Concept explainers

Videos

Applying Job Order Costing in a Service Setting

Marsha Design is an interior design and consulting firm. The uses a

Marsha Design races direct labor and travel costs to each job (client). It assigns indirect costs to clients at a predetermined overhead rate based on direct labor hours.

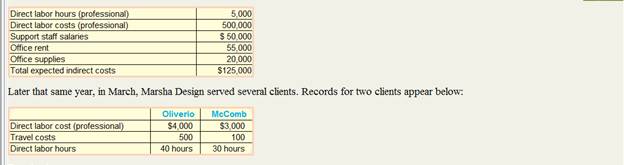

At the beginning of the year, the managing partner, Marsha Cain, prepared the following budget:

Later that same year, in March, Marsha several Records two clients appear below:

1. Compute Marsha Design's predetermined overhead rate current year.

2. Compute the total cost of serving the listed.

3. Assume that Marsha charges clients $250 per hour for interior design services. How much gross profit would she earn on each of the clients above, ignoring any difference between actual and overhead?

Want to see the full answer?

Check out a sample textbook solution

Chapter 2 Solutions

Managerial Accounting - With Access

- Brady Furniture Company manufactures wooden oak furniture. The company employs a job cost system to trace manufacturing costs to jobs. Each job represents a batch of furniture of the same type. Information regarding direct materials on selected jobs throughout the year is as follows: Dining tables are the most difficult furniture item in Bradys catalog to manufacture. Thus, the most skilled employees are scheduled to make dining tables, unless they are required for other jobs. a. Determine the material cost per unit for each job. b. Use the January material cost per unit for each type of furniture as the base material cost. For each month and each type of furniture, determine the unit material cost as a percent of the base unit material cost. Round percent to one decimal place. Use the following table format: c. Develop a line chart of the percent of unit material cost to the base unit material cost. Place the months on the horizontal axis and use three lines for the three different types of furniture. d. Interpret the chart. What is happening to the dining tables?arrow_forwardAntolini Enterprises produces mens sports coats that are sold by popular department stores. Each retail order is treated as a job that accumulates materials, labor, and overhead costs for a batch of sports coats. Management has obtained data on the labor costs for four selected jobs over a six-month period. Each selected job represents a similar style and size of sports coat. The data are as follows: a. Determine the direct labor cost per unit for each job. b. Interpret the trend in per-unit labor cost. c. Determine the direct labor hours per sports coat. d. Interpret what may be happening with Job 192.arrow_forwardCynthia Rogers, the cost accountant for Sanford Manufacturing, is preparing a management report that must include an allocation of overhead. The budgeted overhead for each department and the data for one job are as follows: Using the departmental overhead application rates, and allocating overhead on the basis of direct labor hours, overhead applied to Job 231 in the Tooling Department would be: a. 44.00. b. 197.50. c. 241.50. d. 501.00.arrow_forward

- Gerken Fabrication Inc. uses the job order cost system of accounting. The following information was taken from the companys books after all posting had been completed at the end of March: a. Compute the total production cost of each job. b. Prepare the journal entries to charge the costs of materials, labor, and factory overhead to Work in Process. c. Prepare the journal entry to transfer the cost of jobs completed to Finished Goods. d. Compute the unit cost of each job. e. Compute the selling price per unit for each job, assuming a mark-on percentage of 50%.arrow_forwardJob order cost sheets show the following costs assigned to each job: The company assigns overhead at twice the direct labor cost. What is the total cost for each job?arrow_forwardDetermining job costcalculation of predetermined rate for applying overhead by direct labor cost and direct labor hour methods Beemer Products Inc. has its factory divided into three departments, with individual factory overhead rates for each department. In each department, all the operations are sufficiently alike for the department to be regarded as a cost center. The estimated monthly factory overhead for the departments is as follows: Forming, 64,000; Shaping, 36,000; and Finishing, 10,080. The estimated production data include the following: The job cost ledger shows the following data for X6, which was completed during the month: Required: Determine the cost of X6. Assume that the factory overhead is applied to production orders, based on the following: 1. Direct labor cost 2. Direct labor hours (Hint: You must first determine overhead rates for each department, rounding rates to the nearest cent.)arrow_forward

- The following describes the job responsibilities of two employees of Barney Manufacturing. Joan Dennison, Cost Accounting Manager. Joan is responsible for measuring and collecting costs associated with the manufacture of the garden hose product line. She is also responsible for preparing periodic reports that compare the actual costs with planned costs. These reports are provided to the production line managers and the plant manager. Joan helps to explain and interpret the reports. Steven Swasey, Production Manager. Steven is responsible for the manufacture of the high-quality garden hose. He supervises the line workers, helps to develop the production schedule, and is responsible for seeing that production quotas are met. He is also held accountable for controlling manufacturing costs. Required: CONCEPTUAL CONNECTION Identify Joan and Steven as line or staff and explain your reasons.arrow_forwardNutts management is very concerned about the cost of overhead on its jobs. When jobs are complete, overhead costs should be between 15% and 20% of total costs. For example, the labor cost on Job 8958 is 25% of total costs, higher than the norm. Open Job 8961 and click the Chart sheet tab. A pie chart appears showing the cost components on that job. Record the labor cost percentage in the space provided. Repeat this for each of the jobs worked on in August. Did Nutt maintain good cost control on all its jobs? Explain. Worksheet. During September, Job 8963 required two additional material requisitions to complete the job. Open JOB8963 and modify the job cost sheet to include an area for four direct material requisition entries instead of three. Then enter the following two materials requisitions onto the worksheet: Preview the printout to make sure it will print neatly on one page, and then print the worksheet. Save the completed worksheet as JOBT. Chart. Open JOB8964 and click the Chart sheet tab. Prepare a bar chart for JOB8964 showing the amount of material, labor, and overhead required to complete the job. Use the Chart Data Table found in rows 4246 as a basis for preparing the chart. Enter your name somewhere on the chart. Save the file again as J0B8964. Print the chart.arrow_forwardSultan, Inc. manufactures goods to special order and uses a job order cost system. During its first month of operations, the following selected transactions took place: Required: 1. Prepare a schedule reflecting the cost of each of the four jobs. 2. Prepare journal entries to record the transactions. 3. Compute the ending balance in Work in Process. 4. Compute the ending balance in Finished Goods.arrow_forward

- JOB ORDER COSTING WITH UNDER- AND OVERAPPLIED FACTORY OVERHEAD M Evans Sons manufactures parts for radios. For each job order, it maintains ledger sheets on which it records direct labor, direct materials, and factory overhead applied. The factory overhead control account contains postings of actual overhead costs. At the end of the month, the under- or overapplied factory overhead is charged to the cost of goods sold account. Factory overhead is applied on the basis of direct labor hours. For Job Nos. 101, 102, 103, and 104, direct labor hours are 12,000, 10,000, 11,000, and 18,000, respectively. The overhead application rate is 1.20/direct labor hour (a) Purchased raw materials on account, 50,000. (b) Issued direct materials: (c) Issued indirect materials to production, 8,000. (d) Incurred direct labor costs: (e) Charged indirect labor to production, 15,000. (f) Paid electricity bill, taxes, and repair fees for the factory and charged to production, 8,000. (g) Depreciation expense on factory equipment, 30,000. (h) Applied factory overhead to Job Nos. 101-104 using the predetermined factory overhead rare (see above). (i) Finished Job Nos. 101-103 and transferred to the finished goods inventory account as products N, O, and P. (j) Sold products N and O for 50,000 and 45,400, respectively. (k) Transferred under- or overapplied factory overhead balance to the cost of goods sold account. REQUIRED 1. Prepare general journal entries to record transactions (a) through (k). Make compound entries for (b), (d), and (h), with separate debits for each job. 2. Post the entries to the work in process and finished goods T accounts only and determine the ending balances in these accounts. 3. Compute the balance in the job cost ledger and verify that this balance agrees with that in the work in process control account.arrow_forwardOverhead Assignment: Actual and Normal Activity Compared Reynolds Printing Company specializes in wedding announcements. Reynolds uses an actual job-order costing system. An actual overhead rate is calculated at the end of each month using actual direct labor hours and overhead for the month. Once the actual cost of a job is determined, the customer is billed at actual cost plus 50%. During April, Mrs. Lucky, a good friend of owner Jane Reynolds, ordered three sets of wedding announcements to be delivered May 10, June 10, and July 10, respectively. Reynolds scheduled production for each order on May 7, June 7, and July 7, respectively. The orders were assigned job numbers 115, 116, and 117, respectively. Reynolds assured Mrs. Lucky that she would attend each of her daughters weddings. Out of sympathy and friendship, she also offered a lower price. Instead of cost plus 50%, she gave her a special price of cost plus 25%. Additionally, she agreed to wait until the final wedding to bill for the three jobs. On August 15, Reynolds asked her accountant to bring her the completed job-order cost sheets for Jobs 115, 116, and 117. She also gave instructions to lower the price as had been agreed upon. The cost sheets revealed the following information: Reynolds could not understand why the overhead costs assigned to Jobs 116 and 117 were so much higher than those for Job 115. She asked for an overhead cost summary sheet for the months of May, June, and July, which showed that actual overhead costs were 20,000 each month. She also discovered that direct labor hours worked on all jobs were 500 hours in May and 250 hours each in June and July. Required: 1. How do you think Mrs. Lucky will feel when she receives the bill for the three sets of wedding announcements? 2. Explain how the overhead costs were assigned to each job. 3. Assume that Reynoldss average activity is 500 hours per month and that the company usually experiences overhead costs of 240,000 each year. Can you recommend a better way to assign overhead costs to jobs? Recompute the cost of each job and its price, given your method of overhead cost assignment. Which method do you think is best? Why?arrow_forwardA manufacturing company has two service and two production departments. Human Resources and Machine Repair are the service departments. The production departments are Grinding and Polishing. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The human resources department services all departments of the company, and its costs are allocated using the numbers of employees within each department, while machine repair costs are allocable to Grinding and Polishing on the basis of machine hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,