Videos

KarlAuto Corporation manufactures automobiles, vans, and trucks. Among the various KarlAuto plants around the United States is the Bloomington plant, where vinyl covers and upholstery fabric are sewn. These are used to cover interior seating and other surfaces of KarlAuto products.

Pam Teegin is the plant manager for the Bloomington cover plant—the first KarlAuto plant in the region. As other area plants were opened, Teegin, in recognition of her management ability, was given the responsibility to manage them. Teegin functions as a regional manager, although the budget for her and her staff is charged to the Bloomington plant.

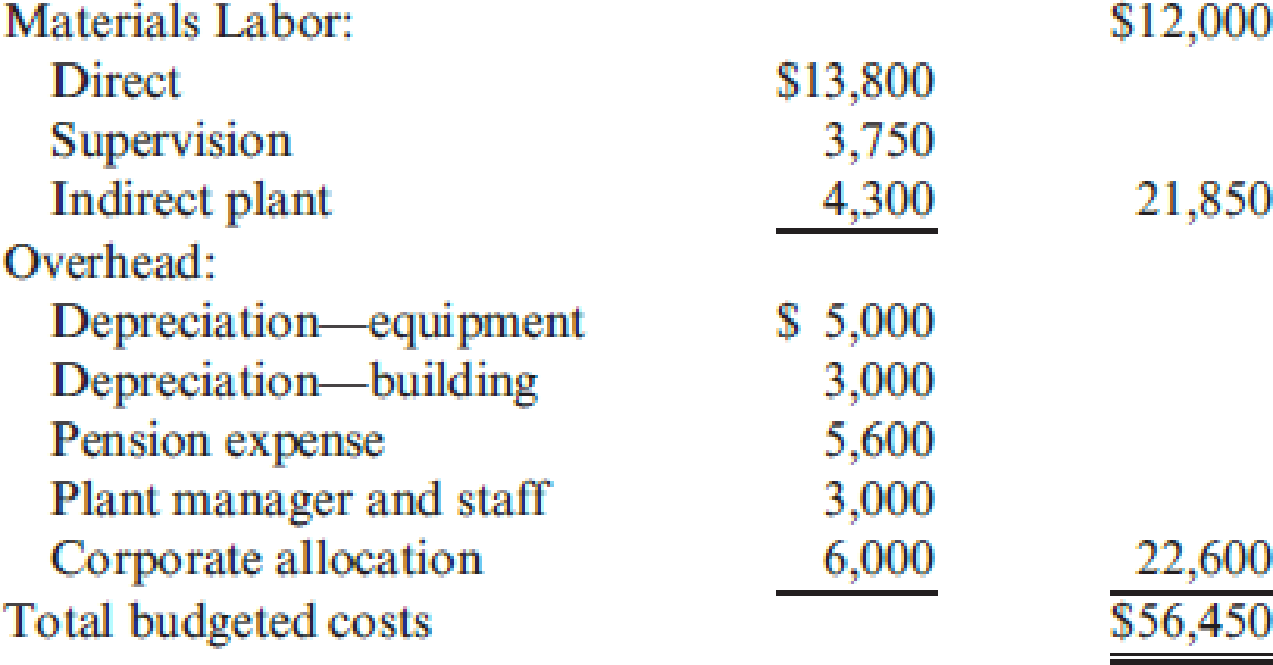

Teegin has just received a report indicating that KarlAuto could purchase the entire annual output of the Bloomington cover plant from outside suppliers for $32 million. Teegin was astonished at the low outside price, because the budget for the Bloomington plant’s operating costs was set at $56.45 million. Teegin believes that the Bloomington plant will have to close down operations in order to realize the $24.45 million in annual cost savings.

The budget (in thousands) for the Bloomington plant’s operating costs for the coming year follows:

Additional facts regarding the plant’s operations are as follows:

Due to the Bloomington plant’s commitment to use high-quality fabrics in all of its products, the Purchasing Department was instructed to place blanket orders with major suppliers to ensure the receipt of sufficient materials for the coming year. If these orders are canceled as a consequence of the plant closing, termination charges would amount to 18 percent of the cost of direct materials.

Approximately 600 plant employees will lose their jobs if the plant is closed. This includes all direct laborers and supervisors as well as the plumbers, electricians, and other skilled workers classified as indirect plant workers. Some would be able to find new jobs, but many others would have difficulty. All employees would have difficulty matching the Bloomington plant’s base pay of $29.40 per hour, the highest in the area. A clause in the Bloomington plant’s contract with the union may help some employees; the company must provide employment assistance to its former employees for 12 months after a plant closing. The estimated cost to administer this service would be $1 million for the year.

Some employees would probably elect early retirement because the company has an excellent pension plan. In fact, $4.6 million of next year’s pension expense would continue whether or not the plant is open.

Teegin and her staff would not be affected by the closing of the Bloomington plant. They would still be responsible for administering three other area plants.

Equipment

Required:

- 1. Prepare a quantitative analysis to help in deciding whether or not to close the Bloomington plant. Explain how you treated the nonrecurring relevant costs.

- 2. Consider the analysis in Requirement 1, and add to it the qualitative factors that you believe are important to the decision. What is your decision? Would you close the plant? Explain. (CMA adapted)

Trending nowThis is a popular solution!

Chapter 17 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Rick Pines and Joe Lopez are the plant managers for High Mountain Lumber’s particleboard division. High Mountain Lumber has adopted a just-in-time management philosophy. Each plant combines wood chips with chemical adhesives to produce particle board to order, and all product is sold as soon as it is completed. Laura Green is High Mountain Lumber’s regional controller. All of High Mountain Lumber’s plants and divisions send Green their production and cost information. While reviewing the numbers of the two particleboard plants, she is surprised to find that both plants estimate their ending Work-in-Process Inventories at 75% complete, which is higher than usual. Green calls Lopez, whom she has known for some time. He admits that to ensure their division would meet its profit goal and that both he and Pines would make their bonus (which is based on division profit), they agreed to inflate the percentage completion. Lopez explains, “Determining the percent complete always requires…arrow_forwardRick Pines and Joe Lopez are the plant managers for High Mountain Lumber’s particle board division. High Mountain Lumber has adopted a just-in-time management philosophy. Each plant combines wood chips with chemical adhesives to produce particle board to order, and all product is sold as soon as it is completed. Laura Green is High Mountain Lumber’s regional controller. All of High Mountain Lumber’s plants and divisions send Green their production and cost information. While reviewing the numbers of the two particle board plants, she is surprised to find that both plants estimate their ending Work-in-Process Inventories at 75% complete, which is higher than usual. Green calls Lopez, whom she has known for some time. He admits that to ensure their division would meet its profit goal and that both he and Pines would make their bonus (which is based on division profit), they agreed to inflate the percentage completion. Lopez explains, “Determining the percent complete always requires…arrow_forwardQuincy Farms is a producer of items made from farm products that are distributed to supermarkets. For many years, Quincys products have had strong regional sales on the basis of brand recognition. However, other companies have been marketing similar products in the area, and price competition has become increasingly important. Doug Gilbert, the companys controller, is planning to implement a standard costing system for Quincy and has gathered considerable information from his coworkers on production and direct materials requirements for Quincys products. Doug believes that the use of standard costing will allow Quincy to improve cost control and make better operating decisions. Quincys most popular product is strawberry jam. The jam is produced in 10-gallon batches, and each batch requires six quarts of good strawberries. The fresh strawberries are sorted by hand before entering the production process. Because of imperfections in the strawberries and spoilage, one quart of strawberries is discarded for every four quarts of acceptable berries. Three minutes is the standard direct labor time required for sorting strawberries in order to obtain one quart of strawberries. The acceptable strawberries are then processed with the other ingredients: processing requires 12 minutes of direct labor time per batch. After processing, the jam is packaged in quart containers. Doug has gathered the following information from Joe Adams, Quincys cost accountant, relative to processing the strawberry jam. a. Quincy purchases strawberries at a cost of 0.80 per quart. All other ingredients cost a total of 0.45 per gallon. b. Direct labor is paid at the rate of 9.00 per hour. c. The total cost of direct material and direct labor required to package the jam is 0.38 per quart. Joe has a friend who owns a strawberry farm that has been losing money in recent years. Because of good crops, there has been an oversupply of strawberries, and prices have dropped to 0.50 per quart. Joe has arranged for Quincy to purchase strawberries from his friends farm in hopes that the 0.80 per quart will put his friends farm in the black. Required: 1. Discuss which coworkers Doug probably consulted to set standards. What factors should Doug consider in establishing the standards for direct materials and direct labor? 2. Develop the standard cost sheet for the prime costs of a 10-gallon batch of strawberry jam. 3. Citing the specific standards of the IMA Statement of Ethical Professional Practice described in Chapter 1, explain why Joes behavior regarding the cost information provided to Doug is unethical. (CMA adapted)arrow_forward

- Paul Golding and his wife, Nancy, established Crunchy Chips in 1938. Over the past 60 years, the company has established distribution channels in 11 western states, with production facilities in Utah, New Mexico, and Colorado. In 1980, Pauls son, Edward, took control of the business. By 2017, it was clear that the companys plants needed to gain better control over production costs to stay competitive. Edward hired a consultant to install a standard costing system. To help the consultant establish the necessary standards, Edward sent her the following memo: The manufacturing process for potato chips begins when the potatoes are placed into a large vat in which they are automatically washed. After washing, the potatoes flow directly to an automatic peeler. The peeled potatoes then pass by inspectors, who manually cut out deep eyes or other blemishes. After inspection, the potatoes are automatically sliced and dropped into the cooking oil. The frying process is closely monitored by an employee. After the chips are cooked, they pass under a salting device and then pass by more inspectors, who sort out the unacceptable finished chips (those that are discolored or too small). The chips then continue on the conveyor belt to a bagging machine that bags them in 1-pound bags. After bagging, the bags are placed in a box and shipped. The box holds 15 bags. The raw potato pieces (eyes and blemishes), peelings, and rejected finished chips are sold to animal feed producers for 0.16 per pound. The company uses this revenue to reduce the cost of potatoes. We would like this reflected in the price standard relating to potatoes. Crunchy Chips purchases high-quality potatoes at a cost of 0.245 per pound. Each potato averages 4.25 ounces. Under efficient operating conditions, it takes four potatoes to produce one 16-ounce bag of plain chips. Although we label bags as containing 16 ounces, we actually place 16.3 ounces in each bag. We plan to continue this policy to ensure customer satisfaction. In addition to potatoes, other raw materials are the cooking oil, salt, bags, and boxes. Cooking oil costs 0.04 per ounce, and we use 3.3 ounces of oil per bag of chips. The cost of salt is so small that we add it to overhead. Bags cost 0.11 each and boxes 0.52 each. Our plant produces 8.8 million bags of chips per year. A recent engineering study revealed that we would need the following direct labor hours to produce this quantity if our plant operates at peak efficiency: Im not sure that we can achieve the level of efficiency advocated by the study. In my opinion, the plant is operating efficiently for the level of output indicated if the hours allowed are about 10% higher. The hourly labor rates agreed upon with the union are: Overhead is applied on the basis of direct labor dollars. We have found that variable overhead averages about 116% of our direct labor cost. Our fixed overhead is budgeted at 1,135,216 for the coming year. Required: 1. Discuss the benefits of a standard costing system for Crunchy Chips. 2. Discuss the presidents concern about using the result of the engineering study to set the labor standards. What standard would you recommend? 3. Form a group with two or three other students. Develop a standard cost sheet for Crunchy Chips plain potato chips. Round all computations to four decimal places. 4. Suppose that the level of production was 8.8 million bags of potato chips for the year as planned. If 9.5 million pounds of potatoes were used, compute the materials usage variance for potatoes.arrow_forwardMossfort, Inc., has a division in Canada that makes long-lasting exterior wood stain. Mossfort has another U.S. division, the Retail Division, that operates a chain of home improvement stores. The Retail Division would like to buy the unique, long-lasting wood stain from the Canadian division, since this type of stain is not currently available. The Exterior Stain Division incurs manufacturing costs of 13.45 for one gallon of stain. If the Retail Division purchases the stain from the Canadian division, the shipping costs will be 1.40 per gallon, but sales commissions of 0.75 per gallon will be avoided with an internal transfer. The Retail Division plans to sell the stain for 32.80 per gallon. Normally, the Retail Division earns a gross margin of 35 percent above cost of goods sold. Required: 1. Which Section 482 method should be used to calculate the allowable transfer price? 2. Calculate the appropriate transfer price per gallon. (Round to the nearest cent.)arrow_forwardPaterson Company, a U.S.-based company, manufactures and sells electronic components worldwide. Virtually all its manufacturing takes place in the United States. The company has marketing divisions throughout Europe, including France. Debbie Kishimoto, manager of this division, was hired from a competitor 3 years ago. Debbie, recently informed of a price increase in one of the major product lines, requested a meeting with Jeff Phillips, marketing vice president. Their conversation follows. Debbie: Jeff, I simply dont understand why the price of our main product has increased from 5.00 to 5.50 per unit. We negotiated an agreement earlier in the year with our manufacturing division in Philadelphia for a price of 5.00 for the entire year. I called the manager of that division. He said that the original price was still acceptablethat the increase was a directive from headquarters. Thats why I wanted to meet with you. I need some explanations. When I was hired, I was told that pricing decisions were made by the divisions. This directive interferes with this decentralized philosophy and will lower my divisions profits. Given current market conditions, there is no way we can pass on the cost increase. Profits for my division will drop at least 600,000 if this price is maintained. I think a midyear increase of this magnitude is unfair to my division. Jeff: Under normal operating conditions, headquarters would not interfere with divisional decisions. But as a company, we are having some problems. What you just told me is exactly why the price of your product has been increased. We want the profits of all our European marketing divisions to drop. Debbie: What do you mean that you want the profits to drop? That doesnt make any sense. Arent we in business to make money? Jeff: Debbie, what you lack is corporate perspective. We are in business to make money, and thats why we want European profits to decrease. Our U.S. divisions are not doing well this year. Projections show significant losses. At the same time, projections for European operations show good profitability. By increasing the cost of key products transferred to Europeto your division, for examplewe increase revenues and profits in the United States. By decreasing your profits, we avoid paying taxes in France. With losses on other U.S. operations to offset the corresponding increase in domestic profits, we avoid paying taxes in the United States as well. The net effect is a much-needed increase in our cash flow. Besides, you know how hard it is in some of these European countries to transfer out capital. This is a clean way of doing it. Debbie: Im not so sure that its clean. I cant imagine the tax laws permitting this type of scheme. There is another problem, too. You know that the companys bonus plans are tied to a divisions profits. This plan could cost all of the European managers a lot of money. Jeff: Debbie, you have no reason to worry about the effect on your bonusor on our evaluation of your performance. Corporate management has already taken steps to ensure no loss of compensation. The plan is to compute what income would have been if the old price had prevailed and base bonuses on that figure. Ill meet with the other divisional managers and explain the situation to them as well. Debbie: The bonus adjustment seems fair, although I wonder if the reasons for the drop in profits will be remembered in a couple of years when Im being considered for promotion. Anyway, I still have some strong ethical concerns about this. How does this scheme relate to the tax laws? Jeff: We will be in technical compliance with the tax laws. In the United States, Section 482 of the Internal Revenue Code governs this type of transaction. The key to this law, as well as most European laws, is evidence of an arms-length price. Since youre a distributor, we can use the resale price method to determine such a price. Essentially, the arms-length price for the transferred good is backed into by starting with the price at which you sell the product and then adjusting that price for the markup and other legitimate differences, such as tariffs and transportation. Debbie: If I were a French tax auditor, I would wonder why the markup dropped from last year to this year. Are we being good citizens and meeting the fiscal responsibilities imposed on us by each country in which we operate? Jeff: Well, a French tax auditor might wonder about the drop in markup. But, the markup is still within reason, and we can make a good argument for increased costs. In fact, weve already instructed the managers of our manufacturing divisions to legitimately reassign as many costs as they can to the European product lines. So far, they have been very successful. I think our records will support the increase that you are receiving. You really do not need to be concerned with the tax authorities. Our tax department assures me that this has been carefully researchedits unlikely that a tax audit will create any difficulties. Itll all be legal and above board. Weve done this several times in the past with total success. Required: 1. Do you think that the tax-minimization scheme described to Debbie Kishimoto is in harmony with the ethical behavior that should be displayed by top corporate executives? Why or why not? What would you do if you were Debbie? 2. Apparently, the tax department of Paterson Company has been strongly involved in developing the tax-minimization scheme. Assume that the accountants responsible for the decision are CMAs and members of the IMA, subject to the IMA standards of ethical conduct. Review the IMA standards for ethical conduct in Chapter 1. Are any of these standards being violated by the accountants in Patersons tax department? If so, identify them. What should these tax accountants do if requested to develop a questionable taxminimization scheme?arrow_forward

- Production of sofas at the Cosyhome factory depends on two highly autonomous divisions within the firm. The Woodie division is responsible for manufacturing the wooden chair frame and the Softie division produces the fabric to cover the chairs. Cosyhome operates in a very seasonal and highly competitive market and therefore is keen to implement improvements to its products. One such improvement is a revolutionary new nylon fabric. The Softie division has been asked by the Woodie division to produce the fabric for 4,000 chairs. If Softie meets this request, it will have to reduce output of its existing fabric which it currently sells to firms outside Cosyhome at £15 per metre. This is also the price Woodie must pay for any material purchased from Softie. No external market is expected to be available for the highly specialised nylon fabric. Woodie anticipates that chairs made with the new material will be sold for £23.90 more than at present. Market resistance to higher prices will…arrow_forwardCompu Limited is a company that manufactures computer monitors, keyboards, computer boxes and modems (both internal and external). These four products are sold all over the country and in a few overseas markets. The head office is situated in Sandton, South Africa, with three plants in other parts of the country. Four years ago, a fourth plant was opened in Zimbabwe to take advantage of the inexpensive labour available. 90% of the items manufactured in Zimbabwe are shipped back to South Africa and the remaining 10% are sold in other African countries. Compu Limited advertises its products in computer magazines, on the internet and over the television. It shares are traded on the Johannesburg Stock Exchange (JSE). Three major organisations account for almost 50% of Compu’s sales and the remaining sales are made to other smaller computer manufacturers. Lately one of these customers is constantly complaining about the lack of new technology in Compu’s products. A total of 900 plant…arrow_forwardCompu Limited is a company that manufactures computer monitors, keyboards, computer boxes and modems (both internal and external). These four products are sold all over the country and in a few overseas markets. The head office is situated in Sandton, South Africa, with three plants in other parts of the country. Four years ago, a fourth plant was opened in Zimbabwe to take advantage of the inexpensive labour available. 90% of the items manufactured in Zimbabwe are shipped back to South Africa and the remaining 10% are sold in other African countries. Compu Limited advertises its products in computer magazines, on the internet and over the television. It shares are traded on the Johannesburg Stock Exchange (JSE). Three major organisations account for almost 50% of Compu’s sales and the remaining sales are made to other smaller computer manufacturers. Lately one of these customers is constantly complaining about the lack of new technology in Compu’s products. A total of 900 plant…arrow_forward

- Washington, Inc., makes three models of motorized carts for vacation resorts, X-10, X-20, and X-40. Washington manufactures the carts in two assembly departments: Department A and Department B. All three models are processed initially in Department A, where all material is assembled. The X-10 model is then transferred to finished goods. After processing in Department A, the X-20 and X-40 models are transferred to Department B for final assembly, and then transferred to finished goods. There were no beginning work-in-process inventories on April 1. Data for April are shown in the following table. Ending work in process is 25 percent complete in Department A and 60 percent complete in Department B. Conversion costs are allocated based on the number of equivalent units processed in each department. Total X-10 X-20 X-40 Units started 500 300 200 Units completed in Department A 400 260 180 Units completed in Department B 225…arrow_forwardWashington, Inc., makes three models of motorized carts for vacation resorts, X-10, X-20, and X-40. Washington manufactures the carts in two assembly departments: Department A and Department B. All three models are processed initially in Department A, where all material is assembled. The X-10 model is then transferred to finished goods. After processing in Department A, the X-20 and X-40 models are transferred to Department B for final assembly, and then transferred to finished goods.There were no beginning work-in-process inventories on April 1. Data for April are shown in the following table. Ending work in process is 20 percent complete in Department A and 60 percent complete in Department B. Conversion costs are allocated based on the number of equivalent units processed in each department. Total X-10 X-20 X-40 Units started 510 390 270 Units completed in Department A 440 250 180 Units completed in Department B 225…arrow_forwardThe Blair Company’s three assembly plants are located in California, Georgia, and New Jersey. Previously, the company purchased a major subassembly, which becomes part of the final product, from an outside firm. Blair has decided to manufacture the subassemblies within the company and must now consider whether to rent one centrally located facility (e.g., in Missouri, where all the subassemblies would be manufactured) or to rent three separate facilities, each located near one of the assembly plants, where each facility would manufacture only the subassemblies needed for the nearby assembly plant. A single, centrally located facility, with a production capacity of 18,000 units per year, would have fixed costs of $900,000 per year and a variable cost of $250 per unit. Three separate decentralized facilities, with production capacities of 8,000, 6,000, and 4,000 units per year, would have fixed costs of $475,000, $425,000, and $400,000, respectively, and variable costs per unit of only…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Auditing: A Risk Based-Approach to Conducting a Q...AccountingISBN:9781305080577Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:South-Western College Pub

Auditing: A Risk Based-Approach to Conducting a Q...AccountingISBN:9781305080577Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:South-Western College Pub