HORNGRENS COST ACCOUNTING CUSTOM FOR UC

null Edition

ISBN: 9780136696667

Author: Datar

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 7, Problem 7.43P

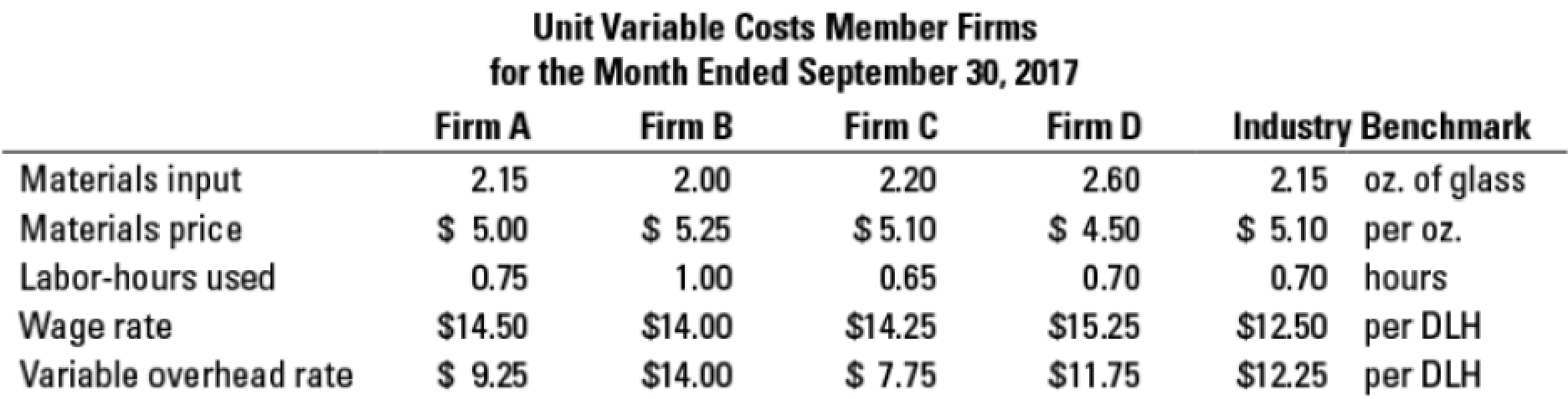

Use of materials and manufacturing labor variances for benchmarking. You are a new junior accountant at In Focus Corporation, maker of lenses for eyeglasses. Your company sells generic-quality lenses for a moderate price. Your boss, the controller, has given you the latest month’s report for the lens trade association. This report includes information related to operations for your firm and three of your competitors within the trade association. The report also includes information related to the industry benchmark for each line item in the report. You do not know which firm is which, except that you know you are Firm A.

- 1. Calculate the total variable cost per unit for each firm in the trade association. Compute the percent of total for the material, labor, and variable

overhead components. - 2. Using the trade association’s industry benchmark, calculate direct materials and direct manufacturing labor price and efficiency variances for the four firms. Calculate the percent over standard for each firm and each variance.

- 3. Write a brief memo to your boss outlining the advantages and disadvantages of belonging to this trade association for benchmarking purposes. Include a few ideas to improve productivity that you want your boss to take to the department heads’ meeting.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Use of materials and manufacturing labor variances for benchmarking. You are a new junior accountant at In Focus Corporation, maker of lenses for eyeglasses. Your company sells generic-quality lenses for a moderate price. Your boss, the controller, has given you the latest month’s report for the lens trade association. This report includes information related to operations for your rm and three of your competitors within the trade association. The report also includes information related to the industry benchmark for each line item in the report. You do not know which rm is which, except that you know you are Firm A.

Computing standard cost variances and reporting to management

Hear Smart manufactures headphone cases. During September 2018, the company produced and sold 105,000 cases and recorded the following cost data:

Requirements

Compute the cost and efficiency variances for direct materials and direct labor.

For manufacturing overhead, compute the variable overhead cost and efficiency variances and the fixed overhead cost and volume variances.

Hear Smarts management used better quality materials during September. Discuss the trade-off between the two direct material variances.

Computing standard cost variances and reporting to management

Headset manufactures headphone cases. During September 2018, the company produced 106,000 cases and recorded the following cost data:

Requirements

Compute the cost and efficiency variances for direct materials and direct labor.

For manufacturing overhead, compute the variable overhead cost and efficiency variances and the fixed overhead cost and volume variances.

Headset’s management used better-quality materials during September. Discuss the trade-off between the two direct material variances.

Chapter 7 Solutions

HORNGRENS COST ACCOUNTING CUSTOM FOR UC

Ch. 7 - What is the relationship between management by...Ch. 7 - What are two possible sources of information a...Ch. 7 - Distinguish between a favorable variance and an...Ch. 7 - What is the key difference between a static budget...Ch. 7 - Why might managers find a flexible-budget analysis...Ch. 7 - Describe the steps in developing a flexible...Ch. 7 - List four reasons for using standard costs.Ch. 7 - How might a manager gain insight into the causes...Ch. 7 - List three causes of a favorable direct materials...Ch. 7 - Describe three reasons for an unfavorable direct...

Ch. 7 - How does variance analysis help in continuous...Ch. 7 - Why might an analyst examining variances in the...Ch. 7 - Prob. 7.13QCh. 7 - When inputs are substitutable, how can the direct...Ch. 7 - Benchmarking against other companies enables a...Ch. 7 - Metal Shelf Companys standard cost for raw...Ch. 7 - All of the following statements regarding...Ch. 7 - Amalgamated Manipulation Manufacturings (AMM)...Ch. 7 - Atlantic Company has a manufacturing facility in...Ch. 7 - Basix Inc. calculates direct manufacturing labor...Ch. 7 - Flexible budget. Sweeney Enterprises manufactures...Ch. 7 - Flexible budget. Bryant Companys budgeted prices...Ch. 7 - Flexible-budget preparation and analysis. Bank...Ch. 7 - Flexible budget, working backward. The Clarkson...Ch. 7 - Flexible-budget and sales volume variances....Ch. 7 - Price and efficiency variances. Sunshine Foods...Ch. 7 - Materials and manufacturing labor variances....Ch. 7 - Direct materials and direct manufacturing labor...Ch. 7 - Price and efficiency variances, journal entries....Ch. 7 - Materials and manufacturing labor variances,...Ch. 7 - Journal entries and T-accounts (continuation of...Ch. 7 - Price and efficiency variances, benchmarking....Ch. 7 - Static and flexible budgets, service sector....Ch. 7 - Flexible budget, direct materials, and direct...Ch. 7 - Variance analysis, nonmanufacturing setting. Joyce...Ch. 7 - Comprehensive variance analysis review. Ellis...Ch. 7 - Possible causes for price and efficiency...Ch. 7 - Material-cost variances, use of variances for...Ch. 7 - Direct manufacturing labor and direct materials...Ch. 7 - Direct materials efficiency, mix, and yield...Ch. 7 - Direct materials and manufacturing labor...Ch. 7 - Direct materials and manufacturing labor...Ch. 7 - Use of materials and manufacturing labor variances...Ch. 7 - Direct manufacturing labor variances: price,...Ch. 7 - Direct-cost and selling price variances. MicroDisk...Ch. 7 - Variances in the service sector. Derek Wilson...Ch. 7 - Prob. 7.47P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Sommers Company uses the following rule to determine whether materials usage variances should be investigated: A materials usage variance will be investigated anytime the amount exceeds the lesser of 12,000 or 10% of the standard cost. Reports for the past 5 weeks provided the following information: Required: 1. Using the rule provided, identify the cases that will be investigated. 2. CONCEPTUAL CONNECTION Suppose investigation reveals that the cause of an unfavorable materials usage variance is the use of lower-quality materials than are normally used. Who is responsible? What corrective action would likely be taken? 3. CONCEPTUAL CONNECTION Suppose investigation reveals that the cause of a significant unfavorable materials usage variance is attributable to a new approach to manufacturing that takes less labor time but causes more material waste. Examination of the labor efficiency variance reveals that it is favorable and larger than the unfavorable materials usage variance. Who is responsible? What action should be taken?arrow_forwardRefer to the information for Cinturon Corporation on the previous page. Required: 1. Break down the total variance for labor into a rate variance and an efficiency variance using the columnar and formula approaches. 2. CONCEPTUAL CONNECTION As part of the investigation of the unfavorable variances, the plant manager interviews the production manager. The production manager complains strongly about the quality of the leather strips. He indicates that the strips are of lower quality than usual and that workers have to be more careful to avoid a belt with cracks and more time is required. Also, even with extra care, many belts have to be discarded and new ones produced to replace the rejects. This replacement work has also produced some overtime demands. What corrective action should the plant manager take?arrow_forwardThe management of Golding Company has determined that the cost to investigate a variance produced by its standard cost system ranges from 2,000 to 3,000. If a problem is discovered, the average benefit from taking corrective action usually outweighs the cost of investigation. Past experience from the investigation of variances has revealed that corrective action is rarely needed for deviations within 8% of the standard cost. Golding produces a single product, which has the following standards for materials and labor: Actual production for the past 3 months follows, with the associated actual usage and costs for materials and labor. There were no beginning or ending raw materials inventories. Required: 1. What upper and lower control limits would you use for materials variances? For labor variances? 2. Compute the materials and labor variances for April, May, and June. Identify those that would require investigation by comparing each variance to the amount of the limit computed in Requirement 1. Compute the actual percentage deviation from standard. Round all unit costs to four decimal places. Round variances to the nearest dollar. Round variance rates to three decimal places so that percentages will show to one decimal place. 3. CONCEPTUAL CONNECTION Let the horizontal axis be time and the vertical axis be variances measured as a percentage deviation from standard. Draw horizontal lines that identify upper and lower control limits. Plot the labor and material variances for April, May, and June. Prepare a separate graph for each type of variance. Explain how you would use these graphs (called control charts) to assist your analysis of variances.arrow_forward

- Cost and production data for Binghamton Beverages Inc. are presented as follows: Required: Calculate net variances for materials, labor, and factory overhead. Calculate specific materials and labor variances by department, using the diagram format in Figure 8-4. Comment on the possible causes for each of the variances that you computed. Make all journal entries to record production costs in Work in Process and Finished Goods. Determine the balance of ending Work in Process in each department. Assume that 4,000 units were sold at $40 each. Calculate the gross margin based on standard cost. Calculate the gross margin based on actual cost. Why does the gross margin at actual cost differ from the gross margin at standard cost. As the plant controller, you present the variance report in Item 1 above to Paul Crooke, the plant manager. After reading it, Paul states: “If we present this performance report to corporate with that large unfavorable labor variance in Blending, nobody in the plant will receive a bonus. Those standard hours of 5,500 are way too tight for this production process. Fifty-eight hundred hours would be more reasonable, and that would result in a favorable labor efficiency variance that would more than offset the unfavorable labor rate variance. Please redo the variance calculations using 5,800 hours as the standard.” You object, but Paul ends the conversation with, “That is an order.” What standards of ethical professional practice would be violated if you adhered to Paul’s order? How would you attempt to resolve this ethical conflict?arrow_forwardMaking journal entries Assume that during the month of April the production report of Algonquin Adhesives Inc. in E8-10 revealed the following information: Make journal entries to charge materials (use the materials purchase price variance) and labor to Work in Process. (Remember to retrieve the standard costs from E8-10 before solving this exercise.)arrow_forwardEd Co. manufactures two types of O rings, large and small. Both rings use the same material but require different amounts. Standard materials for both are shown. At the beginning of the month, Edve Co. bought 25,000 feet of rubber for $6.875. The company made 3,000 large O rings and 4,000 small O rings. The company used 14,500 feet of rubber. A. What are the direct materials price variance, the direct materials quantity variance, and the total direct materials cost variance? B. If they bought 10,000 connectors costing $310, what would the direct materials price variance be for the connectors? C. If there was an unfavorable direct materials price variance of $125, how much did they pay per toot for the rubber?arrow_forward

- As part of its cost control program, Tracer Company uses a standard costing system for all manufactured items. The standard cost for each item is established at the beginning of the fiscal year, and the standards are not revised until the beginning of the next fiscal year. Changes in costs, caused during the year by changes in direct materials or direct labor inputs or by changes in the manufacturing process, are recognized as they occur by the inclusion of planned variances in Tracers monthly operating budgets. The following direct labor standard was established for one of Tracers products, effective June 1, 2012, the beginning of the fiscal year: The standard was based on the direct labor being performed by a team consisting of five persons with Assembler A skills, three persons with Assembler B skills, and two persons with machinist skills; this team represents the most efficient use of the companys skilled employees. The standard also assumed that the quality of direct materials that had been used in prior years would be available for the coming year. For the first seven months of the fiscal year, actual manufacturing costs at Tracer have been within the standards established. However, the company has received a significant increase in orders, and there is an insufficient number of skilled workers to meet the increased production. Therefore, beginning in January, the production teams will consist of eight persons with Assembler A skills, one person with Assembler B skills, and one person with machinist skills. The reorganized teams will work more slowly than the normal teams, and as a result, only 80 units will be produced in the same time period in which 100 units would normally be produced. Faulty work has never been a cause for units to be rejected in the final inspection process, and it is not expected to be a cause for rejection with the reorganized teams. Furthermore, Tracer has been notified by its direct materials supplier that lower-quality direct materials will be supplied beginning January 1. Normally, one unit of direct materials is required for each good unit produced, and no units are lost due to defective direct materials. Tracer estimates that 6 percent of the units manufactured after January 1 will be rejected in the final inspection process due to defective direct materials. Required: 1. Determine the number of units of lower quality direct materials that Tracer Company must enter into production in order to produce 47,000 good finished units. 2. How many hours of each class of direct labor must be used to manufacture 47,000 good finished units? 3. Determine the amount that should be included in Tracers January operating budget for the planned direct labor variance caused by the reorganization of the direct labor teams and the lower quality direct materials. (CMA adapted)arrow_forwardEthics in Action In August, Lannister Company introduced a new performance measurement system in manufacturing operations. One of the new performance measures is lead time, which is determined by tagging a random sample of items with a log sheet throughout the month. The log sheets recorded the time that the sample items started production and the time that they ended production, as well as all steps in between. At the end of the month, the controller collected the log sheets and computed the average lead time of the tagged products. This number was reported to central management and was used to evaluate the performance of the plant manager. Because of the poor lead time results reported for August, the plant was under extreme pressure to reduce lead time in September. The following memo was intercepted by the controller. Date: September 3 To: Hourly Employees From: Plant Manager During last month, you may have noticed that some of the products were tagged with a log sheet. This sheet records the time that a product enters production and the time that it leaves production. The difference between these two times is termed the lead time. Our plant is evaluated on improving lead time. From now on, I ask all of you to keep an eye out for the tagged items. When you see a tagged item, it is to receive special attention. Work on that item first, and then immediately move it to the next operation. Under no circumstances should tagged items wait on any other work that you have. Naturally, report accurate information. I insist that you record the correct times on the log sheet as the product goes through your operations. How should the controller respond to this discovery?arrow_forwardWarner Company has the following data for the past year: Warner uses the overhead control account to accumulate both actual and applied overhead. Required: 1. Calculate the overhead variance for the year and close it to cost of goods sold. 2. Assume the variance calculated is material. After prorating, close the variances to the appropriate accounts and provide the final ending balances of these accounts. 3. What if the variance is of the opposite sign calculated in Requirement 1? Provide the appropriate adjusting journal entries for Requirements 1 and 2.arrow_forward

- Using variance analysis and interpretation Last year, Wrigley Corp. adopted a standard cost system. Labor standards were set on the basis of time studies and prevailing wage rates. Materials standards were determined from materials specifications and the prices then in effect. On June 30, the end of the current fiscal year, a partial trial balance revealed the following: Standards set at the beginning of the year have remained unchanged. All inventories are priced at standard cost. What conclusions can be drawn from each of the four variances shown in Wrigleys trial balance?arrow_forwardJameson Company produces paper towels. The company has established the following direct materials and direct labor standards for one case of paper towels: During the first quarter of the year, Jameson produced 45,000 cases of paper towels. The company purchased and used 135,700 pounds of paper pulp at 0.38 per pound. Actual direct labor used was 91,000 hours at 12.10 per hour. Required: 1. Calculate the direct materials price and usage variances. 2. Calculate the direct labor rate and efficiency variances. 3. Prepare the journal entries for the direct materials and direct labor variances. 4. Describe how flexible budgeting variances relate to the direct materials and direct labor variances computed in Requirements 1 and 2.arrow_forwardPotter Company has installed a JIT purchasing and manufacturing system and is using back-flush accounting for its cost flows. It currently uses a two-trigger approach with the purchase of materials as the first trigger point and the completion of goods as the second trigger point. During the month of June, Potter had the following transactions: There were no beginning or ending inventories. All goods produced were sold with a 60 percent markup. Any variance is closed to Cost of Goods Sold. (Variances are recognized monthly.) Required: 1. Prepare the journal entries that would have been made using a traditional accounting approach for cost flows. 2. Prepare the journal entries for the month using backflush costing.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Excel Applications for Accounting Principles

Accounting

ISBN:9781111581565

Author:Gaylord N. Smith

Publisher:Cengage Learning

What is variance analysis?; Author: Corporate finance institute;https://www.youtube.com/watch?v=SMTa1lZu7Qw;License: Standard YouTube License, CC-BY