Concept explainers

Videos

Sweet Dreams Bakery was started five years ago by Della Fontera who was known for her breads, sweet rolls, and personalized cakes. Della had kept her accounting system simple, believing that she had a good intuitive handle on costs. She had been using the following formula to describe her monthly overhead costs:

Overhead cost = $7,800 + $7.50 (direct labor hours)

For breads and sweet rolls that were available in the bakery case each day, she applied a standard pricing system. For special orders, however, Della needed her cost formula to help her come up with an estimated cost for the personalized cake or wedding cake. To that cost, she applied a markup percentage.

Lately, however, the increase in the variety of orders and the elaborateness of the wedding cakes made her wonder if a more sophisticated view of costs would help her in planning, budgeting, and pricing.

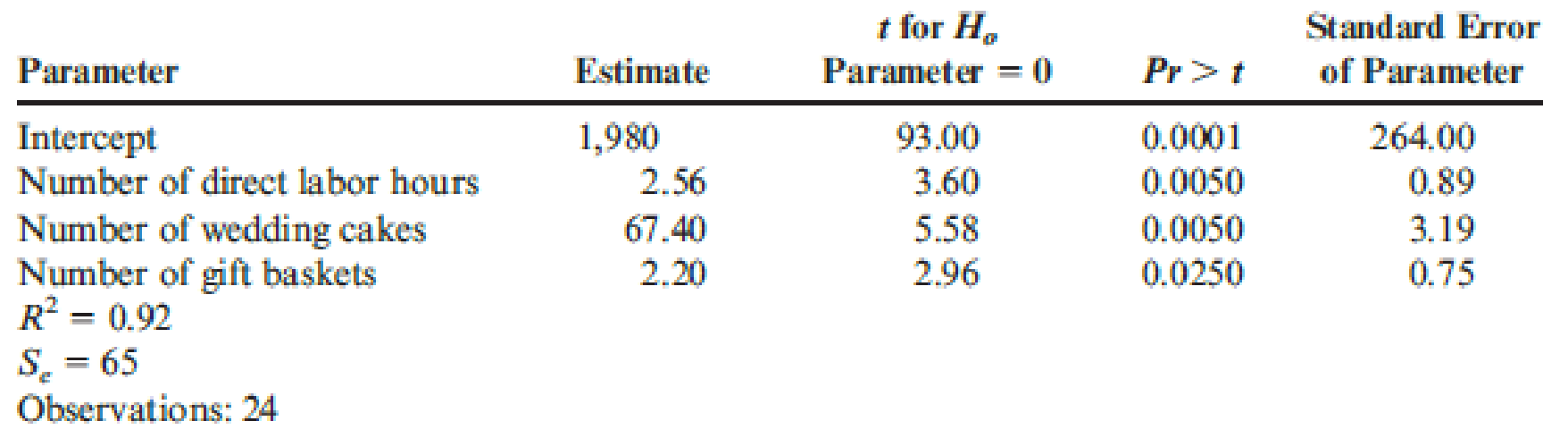

After some late-night discussions with her workers, Della determined that Sweet Dreams’ expansion into wedding cakes and gift baskets had made special orders a more complex operation. The various shapes of the wedding cake tiers had required Della’s investing in different- sized cake pans, as well as decorating tips for icing. The different icing patterns and elaborate designs took much more time for icing, as well. In addition, while a five-year-old’s birthday cake just requires that the child’s name and (possibly) the superhero’s name are spelled correctly, a wedding cake is a once-in-a-lifetime item that must achieve perfection. (Della hated to use the term “bridezilla” but.…) Gift baskets required Della to stock baskets, cellophane, and bows. Then when an order came in, a worker had to stop baking to arrange the muffins and breads artfully in the basket, wrap it, and tie the bow. While it seemed simple enough, this took time and thought. Thus, the number of direct labor hours was still an important variable, but so were the number of wedding cakes and gift baskets. Della rummaged through her college textbooks and found information on regression. Then, with help from one of her computer savvy workers, she ran multiple regression tables for the past 24 months of data for Sweet Dreams for three independent variables: number of direct labor hours, the number of wedding cakes, and the number of gift baskets. The following printout was obtained:

Required:

- 1. Write out the cost equation for Sweet Dreams’ monthly overhead cost.

- 2. Suppose that next month Sweet Dreams expects to have 550 direct labor hours, 35 wedding cakes, and 20 gift baskets. What is the expected overhead? (Round to the nearest dollar.)

- 3. What does R2 mean in this equation? Overall, what is your evaluation of the cost equation that was developed for the cost of overhead? Suppose that Sweet Dreams charges an extra $2.50 to prepare a gift basket. This charge is in addition to the price charged for the items (e.g., muffins) that the customer chooses to put into the basket. How might Della use the results of the regression equation to see whether or not the $2.50 charge is appropriate?

Trending nowThis is a popular solution!

Chapter 3 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Salley is developing material and labor standards for her company. She finds that it costs $0.55 per pound of material per widget. Each widget requires 6 pounds of material per widget. Salley is also working with the operations manager to determine what the standard labor cost is for a widget. Upon observation, Salley notes that it takes 3 hours in the assembly department and 1 hour in the finishing department to complete one widget. All employees are paid $10.50 per hour. A. What is the standard materials cost per unit for a widget? 8. What is the standard labor cost per unit for a widget?arrow_forwardVentana Window and Wall Treatments Company provides draperies, shades, and various window treatments. Ventana works with the customer to design the appropriate window treatment, places the order, and installs the finished product. Direct materials and direct labor costs are easy to trace to the jobs. Ventanas income statement for last year is as follows: Ventana wants to find a markup on cost of goods sold that will allow them to earn about the same amount of profit on each job as was earned last year. Required: 1. What is the markup on cost of goods sold (COGS) that will maintain the same profit as last year? (Round the percentage to two significant digits.) 2. A customer orders draperies and shades for a remodeling job. The job will have the following costs: What is the price that Ventana will quote given the markup percentage calculated in Requirement 1? (Round the price to the nearest dollar.) 3. What if Ventana wants to calculate a markup on direct materials cost, since it is the largest cost of doing business? What is the markup on direct materials cost that will maintain the same profit as last year? (Round the percentage to two significant digits.) What is the bid price Ventana will use for the job given in Requirement 2 if the markup percentage is calculated on the basis of direct materials cost? (Round to the nearest dollar.)arrow_forwardBig Mikes, a large hardware store, has gathered data on its overhead activities and associated costs for the past 10 months. Nizam Sanjay, a member of the controllers department, believes that overhead activities and costs should be classified into groups that have the same driver. He has decided that unloading incoming goods, counting goods, and inspecting goods can be grouped together as a more general receiving activity, since these three activities are all driven by the number of receiving orders. The 10 months of data shown below have been gathered for the receiving activity. Required: 1. Prepare a scattergraph, plotting the receiving costs against the number of purchase orders. Use the vertical axis for costs and the horizontal axis for orders. 2. Select two points that make the best fit, and compute a cost formula for receiving costs. 3. Using the high-low method, prepare a cost formula for the receiving activity. 4. Using the method of least squares, prepare a cost formula for the receiving activity. What is the coefficient of determination?arrow_forward

- You are a management accountant for Time Treasures Company, whose company has recently signed an outsourcing agreement with Spotless. Inc., a janitorial service company. Spotless will provide all of Time Treasures janitorial services, including sweeping floors, hauling trash, washing windows, stocking restrooms, and performing minor repairs. Time Treasures will be billed at an hourly rate based on the type of service performed. The work of common laborers (sweeping, hauling trash) is to be billed at $8 per hour. More skilled (repairs) and more dangerous work (washing outside windows on the 23rd floor) are to be billed at $18 per hour. Supervisory time is to be billed at $20 per hour. Spotless will submit monthly invoices, which will show the number and types of hours for which Time Treasures is being charged. The outsourcing contract is simple and straightforward. A. What are some of the internal control problems you foresee as a result of our sourcing the janitorial service with this contract? B. Explain recommendations to control risk that would you suggest after reviewing the contract.arrow_forwardMott Company recently implemented a JIT manufacturing system. After one year of operation, Heidi Burrows, president of the company, wanted to compare product cost under the JIT system with product cost under the old system. Motts two products are weed eaters and lawn edgers. The unit prime costs under the old system are as follows: Under the old manufacturing system, the company operated three service centers and two production departments. Overhead was applied using departmental overhead rates. The direct overhead costs associated with each department for the year preceding the installation of JIT are as follows: Under the old system, the overhead costs of the service departments were allocated directly to the producing departments and then to the products passing through them. (Both products passed through each producing department.) The overhead rate for the Machining Department was based on machine hours, and the overhead rate for assembly was based on direct labor hours. During the last year of operations for the old system, the Machining Department used 80,000 machine hours, and the Assembly Department used 20,000 direct labor hours. Each weed eater required 1.0 machine hour in Machining and 0.25 direct labor hour in Assembly. Each lawn edger required 2.0 machine hours in Machining and 0.5 hour in Assembly. Bases for allocation of the service costs are as follows: Upon implementing JIT, a manufacturing cell for each product was created to replace the departmental structure. Each cell occupied 40,000 square feet. Maintenance and materials handling were both decentralized to the cell level. Essentially, cell workers were trained to operate the machines in each cell, assemble the components, maintain the machines, and move the partially completed units from one point to the next within the cell. During the first year of the JIT system, the company produced and sold 20,000 weed eaters and 30,000 lawn edgers. This output was identical to that for the last year of operations under the old system. The following costs have been assigned to the manufacturing cells: Required: 1. Compute the unit cost for each product under the old manufacturing system. 2. Compute the unit cost for each product under the JIT system. 3. Which of the unit costs is more accurate? Explain. Include in your explanation a discussion of how the computational approaches differ. 4. Calculate the decrease in overhead costs under JIT, and provide some possible reasons that explain the decrease.arrow_forwardBrees, Inc., a manufacturer of golf carts, has just received an offer from a supplier to provide 2,600 units of a component used in its main product. The component is a track assembly that is currently produced internally. The supplier has offered to sell the track assembly for 66 per unit. Brees is currently using a traditional, unit-based costing system that assigns overhead to jobs on the basis of direct labor hours. The estimated traditional full cost of producing the track assembly is as follows: Prior to making a decision, the companys CEO commissioned a special study to see whether there would be any decrease in the fixed overhead costs. The results of the study revealed the following: 3 setups1,160 each (The setups would be avoided, and total spending could be reduced by 1,160 per setup.) One half-time inspector is needed. The company already uses part-time inspectors hired through a temporary employment agency. The yearly cost of the part-time inspectors for the track assembly operation is 12,300 and could be totally avoided if the part were purchased. Engineering work: 470 hours, 45/hour. (Although the work decreases by 470 hours, the engineer assigned to the track assembly line also spends time on other products, and there would be no reduction in his salary.) 75 fewer material moves at 30 per move. Required: 1. Ignore the special study, and determine whether the track assembly should be produced internally or purchased from the supplier. 2. Now, using the special study data, repeat the analysis. 3. Discuss the qualitative factors that would affect the decision, including strategic implications. 4. After reviewing the special study, the controller made the following remark: This study ignores the additional activity demands that purchasing would cause. For example, although the demand for inspecting the part on the production floor decreases, we may need to inspect the incoming parts in the receiving area. Will we actually save any inspection costs? Is the controller right?arrow_forward

- Jean and Tom Perritz own and manage Happy Home Helpers, Inc. (HHH), a house-cleaning service. Each cleaning (cleaning one house one time) takes a team of three house cleaners about 1.5 hours. On average, HHH completes about 15,000 cleanings per year. The following total costs are associated with the total cleanings: Next year, HHH expects to purchase 25,600 of direct materials. Projected beginning and ending inventories for direct materials are as follows: There is no work-in-process inventory; in other words, a cleaning is started and completed on the same day. Required: 1. Prepare a statement of services produced in good form. 2. What if HHH planned to purchase 30,000 of direct materials? Assume there would be no change in beginning and ending inventories of materials. Explain which line items on the statement of services produced would be affected and how (increase or decrease).arrow_forwardJean and Tom Perritz own and manage Happy Home Helpers, Inc. (HHH), a house-cleaning service. Each cleaning (cleaning one house one time) takes a team of three house cleaners about 1.5 hours. On average, HHH completes about 15,000 cleanings per year. The following total costs are associated with the total cleanings: Next year, HHH expects to purchase 25,600 of direct materials. Projected beginning and ending inventories for direct materials are as follows: There is no work-in-process inventory and no finished goods inventory; in other words, a cleaning is started and completed on the same day. HHH expects to sell 15,000 cleanings at a price of 45 each next year. Total selling expense is projected at 22,000, and total administrative expense is projected at 53,000. Required: 1. Prepare an income statement in good form. 2. What if Jean and Tom increased the price to 50 per cleaning and no other information was affected? Explain which line items in the income statement would be affected and how.arrow_forwardBox Springs. Inc., makes two sizes of box springs: queen and king. The direct material for the queen is $35 per unit and $55 is used in direct labor, while the direct material for the king is $55 per unit, and the labor cost is $70 per unit. Box Springs estimates it will make 4,300 queens and 3,000 kings in the next year. It estimates the overhead for each cost pool and cost driver activities as follows: How much does each unit cost to manufacture?arrow_forward

- Reggie Wilmore has just started a new businessbuilding and installing custom garage organization systems. Reggie builds the cabinets and work benches in his workshop, then installs them in clients garages. Reggie figures his overhead for the coming year will be 12,000. Since his business is labor intensive, he plans to use direct labor hours as his overhead driver. For the coming year, he expects to complete 100 jobs, averaging 25 direct labor hours each. However, he has the capacity to complete 125 jobs averaging 25 direct labor hours each. Required: 1. Four measures of activity level were mentioned in the text. Which two measures is Reggie considering in computing a predetermined overhead rate? 2. Compute the predetermined overhead rates using each of the measures in your answer to Requirement 1. 3. Which one would you recommend that Reggie use? Why?arrow_forwardReggie Wilmore has just started a new businessbuilding and installing custom garage organization systems. Reggie builds the cabinets and work benches in his workshop, then installs them in clients garages. Reggie figures his overhead for the coming year will be 12,000. Since his business is labor intensive, he plans to use direct labor hours as his overhead driver. For the coming year, he expects to complete 100 jobs, averaging 25 direct labor hours each. However, he has the capacity to complete 125 jobs averaging 25 direct labor hours each. Required: 1. What source documents will Reggie need to account for costs in his new business? 2. Suppose Reggies business grows, and he expands his workshop and hires three additional carpenters to help him. What source documents will he need now?arrow_forwardFirenza Company manufactures specialty tools to customer order. Budgeted overhead for the coming year is: Previously, Sanjay Bhatt, Firenza Companys controller, had applied overhead on the basis of machine hours. Expected machine hours for the coming year are 50,000. Sanjay has been reading about activity-based costing, and he wonders whether or not it might offer some advantages to his company. He decided that appropriate drivers for overhead activities are purchase orders for purchasing, number of setups for setup cost, engineering hours for engineering cost, and machine hours for other. Budgeted amounts for these drivers are 5,000 purchase orders, 500 setups, and 2,500 engineering hours. Sanjay has been asked to prepare bids for two jobs with the following information: The typical bid price includes a 40 percent markup over full manufacturing cost. Required: 1. Calculate a plantwide rate for Firenza Company based on machine hours. What is the bid price of each job using this rate? 2. Calculate activity rates for the four overhead activities. What is the bid price of each job using these rates? 3. Which bids are more accurate? Why?arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College