Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN: 9781305970663

Author: Don R. Hansen, Maryanne M. Mowen

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 13, Problem 25P

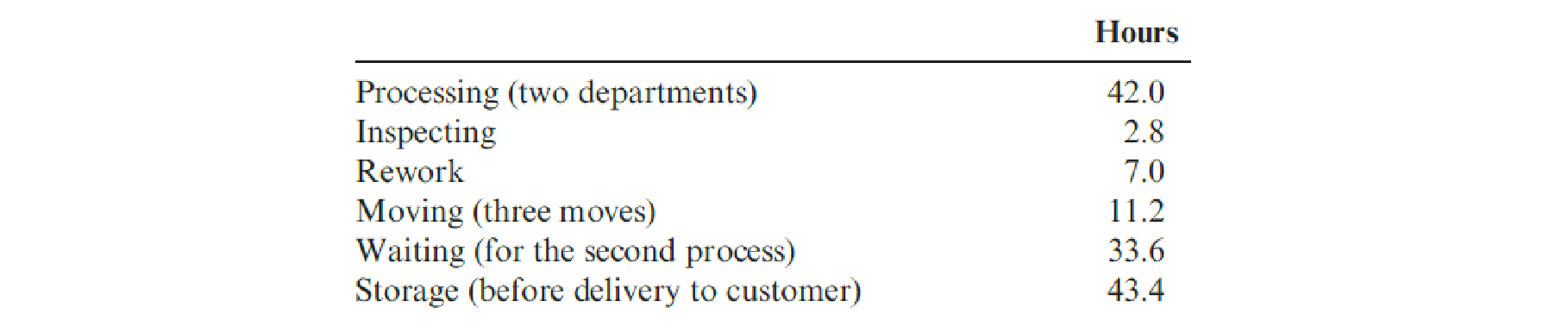

Auflegger, Inc., manufactures a product that experiences the following activities (and times):

Required:

- 1. Compute the MCE for this product.

- 2. A study lists the following root causes of the inefficiencies: poor quality components from suppliers, lack of skilled workers, and plant layout. Suggest a possible cost reduction strategy, expressed as a series of if-then statements that will reduce MCE and lower costs. Finally, prepare a strategy map that illustrates the causal paths. In preparing the map, use only three perspectives: learning and growth, process, and financial.

- 3. Is MCE a lag or a lead measure? If and when MCE acts as a lag measure, what lead measures would affect it?

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Data Screen Corporation is a highly automated manufacturing firm. The vice president of finance has decided that traditional standards are inappropriate for performance measures in an automated environment. Labor is insignificant in terms of the total cost of production and tends to be fixed, material quality is considered more important than minimizing material cost, and customer satisfaction is the number one priority. As a result, production and delivery performance measures have been chosen to evaluate performance. The following information is considered typical of the time involved to complete and ship orders.

Waiting time:From order being placed to start of production ..................................... 8.0 daysFrom start of production to completion ..................................................... 7.0 daysInspection time ....................................................................... .............................. 1.5 daysProcessing time…

Wolk Corporation is a highly automated manufacturing firm. The vice president of finance has decided that traditional standards are inappropriate for performance measures in an automated environment. Labor for this company is insignificant in terms of the total cost of production and tends to be fixed, material quality is considered more important than minimizing material cost, and customer satisfaction is the number one priority. As a result, delivery performance measures have been chosen to evaluate performance. The following information is considered typical of the time involved to complete customer orders.

From time order is placed to time order received by manufacturing

18.0

days

From time order is received by manufacturing to time production begins

9.0

days

Inspection time

3.5

days

Process (manufacturing) time

7.0

days

Move time

4.5

days

What is the production (manufacturing) lead time for this order?

Multiple Choice

34 days.

16…

Worldwide Corporation is a highly automated manufacturing firm. The vice president of finance has decided that traditional standards are inappropriate for performance measures in an automated environment. Labor is significant in terms of the total cost of production and tends to be fixed, material quality is considered more important than minimizing material cost and customer satisfaction is the number one priority. As a result, delivery performance measures have been chosen to evaluate performance. The following information is considered typical of the time involved to complete orders:

- Wait time:

-From order being placed to

start of production

-From start of production to 10.0 days

completion

- Inspection time 1.5 days

- Process time…

Chapter 13 Solutions

Cornerstones of Cost Management (Cornerstones Series)

Ch. 13 - Describe a strategic-based responsibility...Ch. 13 - What is a Balanced Scorecard?Ch. 13 - What is meant by balanced measures?Ch. 13 - Prob. 4DQCh. 13 - Prob. 5DQCh. 13 - What are stretch targets? What is their strategic...Ch. 13 - Prob. 7DQCh. 13 - What are the three strategic themes of the...Ch. 13 - Prob. 9DQCh. 13 - Explain what is meant by the long wave and the...

Ch. 13 - Prob. 11DQCh. 13 - Prob. 12DQCh. 13 - What is a testable strategy?Ch. 13 - Prob. 14DQCh. 13 - Prob. 15DQCh. 13 - Norton Company has the following data for one of...Ch. 13 - Craig, Inc., has provided the following...Ch. 13 - Prob. 3CECh. 13 - The following comment was made by the CEO of a...Ch. 13 - Prob. 5ECh. 13 - Prob. 6ECh. 13 - Consider the following list of scorecard measures:...Ch. 13 - Hatch Manufacturing produces multiple machine...Ch. 13 - Computador has a manufacturing plant in Des Moines...Ch. 13 - Refer to Exercise 13.9. Assume that the company...Ch. 13 - The following if-then statements were taken from a...Ch. 13 - Consider the following quality improvement...Ch. 13 - Bannister Company, an electronics firm, buys...Ch. 13 - Prob. 14ECh. 13 - In a balanced scorecard, a key strategic if-then...Ch. 13 - Which of the following objectives would be...Ch. 13 - A manufacturing cell produces 40 units in five...Ch. 13 - Which of the following objectives would likely be...Ch. 13 - Which of the following objectives would likely be...Ch. 13 - Carson Wellington, president of Mallory Plastics,...Ch. 13 - At the end of 20x1, Mejorar Company implemented a...Ch. 13 - Refer to the data in Problem 13.21. 1. Express...Ch. 13 - The following strategic objectives have been...Ch. 13 - Lander Parts, Inc., produces various automobile...Ch. 13 - Auflegger, Inc., manufactures a product that...Ch. 13 - Prob. 26PCh. 13 - At the beginning of the last quarter of 20x1,...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Because of high production-changeover time and costs, a director of manufacturing must convince management that a proposed manufacturing method reduces costs before the new method can be implemented. The current production method operates with a mean cost of $220 per hour. A research study will measure the cost of the new method over a sample production period. Develop the null and alternative hypotheses most appropriate for this study. Comment on the conclusion when H0 cannot be rejected. Comment on the conclusion when H0 can be rejected.arrow_forwardThe following series of statements or phrases are associated with product life-cycle viewpoints. Identify whether each one is associated with the marketing, production, or customer viewpoint. Where possible, identify the particular characteristic being described. If the statement or phrase fits more than one viewpoint, label it as interactive. Explain the interaction. a. Sales are increasing at an increasing rate. b. The cost of maintaining the product after it is purchased. c. The product is losing market acceptance and sales are beginning to decrease. d. A design is chosen to minimize post-purchase costs. e. Ninety percent or more of the costs are committed during the development stage. f. The length of time that the product serves the needs of a customer. g. All the costs associated with a product for its entire life cycle. h. The time in which a product generates revenue for a company. i. Profits tend to reach peak levels during this stage. j. Customers have the lowest price sensitivity during this stage. k. Describes the general sales pattern of a product as it passes through distinct life-cycle stages. l. The concern is with product performance and price. m. Actions taken so that life-cycle profits are maximized. n. Emphasizes internal activities that are needed to develop, produce, market, and service products.arrow_forwardAbernathy, Inc., produces two different generators and is concerned about their quality. The company has identified the following quality activities and costs associated with the two products: Required: 1. Calculate the quality cost per unit for each product, and break this unit cost into quality cost categories. Which of the two seems to have the lowest quality? 2. How might a manager use the unit quality cost information?arrow_forward

- The management of Hartman Company is trying to determine the amount of each of two products to produce over the coming planning period. The following information concerns labor availability, labor utilization, and product profitability: a. Develop a linear programming model of the Hartman Company problem. Solve the model to determine the optimal production quantities of products 1 and 2. b. In computing the profit contribution per unit, management does not deduct labor costs because they are considered fixed for the upcoming planning period. However, suppose that overtime can be scheduled in some of the departments. Which departments would you recommend scheduling for overtime? How much would you be willing to pay per hour of overtime in each department? c. Suppose that 10, 6, and 8 hours of overtime may be scheduled in departments A, B, and C, respectively. The cost per hour of overtime is 18 in department A, 22.50 in department B, and 12 in department C. Formulate a linear programming model that can be used to determine the optimal production quantities if overtime is made available. What are the optimal production quantities, and what is the revised total contribution to profit? How much overtime do you recommend using in each department? What is the increase in the total contribution to profit if overtime is used?arrow_forwardSalem Electronics currently produces two products: a programmable calculator and a tape recorder. A recent marketing study indicated that consumers would react favorably to a radio with the Salem brand name. Owner Kenneth Booth was interested in the possibility. Before any commitment was made, however, Kenneth wanted to know what the incremental fixed costs would be and how many radios must be sold to cover these costs. In response, Betty Johnson, the marketing manager, gathered data for the current products to help in projecting overhead costs for the new product. The overhead costs based on 30,000 direct labor hours follow. (The high-low method using direct labor hours as the independent variable was used to determine the fixed and variable costs.) All depreciation. The following activity data were also gathered: Betty was told that a plantwide overhead rate was used to assign overhead costs based on direct labor hours. She was also informed by engineering that if 20,000 radios were produced and sold (her projection based on her marketing study), they would have the same activity data as the recorders (use the same direct labor hours, machine hours, setups, and so on). Engineering also provided the following additional estimates for the proposed product line: Upon receiving these estimates, Betty did some quick calculations and became quite excited. With a selling price of 26 and just 18,000 of additional fixed costs, only 4,500 units had to be sold to break even. Since Betty was confident that 20,000 units could be sold, she was prepared to strongly recommend the new product line. Required: 1. Reproduce Bettys break-even calculation using conventional cost assignments. How much additional profit would be expected under this scenario, assuming that 20,000 radios are sold? 2. Use an activity-based costing approach, and calculate the break-even point and the incremental profit that would be earned on sales of 20,000 units. 3. Explain why the CVP analysis done in Requirement 2 is more accurate than the analysis done in Requirement 1. What recommendation would you make?arrow_forwardKagle design engineers are in the process of developing a new green product, one that will significantly reduce impact on the environment and yet still provide the desired customer functionality. Currently, two designs are being considered. The manager of Kagle has told the engineers that the cost for the new product cannot exceed 550 per unit (target cost). In the past, the Cost Accounting Department has given estimated costs using a unit-based system. At the request of the Engineering Department, Cost Accounting is providing both unit-and activity-based accounting information (made possible by a recent pilot study producing the activity-based data). Unit-based system: Variable conversion activity rate: 100 per direct labor hour Material usage rate: 20 per part ABC system: Labor usage: 15 per direct labor hour Material usage (direct materials): 20 per part Machining: 75 per machine hour Purchasing activity: 150 per purchase order Setup activity: 3,000 per setup hour Warranty activity: 500 per returned unit (usually requires extensive rework) Customer repair cost: 25 per repair hour (average) Required: 1. Select the lower-cost design using unit-based costing. Are logistical and post-purchase activities considered in this analysis? 2. Select the lower-cost design using ABC analysis. Explain why the analysis differs from the unit-based analysis. 3. What if the post-purchase cost was an environmental contaminant and amounted to 10 per unit for Design A and 40 per unit for Design B? Assume that the environmental cost is borne by society. Now which is the better design?arrow_forward

- Explain how a plantwide overhead rate, using a unit-based driver, can produce distorted product costs. In your answer, identify two major factors that impair the ability of plantwide rates to assign cost accurately.arrow_forwardLarsen, Inc., produces two types of electronic parts and has provided the following data: There are four activities: machining, setting up, testing, and purchasing. Required: 1. Calculate the activity consumption ratios for each product. 2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted? 3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?arrow_forwardDiscuss how, as warehouse manager for Vinnies Vinyls, you view the different rate of allocated costs the warehouse is being charged compared to the West store. Describe the implications of this. What steps could you take to solve this discrepancy? What alternatives would you consider, assuming management is willing to consider making changes in the rate?arrow_forward

- Continuous improvement is the governing principle of a lean accounting system. Following are several performance measures. Some of these measures would be associated with a traditional standard-costing accounting system, and some would be associated with a lean accounting system. a. Materials price variances b. Cycle time c. Comparison of actual product costs with target costs d. Materials quantity or efficiency variances e. Comparison of actual product costs over time (trend reports) f. Comparison of actual overhead costs, item by item, with the corresponding budgeted costs g. Comparison of product costs with competitors product costs h. Percentage of on-time deliveries i. First-time through j. Reports of value- and non-value-added costs k. Labor efficiency variances l. Days of inventory m. Downtime n. Manufacturing cycle efficiency (MCE) o. Unused (available) capacity variance p. Labor rate variance q. Using a sister plants best practices as a performance standard Required: 1. Classify each measure as lean or traditional (standard costing). If traditional, discuss the measures limitations for a lean environment. If it is a lean measure, describe how the measure supports the objectives of lean manufacturing. 2. Classify the measures into operational (nonfinancial) and financial categories. Explain why operational measures are better for control at the shop level (production floor) than financial measures. Should any financial measures be used at the operational level? 3. Suggest some additional measures that you would like to see added to the list that would be supportive of lean objectives.arrow_forwardMorrisons Plastics Division, a profit center, sells its products to external customers as well as to other internal profit centers. Which one of the following circumstances would justify the Plastics Division selling a product internally to another profit center at a price that is below the market-based transfer price? a. The buying unit has excess capacity. b. The selling unit is operating at full capacity. c. Routine sales commissions and collection costs would be avoided. d. The profit centers managers are evaluated on the basis of unit operating income.arrow_forwardWhich of the following is a reason a company would implement activity-based costing? A. The cost of record keeping is high. B. The additional data obtained through traditional allocation are not worth the cost. C. They want to improve the data on which decisions are made. D. A company only has one cost driver.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:9781337514835

Author:MOYER

Publisher:CENGAGE LEARNING - CONSIGNMENT

Essentials of Business Analytics (MindTap Course ...

Statistics

ISBN:9781305627734

Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Relevant Costing Explained; Author: Kaplan UK;https://www.youtube.com/watch?v=hnsh3hlJAkI;License: Standard Youtube License