Videos

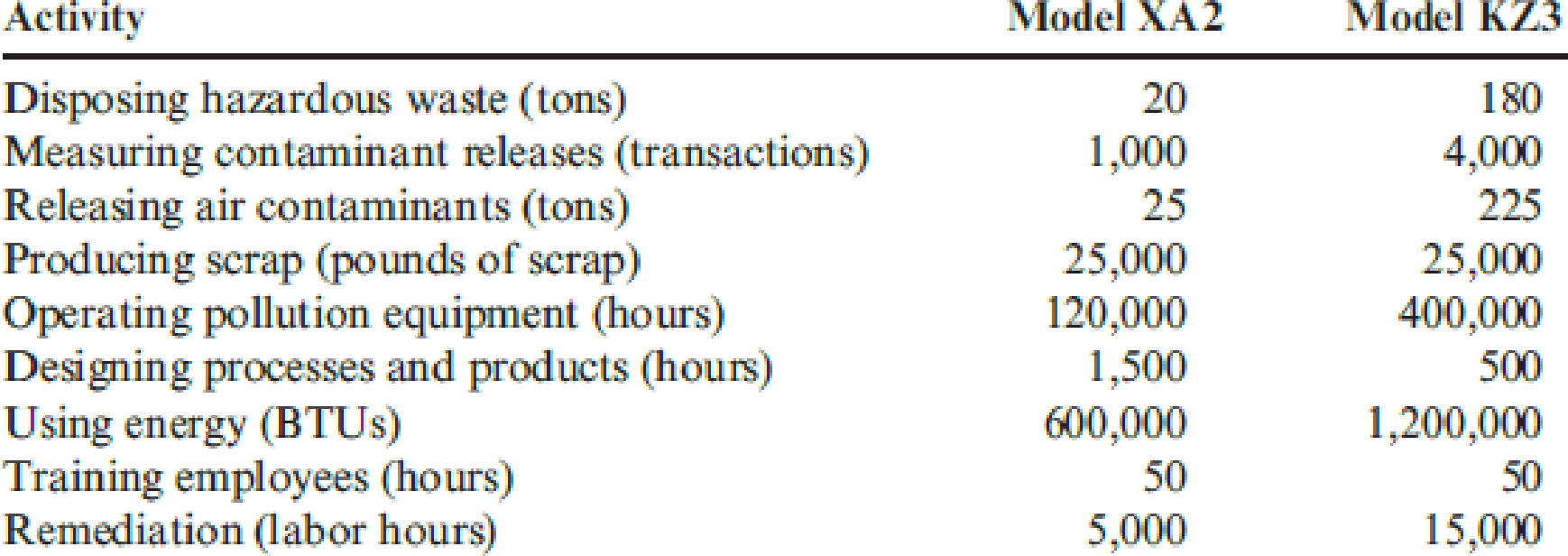

Refer to Problem 14.43. In 20x3, Jack Carter, president of Kartel, requested that environmental costs be assigned to the two major products produced by the company. He felt that knowledge of the environmental product costs would help guide the design decisions that would be necessary to improve environmental performance. The products represent two different models of a cellular phone (Model XA2 and Model KZ3). The models use different processes and materials. To assign the costs, the following data were gathered for 20x3:

During 20x3, Kartel’s division produced 200,000 units of Model XA2 and 300,000 units of Model KZ3.

Required:

- 1. Using the activity data, calculate the environmental cost per unit for each model. How will this information be useful?

- 2. Upon examining the cost data produced in Requirement 1, an environmental engineer made the following suggestions: (1) substitute a new plastic for a material that appeared to be the source of much of the hazardous waste (the new material actually cost less than the contaminating material it would replace), and (2) redesign the processes to reduce the amount of air contaminants produced.

As a result of the first suggestion, by 20x5, the amount of hazardous waste produced had diminished to 50 tons, 10 tons for Model XA2 and 40 tons for Model KZ3. The second suggestion reduced the contaminants released by 50 percent by 20x5 (15 tons for Model XA2 and 110 tons for Model KZ3). The need for pollution equipment also diminished, and the hours required for operating this equipment for Model XA2 and Model KZ3 were reduced to 60,000 and 200,000, respectively. Calculate the unit cost reductions for the two models associated with the actions and outcomes described (assume the same production as in 20x3). Do you think the efforts to reduce the environmental cost per unit were economically justified? Explain.

Want to see the full answer?

Check out a sample textbook solution

Chapter 14 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Kagle design engineers are in the process of developing a new green product, one that will significantly reduce impact on the environment and yet still provide the desired customer functionality. Currently, two designs are being considered. The manager of Kagle has told the engineers that the cost for the new product cannot exceed 550 per unit (target cost). In the past, the Cost Accounting Department has given estimated costs using a unit-based system. At the request of the Engineering Department, Cost Accounting is providing both unit-and activity-based accounting information (made possible by a recent pilot study producing the activity-based data). Unit-based system: Variable conversion activity rate: 100 per direct labor hour Material usage rate: 20 per part ABC system: Labor usage: 15 per direct labor hour Material usage (direct materials): 20 per part Machining: 75 per machine hour Purchasing activity: 150 per purchase order Setup activity: 3,000 per setup hour Warranty activity: 500 per returned unit (usually requires extensive rework) Customer repair cost: 25 per repair hour (average) Required: 1. Select the lower-cost design using unit-based costing. Are logistical and post-purchase activities considered in this analysis? 2. Select the lower-cost design using ABC analysis. Explain why the analysis differs from the unit-based analysis. 3. What if the post-purchase cost was an environmental contaminant and amounted to 10 per unit for Design A and 40 per unit for Design B? Assume that the environmental cost is borne by society. Now which is the better design?arrow_forwardClassify the following environmental activities as prevention costs, detection costs, internal failure costs, or external failure costs. For external failure costs, classify the costs as societal or private. Also, label those activities that are compatible with sustainable development (SD). 1. A company takes actions to reduce the amount of material in its packages. 2. After the activated carbons useful life, a soft-drink producer returns this material used for purifying water for its beverages to the supplier. The supplier reactivates the carbon for a second use in nonfood applications. As a consequence, many tons of material are prevented from entering landfills. 3. An evaporator system is installed to treat wastewater and collect usable solids for other uses. 4. The inks used to print snack packages (for chips) contain heavy metals. 5. Processes are inspected to ensure compliance with environmental standards. 6. Delivery boxes are used five times and then recycled. This prevents 112 million pounds of cardboard from entering landfills and saves 2 million trees per year. 7. Scrubber equipment is installed to ensure that air emissions are less than the level permitted by law. 8. Local residents are incurring medical costs from illnesses caused by air pollution from automobile exhaust pollution. 9. As part of implementing an environmental perspective for the Balanced Scorecard, environmental performance measures are developed. 10. Because of liquid and solid residues being discharged into a local lake, the lake is no longer fit for swimming, fishing, and other recreational activities. 11. To reduce energy consumption, magnetic ballasts are replaced with electronic ballasts, and more efficient light bulbs and lighting sensors are installed. As a result, 2.3 million kilowatt-hours of electricity are saved per year. 12. Due to a legal settlement, a chemicals company must spend 20,000,000 to clean up contaminated soil. 13. A soft-drink company uses the following practice: In all bottling plants, packages damaged during filling are collected and recycled (glass, plastic, and aluminum). 14. Products are inspected to ensure that the gaseous emissions produced during operation follow legal and company guidelines. 15. Operating pollution control equipment incurs costs. 16. An internal audit is conducted to verify that environmental policies are being followed.arrow_forwardTwo products, Product A and Product B, are associated with the following environmental activities and associated data: Driver data: Which of the two products has the greatest environmental impact? a. Product A because its total environmental cost is 400,000. b. Product A because it causes more waste and pollution control than Product B. c. Product B because its total environmental cost is 400,000. d. Product B because its environmental cost per unit is five times more than Product As unit environmental cost.arrow_forward

- Coyle Pharmaceuticals produces two organic chemicals (Org AB and Org XY) used in the production of two of its most wide-selling anti-cancer drugs. The controller and environmental manager have identified the following environmental activities and costs associated with the two products: Required: 1. Calculate the environmental cost per pound for each product. Which of the two products appears to cause the most degradation to the environment? 2. In which environmental category would you classify excessive use of materials and energy? 3. Suppose that the toxin releases cause health problems for those who live near the chemical plant. The costs, due to missed work and medical treatments, are estimated at 2,025,000 per year. How would assignment of these costs change the unit cost? Should they be assigned?arrow_forwardRefer to Problem 14.41. In the environmental benefits section of the report, three types of benefits are listed: income, savings, and cost avoidance. Now, consider the following data for selected items for a four-year period: The engineering design costs were incurred to redesign the production processes and products. Redesign of the product allowed the substitution of a material that produced less ozone-depleting substances. Modifications in the design of the processes also accomplished the same objective. Because of the improvements, the company was able to reduce the demand for pollution control equipment (with its attendant depreciation and operating costs) and avoid fines and litigation costs. All of the savings generated in a given year represent costs avoided for future years. The engineering costs are investments in design projects. Once the results of the project are realized, design costs can be reduced to lower levels. However, since some ongoing design activity is required for maintaining the system and improving it as needed, the environmental engineering cost will not be reduced lower than the 90,000 reported in 20x5. Required: 1. Prepare a partial environmental financial statement, divided into benefit and cost sections for 20x3, 20x4, and 20x5. 2. Evaluate and explain the outcomes. Does this result support or challenge ecoefficiency? Explain.arrow_forwardAbernathy, Inc., produces two different generators and is concerned about their quality. The company has identified the following quality activities and costs associated with the two products: Required: 1. Calculate the quality cost per unit for each product, and break this unit cost into quality cost categories. Which of the two seems to have the lowest quality? 2. How might a manager use the unit quality cost information?arrow_forward

- Auflegger, Inc., manufactures a product that experiences the following activities (and times): Required: 1. Compute the MCE for this product. 2. A study lists the following root causes of the inefficiencies: poor quality components from suppliers, lack of skilled workers, and plant layout. Suggest a possible cost reduction strategy, expressed as a series of if-then statements that will reduce MCE and lower costs. Finally, prepare a strategy map that illustrates the causal paths. In preparing the map, use only three perspectives: learning and growth, process, and financial. 3. Is MCE a lag or a lead measure? If and when MCE acts as a lag measure, what lead measures would affect it?arrow_forwardAt Jeekes PolyChem Products LLC, customers needs are translated into product specifications by the design or engineering department. Which of the following objectives of production management is addressed by Jeekes Polychem Products LLC? a. Right time b. Right quality c. Right quantity d. Right cost Mr. Saud bought a new mobile phone for himself. He explained to his friend that the mobile phone has a camera, Facebook facility, and music facility in addition to the basic functions like phone calls and messaging. Which dimension of "product quality" is Mr. Saud referring to? a. Features b. Aesthetics c. Reputation d. Conformancearrow_forwardThe Chopin Company has decided to introduce a new product. The new product can be manufactured by either a computer-assisted manufacturing (CAM) or a labor-intensive production (LIP) system. The manufacturing method will not affect the quality of the product. The estimated manufacturing costs for each of the two methods are as follows. CAM System: Direct Material = $5.0 Direct Labor (DLH) = 0.5 DLH X $12 = $6 Variable Overhead = 0.5DLHx$6 = $3 Fixed Iverhead* = $ 2,440,000 LIP System: Direct Material = $5.6 Direct Labor (DLH) = 0.8 DLH X $9 = $7.2 Variable Overhead = 0.8 DLH X $6 = $4.8 Fixed Overhead* = $1,320,000 *These costs are directly traceable to the new product line. They would not be incurred if the new product were not produced. The company’s marketing research department has recommended an introductory unit sales price of $30. Selling expenses are estimated to be $500,000 annually plus $2 for each unit sold. (Ignore income taxes.) Required 4. Describe the circumstances under…arrow_forward

- The Chopin Company has decided to introduce a new product. The new product can be manufactured by either a computer-assisted manufacturing (CAM) or a labor-intensive production (LIP) system. The manufacturing method will not affect the quality of the product. The estimated manufacturing costs for each of the two methods are as follows. CAM System: Direct Material = $5.0 Direct Labor (DLH) = 0.5 DLH X $12 = $6 Variable Overhead = 0.5DLHx$6 = $3 Fixed Iverhead* = $ 2,440,000 LIP System: Direct Material = $5.6 Direct Labor (DLH) = 0.8 DLH X $9 = $7.2 Variable Overhead = 0.8 DLH X $6 = $4.8 Fixed Overhead* = $1,320,000 *These costs are directly traceable to the new product line. They would not be incurred if the new product were not produced. The company’s marketing research department has recommended an introductory unit sales price of $30. Selling expenses are estimated to be $500,000 annually plus $2 for each unit sold. (Ignore income taxes.) Required: Calculate the estimated…arrow_forwardMariah Enterprises makes a variety of consumer electronic products. Its camera manufacturing plant is considering choosing between two different processes, named Alpha and Beta, which can be used to make two component parts A and B. To make the correct decision, the managers would like to compare the labor and multifactor productivity of process Alpha with that of process Beta. The value of process output for component A and B are $175 and $140 per unit, respectively. The corresponding overhead costs are $6,000 and $5,000, respectively. Process Alpha Process Beta Product A B C D Output (units) 50 60 30 80 Labor ($) $1,200 $1,400 $1,000 $2,000 Material ($) $2,500 $3,000 $1,400 $3,500 a. Which process, Alpha or Beta, is more productive? b. What conclusions can you draw from your analysis?arrow_forwardGreen Manufacturing is a traditional manufacturing company located in the midwestern United States. The company's operations manager is developing a strategy to become more CSR-oriented. In an effort to evaluate possible areas where CSR initiatives can be implemented, the manager has gathered the following data regarding three potential CSR activities: Initial Added Cost Variable Cost Variable Savings Recycle and reuse production materials $ 5,000 $0.10 per lb. of recycled material $0.15 per lb. of recycled material Add solar panels as a source of power 700,000 $ 1,000 per year $ 33,000 per year Replace assembly room light fixtures with natural light 120,000 $ 180 per month $ 220 per month The recycling activity would carry on indefinitely. The solar panels would have a useful life of 30 years. The replacement of assembly room light fixtures with natural light is assumed to have an 80-year effect. a. Identify which CSR activities Green Manufacturing should…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College