Concept explainers

Videos

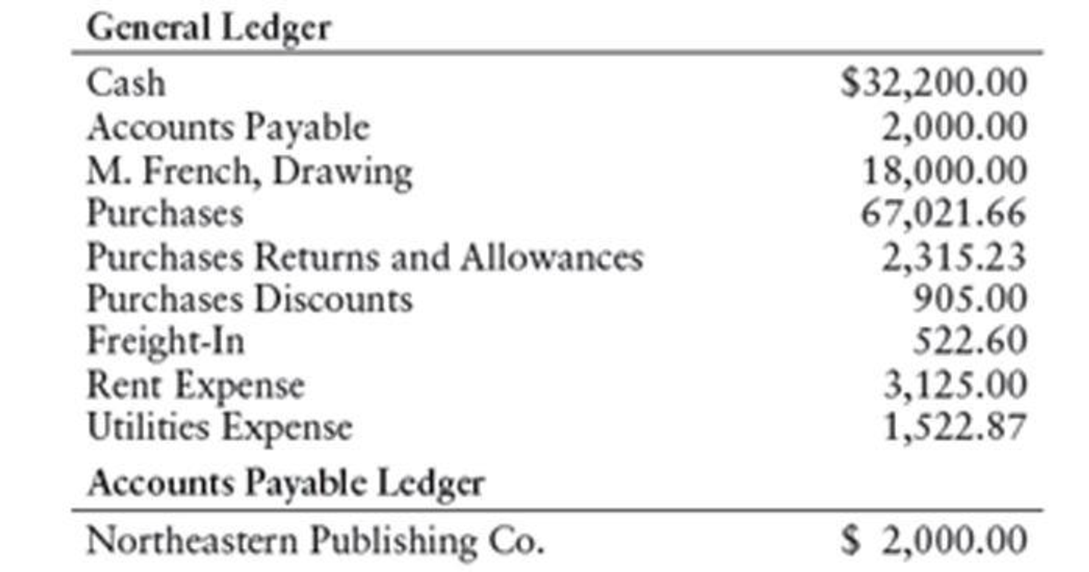

Michelle French owns and operates Books and More, a retail book store. Selected account balances on June 1 are as follows:

The following purchases and cash payments transactions took place during the month of June:

June 1 Purchased books on account from Irving Publishing Company, $2,100. Invoice No. 101, terms 2/10, n/30, FOB destination.

2 Issued Cheek No. 300 to Northeastern Publishing Co. for goods purchased on May 23, terms 2/10, n/30, $1,960 (the $2,000 invoice amount less the 2% discount).

3 Purchased books on account from Broadway Publishing, Inc., $2,880. Invoice No. 711, less a 20% trade discount, and invoice terms of 3/10, n/30, FOB shipping point.

3 Issued Cheek No. 301 to Mayday Shipping for delivery from Broadway Publishing, Inc., $250.

4 Issued Cheek No. 302 for June rent, $625.

8 Purchased books on account from Northeastern Publishing Co., $5,825. Invoice No. 268, terms 2/com, n/60, FOB destination.

10 Received a credit memo from Irving Publishing Company, $550. Books had been returned because the covers were on upside down.

13 Issued Check No. 304 to Broadway Publishing, Inc., for the purchase made on June 3. (Check No. 303 was voided because an error was made in preparing it.)

28 Made the following purchases:

30 Issued Cheek No. 305 to Taylor County Utility Co. for June utilities, $325.

30 French withdrew cash for personal use, $4,500. Issued Check No. 306.

30 Issued Cheek No. 307 to Irving Publishing Company for purchase made on June 1 less returns made on June 10.

30 Issued Check No. 308 to Northeastern Publishing Co. for purchase made on June 8.

30 Issued Check No. 309 for books purchased at an auction, $1,328.

REQUIRED

- 1. Enter the transactions in a general journal (start with page 16).

- 2. Post from the journal to the general ledger accounts and the accounts payable ledger. Use general ledger account numbers as indicated in the chapter.

- 3. Prepare a schedule of accounts payable.

- 4. If merchandise inventory was $35,523 on January 1 and $42,100 as of June 30, prepare the cost of goods sold section of the income statement for the six months ended June 30,20--.

1.

Journalize the purchases and cash payment transactions for the month of June.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- ■ Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- ■ Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Journalize the purchases and cash payment transactions for the month of June.

Transaction on June 1:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 1 | Purchases | 501 | 2,100 | ||

| Accounts Payable, Company IP | 202/✓ | 2,100 | ||||

| (Record purchases made on account) | ||||||

Table (1)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Company IP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on June 2:

| Page: 16 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| June | 2 | Accounts Payable, Corporation NP | 202/✓ | 2,000 | ||

| Cash | 101 | 1,960 | ||||

| Purchases Discounts | 501.2 | 40 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (2)

Description:

- ■ Accounts Payable, Corporation NP is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

- ■ Purchases Discounts is a contra-purchases or contra-costs account, and contra-purchases accounts increase the equity value, and an increase in equity is credited.

Working Note 1:

Compute purchases discount value.

Working Note 2:

Compute amount of cash paid (Refer to Working Note 2 for purchase discount value).

Transaction on June 3:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 3 | Purchases | 501 | 2,304 | ||

| Accounts Payable, Incorporation BP | 202/✓ | 2,304 | ||||

| (Record purchases made on account) | ||||||

Table (3)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Incorporation BP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Working Note 3:

Compute the purchase invoice value.

Transaction on June 3:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 3 | Freight-In | 502 | 250 | ||

| Cash | 101 | 250 | ||||

| (Record payment of freight charges) | ||||||

Table (4)

Description:

- ■ Freight-In is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on June 4:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 4 | Rent Expense | 521 | 625 | ||

| Cash | 101 | 625 | ||||

| (Record payment of rent expense) | ||||||

Table (5)

Description:

- ■ Rent Expense is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on June 8:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 8 | Purchases | 501 | 5,825 | ||

| Accounts Payable, Corporation NP | 202/✓ | 5,825 | ||||

| (Record purchases made on account) | ||||||

Table (6)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Corporation NP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on June 10:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 10 | Accounts Payable, Company IP | 202/✓ | 550 | ||

| Purchases Returns and Allowances | 501.1 | 550 | ||||

| (Record merchandise returned) | ||||||

Table (7)

Description:

- ■ Accounts Payable, Company IP is a liability account. Since inventory is returned, amount to be paid has decreased, liability account is decreased, and a decrease in liability is debited.

- ■ Purchases Returns and Allowances is a contra-cost account, and contra-cost accounts increase the equity value, and an increase in equity is credited.

Transaction on June 13:

| Page: 16 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| June | 13 | Accounts Payable, Incorporation BP | 202/✓ | 2,304.00 | ||

| Cash | 101 | 2,234.88 | ||||

| Purchases Discounts | 501.2 | 69.12 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (8)

Description:

- ■ Accounts Payable, Incorporation BP is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

- ■ Purchases Discounts is a contra-purchases or contra-costs account, and contra-purchases accounts increase the equity value, and an increase in equity is credited.

Working Note 4:

Compute purchases discount value (Refer to Working Note 3 for value of purchases).

Working Note 5:

Compute amount of cash paid (Refer to Working Note 4 for purchase discount value).

Transaction on June 28:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 28 | Purchases | 501 | 2,350 | ||

| Accounts Payable, Incorporation BP | 202/✓ | 2,350 | ||||

| (Record purchases made on account) | ||||||

Table (9)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Incorporation BP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on June 28:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 28 | Purchases | 501 | 4,200 | ||

| Accounts Payable, Corporation NP | 202/✓ | 4,200 | ||||

| (Record purchases made on account) | ||||||

Table (10)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Corporation NP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on June 28:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 28 | Purchases | 501 | 3,450 | ||

| Accounts Payable, Corporation RP | 202/✓ | 3,450 | ||||

| (Record purchases made on account) | ||||||

Table (11)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Accounts Payable, Corporation RP is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on June 30:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 30 | Utilities Expense | 533 | 325 | ||

| Cash | 101 | 325 | ||||

| (Record payment of utilities expense) | ||||||

Table (12)

Description:

- ■ Utilities Expense is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on June 30:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 30 | F, Drawing | 533 | 4,500 | ||

| Cash | 101 | 4,500 | ||||

| (Record withdrawal for personal use) | ||||||

Table (13)

Description:

- ■ F, Drawings is a contra-capital account. Contra-capital accounts have a normal debit balance, hence the account is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on June 30:

| Page: 16 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| June | 30 | Accounts Payable, Company IP | 202/✓ | 1,550 | ||

| Cash | 101 | 1,550 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (14)

Description:

- ■ Accounts Payable, Company IP is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Note 6:

Compute amount of cash paid.

Transaction on June 30:

| Page: 16 | ||||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| June | 30 | Accounts Payable, Corporation NP | 202/✓ | 5,825.00 | ||

| Cash | 101 | 5,708.50 | ||||

| Purchases Discounts | 501.2 | 116.50 | ||||

| (Record cash paid for purchases on account) | ||||||

Table (15)

Description:

- ■ Accounts Payable, Corporation NP is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

- ■ Purchases Discounts is a contra-purchases or contra-costs account, and contra-purchases accounts increase the equity value, and an increase in equity is credited.

Working Note 7:

Compute purchases discount value.

Working Note 8:

Compute amount of cash paid (Refer to Working Note 7 for purchase discount value).

Transaction on June 30:

| Page: 16 | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| June | 30 | Purchases | 501 | 1,328 | ||

| Cash | 101 | 1,328 | ||||

| (Record purchase of inventory) | ||||||

Table (16)

Description:

- ■ Purchases is an expense account which records the cost of inventory purchased. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

2.

Post the given transactions into the accounts of the general ledger, and the suppliers account in accounts payable ledger.

Explanation of Solution

Posting transactions: The process of transferring the journalized transactions into the accounts of the ledger is known as posting the transactions.

Post the given transactions into the accounts of the general ledger.

| ACCOUNT Cash ACCOUNT NO. 101 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 32,200.00 | |||

| 2 | J16 | 1,960.00 | 30,240.00 | ||||

| 3 | J16 | 250.00 | 29,990.00 | ||||

| 4 | J16 | 625.00 | 29,365.00 | ||||

| 13 | J16 | 2,234.88 | 27,130.12 | ||||

| 30 | J16 | 325.00 | 26,805.12 | ||||

| 30 | J16 | 4,500.00 | 22,305.12 | ||||

| 30 | J16 | 1,550.00 | 20,755.12 | ||||

| 30 | J16 | 5708.50 | 15,046.62 | ||||

| 30 | J16 | 1,328.00 | 13,718.62 | ||||

Table (17)

| ACCOUNT Accounts Payable ACCOUNT NO. 202 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 2,000 | |||

| 1 | J16 | 2,100 | 4,100 | ||||

| 2 | J16 | 2,000 | 2,100 | ||||

| 3 | J16 | 2,304 | 4,404 | ||||

| 8 | J16 | 5,825 | 10,229 | ||||

| 10 | J16 | 550 | 9,679 | ||||

| 13 | J16 | 2,304 | 7,375 | ||||

| 28 | J16 | 2,350 | 9,725 | ||||

| 28 | J16 | 4,200 | 13,925 | ||||

| 28 | J16 | 3,450 | 17,375 | ||||

| 30 | J16 | 1,550 | 15,825 | ||||

| 30 | J16 | 5,825 | 10,000 | ||||

Table (18)

| ACCOUNT Purchases ACCOUNT NO. 501 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 67,021.66 | |||

| 1 | J16 | 2,100.00 | 69,121.66 | ||||

| 3 | J16 | 2,304.00 | 71,425.66 | ||||

| 8 | J16 | 5,825.00 | 77,250.66 | ||||

| 28 | J16 | 2,350.00 | 79,600.66 | ||||

| 28 | J16 | 4,200.00 | 83,800.66 | ||||

| 28 | J16 | 3,450.00 | 87,250.66 | ||||

| 30 | J16 | 1,328.00 | 88,578.66 | ||||

Table (19)

| ACCOUNT Purchases Returns and Allowances ACCOUNT NO. 501.1 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 2,315.23 | |||

| 10 | J16 | 550.00 | 2,865.23 | ||||

Table (20)

| ACCOUNT Purchases Discounts ACCOUNT NO. 501.2 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 905.00 | |||

| 2 | J16 | 40.00 | 945.0 | ||||

| 13 | J16 | 69.12 | 1,014.12 | ||||

| 30 | J16 | 116.50 | 1,130.62 | ||||

Table (21)

| ACCOUNT Freight-In ACCOUNT NO. 502 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 522.60 | |||

| 3 | J16 | 250.00 | 772.60 | ||||

Table (22)

| ACCOUNT Rent Expense ACCOUNT NO. 521 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 3,125.00 | |||

| 4 | J16 | 625.00 | 3,750.00 | ||||

Table (23)

| ACCOUNT Utilities Expense ACCOUNT NO. 533 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 1,522.87 | |||

| J16 | 325.00 | 1,847.87 | |||||

Table (24)

| ACCOUNT F, Drawings ACCOUNT NO. 312 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| June | 1 | Balance | ✓ | 18,000 | |||

| J16 | 4,500 | 22,500 | |||||

Table (25)

Post the accounts payable balances of the suppliers to the supplier accounts in the accounts payable ledger.

| NAME Incorporation BP | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| June | 3 | J16 | 2,304 | 2,304 | ||

| 13 | J16 | 2,304 | 0 | |||

| 28 | J16 | 2,350 | 2,350 | |||

Table (26)

| NAME Company IP | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| June | 1 | J16 | 2,100 | 2,100 | ||

| 10 | J16 | 550 | 1,550 | |||

| 30 | J16 | 1,550 | 0 | |||

Table (27)

| NAME Corporation NP | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| June | 1 | Balance | ✓ | 2,000 | ||

| 2 | J16 | 2,000 | 0 | |||

| 8 | J16 | 5,825 | 5,825 | |||

| 28 | J16 | 4,200 | 10,025 | |||

| 30 | J16 | 5,825 | 4,200 | |||

Table (28)

| NAME Corporation RP | ||||||

| ADDRESS | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| June | 28 | J16 | 3,450 | 3,450 | ||

Table (29)

3.

