing and Cooking activities, which both rely on the Janitorial and Maintenance activities. Kizzle’s management knows the most practical driver of Janitorial costs is square feet, but is uncertain whether to allocate Maintenance costs based on asset value of production equipment, number of service calls, or machine hours. Kizzle’s management estimates that the Cooking and Mixing activities each require about twice as much space as the Maintenance activity. 1. Identify the base for choosing the cost driver. a. The company needs to choose a driver that can be measured practically. b. The company needs to choose the driver that matches the department activity. c. The company needs to choose the driver that matches the support department function. d. All the above. Identify the driver which cannot be used as cost driver for maintenance cost. a. Square feet. b.…arrow_forward

- Mystic Bottling Company bottles popular beverages in the Bottling Department. The beverages are produced by blending concentrate with water and sugar. The concentrate is purchased from a concentrate producer. The concentrate producer sets higher prices for the more popular concentrate flavors. A simplified Bottling Department cost of production report separating the cost of bottling the four flavors follows: Attachment Beginning and ending work in process inventories are negligible, so they are omitted from the cost of production report. The flavor changeover cost represents the cost of cleaning the bottling machines between production runs of different flavors. Prepare a memo to the production manager, analyzing this comparative cost information. In your memo, provide recommendations for further action, along with supporting schedules showing the total cost per case and cost per case by cost element.Round all supporting calculations to the nearest cent.arrow_forwardEngineering LLC is facing a cost issues in their production department. The Production manager of Al Maha Engineering LLC wants to adopt standard costing in their company to tackle cost issues. He wants know the meaning of standard cost of a product. Which of the following statement is the meaning of standard cost of a product? a. The average unit cost of products produced during a particular period. b. The average unit cost of products produced in the previous period. c. The unit cost of products incurred at the start of a particular period. d. The planned unit cost of products produced during a particular period.arrow_forwardDK manufactures three products, W, X and Y. Each product uses the same materials and the same type of direct labour but in different quantities. The company currently uses a cost plus basis to determine the selling price of its products. This is based on full cost using an overhead absorption rate per direct labour hour. However, the managing director is concerned that the company may be losing sales because of its approach to setting prices. He thinks that a marginal costing approach may be more appropriate, particularly since the workforce is guaranteed a minimum weekly wage and has a three month notice period. Required: a) Given the managing director’s concern about DK’s approach to setting selling prices, discuss the advantages and disadvantages of marginal cost plus pricing AND total cost-plus pricing.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning