Concept explainers

Videos

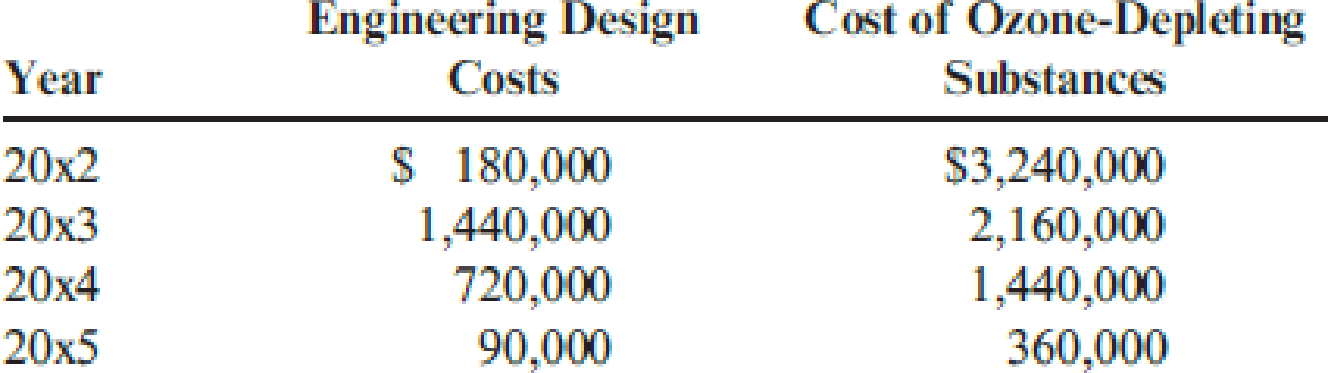

Refer to Problem 14.41. In the environmental benefits section of the report, three types of benefits are listed: income, savings, and cost avoidance. Now, consider the following data for selected items for a four-year period:

The engineering design costs were incurred to redesign the production processes and products. Redesign of the product allowed the substitution of a material that produced less ozone-depleting substances. Modifications in the design of the processes also accomplished the same objective. Because of the improvements, the company was able to reduce the demand for pollution control equipment (with its attendant

Required:

- 1. Prepare a partial environmental financial statement, divided into benefit and cost sections for 20x3, 20x4, and 20x5.

- 2. Evaluate and explain the outcomes. Does this result support or challenge ecoefficiency? Explain.

Trending nowThis is a popular solution!

Chapter 14 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Two products, Product A and Product B, are associated with the following environmental activities and associated data: Driver data: Which of the two products has the greatest environmental impact? a. Product A because its total environmental cost is 400,000. b. Product A because it causes more waste and pollution control than Product B. c. Product B because its total environmental cost is 400,000. d. Product B because its environmental cost per unit is five times more than Product As unit environmental cost.arrow_forwardThe following items are listed in an environmental financial statement (issued as part of an environmental progress report): Environmental benefits (savings, income, and cost avoidance): Ozone-depleting substances cost reductions Hazardous waste disposal cost reductions Hazardous waste material cost reductions Nonhazardous waste disposal cost reductions Nonhazardous waste material cost reductions Recycling income Energy conservation cost savings Packaging cost reductions Environmental costs: Corporate-level administrative costs Auditor fees Environmental engineering Facility professionals and programs Packaging professionals and programs for packaging reductions Pollution controls: Operations and maintenance Pollution controls: Depreciation Attorney fees for cleanup claims, and notices of violations (NOVs) Settlements of government claims Waste disposal Environmental taxes for packaging Remediation/cleanup: On-site Remediation/cleanup: Off-site Required: 1. Classify each item in the statement as prevention, detection, internal failure, or external failure. In classifying the items listed in the environmental benefits category, first classify the underlying cost item (e.g., the cost of hazardous waste disposal). Next, think of how you would classify the cost of the activities that led to the cost reduction. That is, how would you classify the macro activity: reducing hazardous waste cost disposal? 2. Assuming ecoefficiency, what relationship over time would you expect to observe between the environmental benefits category and the environmental costs category?arrow_forwardClassify the following environmental activities as prevention costs, detection costs, internal failure costs, or external failure costs. For external failure costs, classify the costs as societal or private. Also, label those activities that are compatible with sustainable development (SD). 1. A company takes actions to reduce the amount of material in its packages. 2. After the activated carbons useful life, a soft-drink producer returns this material used for purifying water for its beverages to the supplier. The supplier reactivates the carbon for a second use in nonfood applications. As a consequence, many tons of material are prevented from entering landfills. 3. An evaporator system is installed to treat wastewater and collect usable solids for other uses. 4. The inks used to print snack packages (for chips) contain heavy metals. 5. Processes are inspected to ensure compliance with environmental standards. 6. Delivery boxes are used five times and then recycled. This prevents 112 million pounds of cardboard from entering landfills and saves 2 million trees per year. 7. Scrubber equipment is installed to ensure that air emissions are less than the level permitted by law. 8. Local residents are incurring medical costs from illnesses caused by air pollution from automobile exhaust pollution. 9. As part of implementing an environmental perspective for the Balanced Scorecard, environmental performance measures are developed. 10. Because of liquid and solid residues being discharged into a local lake, the lake is no longer fit for swimming, fishing, and other recreational activities. 11. To reduce energy consumption, magnetic ballasts are replaced with electronic ballasts, and more efficient light bulbs and lighting sensors are installed. As a result, 2.3 million kilowatt-hours of electricity are saved per year. 12. Due to a legal settlement, a chemicals company must spend 20,000,000 to clean up contaminated soil. 13. A soft-drink company uses the following practice: In all bottling plants, packages damaged during filling are collected and recycled (glass, plastic, and aluminum). 14. Products are inspected to ensure that the gaseous emissions produced during operation follow legal and company guidelines. 15. Operating pollution control equipment incurs costs. 16. An internal audit is conducted to verify that environmental policies are being followed.arrow_forward

- Verde Company reported operating costs of 50,000,000 as of December 31, 20x5, with the following environmental costs: Required: 1. Prepare an environmental cost report, classifying costs by quality category and expressing each as a percentage of total operating costs. What is the message of this report? 2. Prepare a pie chart that shows the relative distribution of environmental costs by category. What does this report tell you? 3. What if Verde deliberately did not include the cost of damaging the ecosystem because of solid waste disposal in its environmental cost report? Offer possible reasons for this decision. If consciously avoided, is this decision unethical?arrow_forwardKagle design engineers are in the process of developing a new green product, one that will significantly reduce impact on the environment and yet still provide the desired customer functionality. Currently, two designs are being considered. The manager of Kagle has told the engineers that the cost for the new product cannot exceed 550 per unit (target cost). In the past, the Cost Accounting Department has given estimated costs using a unit-based system. At the request of the Engineering Department, Cost Accounting is providing both unit-and activity-based accounting information (made possible by a recent pilot study producing the activity-based data). Unit-based system: Variable conversion activity rate: 100 per direct labor hour Material usage rate: 20 per part ABC system: Labor usage: 15 per direct labor hour Material usage (direct materials): 20 per part Machining: 75 per machine hour Purchasing activity: 150 per purchase order Setup activity: 3,000 per setup hour Warranty activity: 500 per returned unit (usually requires extensive rework) Customer repair cost: 25 per repair hour (average) Required: 1. Select the lower-cost design using unit-based costing. Are logistical and post-purchase activities considered in this analysis? 2. Select the lower-cost design using ABC analysis. Explain why the analysis differs from the unit-based analysis. 3. What if the post-purchase cost was an environmental contaminant and amounted to 10 per unit for Design A and 40 per unit for Design B? Assume that the environmental cost is borne by society. Now which is the better design?arrow_forwardAt the end of 20x5, Bing Pharmaceuticals began to implement an environmental quality management program. As a first step, it identified the following costs in its accounting records as environmentally related for the calendar year just ended: Required: 1. Prepare an environmental cost report by category. Assume that total operating costs are 150,000,000. 2. Use a pie chart to illustrate the relative distribution percentages for each environmental cost category. Comment on what this distribution communicates to a manager.arrow_forward

- The following environmental cost reports for 20x3, 20x4, and 20x5 (year end December 31) are for the Communications Products Division of Kartel, a telecommunications company. In 2011, Kartel committed itself to a continuous environmental improvement program, which was implemented throughout the company. At the beginning of 20x5, Kartel began a new program of recycling nonhazardous scrap. The effort produced recycling income totaling 25,000. The marketing vice president and the environmental manager estimated that sales revenue had increased by 200,000 per year since 20x3 because of an improved public image relative to environmental performance. The companys Finance Department also estimated that Kartel saved 80,000 in 20x5 because of reduced finance and insurance costs, all attributable to improved environmental performance. All reductions in environmental costs from 20x3 to 20x5 are attributable to improvement efforts. Furthermore, any reductions represent ongoing savings. Required: 1. Prepare an environmental financial statement for 20x5 (for the Products Division). In the cost section, classify environmental costs by category (prevention, detection, etc.). 2. Evaluate the changes in environmental performance.arrow_forwardUsing the Taguchi quality loss function, an average loss of 20 per unit is calculated. During the year, 25,000 units were produced. Which of the following statements represents the correct application of the Taguchi loss function? a. The hidden costs of internal failure are 500,000. b. The hidden costs of external failure are 500,000. c. The costs of detection activities are 20 per unit inspected. d. The total external costs are 500,000.arrow_forwardCoyle Pharmaceuticals produces two organic chemicals (Org AB and Org XY) used in the production of two of its most wide-selling anti-cancer drugs. The controller and environmental manager have identified the following environmental activities and costs associated with the two products: Required: 1. Calculate the environmental cost per pound for each product. Which of the two products appears to cause the most degradation to the environment? 2. In which environmental category would you classify excessive use of materials and energy? 3. Suppose that the toxin releases cause health problems for those who live near the chemical plant. The costs, due to missed work and medical treatments, are estimated at 2,025,000 per year. How would assignment of these costs change the unit cost? Should they be assigned?arrow_forward

- Kagle design engineers are in the process of developing a new “green” product, one that will significantly reduce impact on the environment and yet still provide the desired customer functionality. Currently, two designs are being considered. The manager of Kagle has told the engineers that the cost for the new product cannot exceed $550 per unit (target cost). In the past, the Cost Accounting Department has given estimated costs using a unit-based system. At the request of the Engineering Department, Cost Accounting is providing both unit- and activity-based accounting information (made possible by a recent pilot study producing the activity-based data). Unit-based system:Variable conversion activity rate: $100 per direct labor hourMaterial usage rate: $20 per partABC system:Labor usage: $15 per direct labor hourMaterial usage (direct materials): $20 per partMachining: $75 per machine hourPurchasing activity: $150 per purchase orderSetup activity: $3,000 per setup hourWarranty…arrow_forwardIn trying to decide whether or not to replace a sorting/baling machine in a solid waste recycling operation, an engineer calculated the annual worthvalues for the in-place machine and a challenger. On the basis of these costs, the defender should be replaced:a. now.b. 1 year from now.c. 2 years from now.d. 3 years from now.arrow_forwardAt the beginning of the year, Devonshire Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years: Preceding Year Current Year Sales $2,400,000 $2,400,000 Quality training 30,000 48,000 Material inspections 7,000 8,000 Scrap 48,000 30,000 Rework 60,000 48,000 Product inspection 10,000 12,000 Product warranty 36,000 24,000 For the current year, appraisal costs are what percentage of sales? a.0.500% b.0.333% c.3.333% d.0.833%arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning