Concept explainers

Videos

Calculate income tax amounts under various circumstances

• LO16–1, LO16–2

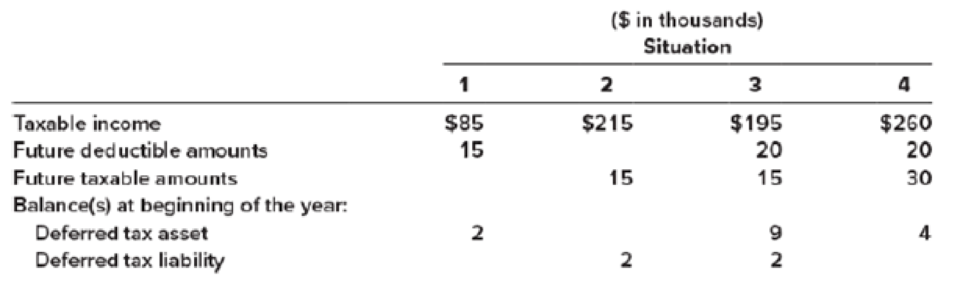

Four independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences:

The enacted tax rate is 40%.

Required:

For each situation, determine the:

a. Income tax payable currently

b.

c. Deferred tax asset—change (dr) cr

d.

e. Deferred tax liability—change (dr) cr

f. Income tax expense

Want to see the full answer?

Check out a sample textbook solution

Chapter 16 Solutions

INTERMEDIATE ACCOUNTING RMU 9TH EDITION

Additional Business Textbook Solutions

Managerial Accounting (4th Edition)

Advanced Financial Accounting

Principles of Accounting Volume 2

Cost Accounting (15th Edition)

Accounting for Governmental & Nonprofit Entities

Financial Accounting, Student Value Edition (4th Edition)

- 39 Two independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences: SITUATION Taxable income Amounts at year-end: Future deductible amounts Future taxable amounts Balances at beginning of year, debit (credit): Deferred tax asset Deferred tax liability The enacted tax rate is 40% for both situations. Required: For each situation determine the following: (a) Income tax payable currently. (b) Deferred tax asset - balance at year-end. (c) Deferred tax asset change debit or (credit) for the year. (d) Deferred tax liability - balance at year-end. (e) Deferred tax liability change debit or (credit) for the year. (f) Income tax expense for the year. 1 2 $ 39,000 $ 79,000 4,900 0 11,100 4,900 $ 1,000 0 $ 4,440 1,000 SITUATION 2arrow_forwardQuestion 20: Identify the incorrect statement regarding EFTPS. Answer: А. O It's a free, online service for remitting federal tax payments. В. O Payments can be made via phone, Internet, or wire transfer. С. When using the EFTPS, payments are due by 11:59 p.m. on the tax due date. D. O Requirements for use include enrollment and setting up a unique PIN.arrow_forwardProblem 16-145 Four independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences reported first on: Income Statement Tax Return Revenue Expense Revenue Expense $21,000 (1.) (2.) (3.) (4.) $21,000 $15, 200 $21,000 $15, 200 $21, 000 $10, 200 Required: For each situation, determine the taxable income assuming pretax accounting income is $100,000. (Amounts to be deducted should be indicated by a minus sign.) 1 2 3 4 Accounting income Temporary differences: Income statement first: Revenue Expense Tax return first: Revenue Expense Taxable incomearrow_forward

- Question 11: Which statement regarding the calculation of taxes is accurate? Answer: A. O For simplicity, taxable income for local, state, and federal income tax withholdings has been standardized. В. O All taxes are calculated based on net pay. С. O Because retirement plans are exempt from federal income tax, you add the contributed amount before calculating the employee's federal withholding. D. O Taxes may be calculated based on an amount lower than gross pay, and not all taxes are calculated based on the same amount. Question 12: Which of these is a credit reduction state/territory? Question 15: Union dues are considered a deduction. Answer: Answer: A. O Connecticut A. O cafeteria В. O Ohio В. O insurance C. O Virginia O mandatory С. D. O U.S. Virgin Islands D. O voluntary Question 14: Alejandra owns and operates an appliance store where employees clock in and out for each shift. Per the FLSA, Alejandra rounds employee time worked to the nearest 15-minute increment. On Tuesday this…arrow_forwardNalad Corp. provided the following data related to accounting and taxable income: 20X8 20X9 Pre-tax accounting income (financial statements) Taxable income (tax return) $510,000 295,000 40% $495,000 710,000 40% Income tax rate There are no existing temporary differences other than those reflected in these data. There are no permanent differences. Required: 1-a. How much tax expense would be reported in each year if the taxes payable method was used? Tax Expense 20X8 20X9 1-b. What is the implied tax rate? (Round your answers to 1 decimal place.) 20X8 20X9 Implied tax ratearrow_forwardExercise 3-23 (Algorithmic) (LO. 6) Compute the 2022 tax liability and the marginal and average tax rates for the following taxpayers. Click here to access the 2022 tax rate schedule. If required, round the tax liability to the nearest dollar. When required, round the average rates to four decimal places before converting to a percentage (i.e., .67073 would be rounded to .6707 and entered as 67.07%). a. Chandler, who files as a single taxpayer, has taxable income of $101,200. Tax liability: Marginal rate: Average rate: % % b. Lazare, who files as a head of household, has taxable income of $58,200. Tax liability: Marginal rate: Average rate: % %arrow_forward

- Question 11: Which statement regarding the calculation of taxes is accurate? Answer: A. O For simplicity, taxable income for local, state, and federal income tax withholdings has been standardized. B. O All taxes are calculated based on net pay. C. O Because retirement plans are exempt from federal income tax, you add the contributed amount before calculating the employee's federal withholding. D. O Taxes may be calculated based on an amount lower than gross pay, and not all taxes are calculated based on the same amount. Question 12: Which of these is a credit reduction state/territory? Question 15: Union dues are considered a deduction. Answer: Answer: A. A. O Connecticut O cafeteria B. O Ohio B. O insurance C. O Virginia C. O mandatory D. O U.S. Virgin Islands D. O voluntary Question 14: Alejandra owns and operates an appliance store where employees clock in and out for each shift. Per the FLSA, Alejandra rounds employee time worked to the nearest 15-minute increment. On Tuesday this…arrow_forwardSave & Exit Subm Two independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences: SITUATION Taxable income Amounts at year-end: Future deductible amounts 2. $46,000 $86,000 5,600 10,600 0 5,600 Future taxable amounts Balances at beginning of year, dr (cr): Deferred tax asset, Deferred tax liability $ 1,000 $ 3,180 0 1,000 The enacted tax rate is 30% for both situations. Required: For each situation determine the: SITUATION 2. (a.) Income tax payable currently. (b.) Deferred tax asset - balance at year-end. (c.) Deferred tax asset change dr or (cr) for the year. (d.) Deferred tax liability - balance at year-end. (e.) Deferred tax liability change dr or (cr) for the year. (f.) Income tax expense for the year. Next > 31 of 39arrow_forwardWhat amount of current income tax liability should be reported at year end? a. ₱ 1,780,000 b. ₱ 2,280,000 c. ₱ 2,880,000 d. ₱ 2,580,000arrow_forwardK A tax rate schedule is given in the table. If x equals taxable income and y equals the tax due, construct a function y = f(x) for the tax schedule. f(x) = 0.11x +(x-D ☐+(×-D) If taxable income is over But not over 0 8,000 30,700 74,300 74,300 The tax is this amount 0.00 + 8,000 30,700 880.00 + 4,512.00 + 14,976.00 + if 0 74,300 Plus this % 11% 16% 24% 31% Of the excess over 0 8,000 30,700 74,300arrow_forwardP18-1 Definitions The FASB has defined several terms in regard to accounting for income taxes. Below are various code letters (for terms) followed by definitions. Code Letter Term A Future deductible amount B Income tax payable (or refund) C Effective tax rate D Valuation allowance E Deferred tax asset F Operating loss carryforward G Taxable income H Deferred tax consequences I Future taxable amount J Deferred tax liability K Temporary difference L Income tax expense (or benefit) M Deferred tax expense (or benefit) _________1. The deferred tax consequences of future deductible amounts and operating loss carryforwards _________2. A difference between the tax basis of an asset or liability and its reported amount in the financial statements that will result in taxable or deductible amounts in future years when the reported…arrow_forward1. What self-employment tax rate is applied to earnings that exceed $142,800 in a year and also do NOT exceed the additional Medicare tax threshold? Answer: A. 15.3% B. 12.4% C. 2.9% D. 1.45% 2. What is the standard credit applied to the FUTA tax rate in non-credit reduction states? Answer: A. 0.6% B. 0.9% C. 5.4% D. 6% 3. An employer in a non-credit reduction state would pay FUTA taxes of _____ for an employee whose year-to-date earnings prior to the current period are $7,200 and who earns $1,100 during the current period. Answer: A. $0 B. $6.60 C. $43.20 D. $49.80arrow_forwardarrow_back_iosSEE MORE QUESTIONSarrow_forward_ios

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning