INTERMEDIATE ACCOUNTING RMU 9TH EDITION

9th Edition

ISBN: 9781260998726

Author: SPICELAND

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 16, Problem 16.30E

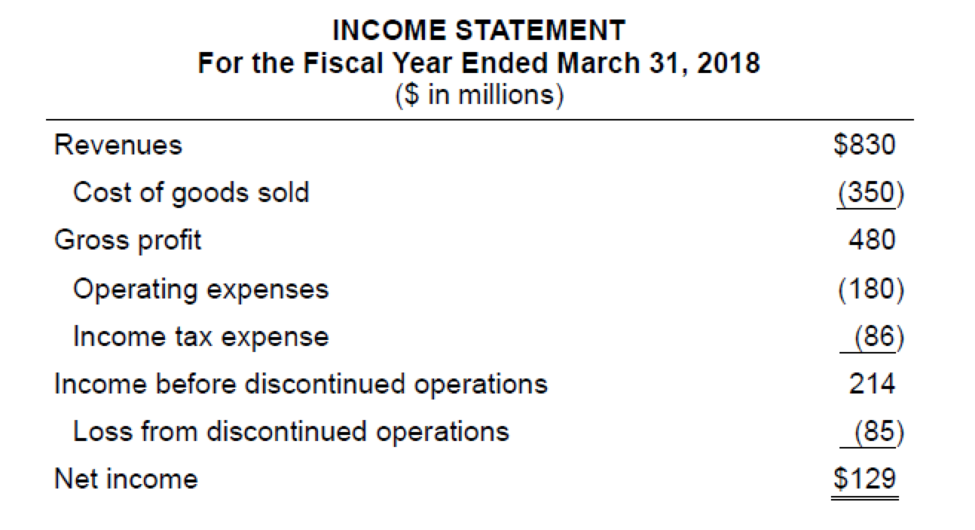

Intraperiod tax allocation

• LO16–10

The following income statement does not reflect intraperiod tax allocation.

Required:

Recast the income statement to reflect intraperiod tax allocation.

The company’s tax rate is 40%.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

7

Taxable income

Marginal tax rate

0-12.000 €

0%

12.001-30.000€

29%

30.001-75.000 €

39%

άνω 75.000 €

40%

Based on the data in the table above, calculate the total tax and the average tax rate for each of the following individuals:(i) A part-time employee with an annual income of € 8,000.(ii) A full-time employee with an annual income of € 35,000.(iii) A manager of a multinational company with an annual income of € 500,000.

Question 11: The taxable earnings threshold over which FUTA tax is not levied is:

Answer:

A.

O S7,000

В.

O $142,800

С.

S200,000

D.

S250,000

Item 2

The tax rates for a particular year are shown below:

Taxable Income

Tax Rate

$0 – 50,000

15

%

50,001 – 75,000

25

%

75,001 – 100,000

34

%

100,001 – 335,000

39

%

What is the average tax rate for a firm with taxable income of $129,513?

Chapter 16 Solutions

INTERMEDIATE ACCOUNTING RMU 9TH EDITION

Ch. 16 - Prob. 16.1QCh. 16 - A deferred tax liability (or asset) is described...Ch. 16 - Prob. 16.3QCh. 16 - Prob. 16.4QCh. 16 - Temporary differences result in future taxable or...Ch. 16 - Identify three examples of differences with no...Ch. 16 - The income tax rate for Hudson Refinery has been...Ch. 16 - Suppose a tax reform bill is enacted that causes...Ch. 16 - A net operating loss occurs when tax-deductible...Ch. 16 - Prob. 16.10Q

Ch. 16 - Additional disclosures are required pertaining to...Ch. 16 - Additional disclosures are required pertaining to...Ch. 16 - Prob. 16.13QCh. 16 - Prob. 16.14QCh. 16 - IFRS and U.S. GAAP follow similar approaches to...Ch. 16 - Temporary difference LO161 A company reports...Ch. 16 - Prob. 16.2BECh. 16 - Temporary difference LO162 A company reports...Ch. 16 - Prob. 16.4BECh. 16 - Temporary difference; income tax payable given ...Ch. 16 - Valuation allowance LO162, LO163 At the end of...Ch. 16 - Valuation allowance LO162, LO163 VeriFone Systems...Ch. 16 - Temporary and permanent differences; determine...Ch. 16 - Calculate taxable income LO161, LO164 Shannon...Ch. 16 - Multiple tax rates LO165 J-Matt, Inc., had pretax...Ch. 16 - Change in tax rate LO165 Superior Developers...Ch. 16 - Net operating loss carryforward LO167 During its...Ch. 16 - Net operating loss carryback LO167 AirParts...Ch. 16 - Tax uncertainty LO169 First Bank has some...Ch. 16 - Intraperiod tax allocation LO1610 Southeast...Ch. 16 - Temporary difference; taxable income given LO161...Ch. 16 - Prob. 16.2ECh. 16 - Prob. 16.3ECh. 16 - Prob. 16.4ECh. 16 - Prob. 16.5ECh. 16 - Prob. 16.6ECh. 16 - Identify future taxable amounts and future...Ch. 16 - Calculate income tax amounts under various...Ch. 16 - Determine taxable income LO161, LO162 Eight...Ch. 16 - Prob. 16.10ECh. 16 - Deferred tax asset; income tax payable given;...Ch. 16 - Prob. 16.12ECh. 16 - Prob. 16.13ECh. 16 - Multiple differences LO164, LO166 For the year...Ch. 16 - Multiple t ax rates LO162, LO165 Allmond...Ch. 16 - Prob. 16.16ECh. 16 - Deferred taxes; change in tax rates LO161, LO165...Ch. 16 - Multiple temporary differences; record income...Ch. 16 - Multiple temporary differences; record income...Ch. 16 - Net operating loss carryforward LO167 During...Ch. 16 - Net operating loss carryback LO167 Wynn Sheet...Ch. 16 - Net operating loss carryback and carryforward ...Ch. 16 - Identifying income tax deferrals LO161, LO162,...Ch. 16 - Multiple temporary differences; balance sheet...Ch. 16 - Multiple tax rates LO161, LO164, LO165 Case...Ch. 16 - Prob. 16.26ECh. 16 - Balance sheet classification LO168 As of December...Ch. 16 - Concepts; terminology LO161 through LO168 Listed...Ch. 16 - Tax credit; uncertainty regarding sustainability ...Ch. 16 - Intraperiod tax allocation LO1610 The following...Ch. 16 - FASB codification research LO165, LO168, LO1610...Ch. 16 - Prob. 16.1PCh. 16 - Prob. 16.2PCh. 16 - Prob. 16.3PCh. 16 - Prob. 16.4PCh. 16 - Change in tax rate; record taxes for four years ...Ch. 16 - Multiple differences; temporary difference yet to...Ch. 16 - Multiple differences; calculate taxable income;...Ch. 16 - Multiple differences; taxable income given; two...Ch. 16 - Determine deferred tax assets and liabilities ...Ch. 16 - Prob. 16.10PCh. 16 - Prob. 16.11PCh. 16 - Prob. 16.12PCh. 16 - Prob. 16.13PCh. 16 - Prob. 16.1BYPCh. 16 - Prob. 16.2BYPCh. 16 - Integrating Case 163 Tax effects of accounting...Ch. 16 - Communication Case 164 Deferred taxes; changing...Ch. 16 - Prob. 16.5BYPCh. 16 - Research Case 166 Researching the way tax...Ch. 16 - Analysis Case 167 Reporting deferred taxes; Ford...Ch. 16 - Prob. 16.8BYPCh. 16 - Judgment Case 169 Analyzing the effect of deferred...Ch. 16 - Prob. 16.12BYPCh. 16 - Target Case LO16-1, LO16-2, LO16-4, LO16-8,...Ch. 16 - Prob. 1CCIFRS

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- d cion The table given below shows the absolute tax amounts under five different tax policies for respective income levels. Table 19.2 Annual Pretax Income Tax Policy Alpha O Gamma. Alpha. SO $0 $0 $0 $0 $10,000 $1,000 $1,000 $1,000 $1,000 $1,000 $50,000 $5,000 $6,000 $4,000 $1,000 $900 $100,000 $10,000 $15,000 $6,000 $1,000 $800 Beta. O Eta. Refer to Table 19.2. The tax structure which leads to maximum income inequality is: Delta. Tax Policy Beta Question 18 Tax Policy Gamma 27 Tax Policy Delta Tax Policy Eta $0 tv 9 N 4.nts. Narrow_forwardExercise 16-10 (Algo) Calculate income tax amounts under various circumstances; financial statement effects [LO16-2, 16-3] Four independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences: ($ in thousands) Taxable income Future deductible amounts Future taxable amounts. Balance(s) at beginning of the year: Deferred tax asset Deferred tax liability The enacted tax rate is 25%. Required: Situation 1 2 3 4 $ 112 $ 244 $ 252 $ 344 16 20 20 16 16 56 2 16 8 2 For each situation, determine the following: Note: Enter your answers in thousands rounded to one decimal place (i.e. 1,200 should be entered as 1.2). Negative amounts should be indicated by a minus sign. Leave no cell blank, enter "O" wherever applicable. a. Income tax payable currently. b. Deferred tax asset-ending balance. c. Deferred tax asset-change. d. Deferred tax liability-ending balance. e. Deferred tax liability change. f. Income tax…arrow_forwardChapter 3 Activity – Taxes Individual Income Tax Brackets (2021) Marginal Tax Rate Single, taxable income over: Joint, taxable income over: Head of Household, taxable income over: 10% $0 $0 $0 12% $9,950 $19,900 $14,200 22% $40,525 $81,050 $54,200 24% $86,375 $172,750 $86,350 32% $164,925 $329,850 $164,900 35% $209,425 $418,850 $209,400 37% $523,600 $628,300 $523,600 Standard Deduction Amounts (2021) Filing Status Deduction Amount Single $12,550 Married Filing Jointly $25,100 Head of Household $18,800 Long-term Capital Gains & Qualified Dividends (2021) Tax Rate Single Joint Head of Household 0% Under $40,000 Under $80,800 Under $54,100 15% $40,400 $80,800 $54,100 20% $445,850 $501,600 $473,750 Additional 3.8% Net Investment Income Tax for MAGI over $200,000 / $250,000 / $200,000 Calculate the federal income…arrow_forward

- 1. Ch03 Financial Planning Exercise 4 Chapter 3 Financial Planning Exercise 4 Effect of tax credit vs. tax exemption By defining after-tax income, demonstrate the differences resulting from a $1,500 tax credit versus a $1,500 tax deduction for a single taxpayer in the 25% tax bracket with $41,000 of pre- tax income. Round your answers to two decimal places. (Use Exhibit 3.3.) Deduction $ Credit $arrow_forwardUse the following tax table to determine how much income tax is paid on 915000 of taxable income. Total Paid = $ Rate 10% 15% 25% 28% 33% 35% 39.60% Taxable Income Bracket $0 to $9,325 $9,325 to $37,950 $37,950 to $91,900 $91,900 to $191,650 $191,650 to $416,700 $416,700 to $418,400 $418,400+ Single Taxable Income Tax Brackets and Rates, 2017arrow_forwardTestbank Multiple Choice Question 105 Swifty Corporation, which has a taxable payroll of $1300000, is subject to FUTA tax of 6.2% that includes a state contribution rate of 5.4%. However, because of stable employment experience, the company's state rate has been reduced to 2%. What is the total amount of federal and state unemployment tax for Swifty Corporation? O $ 106600 O $ 36400 O $150800 O $ 52000arrow_forward

- QUESTION 12 Range of taxable income $ 0 to $9,875 Marginal rate 10% 9,875 to 40,125 12 40,125 to 85,525 22 85,525 to 163,300 24 163,300 to 207,350 32 207,350 to 518,400 35 Calculate the total tax liability, after-tax earnings, and average tax rates if before-tax earnings are $25000, $82,000, and $120,000.arrow_forward1. What self-employment tax rate is applied to earnings that exceed $142,800 in a year and also do NOT exceed the additional Medicare tax threshold? Answer: A. 15.3% B. 12.4% C. 2.9% D. 1.45% 2. What is the standard credit applied to the FUTA tax rate in non-credit reduction states? Answer: A. 0.6% B. 0.9% C. 5.4% D. 6% 3. An employer in a non-credit reduction state would pay FUTA taxes of _____ for an employee whose year-to-date earnings prior to the current period are $7,200 and who earns $1,100 during the current period. Answer: A. $0 B. $6.60 C. $43.20 D. $49.80arrow_forwardUse the marginal tax rate chart to answer the question. Tax Bracket Marginal Tax Rate $0–$10,275 10% $10,276–$41,175 12% $41,176–$89,075 22% $89,076–$170,050 24% $170,051–$215,950 32% $215,951–$539,900 35% > $539,901 37% Determine the effective tax rate for a taxable income of $95,600. Round the final answer to the nearest hundredtharrow_forward

- QUESTION 15 What is valid? ○ Tax rate ties together the information you have defined for a Zone Definition and a Tax Class to trigger the different rate of a sales tax. Tax rate ties together buyer's shipping address and payment to trigger the different rate of a sales tax. Tax class defines the percentage of a product's retail price or shipping charges that should be collected as different rate. ○ A Tax Class allows one group for all product so that every product can be taxed the same ratearrow_forwardA e Y l 31% O 12:45 LTE abc SAVE Тext Pen Brush A company has a Deferred Tax Asset of $35,000. Now, the government has just changed the statutory tax rate from 35% to 30% effective immediately. What is the correct journal entry to record the impact of this tax rate change? Dr. Deferred Tax Assets 5000 Cr. Income Tax Payable 5000 Dr. Income Tax Payable 5000 Cr. Deferred Tax Assets 5000 Dr. Income Tax Expense 5000 Cr. Deferred Tax Assets 5000 Dr. Income Tax Expense 5000 Cr. Income Tax Payable 5000 Dr. Deferred Tax Assets 5000 Cr. Income Tax Expense 5000 В I U !!! !!!arrow_forwardProblem 03-09 (Static) [LO 3-3] Company N will receive $100,000 of taxable revenue from a client. Use Appendix A and Appendix B Required: a. Compute the NPV of the $100,000 assuming that Company N will receive $50,000 now (year 0) and $50,000 in year 1. The company's marginal tax rate is 30 percent, and it uses a 6 percent discount rate. b. Compute the NPV of the $100,000 assuming that Company N will receive $50,000 in year 1 and $50,000 in year 2. The company's marginal tax rate is 40 percent, and it uses a 4 percent discount rate. c. Compute the NPV of the $100,000 assuming that Company N will receive $20,000 now (year O) and $20,000 in years 1, 2, 3, and 4. The company's marginal tax rate is 10 percent, and it uses a 9 percent discount rate. Complete this question by entering your answers in the tabs below. Required A Required B Required C Compute the NPV of the $100,000 assuming that Company N will receive $50,000 now (year 0) and $50,000 in year 1. The company's marginal tax rate…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income Taxes

Accounting

ISBN:9780357109731

Author:Hoffman

Publisher:CENGAGE LEARNING - CONSIGNMENT

Operating Loss Carryback and Carryforward; Author: SuperfastCPA;https://www.youtube.com/watch?v=XiYhgzSGDAk;License: Standard Youtube License