Prepare accounts payable schedule for Company BM as at June 30.

Explanation of Solution

Schedule of accounts payable: This is the schedule which is prepared to verify that the total balances of all the suppliers in the accounts payable ledger, equals the balance of Accounts Payable in the general ledger.

Prepare accounts payable schedule for Company BM as at June 30 (Refer to Requirement (2) for all the values and computations of the balances of the customers).

| Company BM | |

| Schedule of Accounts Payable | |

| June 30 | |

| Incorporation BP | $2,350 |

| Corporation NP | 4,200 |

| Corporation RP | 3,450 |

| Total | $10,000 |

Table (30)

Thus, the schedule of accounts payable of Company BM shows a balance of $10,000, as of June 30.

4.

Prepare the cost of goods sold section of income statement for Company BM.

Explanation of Solution

Cost of goods sold: Cost of goods sold is the total of all the expenses incurred by a company to sell the goods during the given period.

Formula to compute cost of goods sold:

| Details | Amount ($) | Amount ($) | Amount ($) |

| Merchandise inventory, January 1 | $XXX | ||

| Purchases | $XXX | ||

| Less: Purchase returns and allowances | $XXX | ||

| Less: Purchases discounts | XXX | XXX | |

| Net purchases | XXX | ||

| Add: Freight-in | XXX | ||

| Cost of goods purchased | XXX | ||

| Goods available for sale | XXX | ||

| Less: Merchandise inventory, December 31 | XXX | ||

| Cost of goods sold | $XXX |

Table (31)

Prepare the cost of goods sold section of income statement for Company BM (Refer to Requirement (2) for all the values and computations of the ledger balances).

| Details | Amount ($) | Amount ($) | Amount ($) |

| Merchandise inventory, January 1 | $35,523.00 | ||

| Purchases | $88,578.66 | ||

| Less: Purchase returns and allowances | $2,865.23 | ||

| Less: Purchases discounts | 1,130.62 | 3,995.85 | |

| Net purchases | 84,582.81 | ||

| Add: Freight-in | 772.60 | ||

| Cost of goods purchased | 85,355.41 | ||

| Goods available for sale | 120,878.41 | ||

| Less: Merchandise inventory, June 30 | 42,100.00 | ||

| Cost of goods sold | $78,778.41 |

Table (32)

Thus, the cost of goods sold of income statement for Company BM is $78,778.41.

Want to see more full solutions like this?

Chapter 11 Solutions

College Accounting Chapters 1-27 (New in Accounting from Heintz and Parry)

- On January 1, Incredible Infants sold goods to Babies Inc. for $1,540, terms 30 days, and received payment on January 18. Which journal would the company use to record this transaction on the 18th? A. sales journal B. purchases journal C. cash receipts journal D. cash disbursements journal E. general journalarrow_forwardThe following transactions were completed by Nelsons Boutique, a retailer, during July. Terms of sales on account are 2/10, n/30, FOB shipping point. July 3Received cash from J. Smith in payment of June 29 invoice of 350, less cash discount. 6Issued Ck. No. 1718, 742.50, to Designer, Inc., for invoice. no. 2256, recorded previously for 750, less cash discount of 7.50. July 9Sold merchandise in the amount of 250 on a credit card. Sales tax on this sale is 6%. The credit card fee the bank deducted for this transaction is 5. 10Issued Ck. No. 1719, 764.40, to Smart Style, Inc., for invoice no. 1825, recorded previously on account for 780. A trade discount of 25% was applied at the time of purchase, and Smart Style, Inc.s credit terms are 2/10, n/30. 12Received 180 cash in payment of June 20 invoice from R. Matthews. No cash discount applied. 18Received 1,575 cash in payment of a 1,500 note receivable and interest of 75. 21Voided Ck. No. 1720 due to error. 25Received and paid utility bill, 152; Ck. No. 1721, payable to City Utilities Company. 31Paid wages recorded previously for the month, 2,586, Ck. No. 1722. Required 1. Journalize the transactions for July in the cash receipts journal, the general journal (for the transaction on July 9th), or the cash payments journal as appropriate. Assume the periodic inventory method is used. 2. If you are using Working Papers, total and rule the journals. Prove the equality of debit and credit totals.arrow_forwardThe following transactions were completed by Nelsons Hardware, a retailer, during September. Terms on sales on account are 1/10, n/30, FOB shipping point. Sept. 4Received cash from M. Alex in payment of August 25 invoice of 275, less cash discount. 7Issued Ck. No. 8175, 915.75, to Top Tools, Inc., for invoice. no. 2256, recorded previously for 925, less cash discount of 9.25. 10Sold merchandise in the amount of 175 on a credit card. Sales tax on this sale is 8%. The credit card fee the bank deducted for this transaction is 5. 11Issued Ck. No. 8176, 653.40, to Snap Tools, Inc. for invoice no. 726, recorded previously on account for 660. A trade discount of 15% was applied at the time of purchase, and Snap Tools, Inc.s credit terms are 1/10, n/45. 15Received 95 cash in payment of August 20 invoice from N. Johnson. No cash discount applied. 19Received 1,165 cash in payment of a 1,100 note receivable and interest of 65. 22Voided Ck. No. 8177 due to error. 26Received and paid telephone bill, 62; Ck. No. 8178, payable to Southern Telephone Company. 30Paid wages recorded previously for the month, 3,266, Ck. No. 8179. Required 1. Journalize the transactions for September in the cash receipts journal, the general journal (for the transaction on Sept. 10th), or the cash payments journal as appropriate. Assume the periodic inventory method is used. 2. If you are using Working Papers, total and rule the journals. Prove the equality of debit and credit totals.arrow_forward

- The following transactions were completed by Hammond Auto Supply during January, which is the first month of this fiscal year. Terms of sale are 2/10, n/30. The balances of the accounts as of January 1 have been recorded in the general ledger in your Working Papers or in CengageNow. Hammond Auto Supply does not track cash sales by customer. Jan. 2Issued Ck. No. 6981 to JSS Management Company for monthly rent, 775. 2J. Hammond, the owner, invested an additional 3,500 in the business. 4Bought merchandise on account from Valencia and Company, invoice no. A691, 2,930; terms 2/10, n/30; dated January 2. 4Received check from Vega Appliance for 980 in payment of 1,000 invoice less discount. 4Sold merchandise on account to L. Paul, invoice no. 6483, 850. 6Received check from Petty, Inc., 637, in payment of 650 invoice less discount. 7Issued Ck. No. 6982, 588, to Fischer and Son, in payment of invoice no. C1272 for 600 less discount. 7Bought supplies on account from Doyle Office Supply, invoice no. 1906B, 108; terms net 30 days. 7Sold merchandise on account to Ellison and Clay, invoice no. 6484, 787. 9Issued credit memo no. 43 to L. Paul, 54, for merchandise returned. 11Cash sales for January 1 through January 10, 4,863.20. 11Issued Ck. No. 6983, 2,871.40, to Valencia and Company, in payment of 2,930 invoice less discount. 14Sold merchandise on account to Vega Appliance, invoice no. 6485, 2,050. Jan. 18Bought merchandise on account from Costa Products, invoice no. 7281D, 4,854; terms 2/10, n/60; dated January 16; FOB shipping point, freight prepaid and added to the invoice, 147 (total 5,001). 21Issued Ck. No. 6984, 194, to M. Miller for miscellaneous expenses not recorded previously. 21Cash sales for January 11 through January 20, 4,591. 23Issued Ck. No. 6985 to Forbes Freight, 96, for freight charges on merchandise purchased on January 4. 23Received credit memo no. 163, 376, from Costa Products for merchandise returned. 29Sold merchandise on account to Bruce Supply, invoice no. 6486, 1,835. 31Cash sales for January 21 through January 31, 4,428. 31Issued Ck. No. 6986, 53, to M. Miller for miscellaneous expenses not recorded previously. 31Recorded payroll entry from the payroll register: total salaries, 6,200; employees federal income tax withheld, 872; FICA Social Security tax withheld, 384.40, FICA Medicare tax withheld, 89.90. 31Recorded the payroll taxes: Social Security tax, 384.40, FICA Medicare tax, 89.90; state unemployment tax, 334.80; federal unemployment tax, 37.20. 31Issued Ck. No. 6987, 4,853.70, for salaries for the month. 31J. Hammond, the owner, withdrew 1,000 for personal use, Ck. No. 6988. Required 1. Record the transactions for January using a sales journal, page 73; a purchases journal, page 56; a cash receipts journal, page 38; a cash payments journal, page 45; and a general journal, page 100. Assume the periodic inventory method is used. 2. Post daily all entries involving customer accounts to the accounts receivable ledger. 3. Post daily all entries involving creditor accounts to the accounts payable ledger. 4. Post daily those entries involving the Other Accounts columns and the general journal to the general ledger. Write the owners name in the Capital and Drawing accounts. 5. Add the columns of the special journals and prove the equality of the debit and credit totals. 6. Post the appropriate totals of the special journals to the general ledger. 7. Prepare a trial balance. 8. Prepare a schedule of accounts receivable and a schedule of accounts payable. Do the totals equal the balances of the related controlling accounts?arrow_forwardThe following transactions were completed by Hammond Auto Supply during January, which is the first month of this fiscal year. Terms of sale are 2/10, n/30. The balances of the accounts as of January 1 have been recorded in the general ledger in your Working Papers or in CengageNow. Hammond Auto Supply does not track cash sales by customer. Jan. 2Issued Ck. No. 6981 to JSS Management Company for monthly rent, 775. 2J. Hammond, the owner, invested an additional 3,500 in the business. 4Bought merchandise on account from Valencia and Company, invoice no. A691, 2,930; terms 2/10, n/30; dated January 2. 4Received check from Vega Appliance for 980 in payment of 1,000 invoice less discount. 4Sold merchandise on account to L. Paul, invoice no. 6483, 850. 6Received check from Petty, Inc., 637, in payment of 650 invoice less discount. 7Issued Ck. No. 6982, 588, to Fischer and Son, in payment of invoice no. C1272 for 600 less discount. 7Bought supplies on account from Doyle Office Supply, invoice no. 1906B, 108; terms net 30 days. 7Sold merchandise on account to Ellison and Clay, invoice no. 6484, 787. 9Issued credit memo no. 43 to L. Paul, 54, for merchandise returned. 11Cash sales for January 1 through January 10, 4,863.20. 11Issued Ck. No. 6983, 2,871.40, to Valencia and Company, in payment of 2,930 invoice less discount. 14Sold merchandise on account to Vega Appliance, invoice no. 6485, 2,050. Jan. 18Bought merchandise on account from Costa Products, invoice no. 7281D, 4,854; terms 2/10, n/60; dated January 16; FOB shipping point, freight prepaid and added to the invoice, 147 (total 5,001). 21Issued Ck. No. 6984, 194, to M. Miller for miscellaneous expenses not recorded previously. 21Cash sales for January 11 through January 20, 4,591. 23Issued Ck. No. 6985 to Forbes Freight, 96, for freight charges on merchandise purchased on January 4. 23Received credit memo no. 163, 376, from Costa Products for merchandise returned. 29Sold merchandise on account to Bruce Supply, invoice no. 6486, 1,835. 31Cash sales for January 21 through January 31, 4,428. 31Issued Ck. No. 6986, 53, to M. Miller for miscellaneous expenses not recorded previously. 31Recorded payroll entry from the payroll register: total salaries, 6,200; employees federal income tax withheld, 872; FICA Social Security tax withheld, 384.40, FICA Medicare tax withheld, 89.90. 31Recorded the payroll taxes: Social Security tax, 384.40, FICA Medicare tax, 89.90; state unemployment tax, 334.80; federal unemployment tax, 37.20. 31Issued Ck. No. 6987, 4,853.70, for salaries for the month. 31J. Hammond, the owner, withdrew 1,000 for personal use, Ck. No. 6988. Required 1. Record the transactions in the general journal for January. If you are using Working Papers, start with page 1 in the journal. Assume the periodic inventory method is used. The chart of accounts is as follows: 2. Post daily all entries involving customer accounts to the accounts receivable ledger. 3. Post daily all entries involving creditor accounts to the accounts payable ledger. 4. Post daily the general journal entries to the general ledger. Write the owners name in the Capital and Drawing accounts. 5. Prepare a trial balance. 6. Prepare a schedule of accounts receivable and a schedule of accounts payable. Do the totals equal the balances of the related controlling accounts?arrow_forwardPURCHASES JOURNAL, CASH PAYMENTS JOURNAL, AND GENERAL JOURNAL Debbie Mueller owns a small retail business called Debbies Doll House. The cash account has a balance of 20,000 on July 1. The following transactions occurred during July: REQUIRED 1. Record the transactions in the purchases journal, cash payments journal, and general journal. Total and rule the purchases and cash payments journals. Prove the cash payments journal. 2. Post from the journals to the general ledger and accounts payable ledger accounts. Use general ledger account numbers as shown in the chapter.arrow_forward

- Your company paid rent of $1,000 for the month with check number 1245. Which journal would the company use to record this? A. sales journal B. purchases journal C. cash receipts journal D. cash disbursements journal E. general journalarrow_forwardReview the following transactions and prepare any necessary journal entries for Tolbert Enterprises. A. On April 7, Tolbert Enterprises contracts with a supplier to purchase 300 water bottles for their merchandise inventory, on credit, for $10 each. Credit terms are 2/10, n/60 from the invoice date of April 7. B. On April 15, Tolbert pays the amount due in cash to the supplier.arrow_forwardDuring the month of October 20--, The Pink Petal flower shop engaged in the following transactions: Selected account balances as of October 1 were as follows: The Pink Petal also had the following subsidiary ledger balances as of October 1: REQUIRED 1. Record the transactions in a sales journal (page 7), cash receipts journal (page 10), purchases journal (page 6), cash payments journal (page 11), and general journal (page 5). Total, verify, and rule the columns where appropriate at the end of the month. 2. Post from the journals to the general ledger, accounts receivable ledger, and accounts payable ledger accounts. Use account numbers as shown in the chapter.arrow_forward

- Analyzing the Accounts The controller for Summit Sales Inc. provides the following information on transactions that occurred during the year: a. Purchased supplies on credit, $18,600 b. Paid $14,800 cash toward the purchase in Transaction a c. Provided services to customers on credit1 $46,925 d. Collected $39,650 cash from accounts receivable e. Recorded depreciation expense, $8,175 f. Employee salaries accrued, $15,650 g. Paid $15,650 cash to employees for salaries earned h. Accrued interest expense on long-term debt, $1,950 i. Paid a total of $25,000 on long-term debt, which includes $1.950 interest from Transaction h j. Paid $2,220 cash for l years insurance coverage in advance k. Recognized insurance expense, $1,340, that was paid in a previous period l. Sold equipment with a book value of $7,500 for $7,500 cash m. Declared cash dividend, $12,000 n. Paid cash dividend declared in Transaction m o. Purchased new equipment for $28,300 cash. p. Issued common stock for $60,000 cash q. Used $10,700 of supplies to produce revenues Summit Sales uses the indirect method to prepare its statement of cash flows. Required: 1. Construct a table similar to the one shown at the top of the next page. Analyze each transaction and indicate its effect on the fundamental accounting equation. If the transaction increases a financial statement element, write the amount of the increase preceded by a plus sign (+) in the appropriate column. If the transaction decreases a financial statement element, write the amount of the decrease preceded by a minus sign (-) in the appropriate column. 2. Indicate whether each transaction results in a cash inflow or a cash outflow in the Effect on Cash Flows column. If the transaction has no effect on cash flow, then indicate this by placing none in the Effect on Cash Flows column. 3. For each transaction that affected cash flows, indicate whether the cash flow would be classified as a cash flow from operating activities, cash flow from investing activities, or cash flow from financing activities. If there is no effect on cash flows, indicate this as a non-cash activity.arrow_forwardThe following transactions were completed by Yang Restaurant Equipment during January, the first month of this fiscal year. Terms of sale are 2/10, n/30. The balances of the accounts as of January 1 have been recorded in the general ledger in your Working Papers or in CengageNow. Yang Restaurant Equipment does not track cash sales by customer. Jan. 2Issued Ck. No. 6981 to Tri-County Management Company for monthly rent, 850. 2L. Yang, the owner, invested an additional 4,500 in the business. 4Bought merchandise on account from Valentine and Company, invoice no. A694, 2,830; terms 2/10, n/30; dated January 2. 4Received check from Velez Appliance for 980 in payment of invoice for 1,000 less discount. 4Sold merchandise on account to L. Parrish, invoice no. 6483, 755. 6Received check from Peck, Inc., 637, in payment of 650 invoice less discount. 7Issued Ck. No. 6982, 588, to Frost and Son, in payment of invoice no. C127 for 600 less discount. 7Bought supplies on account from Dudley Office Supply, invoice no. 190B, 93.54; terms net 30 days. 7Sold merchandise on account to Ewing and Charles, invoice no. 6484, 1,115. 9Issued credit memo no. 43 to L. Parrish, 47, for merchandise returned. 11Cash sales for January 1 through January 10, 4,454.87. 11Issued Ck. No. 6983, 2,773.40, to Valentine and Company, in payment of 2,830 invoice less discount. 14Sold merchandise on account to Velez Appliance, invoice no. 6485, 2,100. 14Received check from L. Parrish, 693.84, in payment of 755 invoice, less return of 47 and less discount. Jan. 19Bought merchandise on account from Crawford Products, invoice no. 7281, 3,700; terms 2/10, n/60; dated January 16; FOB shipping point, freight prepaid and added to invoice, 142 (total 3,842). 21Issued Ck. No. 6984, 245, to A. Bautista for miscellaneous expenses not recorded previously. 21Cash sales for January 11 through January 20, 3,689. 23Received credit memo no. 163, 87, from Crawford Products for merchandise returned. 29Sold merchandise on account to Bradford Supply, invoice no. 6486, 1,697.20. 29Issued Ck. No. 6985 to Western Freight, 64, for freight charges on merchandise purchased January 4. 31Cash sales for January 21 through January 31, 3,862. 31Issued Ck. No. 6986, 65, to M. Pineda for miscellaneous expenses not recorded previously. 31Recorded payroll entry from the payroll register: total salaries, 5,899.95; employees federal income tax withheld, 795; FICA Social Security tax withheld, 365.80, FICA Medicare tax withheld, 85.50. 31Recorded the payroll taxes: FICA Social Security tax, 365.80; FICA Medicare tax, 85.50; state unemployment tax, 318.60; federal unemployment tax, 35.40. 31Issued Ck. No. 6987, 4,653.65, for salaries for the month. 31L. Yang, the owner, withdrew 1,000 for personal use, Ck. No. 6988. Required 1. Record the transactions in the general journal for January. If you are using Working Papers, start with page 1 in the journal. Assume the periodic inventory method is used. The chart of accounts is as follows: 2. Post daily all entries involving customer accounts to the accounts receivable ledger. 3. Post daily all entries involving creditor accounts to the accounts payable ledger. 4. Post daily the general journal entries to the general ledger. Write the owners name in the Capital and Drawing accounts. 5. Prepare a trial balance. 6. Prepare a schedule of accounts receivable and a schedule of accounts payable. Do the totals equal the balances of the related controlling accounts?arrow_forwardThe following transactions were completed by Yang Restaurant Equipment during January, the first month of this fiscal year. Terms of sale are 2/10, n/30. The balances of the accounts as of January 1 have been recorded in the general ledger in your Working Papers or in CengageNow. Yang Restaurant Equipment does not track cash sales by customer. Jan. 2Issued Ck. No. 6981 to Tri-County Management Company for monthly rent, 850. 2L. Yang, the owner, invested an additional 4,500 in the business. 4Bought merchandise on account from Valentine and Company, invoice no. A694, 2,830; terms 2/10, n/30; dated January 2. 4Received check from Velez Appliance for 980 in payment of invoice for 1,000 less discount. 4Sold merchandise on account to L. Parrish, invoice no. 6483, 755. 6Received check from Peck, Inc., 637, in payment of 650 invoice less discount. 7Issued Ck. No. 6982, 588, to Frost and Son, in payment of invoice no. C127 for 600 less discount. 7Bought supplies on account from Dudley Office Supply, invoice no. 190B, 93.54; terms net 30 days. 7Sold merchandise on account to Ewing and Charles, invoice no. 6484, 1,115. 9Issued credit memo no. 43 to L. Parrish, 47, for merchandise returned. 11Cash sales for January 1 through January 10, 4,454.87. 11Issued Ck. No. 6983, 2,773.40, to Valentine and Company, in payment of 2,830 invoice less discount. 14Sold merchandise on account to Velez Appliance, invoice no. 6485, 2,100. 14Received check from L. Parrish, 693.84, in payment of 755 invoice, less return of 47 and less discount. Jan. 19Bought merchandise on account from Crawford Products, invoice no. 7281, 3,700; terms 2/10, n/60; dated January 16; FOB shipping point, freight prepaid and added to invoice, 142 (total 3,842). 21Issued Ck. No. 6984, 245, to A. Bautista for miscellaneous expenses not recorded previously. 21Cash sales for January 11 through January 20, 3,689. 23Received credit memo no. 163, 87, from Crawford Products for merchandise returned. 29Sold merchandise on account to Bradford Supply, invoice no. 6486, 1,697.20. 29Issued Ck. No. 6985 to Western Freight, 64, for freight charges on merchandise purchased January 4. 31Cash sales for January 21 through January 31, 3,862. 31Issued Ck. No. 6986, 65, to M. Pineda for miscellaneous expenses not recorded previously. 31Recorded payroll entry from the payroll register: total salaries, 5,899.95; employees federal income tax withheld, 795; FICA Social Security tax withheld, 365.80, FICA Medicare tax withheld, 85.50. 31Recorded the payroll taxes: FICA Social Security tax, 365.80; FICA Medicare tax, 85.50; state unemployment tax, 318.60; federal unemployment tax, 35.40. 31Issued Ck. No. 6987, 4,653.65, for salaries for the month. 31L. Yang, the owner, withdrew 1,000 for personal use, Ck. No. 6988. Required 1. Record the transactions for January using a sales journal, page 91; a purchases journal, page 74; a cash receipts journal, page 56; a cash payments journal, page 63; and a general journal, page 119. Assume the periodic inventory method is used. 2. Post daily all entries involving customer accounts to the accounts receivable ledger. 3. Post daily all entries involving creditor accounts to the accounts payable ledger. 4. Post daily those entries involving the Other Accounts columns and the general journal to the general ledger. Write the owners name in the Capital and Drawing accounts. 5. Add the columns of the special journals and prove the equality of the debit and credit totals. 6. Post the appropriate totals of the special journals to the general ledger. 7. Prepare a trial balance. 8. Prepare a schedule of accounts receivable and a schedule of accounts payable. Do the totals equal the balances of the related controlling accounts?arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage- Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning