Videos

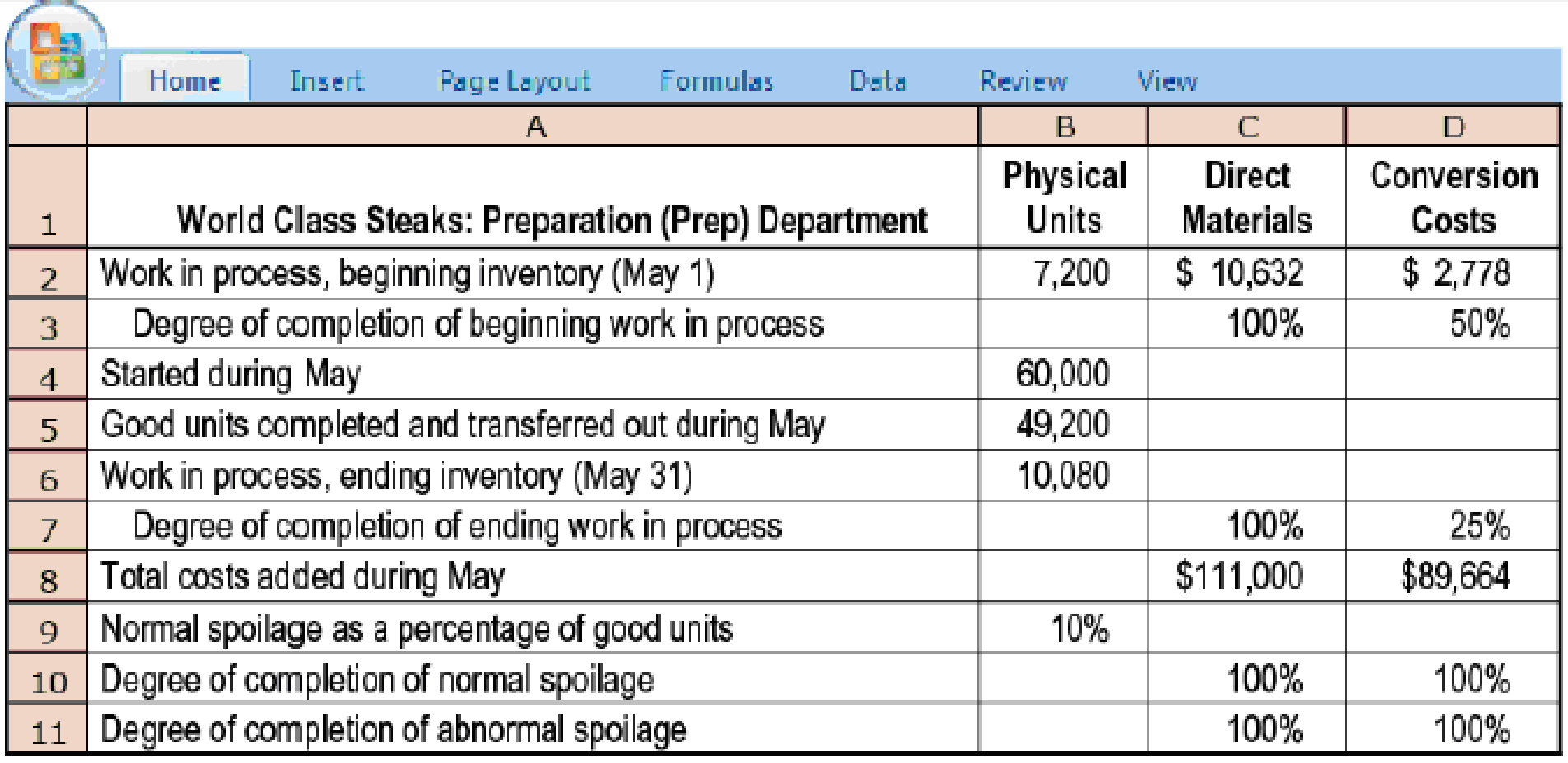

Weighted-average method, spoilage. World Class Steaks is a meat-processing firm based in Texas. It operates under the weighted-average method of

Required

For the prep department, summarize the total costs to account for and assign those costs to units completed and transferred out (including normal spoilage), to abnormal spoilage, and to units in ending work in process. (Problem 18-37 explores additional facets of this problem.)

Learn your wayIncludes step-by-step video

Chapter 18 Solutions

COST ACCOUNTING

Additional Business Textbook Solutions

Construction Accounting And Financial Management (4th Edition)

Horngren's Accounting (11th Edition)

Horngren's Financial & Managerial Accounting, The Financial Chapters (6th Edition)

Managerial Accounting (4th Edition)

Financial Accounting, Student Value Edition (4th Edition)

Horngren's Accounting (12th Edition)

- Benson Pharmaceuticals uses a process-costing system to compute the unit costs of the over-the-counter cold remedies that it produces. It has three departments: mixing, encapsulating, and bottling. In mixing, the ingredients for the cold capsules are measured, sifted, and blended (with materials assumed to be uniformly added throughout the process). The mix is transferred out in gallon containers. The encapsulating department takes the powdered mix and places it in capsules (which are necessarily added at the beginning of the process). One gallon of powdered mix converts into 1,500 capsules. After the capsules are filled and polished, they are transferred to bottling, where they are placed in bottles that are then affixed with a safety seal, lid, and label. Each bottle receives 50 capsules. During March, the following results are available for the first two departments: Overhead in both departments is applied as a percentage of direct labor costs. In the mixing department, overhead is 200% of direct labor. In the encapsulating department, the overhead rate is 150% of direct labor. Required: 1. Prepare a production report for the mixing department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to two decimal places for the unit cost.) 2. Prepare a production report for the encapsulating department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to four decimal places for the unit cost.) 3. CONCEPTUAL CONNECTION Explain why the weighted average method is easier to use than FIFO. Explain when weighted average will give about the same results as FIFO.arrow_forwardHusky Ltd. manufactures toys using a continuous production process that flows through two departments: Forming and Finishing. In the forming department, various components are built and are transferred to the finishing department. In the finishing department, those components are assembled into Husky’s final product and once finished, are transferred to Husky’s Finished Goods Inventory. Any spoilage is detected at the end of the process (i.e. when the toys are 100% complete). Husky uses the FIFO method of accounting for costs. In the Finishing Department, Direct materials are added at 70% of conversion and conversion costs are added evenly throughout the process. Finishing DepartmentPhysical UnitsTransferred InDirect Materials Conversion Work in Process January 1 37,000 $ 76,400 $ 0 $ 30,062Degree of Completion in beginning WIP 65%Units Transferred in from Forming in January 232,500Good Units Transferred Out 240,000Work In Process January 31 24,000Normal Spoilage as a percentage of…arrow_forwardCassa Corporation uses process costing. In Department 2, conversion costs are incurred uniformly throughout the process. Materials are added at the end of the process, following inspection. Normal spoilage is expected to be 5% of good output. Information pertaining to Department 2 include: Units received from Department 1 is 12,000 at a cost of P84,000. Units transferred to finished goods is 9,000 and there are 2,000 units in the ending inventory which are 70% complete. Costs incurred in this department include: Materials - P18,000 with Labor and overhead at P45,600. How much is the cost of goods manufactured in Department 2?arrow_forward

- XYZ is a manufacturer of furniture. It operates a weighted-average costing system and has two departments, cutting and assembly. The cutting department manufactures the furniture components and transfers them to the assembly department. In the assembly department, conversion costs are incurred evenly during the process, and direct materials are added when the assembly process is 80% completed. Spoiled units are detected when the conversion process is 70% completed. On average, XYZ expects spoiled units to be 5% of the good units that survived the inspection in the assembly department. The spoiled units are sold to a local shop for $8 per unit. The proceeds from the sale of spoiled units are credited to the cost of completed goods. In the month of January, 100 units were spoiled and sold to the local shop. Other data for the month of January,2021 are provided below: ASSEMBLY DEPARTMENT DATA FOR THE MONTH OF JANUARY, 2021 WIP, beginning inventory…arrow_forwardJoseph Company uses a standard process costing system in accounting for its one product, which is produced in one department. Inspection takes place at the end of the process, and any spoiled units revealed by inspection are considered abnormal and complete as to all cost elements. All materials are added at the beginning of the process while conversion costs are incurred uniformly throughout the process. Standard costs are as follows: Materials: 6 square meters @ P0.33 Direct labor: ½ hour @ P5.25 Variable factory overhead: ½ hour @ P1.00 Fixed factory overhead: ½ hour @ P1.50 Normal capacity is 17,500 direct labor hours per month. Actual data for November: a. Beginning work in process inventory – 5,000 units (40% converted) b. Started in process during the month – 30,000 units c. Spoiled during November – 1,000 units d. Ending work in process inventory – 2,000 units (80% converted) e. Actual costs incurred: Materials purchased 200,000 square meters @ P0.32 Materials used…arrow_forwardHealthway uses a process-costing system to compute the unit costs of the minerals that it produces. It has three departments: Mixing, Tableting, and Bottling. In Mixing, at the beginning of the process all materials are added and the ingredients for the minerals are measured, sifted, and blended together. The mix is transferred out in gallon containers. The Tableting Department takes the powdered mix and places it in capsules. One gallon of powdered mix converts to 1,600 capsules. After the capsules are filled and polished, they are transferred to Bottling where they are placed in bottles, which are then affixed with a safety seal and a lid and labeled. Each bottle receives 50 capsules. During July, the following results are available for the first two departments (direct materials are added at the beginning in both departments): Overhead in both departments is applied as a percentage of direct labor costs. In the Mixing Department, overhead is 200 percent of direct labor. In the Tableting Department, the overhead rate is 150 percent of direct labor. Required: 1. Prepare a production report for the Mixing Department using the weighted average method. Follow the five steps outlined in the chapter. Round unit cost to three decimal places. 2. Prepare a production report for the Tableting Department. Materials are added at the beginning of the process. Follow the five steps outlined in the chapter. Round unit cost to four decimal places.arrow_forward

- The Converting Department of Tender Soft Tissue Company uses the weighted average method and had 1,900 units in work in process that were 60% complete at the beginning of the period. During the period, 15,800 units were completed and transferred to the Packing Department. There were 1,200 units in process that were 30% complete at the end of the period. a. Determine the number of whole units to be accounted for and to be assigned costs for the period. b. Determine the number of equivalent units of production for the period. Assume that direct materials are placed in process during production.arrow_forwardFor E2-17, prepare any journal entries that would have been different if the only trigger points had been the purchase of materials and the sale of finished goods. Davis Co. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 70,000. b. Requisitioned raw materials to production, 70,000. c. Distributed direct labor costs, 15,000. d. Factory overhead costs incurred, 45,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 195,000, on account. (Hint: Use a single account for raw materials and work in process.)arrow_forwardK-Briggs Company uses the FIFO method to account for the costs of production. For Crushing, the first processing department, the following equivalent units schedule has been prepared: The cost per equivalent unit for the period was as follows: The cost of beginning work in process was direct materials, 40,000; conversion costs, 30,000. Required: 1. Determine the cost of ending work in process and the cost of goods transferred out. 2. Prepare a physical flow schedule.arrow_forward

- Kenkel, Ltd. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 80,000. b. Requisitioned raw materials to production, 80,000. c. Distributed direct labor costs, 10,000. d. Factory overhead costs incurred, 60,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 225,000, on account.arrow_forwardPinter Company had the following environmental activities and product information: 1. Environmental activity costs 2. Driver data 3. Other production data Required: 1. Calculate the activity rates that will be used to assign environmental costs to products. 2. Determine the unit environmental and unit costs of each product using ABC. 3. What if the design costs increased to 360,000 and the cost of toxic waste decreased to 750,000? Assume that Solvent Y uses 6,000 out of 12,000 design hours. Also assume that waste is cut by 50 percent and that Solvent Y is responsible for 14,250 of 15,000 pounds of toxic waste. What is the new environmental cost for Solvent Y?arrow_forwardWeighted Average Method, Nonuniform Inputs, MultipleDepartmentsBenson Pharmaceuticals uses a process-costing system to compute the unit costs of the overthe-counter cold remedies that it produces. It has three departments: mixing, encapsulating,and bottling. In mixing, the ingredients for the cold capsules are measured, sifted, and blended(with materials assumed to be uniformly added throughout the process). The mix is transferredout in gallon containers. The encapsulating department takes the powdered mix and places it incapsules (which are necessarily added at the beginning of the process). One gallon of powderedmix converts into 1,500 capsules. After the capsules are filled and polished, they are transferredto bottling, where they are placed in bottles that are then affixed with a safety seal, lid, and label.Each bottle receives 50 capsules.During March, the following results are available for the first two departments: Overhead in both departments is applied as a percentage of…arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning