Videos

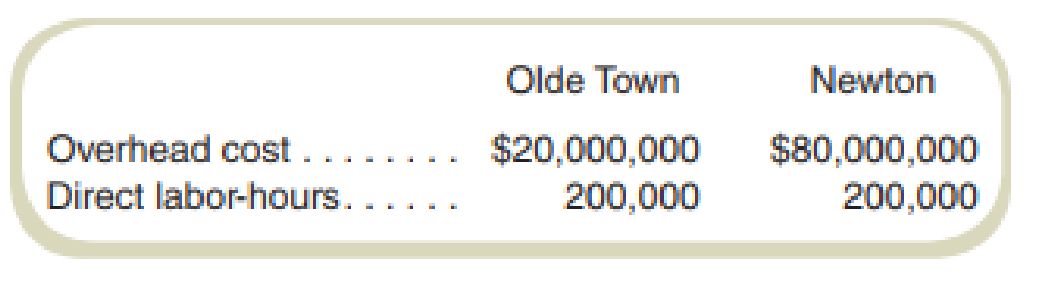

Old Port Shipyards does work for both the U.S. Navy and private shipping companies. Old Port’s major business is renovating ships, which it does at one of two company dry docks referred to by the names of the local towns: Olde Town and Newton.

Data on operations and costs for the two dry docks follow:

Virtually all dry dock costs consist of

Old Port is about to start two jobs, one for the Navy under a cost-plus contract and one for a private shipping company for a fixed fee. Both jobs will require the same number of hours. You have been asked to prepare some costing information. Your supervisor tells you that she is sure the Navy job will be done at Newton and the private job will be done at Olde Town.

Required

- a. Compute the overhead rate at the two shipyards.

- b. Why do you think your supervisor says that the Navy job will be done at Newton?

- c. Is the choice of the production location ethical? Why?

Want to see the full answer?

Check out a sample textbook solution

Chapter 7 Solutions

Gen Combo Fundamentals Of Cost Accounting; Connect Access Card

- Hicks Contracting collects and analyzes cost data in order to track the cost of installing decks on new home construction jobs. The following are some of the costs that they incur. Classify these costs as fixed or variable costs and as product or period costs. Lumber used to construct decks ($12.00 per square foot) Carpenter labor used to construct decks ($10 per hour) Construction supervisor salary ($45,000 per year) Depreciation on tools and equipment ($6,000 per year) Selling and administrative expenses ($35,000 per year) Rent on corporate office space ($34,000 per year) Nails, glue, and other materials required to construct deck (varies per job)arrow_forwardCommunications Jamarcus Bradshaw, plant manager of Georgia Paper Companys papermaking mill, was looking over the cost of production reports for July and August for the Papermaking Department. The reports revealed the following: Jamarcus was concerned about the increased cost per ton from the output of the department. As a result, he asked the plant controller to perform a study to help explain these results. The controller, Leann Brunswick, began the analysis by performing some interviews of key plant personnel in order to understand what the problem might be. Excerpts from an interview with Len Tyson, a paper machine operator, follow: Len: We have two papermaking machines in the department. I have no data, but I think paper machine No. 1 is applying too much pulp and, thus, is wasting both conversion and materials resources. We haven't had repairs on paper machine No. 1 in a while. Maybe this is the problem. Leann: How does too much pulp result in wasted resources? Len: Well, you see, if too much pulp is applied, then we will waste pulp material. The customer will not pay for the extra product; we just use more material to make the product. Also, when there is too much pulp, the machine must be slowed down in order to complete the drying process. This results in additional conversion costs. Leann: Do you have any other suspicions? Len: Well, as you know, we have two productsgreen paper and yellow paper. They are identical except for the color. The color is added to the papermaking process in the paper machine. I think that during August these two color papers have been behaving very differently. I don't have any data, but it just seems as though the amount of waste associated with the green paper has increased. Leann: Why is this? Len: I understand that there has been a change in specifications for the green paper, starting near the beginning of August. This change could be causing the machines to run poorly when making green paper. If this is the case, the cost per ton would increase for green paper. Leann also asked for a database printout providing greater detail on Augusts operating results. September 9 Requested by: Leann Brunswick Papermaking DepartmentAugust detail Prior to preparing a report, Leann resigned from Georgia Paper Company to start her own business. You have been asked to take the data that Leann collected, and write a memo to Jamarcus Bradshaw with a recommendation to management. Your memo should include analysis of the August data to determine whether the paper machine or the paper color explains the increase in the unit cost from July. Include any supporting schedules that are appropriate. Round any calculations to the nearest cent.arrow_forwardHicks Contracting collects and analyzes cost data in order to track the cost of installing decks on new home construction jobs. The following are some of the costs that they incur. Classify these costs as fixed or variable costs and as product or period costs. A. Lumber used to construct decks ($12.00 per square foot) B. Carpenter labor used to construct decks ($10 per hour) C. Construction supervisor salary ($45,000 per year) D. Depreciation on tools and equipment ($6,000 per year) E. Selling and administrative expenses ($35,000 per year) F. Rent on corporate office space ($34,000 per year) G. Nails, glue, and other materials required to construct deck (varies per job)arrow_forward

- Nizam Company produces speaker cabinets. Recently, Nizam switched from a traditional departmental assembly line system to a manufacturing cell in order to produce the cabinets. Sup-pose that the cabinet manufacturing cell is the cost object. Assume that all or a portion of the following costs must be assigned to the cell:a. Depreciation on electric saws, sanders, and drills used to produce the cabinetsb. Power to heat and cool the plant in which the cell is locatedc. Salary of cell supervisord. Wood used to produce the cabinet housingse. Maintenance for the cell’s equipment (provided by the maintenance department)f. Labor used to cut the wood and to assemble the cabinetsg. Replacement sanding beltsh. Cost of janitorial services for the planti. Ordering costs for materials used in productionj. The salary of the industrial engineer (she spends about 20 percent of her time on work forthe cell)k. Cost of maintaining plant and grounds l. Cost of plant’s personnel officem. Depreciation on…arrow_forwardAssigning Direct Labor Costs to Jobs TAC Industries Inc. sells heavy equipment to large corporations and federal, state, and local governments. Corporate sales are the result of a competitive bidding process, where TAC competes against other companies based on selling price. Sales to the government, however, are determined on a cost plus basis, where the selling price is determined by adding a fixed markup percentage to the total job cost. Tandy Lane is the cost accountant for the Equipment Division of TAC Industries Inc. The division is under pressure from senior management to improve operating income. As Tandy reviewed the division’s job cost sheets, she realized that she could increase the division’s operating income by moving a portion of the direct labor hours that had been assigned to the job cost sheets of corporate customers onto the job order costs sheets of government customers. She believed that this would create a “win–win” for the division by (1) reducing the cost of…arrow_forwardElizabeth Flanigan and Associates is an engineering and design firm that specializes in developing plans for recycling plants for municipalities. The firm uses a job costing system to accumlate the cost associated with each design project. Flanigan employs three levels of employee: senior engineers, associate engineers, and clerical staff. The salary cost of the clerical staff is included in overhead, along with the cost of engineering supplies, automobile travel, and equipment depreciation. The cost of airline travel, motels, building permits, and fees from other consultants is charged to each project as direct materials. Overhead is applied to projects using a predetermined overhead rate based on total engineering hours. The rate for 20X0 is $5 per hour. The six different salary levels for 20X1 for the employees of Elizabeth Flanigan and Associates are listed below. The hourly rate is determined by dividing the yearly salary by 2,000 hours per year. Senior engineer Level 1:…arrow_forward

