Concept explainers

Videos

1.

Prepare general journal entries to record transactions (a) through (k) and make compound entries for (b), (d), and (h), with separate debits for each job.

1.

Explanation of Solution

Job order costing is one of the methods of cost accounting under which cost is collected and gathered for each job, work order, or project separately. It is a system by which a factory maintains a separate record of each particular quantity of product that passes through the factory. Job order costing is used when the products produced are significantly different from each other.

Prepare

| Date | Accounts title and explanation |

Debit ($) |

Credit ($) |

| a. | Material | 45,000 | |

| Accounts payable | 45,000 | ||

| (To record the purchase of materials on account.) | |||

| b. | Work in process | 10,000 | |

| Work in process | 11,000 | ||

| Work in process | 9,500 | ||

| Work in process | 12,200 | ||

| Materials | 42,700 | ||

| (To record issuance of direct materials for the job: job no.201,202,203,204) | |||

| c. | Factory overhead | 7,500 | |

| Materials | 7,500 | ||

| (To record the issuance of indirect materials) | |||

| d. | Work in process | 18,000 | |

| Work in process | 19,000 | ||

| Work in process | 20,500 | ||

| Work in process | 17,500 | ||

| Wages payable | 75,000 | ||

| (To record direct labor incurred for the job: job no.201,202,203,204) | |||

| e. | Factory overhead | 11,000 | |

| Wages payable | 11,000 | ||

| (To record the indirect labor charged to production) | |||

| f. | Factory overhead | 7,000 | |

| Cash | 7,000 | ||

| (To record the payment of electricity bill, heating oil, and repairs bills for the factory and charge made to production) | |||

| g. | Factory overhead | 40,000 | |

| | 40,000 | ||

| (To record the depreciation expense on factory equipment) | |||

| h. | Work in process | 15,000 | |

| Work in process | 16,500 | ||

| Work in process | 16,500 | ||

| Work in process | 18,000 | ||

| Factory overhead | 66,000 | ||

| (To record applied factory overhead to the job: job no.201,202,203,204) | |||

| i. | Finished goods (Product C) | 43,000 | |

| Work in process | 43,000 | ||

| (To record the transfer of Job no. 201 to Product C) | |||

| Finished goods (Product D) | 46,500 | ||

| Work in process | 46,500 | ||

| (To record the transfer of Job no.202 to Product D) | |||

| Finished goods (Product E) | 46,500 | ||

| Work in process | 46,500 | ||

| (To record the transfer of Job no.203 to Product E) | |||

| j. | Accounts receivable | 47,000 | |

| Sales | 47,000 | ||

| (To record sale of product C) | |||

| Cost of goods sold | 43,000 | ||

| Finished goods (Product C) | 43,000 | ||

| (To record cost of goods sold on finished goods of Product C) | |||

| Accounts receivable | 49,000 | ||

| Sales | 49,000 | ||

| (To record sale of product D) | |||

| Cost of goods sold | 46,500 | ||

| Finished goods (Product D) | 46,500 | ||

| (To record cost of goods sold on finished goods of Product D) | |||

| k. | Factory overhead | 500 | |

| Cost of goods sold (2) | 500 | ||

| (To record cost of goods sold) |

(Table 1)

Working note:

(1) Calculate the actual factory overhead:

(2) Calculate the cost of goods sold:

2.

2.

Explanation of Solution

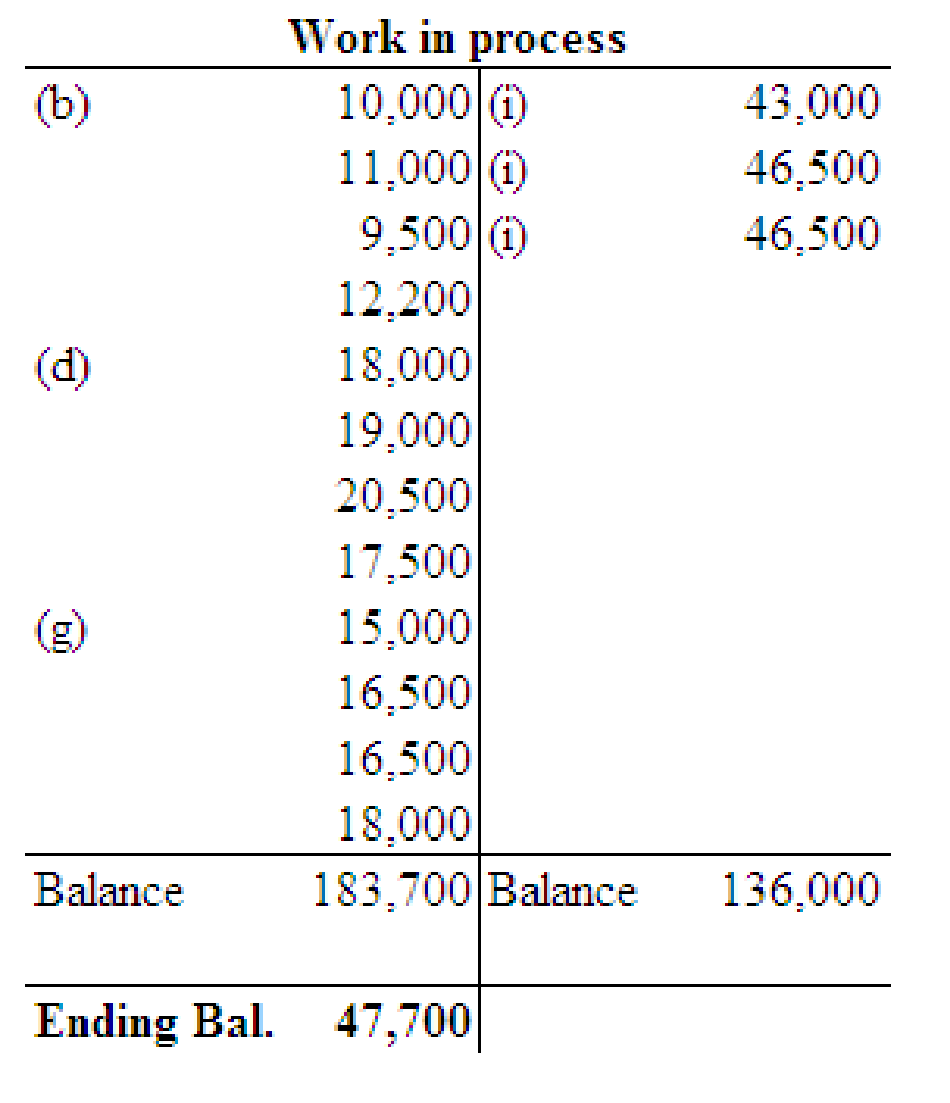

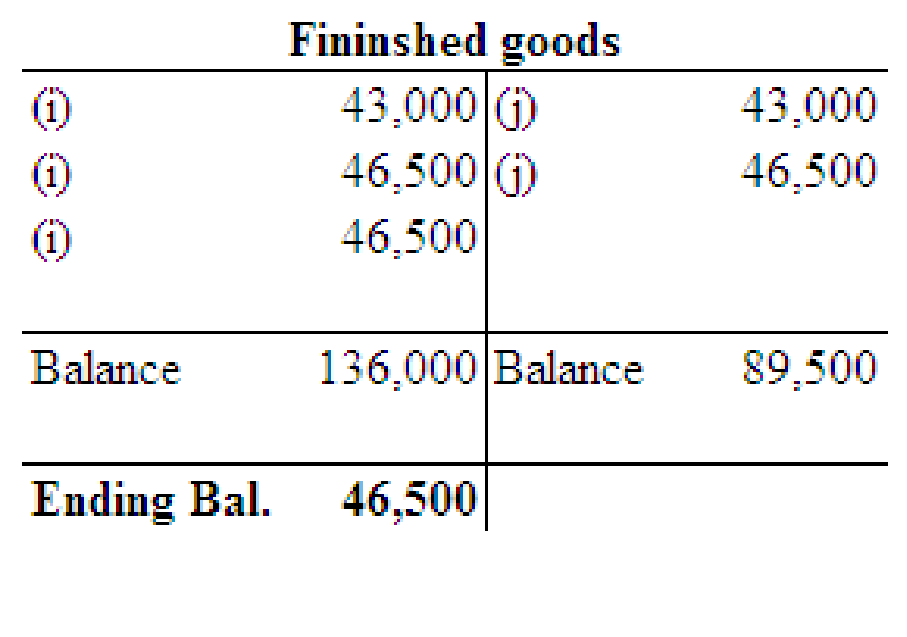

Post the entries to the work in process and finished goods T accounts and determine the ending balances in these accounts.

3.

Compute the balance in the job cost ledger and verify whether the balance agrees with that in the work in process control account.

3.

Explanation of Solution

The balance of the job cost ledger (Job No.204) is $47,700

Want to see more full solutions like this?

Chapter 26 Solutions

College accounting, chapters 1-9

- JOB ORDER COSTING WITH UNDER- AND OVERAPPLIED FACTORY OVERHEAD M Evans Sons manufactures parts for radios. For each job order, it maintains ledger sheets on which it records direct labor, direct materials, and factory overhead applied. The factory overhead control account contains postings of actual overhead costs. At the end of the month, the under- or overapplied factory overhead is charged to the cost of goods sold account. Factory overhead is applied on the basis of direct labor hours. For Job Nos. 101, 102, 103, and 104, direct labor hours are 12,000, 10,000, 11,000, and 18,000, respectively. The overhead application rate is 1.20/direct labor hour (a) Purchased raw materials on account, 50,000. (b) Issued direct materials: (c) Issued indirect materials to production, 8,000. (d) Incurred direct labor costs: (e) Charged indirect labor to production, 15,000. (f) Paid electricity bill, taxes, and repair fees for the factory and charged to production, 8,000. (g) Depreciation expense on factory equipment, 30,000. (h) Applied factory overhead to Job Nos. 101-104 using the predetermined factory overhead rare (see above). (i) Finished Job Nos. 101-103 and transferred to the finished goods inventory account as products N, O, and P. (j) Sold products N and O for 50,000 and 45,400, respectively. (k) Transferred under- or overapplied factory overhead balance to the cost of goods sold account. REQUIRED 1. Prepare general journal entries to record transactions (a) through (k). Make compound entries for (b), (d), and (h), with separate debits for each job. 2. Post the entries to the work in process and finished goods T accounts only and determine the ending balances in these accounts. 3. Compute the balance in the job cost ledger and verify that this balance agrees with that in the work in process control account.arrow_forwardJOB ORDER COSTING WITH UNDER- AND OVERAPPLIED FACTORY OVERHEAD M. Evans Sons manufactures parts for radios. For each job order, it maintains ledger sheets on which it records direct labor, direct materials, and factory overhead applied. The factory overhead control account contains postings of actual overhead costs. At the end of the month, the under- or over applied factory overhead is charged to the cost of goods sold account. Factory overhead is applied on the basis of direct labor hours. For Job Nos. 101, 102,103, and 104, direct labor hours are 12, 000, 10,000, 11, 000, and 18,000, respectively. The overhead application rate is 1.20/direct labor hour. (a) Purchased raw materials on account, 50,000. (b) Issued direct materials: (c) Issued indirect materials to production, 8,000. (d) Incurred direct labor costs: (e) Charged indirect labor to production, 15,000. (f) Paid electricity bill, taxes, and repair fees for the factory and charged to production, 8,000. (g) Depreciation expense on factory equipment, 30,000. (h) Applied factory overhead to Job Nos. 101104 using the predetermined factory overhead rate (see above). (i) Finished Job Nos. 101103 and transferred to the finished goods inventory account as products N, O, and P. (j) Sold products N and for 50,000 and 45,400, respectively. (k) Transferred under- or over applied factory overhead balance to the cost of goods sold account. REQUIRED 1. Prepare general journal entries to record transactions (a) through (k). 2. Post the entries to the work in process and finished goods accounts only and determine the ending balances in these accounts. 3. Compute the balance in the job cost ledger and verify that this balance agrees with that in the work in process control account.arrow_forwardChannel Products Inc. uses the job order cost system of accounting. The following is a list of the jobs completed during March, showing the charges for materials issued to production and for direct labor. Assume that factory overhead is applied on the basis of direct labor costs and that the predetermined rate is 200%. Required: Compute the amount of overhead to be added to the cost of each job completed during the month. Compute the total cost of each job completed during the month. Compute the total cost of producing all the jobs finished during the month.arrow_forward

- Leen Production Co. uses the job order cost system of accounting. The following information was taken from the companys books after all posting had been completed at the end of May: a. Compute the total production cost of each job. b. Prepare the journal entry to transfer the cost of jobs completed to Finished Goods. c. Compute the selling price per unit for each job, assuming a mark-on percentage of 40%. d. Prepare the journal entries to record the sale of Job 1065.arrow_forwardJOURNAL ENTRIES FOR FACTORY OVERHEAD Huang Company manufactures toys. It keeps a factory overhead account where actual factory overhead costs are recorded as a debit, and factory overhead applied is recorded as a credit. At the end of the month, under- or overapplied factory overhead is calculated and transferred to the cost of goods sold account. For the month of January, Huang had the following overhead transactions. Make appropriate general journal entries to record factory overhead and factory overhead applied, and to close the under- or overapplied factory overhead to the cost of goods sold account. Jan.1 Paid rent, 1,000. 10 Paid electricity bill, 250. 15 Paid repair expense, 1,500. 21 Vacation pay for machine operator, 500 (Wages Payable). 31 Depreciation expense for the month, 450. 31 Factory overhead applied was 3,500.arrow_forwardJOURNAL ENTRIES FOR MATERIAL. LABOR, OVERHEAD, AND SALES Alert Enterprises had the following job order transactions during the month of April. Record the transactions in the general journal, including issuance of materials, labor, and factory overhead applied; completed jobs sent to finished goods inventory; closing of the under- or overapplied factory overhead to the cost of goods sold account; and sale of finished goods. Make compound entries for both transactions dared April 25, with separate debits for each job.arrow_forward

- Kingsford Furnishings Company manufactures designer furniture. Kingsford Furnishings uses a job order cost system. Balances on April 1 from the materials ledger are as follows: The materials purchased during April are summarized from the receiving reports as follows: Materials were requisitioned to individual jobs as follows: The glue is not a significant cost, so it is treated as indirect materials (factory overhead). a. Journalize the entry to record the purchase of materials in April. b. Journalize the entry to record the requisition of materials in April. c. Determine the April 30 balances that would be shown in the materials ledger accounts.arrow_forwardSummary information from a companys job cost sheets shows the following information: What are the balances in the work in process inventory, finished goods Inventory, and cost of goods sold for April, May, and June?arrow_forwardSultan, Inc. manufactures goods to special order and uses a job order cost system. During its first month of operations, the following selected transactions took place: Required: 1. Prepare a schedule reflecting the cost of each of the four jobs. 2. Prepare journal entries to record the transactions. 3. Compute the ending balance in Work in Process. 4. Compute the ending balance in Finished Goods.arrow_forward

- JOURNAL ENTRIES FOR FACTORY OVERHEAD Bandy Company manufactures toys. It keeps a factory overhead account where actual factory overhead costs are recorded as a debit and factory overhead applied is recorded as a credit. At the end of the month, under- or overapplied factory overhead is calculated and transferred to the cost of goods sold account. For the month of January, Bandy had the following overhead transactions. Make appropriate general journal entries to record factory overhead and factory overhead applied, and to close the under- or overapplied factory overhead to the cost of goods sold account. Jan. 1 Paid rent, 2,000. 10 Paid electricity bill, 500. 15 Paid repair expense, 3,000. 21 Vacation pay for machine operator, 500 (Wages Payable). 31 Depreciation expense for the month, 500. 31 Factory overhead applied was 6,000.arrow_forwardJob cost sheets show the following information: What are the balances in the work in process inventory, finished goods inventory, and cost of goods sold for January, February, and March?arrow_forwardThe following information, taken from the books of Herman Brothers Manufacturing represents the operations for January: The job cost system is used, and the February cost sheet for Job M45 shows the following: The following actual information was accumulated during February: Required: 1. Using the January data, ascertain the predetermined factory overhead rates to be used during February, based on the following: a. Direct labor cost b. Direct labor hours c. Machine hours 2. Prepare a schedule showing the total production cost of Job M45 under each method of applying factory overhead. 3. Prepare the entries to record the following for February operations: a. The liability for total factory overhead. b. Distribution of factory overhead to the departments. c. Application of factory overhead to the work in process in each department, using direct labor hours. (Use the predetermined rate calculated in Requirement 1.) d. Closing of the applied factory overhead accounts. e. Recording under- and overapplied factory overhead and closing the actual factory overhead accounts.arrow_forward

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning