Concept explainers

Videos

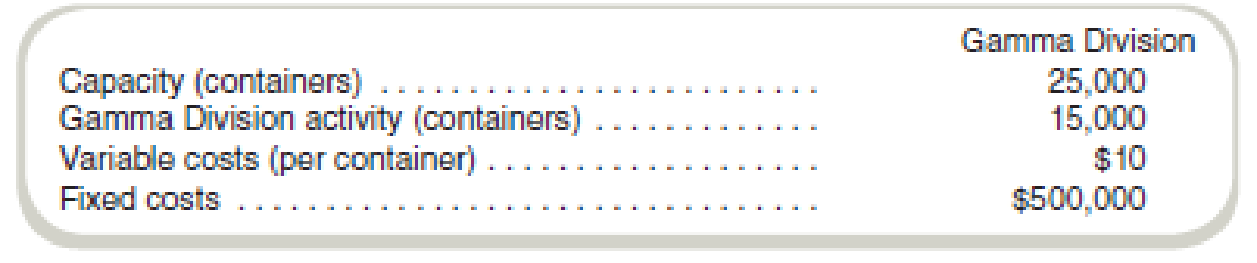

Weaver, Inc., is a large consumer products company, which manufactures health and beauty products sold at grocery and drug stores throughout the country. Gamma Division does both manufacturing and shipping and operates a warehouse and transportation activity in a central location. Gamma loads trucks with products and ships the products using third-party trucking companies to its regional distribution centers.

Weaver recently started a new enterprise, Nu, which would focus on logistics alone, providing transportation services to both other Weaver divisions and third parties. The manager of Nu proposes using the warehouse facility of Gamma, at least to start. Employees of Gamma would load the trucks for the Nu business as well as the Gamma business.

All divisions at Weaver are treated as profit centers with managers evaluated on division profit. The best estimates of the current activity and costs of Gamma Division follow:

Required

- a. The current activity estimated for Nu Division is 5,000 cases. The company has asked you to recommend a transfer price policy to implement. What transfer price would you recommend? Why?

- b. How would the division manager for Gamma Division likely respond? How would you answer?

- c. Another manager has identified another opportunity and also proposes using the Gamma Division facility. Estimated activity for this third division is expected to be 7,500 cases. How would you modify, if at all, your recommendation in requirement (a)?

Want to see the full answer?

Check out a sample textbook solution

Chapter 15 Solutions

Gen Combo Fundamentals Of Cost Accounting; Connect Access Card

- KarlAuto Corporation manufactures automobiles, vans, and trucks. Among the various KarlAuto plants around the United States is the Bloomington plant, where vinyl covers and upholstery fabric are sewn. These are used to cover interior seating and other surfaces of KarlAuto products. Pam Teegin is the plant manager for the Bloomington cover plantthe first KarlAuto plant in the region. As other area plants were opened, Teegin, in recognition of her management ability, was given the responsibility to manage them. Teegin functions as a regional manager, although the budget for her and her staff is charged to the Bloomington plant. Teegin has just received a report indicating that KarlAuto could purchase the entire annual output of the Bloomington cover plant from outside suppliers for 32 million. Teegin was astonished at the low outside price, because the budget for the Bloomington plants operating costs was set at 56.45 million. Teegin believes that the Bloomington plant will have to close down operations in order to realize the 24.45 million in annual cost savings. The budget (in thousands) for the Bloomington plants operating costs for the coming year follows: Additional facts regarding the plants operations are as follows: Due to the Bloomington plants commitment to use high-quality fabrics in all of its products, the Purchasing Department was instructed to place blanket orders with major suppliers to ensure the receipt of sufficient materials for the coming year. If these orders are canceled as a consequence of the plant closing, termination charges would amount to 18 percent of the cost of direct materials. Approximately 600 plant employees will lose their jobs if the plant is closed. This includes all direct laborers and supervisors as well as the plumbers, electricians, and other skilled workers classified as indirect plant workers. Some would be able to find new jobs, but many others would have difficulty. All employees would have difficulty matching the Bloomington plants base pay of 29.40 per hour, the highest in the area. A clause in the Bloomington plants contract with the union may help some employees; the company must provide employment assistance to its former employees for 12 months after a plant closing. The estimated cost to administer this service would be 1 million for the year. Some employees would probably elect early retirement because the company has an excellent pension plan. In fact, 4.6 million of next years pension expense would continue whether or not the plant is open. Teegin and her staff would not be affected by the closing of the Bloomington plant. They would still be responsible for administering three other area plants. Equipment depreciation for the plant is considered to be a variable cost and the units-of-production method is used to depreciate equipment; the Bloomington plant is the only KarlAuto plant to use this depreciation method. However, it uses the customary straight-line method to depreciate its building. Required: 1. Prepare a quantitative analysis to help in deciding whether or not to close the Bloomington plant. Explain how you treated the nonrecurring relevant costs. 2. Consider the analysis in Requirement 1, and add to it the qualitative factors that you believe are important to the decision. What is your decision? Would you close the plant? Explain. (CMA adapted)arrow_forwardThe Mega Supply Corporation has three divisions: Commercial Products, Consumer Products, and Corporate Offices, which are located in Hatfield, South Carolina; Palo Alto, California; and Tulsa, Oklahoma, respectively. The Commercial Products division deals exclusively in sales of industrial products and supplies to business organizations. The Consumer Products division sells nonindustrial products to private consumers. Both divisions have dedicated inventory warehouses at their respective locations in Hatfield and Palo Alto. Because of the dissimilar nature of the commercial and consumer division product lines, they do not share customers or vendors. Currently Mega Supply uses a centralized database, which is located at their Corporate Division in Tulsa. Some relevant database tables and attributes are presented in the figure designated Problem 1. When customers contact their respective sales division, the sales clerk logs into the corporate database, checks credit, determines product availability, and creates a sales invoice. The corporate office typically bills the customer within 3 or 4 days and extends terms of net 30. Inventory control, AR processing, cash receipts, purchases from vendors and AP processing, and cash disbursements are performed by the corporate office. Due to Megas rapid growth, the company has seen a significant increase in sales and purchase transactions, which has resulted in excessive delays in processing transactions from the central database. Since customer service, including rapid response to customer inquiries and sales order processing, is a cornerstone of Megas business model, these delays are unacceptable. Required Mega wants to improve response time by distributing some parts of the corporate database while keeping other parts of it centralized. (A) Develop a schema for distributing Mega Supply Corporations database. Add new tables and attributes as needed but limit the schema to the tables needed to support sales, cash receipts, purchases/AP, and cash disbursements. In your schema, indicate whether tables are centralized, replicated, or partitioned. (B) Explain how the new system will operate.arrow_forwardQuincy Farms is a producer of items made from farm products that are distributed to supermarkets. For many years, Quincys products have had strong regional sales on the basis of brand recognition. However, other companies have been marketing similar products in the area, and price competition has become increasingly important. Doug Gilbert, the companys controller, is planning to implement a standard costing system for Quincy and has gathered considerable information from his coworkers on production and direct materials requirements for Quincys products. Doug believes that the use of standard costing will allow Quincy to improve cost control and make better operating decisions. Quincys most popular product is strawberry jam. The jam is produced in 10-gallon batches, and each batch requires six quarts of good strawberries. The fresh strawberries are sorted by hand before entering the production process. Because of imperfections in the strawberries and spoilage, one quart of strawberries is discarded for every four quarts of acceptable berries. Three minutes is the standard direct labor time required for sorting strawberries in order to obtain one quart of strawberries. The acceptable strawberries are then processed with the other ingredients: processing requires 12 minutes of direct labor time per batch. After processing, the jam is packaged in quart containers. Doug has gathered the following information from Joe Adams, Quincys cost accountant, relative to processing the strawberry jam. a. Quincy purchases strawberries at a cost of 0.80 per quart. All other ingredients cost a total of 0.45 per gallon. b. Direct labor is paid at the rate of 9.00 per hour. c. The total cost of direct material and direct labor required to package the jam is 0.38 per quart. Joe has a friend who owns a strawberry farm that has been losing money in recent years. Because of good crops, there has been an oversupply of strawberries, and prices have dropped to 0.50 per quart. Joe has arranged for Quincy to purchase strawberries from his friends farm in hopes that the 0.80 per quart will put his friends farm in the black. Required: 1. Discuss which coworkers Doug probably consulted to set standards. What factors should Doug consider in establishing the standards for direct materials and direct labor? 2. Develop the standard cost sheet for the prime costs of a 10-gallon batch of strawberry jam. 3. Citing the specific standards of the IMA Statement of Ethical Professional Practice described in Chapter 1, explain why Joes behavior regarding the cost information provided to Doug is unethical. (CMA adapted)arrow_forward

- Sembotix Company has several divisions including a Semiconductor Division that sells semiconductors to both internal and external customers. The company's X-ray Division uses semiconductors as a component in its final product and is evaluating whether to purchase them from the Semiconductor Division or from an external supplier. The market price for semiconductors is $100 per 100 semiconductors. Dave Bryant is the controller of the X-ray Division, and Howard Hillman is the controller of the Semiconductor Division. The following conversation took place between Dave and Howard: Dave: I hear you are having problems selling semiconductors out of your division. Maybe I can help. Howard: You've got that right. We're producing and selling at about 90% of our capacity to outsiders. Last year we were selling 100% of capacity. Would it be possible for your division to pick up some of the excess capacity? After all, we are part of the same company. Dave: What kind of price can you give me?…arrow_forwardCode Incorporated has three divisions (Entertainment, Plastics, and Video Card), each of which is considered an investment center for performance evaluation purposes. The Entertainment Division manufactures video arcade equipment using products produced by the other two divisions, as follows: 1. The Entertainment Division purchases plastic components from the Plastics Division that are considered unique (i.e., they are made exclusively for the Entertainment Division). In addition, the Plastics Division makes less-complex plastic components that it sells externally, to other producers. 2. The Entertainment Division purchases, for each unit it produces, a video card from Code's Video Card Division, which also sells this video card externally (to other producers). The per-unit manufacturing costs associated with each of the above two items, as incurred by the Plastic Components Division and the Video Card Division, respectively, are: Plastic Components Video Cards Direct…arrow_forwardQualSupport Corporation manufactures seats for automobiles, vans, trucks, and various recreational vehicles. The company has a number of plants around the world, including the Denver Cover Plant, which makes seat covers. Ted Vosilo is the plant manager of the Denver Cover Plant but also serves as the regional production manager for the company. His budget as the regional manager is charged to the Denver Cover Plant. Vosilo has just heard that QualSupport has received a bid from an outside vendor to supply the equivalent of the entire annual output of the Denver Cover Plant for $35 million. Vosilo was astonished at the low outside bid because the budget for the Denver Cover Plant’s operating costs for the upcoming year was set at $52 million. If this bid is accepted, the Denver Cover Plant will be closed down. The budget for Denver Cover’s operating costs for the coming year is presented below. Denver Cover PlantAnnual Budget for Operating Costs Materials $ 14,000,000…arrow_forward

- Speed Racer in Victoria makes bicycles for people of all ages. The frames division makes and paints the frames and supplies them to the assembly division where the bicycles are assembled. Speed Racer is a successful and profitable corporation that attributes much of its success to its decentralized operating style. Each division manager is compensated on the basis of division operating income. The assembly division currently acquires all its frames from the frames division. The assembly division manager could purchase similar frames in the market for $480. The frames division is currently operating at 80% of its capacity of 4,000 frames (units) and has the following details: Voltage Regulator Direct materials ($150 per unit x 320 units) $480,000 Direct manufacturing labour ($60 per unit x 3,200 units) 192,000 Variable manufacturing overhead costs ($30 per unit × 3,200 units) 96,000 Fixed manufacturing overhead costs $624,000 All the frames division’s…arrow_forwardSpeed Racer in Victoria makes bicycles for people of all ages. The frames division makes and paints the frames and supplies them to the assembly division where the bicycles are assembled. Speed Racer is a successful and profitable corporation that attributes much of its success to its decentralized operating style. Each division manager is compensated on the basis of division operating income. The assembly division currently acquires all its frames from the frames division. The assembly division manager could purchase similar frames in the market for $480. The frames division is currently operating at 80% of its capacity of 4,000 frames (units) and has the following details: Voltage Regulator Direct materials ($150 per unit x 320 units) $480,000 Direct manufacturing labour ($60 per unit x 3,200 units) 192,000 Variable manufacturing overhead costs ($30 per unit × 3,200 units) 96,000 Fixed manufacturing overhead costs $624,000 All the frames…arrow_forwardSpeed Racer in Victoria makes bicycles for people of all ages. The frames division makes and paints the frames and supplies them to the assembly division where the bicycles are assembled. Speed Racer is a successful and profitable corporation that attributes much of its success to its decentralized operating style. Each division manager is compensated on the basis of division operating income. The assembly division currently acquires all its frames from the frames division. The assembly division manager could purchase similar frames in the market for $480. The frames division is currently operating at 80% of its capacity of 4,000 frames (units) and has the following details: Voltage Regulator Direct materials ($150 per unit x 320 units) $480,000 Direct manufacturing labour ($60 per unit x 3,200 units) 192,000 Variable manufacturing overhead costs ($30 per unit × 3,200 units) 96,000 Fixed manufacturing overhead costs $624,000 All the frames division’s…arrow_forward

- Speed Racer in Victoria makes bicycles for people of all ages. The frames division makes and paints the frames and supplies them to the assembly division where the bicycles are assembled. Speed Racer is a successful and profitable corporation that attributes much of its success to its decentralized operating style. Each division manager is compensated on the basis of division operating income. The assembly division currently acquires all its frames from the frames division. The assembly division manager could purchase similar frames in the market for $480. The frames division is currently operating at 80% of its capacity of 4,000 frames (units) and has the following details: Voltage Regulator Direct materials ($150 per unit x 320 units) $480,000 Direct manufacturing labour ($60 per unit x 3,200 units) 192,000 Variable manufacturing overhead costs ($30 per unit × 3,200 units) 96,000 Fixed manufacturing overhead costs $624,000 All the frames…arrow_forwardSpeed Racer in Victoria makes bicycles for people of all ages. The frames division makes and paints the frames and supplies them to the assembly division where the bicycles are assembled. Speed Racer is a successful and profitable corporation that attributes much of its success to its decentralized operating style. Each division manager is compensated on the basis of division operating income. The assembly division currently acquires all its frames from the frames division. The assembly division manager could purchase similar frames in the market for $480. The frames division is currently operating at 80% of its capacity of 4,000 frames (units) and has the following details: Voltage Regulator Direct materials ($150 per unit x 320 units) $480,000 Direct manufacturing labour ($60 per unit x 3,200 units) 192,000 Variable manufacturing overhead costs ($30 per unit × 3,200 units) 96,000 Fixed manufacturing overhead costs $624,000 All the frames division’s…arrow_forwardualSupport Corporation manufactures seats for automobiles, vans, trucks, and various recreational vehicles. The company has a number of plants around the world, including the Denver Cover Plant, which makes seat covers. Ted Vosilo is the plant manager of the Denver Cover Plant but also serves as the regional production manager for the company. His budget as the regional manager is charged to the Denver Cover Plant. Vosilo has just heard that QualSupport has received a bid from an outside vendor to supply the equivalent of the entire annual output of the Denver Cover Plant for $20.19 million. Vosilo was astonished at the low outside bid because the budget for the Denver Cover Plant’s operating costs for the upcoming year was set at $23.49 million. If this bid is accepted, the Denver Cover Plant will be closed down. The budget for Denver Cover’s operating costs for the coming year is presented below. Denver Cover Plant Annual Budget for Operating Costs Materials $…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Auditing: A Risk Based-Approach to Conducting a Q...AccountingISBN:9781305080577Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:South-Western College Pub

Auditing: A Risk Based-Approach to Conducting a Q...AccountingISBN:9781305080577Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:South-Western College Pub