- Benchmarking, ethics. Amanda McNall is the corporate controller of Scott Quarry. Scott Quarry operates 12 rock-crushing plants in Scott County, Kentucky, that process huge chunks of limestone rock extracted from underground mines. Given the competitive landscape for pricing, Scott’s managers pay close attention to costs. Each plant uses a process-costing system, and at the end of every quarter, each plant manager submits a production report and a production-cost report. The production report includes the plant manager’s estimate of the percentage of completion of the ending work in process as to direct materials and conversion costs, as well as the level of processed limestone inventory. McNall uses these estimates to compute the cost per equivalent unit of work done for each input for the quarter. Plants are ranked from 1 to 12, and the three plants with the lowest cost per equivalent unit for direct materials and conversion costs are each given a bonus and recognized in the company…arrow_forwardBenchmarking, ethics. Amanda McNall is the corporate controller of Scott Quarry. Scott Quarry operates 12 rock-crushing plants in Scott County, Kentucky, that process huge chunks of limestone rock extracted from underground mines. Given the competitive landscape for pricing, Scott’s managers pay close attention to costs. Each plant uses a process-costing system, and at the end of every quarter, each plant manager submits a production report and a production-cost report. The production report includes the plant manager’s estimate of the percentage of completion of the ending work in process as to direct materials and conversion costs, as well as the level of processed limestone inventory. McNall uses these estimates to compute the cost per equivalent unit of work done for each input for the quarter. Plants are ranked from 1 to 12, and the three plants with the lowest cost per equivalent unit for direct materials and conversion costs are each given a bonus and recognized in the company…arrow_forwardBenchmarking, ethics. Amanda McNall is the corporate controller of Scott Quarry. Scott Quarry operates 12 rock-crushing plants in Scott County, Kentucky, that process huge chunks of limestone rock extracted from underground mines. Given the competitive landscape for pricing, Scott’s managers pay close attention to costs. Each plant uses a process-costing system, and at the end of every quarter, each plant manager submits a production report and a production-cost report. The production report includes the plant manager’s estimate of the percentage of completion of the ending work in process as to direct materials and conversion costs, as well as the level of processed limestone inventory. McNall uses these estimates to compute the cost per equivalent unit of work done for each input for the quarter. Plants are ranked from 1 to 12, and the three plants with the lowest cost per equivalent unit for direct materials and conversion costs are each given a bonus and recognized in the company…arrow_forward

- Classifying Costs as Materials, Labor, or Factory Overhead Indicate whether the following costs of Procter & Gamble (PG), a maker of consumer products, would be classified as direct materials cost, direct labor cost, or factory overhead cost: Cost Classification a. Depreciation on assembly line equipment in the Mehoopany, Pennsylvania, paper products plant b. Licensing payments for use of Disney characters on children products c. Maintenance supplies d. Packaging materials e. Paper used in bath tissue f. Plant manager salary for the Iowa City, Iowa, plant g. Resins for body wash products h. Salary of process engineers i. Scents and fragrances used in making soaps and detergents j. Wages of production line employees at the Pineville, Louisiana, soap and detergent plantarrow_forwardQUESTION 1. The Interiors Company located in Dominica, manufactures executive desks. Selected costs associated with the manufacture of the executive desks and the general operations of the company are given below: a) Wood used in the manufacture of the executive desks, at a cost of $500 per desk. b) The executive desks are assembled by workers, at a cost of $100 per desk. c) Workers assembling the executive desks are supervised by a factory supervisor who is paid $75,000 per year. d) Electrical cost of $50 per machine-hour are incurred in the factory in the manufacture of the executive desks (five machine hours are required to produce a desk). e) The depreciation cost of the machines used in the manufacture of the executive desks totals $5,000 per year. f) The salary of the president of the Company is $250,000 per year. g) The Company spends $100,000 per year to advertise its products. h) Salespersons are paid a commission of $80 for each desk sold.Questions:…arrow_forwardArklan Production is upgrading its manufacturing process from a manual process to a highly automated system. Management believes that the new system will result in greater efficiencies and a better finished product. Arklan is also working on a plan to downsize staff after the implementation of the new system. Arklan has used a traditional absorption costing system to calculate unit product costs for external financial reporting. In the past, Arklan has allocated its manufacturing overhead costs using a predetermined plant-wide overhead rate based on direct labor hours. The controller realizes that the new system may require changing the overhead allocation process. Management plans to take the opportunity to reconsider other improvements to the costing system. Identify and explain three benefits of using departmental overhead rates to allocate overhead costs. Explain the difference between absorption costing and variable costing. Identify which is more suitable for internal…arrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning