Concept explainers

Videos

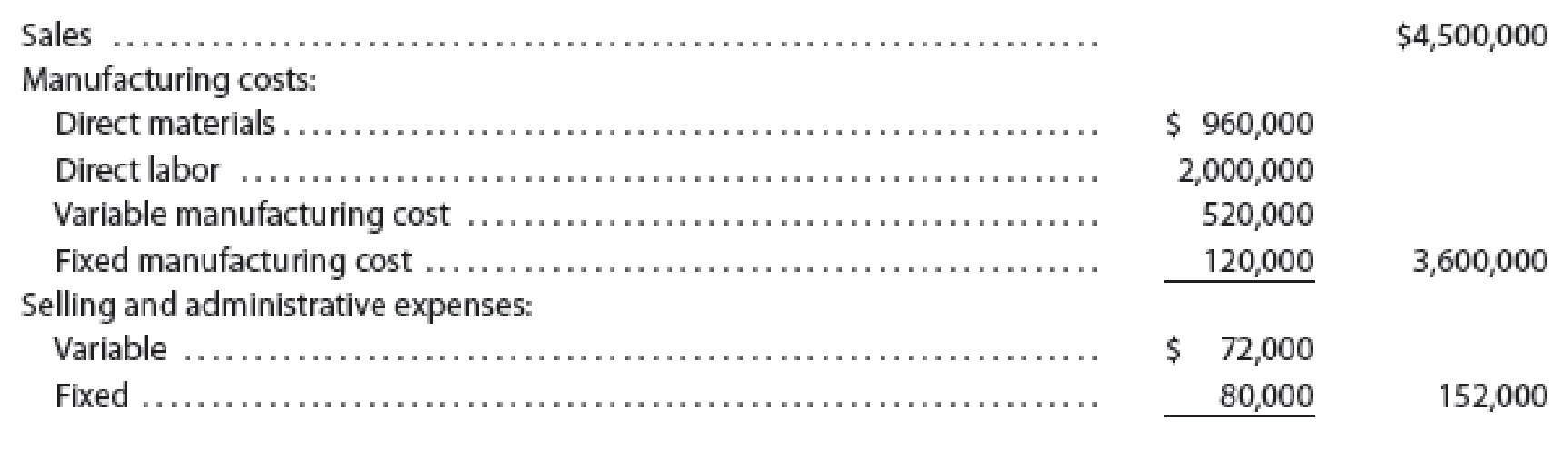

During the first month of operations ended May 31, Big Sky Creations Company produced 40,000 designer cowboy boots, of which 36,000 were sold. Operating data for the month are summarized as follows:

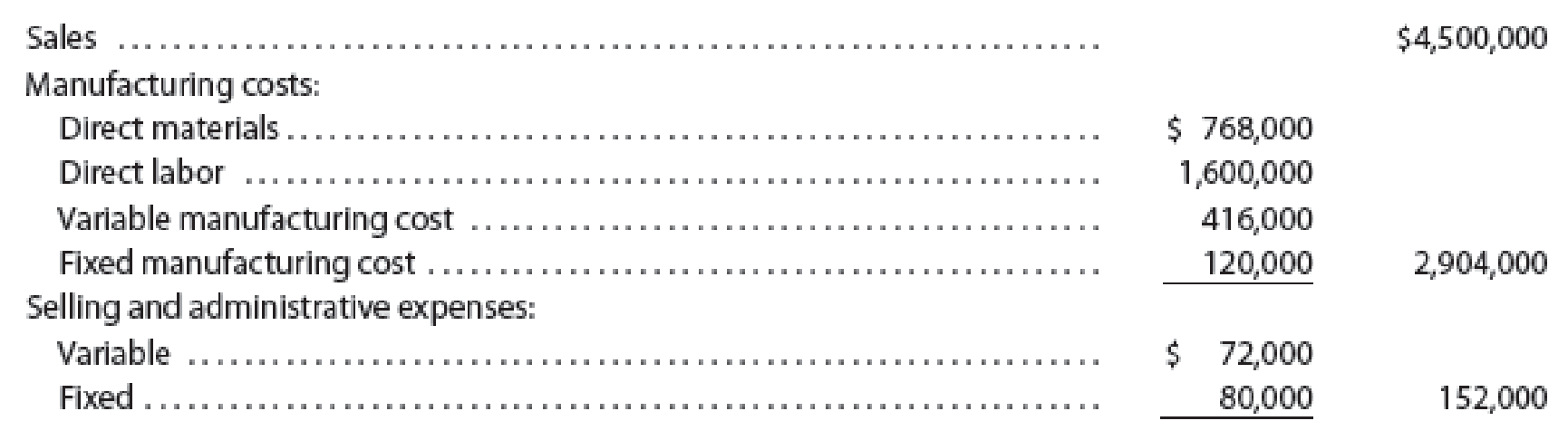

During June, Big Sky Creations produced 32,000 designer cowboy boots and sold 36,000 cowboy boots. Operating data for June are summarized as follows:

Instructions

1. Using the absorption costing concept, prepare income statements for (a) May and (b) June.

2. Using the variable costing concept, prepare income statements for (a) May and (b) June.

3. a. Explain the reason for the differences in operating income in (1) and (2) for May.

b. Explain the reason for the differences in operating income in (1) and (2) for June.

4. Based on your answers to (1) and (2), did Big Sky Creations Company operate more profitably in May or in June? Explain.

1.

Prepare an income statement according to the absorption costing concept for (a) May and (b) June.

Explanation of Solution

Absorption Costing

Absorption costing is compulsory under Generally Accepted Accounting Principles (GAAP) for financial statements circulated to the external users. Under absorption costing, the cost of goods manufactured includes direct materials, direct labor, and factory overhead costs. Fixed factory overhead and variable factory overhead are included as part of factory overhead.

(a)

Prepare an income statement according to the absorption costing concept for May.

| Company BSC | ||

| Absorption costing income statement | ||

| For the month ending May, 31 | ||

| Particulars | Amount ($) | Amount ($) |

| Sales | 4,500,000 | |

| Less: Cost of goods sold | ||

| Cost of goods manufactured | 3,600,000 | |

| Inventory on May, 31 (1) | (360,000) | |

| Total cost of goods sold | (3,240,000) | |

| Gross profit | 1,260,000 | |

| Less: Selling and administrative expenses | (152,000) | |

| Operating income | 1,108,000 | |

Table (1)

Working note (1):

Calculate the value of ending inventory, May 31.

(b)

Prepare an income statement according to the absorption costing concept for June.

| Company BSC | ||

| Absorption costing income statement | ||

| For the month ending June, 30 | ||

| Particulars | Amount ($) | Amount ($) |

| Sales | 4,500,000 | |

| Less: Cost of goods sold | ||

| Cost of goods manufactured | 2,904,000 | |

| Inventory on May, 31 (1) | 360,000 | |

| Total cost of goods sold | 3,264,000 | |

| Gross profit | 1,236,000 | |

| Less: Selling and administrative expenses | 152,000 | |

| Operating income | 1,084,000 | |

Table (2)

2.

Prepare an income statement according to the variable costing concept for (a) May and (b) June.

Explanation of Solution

Variable Costing

Managers frequently use variable costing for internal purposes for taking decision making. The cost of goods manufactured includes direct materials, direct labor, and variable factory overhead. Fixed factory overhead is treated as period (fixed) expense.

(a)

Prepare an income statement according to the variable costing concept for May.

| Company BSC | ||

| Variable costing income statement | ||

| For the month ending May, 31 | ||

| Particulars | Amount ($) | Amount ($) |

| Sales | 4,500,000 | |

| Less: Variable cost of goods sold | ||

| Variable cost of goods manufactured | 3,480,000 | |

| Inventory, May 31 (2) | (348,000) | |

| Total variable cost of goods sold | (3,132,000) | |

| Manufacturing margin | 1,368,000 | |

| Less: Variable selling and administrative expenses | (72,000) | |

| Contribution margin | 1,296,000 | |

| Less: Fixed costs | ||

| Fixed manufacturing costs | 120,000 | |

| Fixed selling and administrative expenses | 80,000 | |

| Total fixed cost | (200,000) | |

| Operating income | 1,096,000 | |

Table (3)

Working note (2):

Calculate the value of ending inventory, May 31.

(b)

Prepare an income statement according to the variable costing concept for June.

| Company BSC | ||

| Variable costing income statement | ||

| For the month ending June, 30 | ||

| Particulars | Amount ($) | Amount ($) |

| Sales | 4,500,000 | |

| Less: Variable cost of goods sold | ||

| Variable cost of goods manufactured | 2,784,000 | |

| Inventory on June 1 (1) | 348,000 | |

| Total variable cost of goods sold | 3,132,000 | |

| Manufacturing margin | 1,368,000 | |

| Less: Variable selling and administrative expenses | (72,000) | |

| Contribution margin | 1,296,000 | |

| Less: Fixed costs | ||

| Fixed manufacturing costs | 120,000 | |

| Fixed selling and administrative expenses | 80,000 | |

| Total fixed cost | (200,000) | |

| Operating income | 1,096,000 | |

Table (4)

3 (a)

Identify the reason for the difference between the amount of operating income reported in (1) and (2) for the month of May.

Explanation of Solution

The difference between the absorption and variable costing operating income of $12,000

Increase in inventory = 4,000 units

Fixed factory overhead per unit = $3

The operating income reported for the month of May under absorption costing exceeds the variable costing by $12,000. This difference exists under absorption costing, because $12,000 of fixed manufacturing costs is included in ending inventory of May under absorption costing, while entire fixed manufacturing costs is expensed in the month of May itself under variable costing.

3 (b)

Identify the reason for the difference between the amount of operating income reported in (1) and (2) for the month of June.

Explanation of Solution

The difference between the absorption and variable costing income from operations of $12,000

The operating income reported for the month of June under absorption costing is less than variable costing by $12,000. This difference exists under absorption costing, because $12,000 of fixed manufacturing costs is included in beginning inventory of June under absorption costing, while entire fixed manufacturing costs is expensed in the month of May itself under variable costing.

4.

Identify the month in which Company BSC operates more profitability, based on findings from (1) and (2).

Explanation of Solution

Based on variable costing concept, Company BSC was equally profitable in May and June. Sales and variable cost per unit were the same for both the month and under both concept. Only difference is allocation of $12,000 of fixed manufacturing cost to May 31 ending inventory under absorption costing.

Want to see more full solutions like this?

Chapter 7 Solutions

Managerial Accounting

- Fresno Industries Inc. manufactures and sells high-quality camping tents. The company began operations on January 1 and operated at 100% of capacity (150,000 units) during the first month, creating an ending inventory of 20,000 units. During February, the company produced 130,000 units during the month but sold 150,000 units at 500 per unit. The February manufacturing costs and selling and administrative expenses were as follows: a. Prepare an income statement according to the absorption costing concept for the month ending February 28. b. Prepare an income statement according to the variable costing concept for for the month ending February 28. c. What is the reason for the difference in the amount of operating income reported in (a) and (b)?arrow_forwardAbsorption and variable costing income statements During the first month of operations ended July 31, YoSan Inc. manufactured 2,400 flat panel televisions, of which 2,000 were sold. Operating data for the month are summarized as follows: Instructions 1. Prepare an income statement based on the absorption costing concept. 2. Prepare an income statement based on the variable costing concept. 3. Explain the reason for the difference in the amount of operating income reported in (1) and (2).arrow_forwardOn October 31, the end of the first month of operations, Maryville Equipment Company prepared the following income statement, based on the variable costing concept: Prepare an income statement under absorption costing.arrow_forward

- At the end of the first year of operations, 21,500 units remained in the finished goods inventory. The unit manufacturing costs during the year were as follows: Determine the cost of the finished goods inventory reported on the balance sheet under (a) the absorption costing concept and (b) the variable costing concept.arrow_forwardJellison Company had the following operating data for its first two years of operations: Jellison produced 90,000 units in the first year and sold 80,000. In the second year, it produced 80,000 units and sold 90,000 units. The selling price per unit each year was 12. Jellison uses an actual costing system for product costing. Required: 1. Prepare income statements for both years using absorption costing. Has firm performance, as measured by income, improved or declined from Year 1 to Year 2? 2. Prepare income statements for both years using variable costing. Has firm performance, as measured by income, improved or declined from Year 1 to Year 2? 3. Which method do you think most accurately measures firm performance? Why?arrow_forwardPattison Products, Inc., began operations in October and manufactured 40,000 units during the month with the following unit costs: Fixed overhead per unit = 280,000/40,000 units produced = 7. Total fixed factory overhead is 280,000 per month. During October, 38,400 units were sold at a price of 24, and fixed marketing and administrative expenses were 130,500. Required: 1. Calculate the cost of each unit using absorption costing. 2. How many units remain in ending inventory? What is the cost of ending inventory using absorption costing? 3. Prepare an absorption-costing income statement for Pattison Products, Inc., for the month of October. 4. What if November production was 40,000 units, costs were stable, and sales were 41,000 units? What is the cost of ending inventory? What is operating income for November?arrow_forward

- Using the information in the previous exercises about Marleys Manufacturing, determine the operating income for department B, assuming department A sold department B 1,000 units during the month and department A reduces the selling price to the market price.arrow_forwardThe following data were adapted from a recent income statement of Caterpillar Inc. (CAT) for the year ended December 31: Assume that 8,500 million of cost of goods sold and 4,000 million of selling, administrative, and other expenses were fixed costs. Inventories at the beginning and end of the year were as follows: Also, assume that 30% of the beginning and ending inventories were fixed costs. a. Prepare an income statement according to the variable costing concept for Caterpillar Inc. Round numbers to nearest million. b. Explain the difference between the amount of operating income reported under the absorption costing and variable costing concepts. Round numbers to nearest million.arrow_forwardDuring the week of May 10, Hyrum Manufacturing produced and shipped 16,000 units of its aluminum wheels: 4,000 units of Model A and 12,000 units of Model B. The cycle time for Model A is 1.09 hours and for Model B is 0.47 hour. The following costs and production hours were incurred: Required: 1. Assume that the value-stream costs and total units shipped apply only to one model (a single-product value stream). Calculate the unit cost, and comment on its accuracy. 2. Assume that Model A is responsible for 40% of the materials cost. Calculate the unit cost for Models A and B, and comment on its accuracy. Explain the rationale for using units shipped instead of units produced in the calculation. 3. Calculate the unit cost for the two models, using DBC. Explain when and why this cost is more accurate than the unit cost calculated in Requirement 2.arrow_forward

- During the week of August 21, Parley Manufacturing produced and shipped 4,000 units of its machine tools: 1,500 units of Tool SK1 and 2,500 units of Tool SK3. The cycle time for SK1 is 0.73 hour, and the cycle time for SK3 is 0.56 hour. The following costs were incurred: Required: 1. Assume that the value-stream costs and total units shipped apply only to one model (a single-product value stream). Calculate the unit cost, and comment on its accuracy. 2. Assume that Tool SK1 is responsible for 60% of the materials cost. Calculate the unit cost for Tool SK 1 and Tool SK3, and comment on its accuracy. Explain the rationale for using units shipped instead of units produced in the calculation. 3. Calculate the unit cost for the two models, using DBC. Explain when and why this cost is more accurate than the unit cost calculated in Requirement 2.arrow_forwardThe cost accountant for River Rock Beverage Co. estimated that total factory overhead cost for the Blending Department for the coming fiscal year beginning February 1 would be 3,150,000, and total direct labor costs would be 1,800,000. During February, the actual direct labor cost totalled 160,000, and factory overhead cost incurred totaled 283,900. a. What is the predetermined factory overhead rate based on direct labor cost? b. Journalize the entry to apply factory overhead to production for February. c. What is the February 28 balance of the account Factory OverheadBlending Department? d. Does the balance in part (c) represent over- or underapplied factory overhead?arrow_forwardIncome Statements under Absorption and Variable Costing In the coming year, Kalling Company expects to sell 28,700 units at 32 each. Kallings controller provided the following information for the coming year: Required: 1. Calculate the cost of one unit of product under absorption costing. 2. Calculate the cost of one unit of product under variable costing. 3. Calculate operating income under absorption costing for next year. 4. Calculate operating income under variable costing for next year.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College