INTERMEDIATE ACCOUNTING RMU 9TH EDITION

9th Edition

ISBN: 9781260998726

Author: SPICELAND

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 16, Problem 16.9E

Determine taxable income

• LO16–1, LO16–2

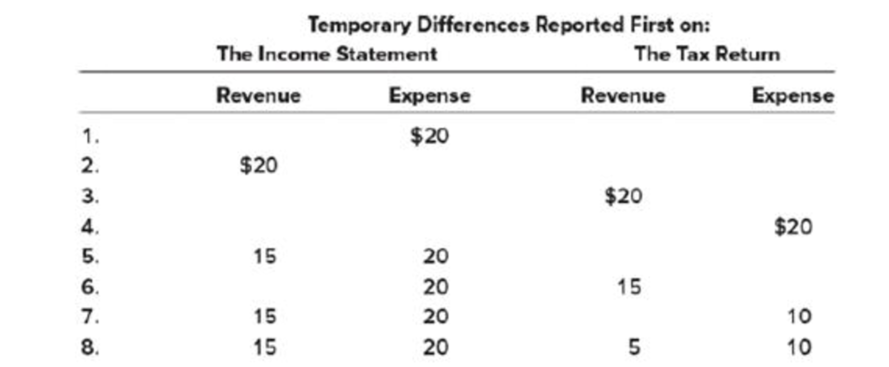

Eight independent situations are described below. Each involves future deductible amounts and/or future taxable amounts ($ in millions).

Required:

For each situation, determine taxable income, assuming pretax accounting income is $100 million.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Page 3 of 4

I. TAXABLE OR NON-TAXABLE INCOME

Put a CHECK MARK on the appropriate column.

If the benefit is taxable or has a taxable portion, indicate the taxable amount on the column provided.

If TAXABLE, how much is

the taxable amount FOR

THE YEAR?

BENEFIT

PURELY NON-

TAXABLE

TAXABLE

1. Laundry allowance amounting to P 4,500 a year

2. Uniform allowance amounting to P6,500 a year

3. Gifts given during Christmas amounting to

P8,000.

4. One sack of rice (50 kg) each month. The rice is

valued at P50.00 per kilo.

5. A one-time actual medical assistance amounting

to P 25,000.00 was received during the year.

IV. PROBLEM SOLVING

Solve the following problems.

Write your final answer on the space provided. Present your solution at the back page or attach a separate

sheet if necessary.

ANSWER

QUESTION

Leah sells gadgets. She is given 13% 0omm

1

How about if the question is How much is the income tax payable assuming the taxable year is 2021?

a. 330,000

b. 775,000

c. 800,000

d. 3,180,000

How much is the net taxable income using itemized deductions?

a. 1,070,000

b. 1,550,000

c. 1,550,000

d. 2,000,000

Chapter 16 Solutions

INTERMEDIATE ACCOUNTING RMU 9TH EDITION

Ch. 16 - Prob. 16.1QCh. 16 - A deferred tax liability (or asset) is described...Ch. 16 - Prob. 16.3QCh. 16 - Prob. 16.4QCh. 16 - Temporary differences result in future taxable or...Ch. 16 - Identify three examples of differences with no...Ch. 16 - The income tax rate for Hudson Refinery has been...Ch. 16 - Suppose a tax reform bill is enacted that causes...Ch. 16 - A net operating loss occurs when tax-deductible...Ch. 16 - Prob. 16.10Q

Ch. 16 - Additional disclosures are required pertaining to...Ch. 16 - Additional disclosures are required pertaining to...Ch. 16 - Prob. 16.13QCh. 16 - Prob. 16.14QCh. 16 - IFRS and U.S. GAAP follow similar approaches to...Ch. 16 - Temporary difference LO161 A company reports...Ch. 16 - Prob. 16.2BECh. 16 - Temporary difference LO162 A company reports...Ch. 16 - Prob. 16.4BECh. 16 - Temporary difference; income tax payable given ...Ch. 16 - Valuation allowance LO162, LO163 At the end of...Ch. 16 - Valuation allowance LO162, LO163 VeriFone Systems...Ch. 16 - Temporary and permanent differences; determine...Ch. 16 - Calculate taxable income LO161, LO164 Shannon...Ch. 16 - Multiple tax rates LO165 J-Matt, Inc., had pretax...Ch. 16 - Change in tax rate LO165 Superior Developers...Ch. 16 - Net operating loss carryforward LO167 During its...Ch. 16 - Net operating loss carryback LO167 AirParts...Ch. 16 - Tax uncertainty LO169 First Bank has some...Ch. 16 - Intraperiod tax allocation LO1610 Southeast...Ch. 16 - Temporary difference; taxable income given LO161...Ch. 16 - Prob. 16.2ECh. 16 - Prob. 16.3ECh. 16 - Prob. 16.4ECh. 16 - Prob. 16.5ECh. 16 - Prob. 16.6ECh. 16 - Identify future taxable amounts and future...Ch. 16 - Calculate income tax amounts under various...Ch. 16 - Determine taxable income LO161, LO162 Eight...Ch. 16 - Prob. 16.10ECh. 16 - Deferred tax asset; income tax payable given;...Ch. 16 - Prob. 16.12ECh. 16 - Prob. 16.13ECh. 16 - Multiple differences LO164, LO166 For the year...Ch. 16 - Multiple t ax rates LO162, LO165 Allmond...Ch. 16 - Prob. 16.16ECh. 16 - Deferred taxes; change in tax rates LO161, LO165...Ch. 16 - Multiple temporary differences; record income...Ch. 16 - Multiple temporary differences; record income...Ch. 16 - Net operating loss carryforward LO167 During...Ch. 16 - Net operating loss carryback LO167 Wynn Sheet...Ch. 16 - Net operating loss carryback and carryforward ...Ch. 16 - Identifying income tax deferrals LO161, LO162,...Ch. 16 - Multiple temporary differences; balance sheet...Ch. 16 - Multiple tax rates LO161, LO164, LO165 Case...Ch. 16 - Prob. 16.26ECh. 16 - Balance sheet classification LO168 As of December...Ch. 16 - Concepts; terminology LO161 through LO168 Listed...Ch. 16 - Tax credit; uncertainty regarding sustainability ...Ch. 16 - Intraperiod tax allocation LO1610 The following...Ch. 16 - FASB codification research LO165, LO168, LO1610...Ch. 16 - Prob. 16.1PCh. 16 - Prob. 16.2PCh. 16 - Prob. 16.3PCh. 16 - Prob. 16.4PCh. 16 - Change in tax rate; record taxes for four years ...Ch. 16 - Multiple differences; temporary difference yet to...Ch. 16 - Multiple differences; calculate taxable income;...Ch. 16 - Multiple differences; taxable income given; two...Ch. 16 - Determine deferred tax assets and liabilities ...Ch. 16 - Prob. 16.10PCh. 16 - Prob. 16.11PCh. 16 - Prob. 16.12PCh. 16 - Prob. 16.13PCh. 16 - Prob. 16.1BYPCh. 16 - Prob. 16.2BYPCh. 16 - Integrating Case 163 Tax effects of accounting...Ch. 16 - Communication Case 164 Deferred taxes; changing...Ch. 16 - Prob. 16.5BYPCh. 16 - Research Case 166 Researching the way tax...Ch. 16 - Analysis Case 167 Reporting deferred taxes; Ford...Ch. 16 - Prob. 16.8BYPCh. 16 - Judgment Case 169 Analyzing the effect of deferred...Ch. 16 - Prob. 16.12BYPCh. 16 - Target Case LO16-1, LO16-2, LO16-4, LO16-8,...Ch. 16 - Prob. 1CCIFRS

Additional Business Textbook Solutions

Find more solutions based on key concepts

Discussion Analysis A13-41 Discussion Questions 1. How do managers use the statement of cash flows? 2. Describ...

Managerial Accounting (5th Edition)

The amount that should be recorded by Company R for building under historical cost principle.

Financial Accounting (11th Edition)

This year, Prewer Inc. received a 160,000 dividend on its investment consisting of 16 percent of the outstandin...

Principles Of Taxation For Business And Investment Planning 2020 Edition

1. For Frank’s Funky Sounds, straight-line depreciation on the trucks is a

Learning Objective 1

a. variable cos...

Horngren's Accounting (12th Edition)

List five asset accounts, three liability accounts, and five expense accounts included in the acquisition and p...

Auditing And Assurance Services

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- LO.2 Oak Corporation has the following general business credit carryovers. If the general business credit generated by activities during 2019 equals 36,000 and the total credit allowed during the current year is 60,000 (based on tax liability), what amounts of the current general business credit and carryovers are utilized against the 2019 income tax liability? What is the amount of unused credit carried forward to 2020?arrow_forwardRequired information [The following information applies to the questions displayed below.] Arndt, Inc. reported the following for 2021 and 2022 ($ in millions): 2021 2022 $ 940 $1,032 852 Revenues Expenses Pretax accounting income (income statement) Taxable income (tax return) 796 $ 144 $ 104 180 %24 214 Tax rate: 25% a. Expenses each year include $58 million from a two-year casualty insurance policy purchased in 2021 for $116 million. The cost is tax deductible in 2021. b. Expenses include $2 million insurance premiums each year for life insurance on key executives. c. Arndt sells one-year subscriptions to a weekly journal. Subscription sales collected and taxable in 2021 and 2022 were $59 million and $75 million, respectively. Subscriptions included in 2021 and 2022 financial reporting revenues were $53 million ($38 million collected in 2020 but not recognized as revenue until 2021) and $59 million, respectively. Hint. View this as two temporary differences-one reversing in 2021; one…arrow_forwardQuestion 8 of 15. A taxpayer is no longer eligible to claim the EIC if they have more than $3,250 $5,000 $10,000 $10,300 Mark for follow up of investment income in 2022. 4arrow_forward

- What is the taxable income for the year 2020? A. P25,000 B. P75,000 C. P280,620 D. P300,000arrow_forwardIn 2022, Lisa and Fred, a married couple, had taxable income of $313,200. If they were to file separate tax returns, Lisa would have reported taxable income of $131,600 and Fred would have reported taxable income of $181,600. Use Tax Rate Schedule for reference. What is the couple's marriage penalty or benefit? Note: Do not round intermediate calculations. Marriage beneftarrow_forwardMultiple Choice 2-34 Social Security Benefits (LO 2.16) For 2021, the maximum percentage of Social Security benefits that could be included in a taxpayer's gross income is: a.25% b.75% c.0% d.50% e.85%arrow_forward

- K Use the table to the right to calculate the federal income tax due for a taxable income of $158,000. The income tax due is $. (Type an integer or a decimal.) If your taxable income is Over- But not Over- $0 $9,275 $9,275 $37,650 $37,650 $91,150 $91,150 $190,150 $413,350 $190,150 $413,350 ******* The tax is Of the amount Over- 10% $927.50 +15% $5,183.75 +25% ********* $18,558.75+28% $46,278.75+33% $119,934.75+ 35% $0 $9,275 $37,650 $91,150 $190,150 $413,350 1 ofarrow_forward2023 TAXABLE INCOME FIRST $53,359 OVER $53,359 TO $106,717 OVER $106,717 TO $165,430 OVER $ $165,430 TO $237,675 OVER $235,675 FILL IN THE BLANK TAX RATE 15.00% 20.50% 26.00% 29.32% 33.00% C) The total income tax burden if your salary is $85,000. type your text here Based on the Canadian Federal Income Tax Brackets for 2023 shown above, calculate and input the numeric answers to the questions below. Round off your answers to the nearest dollar. Do not use $, decimals or comma. For example, instead of $23,486.52, write 23487. For answers requiring a tax rate, enter only the numeric value with two decimal places, with "%" symbol. For example, 20.50%).arrow_forwardQuestion 11: The taxable earnings threshold over which FUTA tax is not levied is: Answer: A. O S7,000 В. O $142,800 С. S200,000 D. S250,000arrow_forward

- Exercise 16-10 (Algo) Calculate income tax amounts under various circumstances; financial statement effects [LO16-2, 16-3] Four independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences: ($ in thousands) Taxable income Future deductible amounts Future taxable amounts. Balance(s) at beginning of the year: Deferred tax asset Deferred tax liability The enacted tax rate is 25%. Required: Situation 1 2 3 4 $ 112 $ 244 $ 252 $ 344 16 20 20 16 16 56 2 16 8 2 For each situation, determine the following: Note: Enter your answers in thousands rounded to one decimal place (i.e. 1,200 should be entered as 1.2). Negative amounts should be indicated by a minus sign. Leave no cell blank, enter "O" wherever applicable. a. Income tax payable currently. b. Deferred tax asset-ending balance. c. Deferred tax asset-change. d. Deferred tax liability-ending balance. e. Deferred tax liability change. f. Income tax…arrow_forwardQuestion 14: The original Social Security tax rate was of taxable earnings. Answer: A. 10% O 1% С. 5% D. 7% B.arrow_forwardHomework i Firm E must choose between two alternative transactions. Transaction 1 requires a $13,250 cash outlay that would be nondeductible in the computation of taxable income. Transaction 2 requires a $18,700 cash outlay that would be a deductible expense. Required: a. Determine the after-tax cost for each transaction. Assume Firm E's marginal tax rate is 25 percent. b. Determine the after-tax cost for each transaction. Assume Firm E's marginal tax rate is 45 percent. Complete this question by entering your answers in the tabs below. Required A Required B After-tax cost Determine the after-tax cost for each transaction. Assume Firm E's marginal tax rate is 25 percent. Note: Negative amounts should be indicated by a minus sign. @ Transaction 1 20 #C Transaction 2 % Saved & 7 2 * O Harrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income Taxes

Accounting

ISBN:9780357109731

Author:Hoffman

Publisher:CENGAGE LEARNING - CONSIGNMENT

Chapter 19 Accounting for Income Taxes Part 1; Author: Vicki Stewart;https://www.youtube.com/watch?v=FMjwcdZhLoE;License: Standard Youtube License