Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN: 9781337788281

Author: James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 6, Problem 17P

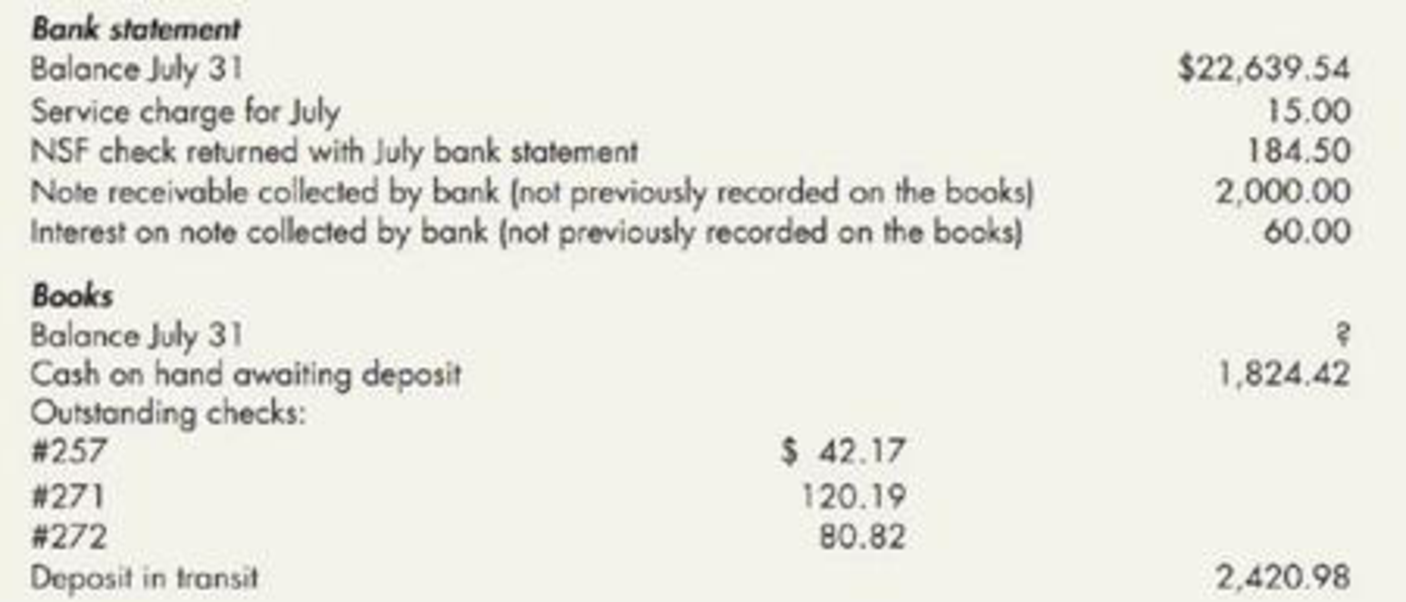

Unknown Book Balance (Appendix 6.1) The following information pertains to the Cash account of Nakamoto Corporation for the month of July 2019:

Required:

- 1. Prepare a bank reconciliation to determine Nakamoto’s adjusted cash balance on July 31.

- 2. Next Level Determine Nakamoto’s unadjusted cash balance (per books) on July 31.

- 3. Prepare the

adjusting entries necessary to bring Nakamoto’s cash account balance up to date on July 31.

Expert Solution & Answer

Trending nowThis is a popular solution!

Chapter 6 Solutions

Intermediate Accounting: Reporting And Analysis

Ch. 6 - What are the components of cash? What items may be...Ch. 6 - Prob. 2GICh. 6 - Prob. 3GICh. 6 - Prob. 4GICh. 6 - Prob. 5GICh. 6 - How are trade receivables different from nontrade...Ch. 6 - How is revenue recognition related to the...Ch. 6 - Prob. 8GICh. 6 - Prob. 9GICh. 6 - What is a sales return? A sales allowance?...

Ch. 6 - Discuss the differences between the allowance...Ch. 6 - Prob. 12GICh. 6 - Prob. 13GICh. 6 - What method of bad debt estimation categorizes...Ch. 6 - Why does the write-off of uncollectible accounts...Ch. 6 - Discuss the difference between a secured borrowing...Ch. 6 - When does a company record the transfer of...Ch. 6 - Prob. 18GICh. 6 - What is a non-interest-bearing note? How does...Ch. 6 - Prob. 20GICh. 6 - How are the cash proceeds determined when a note...Ch. 6 - Under IFRS, what criteria must be satisfied in...Ch. 6 - Prob. 23GICh. 6 - (Appendix 6. 1) What is the purpose of a petty...Ch. 6 - (Appendix 6. 7) Why are actual expenses, rather...Ch. 6 - Prob. 26GICh. 6 - Prob. 27GICh. 6 - Prob. 1MCCh. 6 - Greenfield Company had the following cash balances...Ch. 6 - A company is in its first year of operations and...Ch. 6 - Marmol Corporation uses the allowance method for...Ch. 6 - On January 1, 2019, King Companys Allowance for...Ch. 6 - Prior to adjustments, Barrett Companys account...Ch. 6 - A method of estimating bad debts that focuses on...Ch. 6 - When the accounts receivable of a company are sold...Ch. 6 - Prob. 9MCCh. 6 - Prob. 10MCCh. 6 - Prob. 11MCCh. 6 - On December 31, Harrison Company reports the...Ch. 6 - Lindley Enterprises sells hand woven rugs. Paige...Ch. 6 - Long Corporation is a fabric manufacturing...Ch. 6 - Refer to RE6-3. Assume Long records accounts...Ch. 6 - Longmire Sons nude sales un credit to Alderman...Ch. 6 - Refer to RE6-5. Assume Longmire uses a perpetual...Ch. 6 - McKinney Co. estimates its uncollectible accounts...Ch. 6 - Refer to RE6-7. At the end of the first quarter of...Ch. 6 - Refer to RE6-8. On April 23, 2020, McKinncy Co....Ch. 6 - On December 1 of the current year, Jordan Inc....Ch. 6 - On December 1 of the current year, Jordan Inc....Ch. 6 - On December 1, Newton Enterprises sells 100,000 of...Ch. 6 - Kaseys Cake Shop made 20,000 in sales of wedding...Ch. 6 - On June 1, Phillips Corporation sold, with...Ch. 6 - Prob. 15RECh. 6 - Prob. 16RECh. 6 - Computing; the Cash Balance Listed below are ten...Ch. 6 - Prob. 2ECh. 6 - Journal Entry to Separate Receivables An...Ch. 6 - Prob. 4ECh. 6 - Prob. 5ECh. 6 - Prob. 6ECh. 6 - Accounts Receivable Calculations The following...Ch. 6 - Estimation versus Direct Write-Off of Bad Debts...Ch. 6 - Estimating Bad Debts from Receivables Balances The...Ch. 6 - Aging Analysis of Accounts Receivable Cowens, a...Ch. 6 - Comparison of Bad Debt Estimation Methods Bradford...Ch. 6 - Inferring Accounts Receivable Amounts At the end...Ch. 6 - ReceivablesBad Debts At January 1, 2019, the...Ch. 6 - Transferring Accounts Receivable White Corporation...Ch. 6 - Transfer of Accounts Receivable Inder Corporation...Ch. 6 - Generating Cash from Receivables Guide Company...Ch. 6 - Interest-Bearing and Non-Interest-Bearing Notes On...Ch. 6 - Computing the Proceeds from the Sale of Notes...Ch. 6 - Recording the Sale of Notes Receivable Singer...Ch. 6 - Prob. 20ECh. 6 - Prob. 21ECh. 6 - Prob. 22ECh. 6 - Prob. 23ECh. 6 - Prob. 24ECh. 6 - Prob. 1PCh. 6 - Prob. 2PCh. 6 - Estimating Bad Debts Keegan Corporations...Ch. 6 - Allowance for Bad Accounts Installment Jewelry...Ch. 6 - Allowance for Doubtful Accounts From inception of...Ch. 6 - Prob. 6PCh. 6 - Aging Accounts Receivable On September 30. 2019...Ch. 6 - Prob. 8PCh. 6 - Prob. 9PCh. 6 - Prob. 10PCh. 6 - Factoring and Assignment of Accounts Receivable...Ch. 6 - Recording Note Transactions The following...Ch. 6 - Notes Receivable Transactions The following notes...Ch. 6 - Analyzing Accounts Receivable Upham Companys June...Ch. 6 - Comprehensive Receivables Problem Blackmon...Ch. 6 - Prob. 16PCh. 6 - Unknown Book Balance (Appendix 6.1) The following...Ch. 6 - Prob. 18PCh. 6 - Prob. 19PCh. 6 - Prob. 1CCh. 6 - Prob. 2CCh. 6 - Bad Debt Expense When a company has a policy of...Ch. 6 - Prob. 4CCh. 6 - Receivables Issues Magrath Company has an...Ch. 6 - Components of Cash Cash is an important asset of a...Ch. 6 - Prob. 7CCh. 6 - Transfer of Accounts and Notes Receivable Tidal...Ch. 6 - Ethics and Sales Returns At the end of 2019, the...Ch. 6 - Analyzing Starbuckss Cash and Receivables...Ch. 6 - Researching GAAP Situation Hamilton Company...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Complex Balance Sheet Presented below is the unaudited balance sheet as of December 31, 2019, prepared by Zeus Manufacturing Corporations bookkeeper. Your company has been engaged to perform an audit, during which you discover the following information: 1. Checks totaling 14,000 in payment of accounts payable were mailed on December 31, 2019, but were not recorded until 2020. Late in December 2019, the bank returned a customers 2,000 check marked NSF, but no entry was made. Cash includes 100,000 restricted for building purposes. 2. Included in accounts receivable is a 30,000 note due on December 31, 2022, from Zeuss president. 3. During 2019, Zeus purchased 500 shares of common stock of a major corporation that supplies Zeus with raw materials. Total cost of this stock was 51,300, and fair value on December 31, 2019, was 51,300. Zeus plans to hold these shares indefinitely. 4. Treasury stock was recorded at cost when Zeus purchased 200 of its own shares for 32 per share in May 2019. This amount is included in investments. 5. On December 31, 2019, Zeus borrowed 500,000 from a bank in exchange for a 10% note payable, manning December 31, 2024. Equal principal payments are due December 31 of each year beginning in 2020. This note is collateralized by a 250,000 tract of land acquired as a potential future building site, which is included in land. 6. The mortgage payable requires 50,000 principal payments, plus interest, at the end of each month. Payments were made on January 31 and February 28, 2020. The balance of this mortgage was due June 30, 2020. On March 1, 2020, prior to issuance of the audited financial statements, Zeus consummated a non-cancelable agreement with the lender to refinance this mortgage. The new terms require 100,000 annual principal payments, plus interest, on February 28 of each year, beginning in 2021. The final payment is due February 28, 2028. 7. The lawsuit liability will be paid in 2020. 8. Of the total deferred tax liability; 5,000 is considered a current liability. 9. The current income tax expense reported in Zeuss 2019 income statement was 61,200. 10. The company was authorized to issue 100,000 shares of 50 par value common stock.arrow_forwardCromwell Company has the following trial balance account balances, given in no certain order, as of December 31, 2018. Using the information provided, prepare Cromwells annual financial statements (omit the Statement of Cash Flows).arrow_forwardThe accounts in the ledger of Hickory Furniture Company as of December 31, 2019, are listed in alphabetical order as follows. All accounts have normal balances. The balance of the cash account has been intentionally omitted. Prepare an unadjusted trial balance, listing the accounts in their normal order and inserting the missing figure for cash.arrow_forward

- The revenue and cash receipts journals for Mirage Productions Inc. follow. The accounts receivable control account has a August 1, 2016, balance of 4,230 consisting of an amount due from Celestial Studios Inc. Prepare a listing of the accounts receivable customer balances and verify that the total agrees with the ending balance of the accounts receivable controlling account.arrow_forwardDetermining Cash Flows from Financing Activities Solomon Construction Company reported the following amount on its balance sheet at the end of 2019 and 2018 for notes payable: Required: 1. If Solomon did not repay any notes payable during 2019, determine how much cash Solomon received from the issuance of notes payable. 2. If Solomon repaid $40,000 of notes payable during 2019, determine what amounts Solomon would report in the financing activities section of the statement of cash flows.arrow_forwardOn December 31, Harrison Company reports the following assets: Which of these are included in, and excluded from, cash on the companys balance sheet?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning  College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Survey of Accounting (Accounting I)

Accounting

ISBN:9781305961883

Author:Carl Warren

Publisher:Cengage Learning

College Accounting (Book Only): A Career Approach

Accounting

ISBN:9781337280570

Author:Scott, Cathy J.

Publisher:South-Western College Pub

Financial Accounting

Accounting

ISBN:9781305088436

Author:Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:Cengage Learning

The accounting cycle; Author: Alanis Business academy;https://www.youtube.com/watch?v=XTspj8CtzPk;License: Standard YouTube License, CC-BY