Principles of Cost Accounting

17th Edition

ISBN: 9781305087408

Author: Edward J. Vanderbeck, Maria R. Mitchell

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 7, Problem 9E

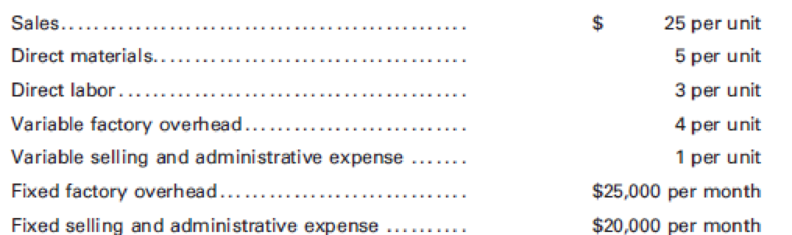

Cortez Manufacturing, Inc. has the following flexible budget formulas and amounts:

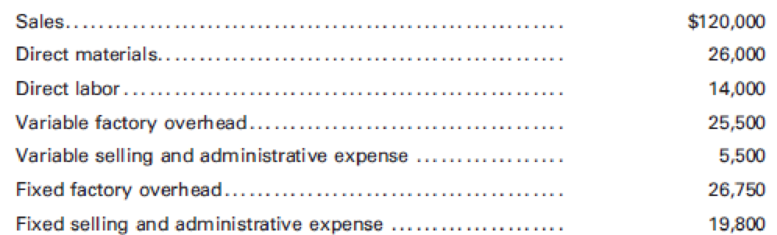

Actual results for May for the production and sale of 5,000 units were as follows:

Prepare a performance report for May that includes the identification of the favorable and unfavorable variances.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Chapter 7 Solutions

Principles of Cost Accounting

Ch. 7 - Prob. 1QCh. 7 - Prob. 2QCh. 7 - Prob. 3QCh. 7 - Prob. 4QCh. 7 - Explain zero-based budgeting and how it differs...Ch. 7 - Prob. 6QCh. 7 - Which operating budget must be prepared before the...Ch. 7 - Prob. 8QCh. 7 - Why is it important to have front-line managers...Ch. 7 - If the sales forecast estimates that 50,000 units...

Ch. 7 - What are the advantages and disadvantages of each...Ch. 7 - What three operating budgets can be prepared...Ch. 7 - Prob. 13QCh. 7 - What are the three budgets that are needed in...Ch. 7 - Why might Web-based budgeting be more useful than...Ch. 7 - What is a flexible budget?Ch. 7 - Why is a flexible budget better than a master...Ch. 7 - Why is it important to distinguish between...Ch. 7 - Why is the concept of relevant range important...Ch. 7 - In comparing actual sales revenue to flexible...Ch. 7 - How would you define the following? a. Theoretical...Ch. 7 - Is it possible for a factory to operate at more...Ch. 7 - If a factory operates at 100% of capacity one...Ch. 7 - How is the standard cost per unit for factory...Ch. 7 - When allocating service department costs to...Ch. 7 - The sales department of Macro Manufacturing Co....Ch. 7 - The sales department of F. Pollard Manufacturing...Ch. 7 - Barnes Manufacturing Co. forecast October sales to...Ch. 7 - Prepare a cost of goods sold budget for the Crest...Ch. 7 - Prepare a cost of goods sold budget for MacLaren...Ch. 7 - Roman Inc. has the following totals from its...Ch. 7 - Starburst Inc. has the following items and amounts...Ch. 7 - Using the following per-unit and total amounts,...Ch. 7 - Cortez Manufacturing, Inc. has the following...Ch. 7 - Prob. 10ECh. 7 - Prob. 11ECh. 7 - Prob. 12ECh. 7 - Prob. 13ECh. 7 - Calculating factory overhead The normal capacity...Ch. 7 - The Sales Department of Minimus Inc. has forecast...Ch. 7 - Sales, production, direct materials, direct labor,...Ch. 7 - Budgeted selling and administrative expenses for...Ch. 7 - Prob. 4PCh. 7 - Selling and administrative expense budget and...Ch. 7 - Preparing a flexible budget Use the information in...Ch. 7 - Preparing a performance report Use the flexible...Ch. 7 - Preparing a performance report Use the flexible...Ch. 7 - Flexible budget for factory overhead Presented...Ch. 7 - Prob. 10PCh. 7 - Overhead application rate Creole Manufacturing...Ch. 7 - Overhead application rate Roll Tide Manufacturing...Ch. 7 - Flexible budgeting, performance measurement, and...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Marten Company has a cost-benefit policy to investigate any variance that is greater than 1,000 or 10% of budget, whichever is larger. Actual results for the previous month indicate the following: The company should investigate: a. neither the materials variance nor the labor variance. b. the materials variance only. c. the labor variance only. d. both the materials variance and the labor variance.arrow_forwardThe normal capacity of a manufacturing plant is 30,000 direct labor hours or 20,000 units per month. Standard fixed costs are 6,000, and variable costs are 12,000. Data for two months follow: For each month, make a single journal entry to charge overhead to Work in Process, to close Factory Overhead, and to record variances. Indicate the types of variances and state whether each is favorable or unfavorable. (Hint: You must first compute the flexible-budget and production-volume variances.)arrow_forwardFargo Co. manufactures products in batches of 100 units per batch. The company uses a standard cost system and prepares budgets that call for 500 of these batches per period. Budgeted fixed overhead is $60,000 per period. The standard costs per batch follow: During the period, 503 batches were manufactured, and the following costs were incurred: Required: Calculate the variances for materials, labor, and overhead. For overhead, use the two-variance method. (Hint: Please use the information given about the budgeted fixed overhead to compute the variable overhead rate.)arrow_forward

- Kavallia Company set a standard cost for one item at 328,000; allowable deviation is 14,500. Actual costs for the past six months are as follows: Required: 1. Calculate the variance from standard for each month. Which months should be investigated? 2. What if the company uses a two-part rule for investigating variances? The allowable deviation is the lesser of 4 percent of the standard amount or 14,500. Now which months should be investigated?arrow_forwardAs part of its cost control program, Tracer Company uses a standard costing system for all manufactured items. The standard cost for each item is established at the beginning of the fiscal year, and the standards are not revised until the beginning of the next fiscal year. Changes in costs, caused during the year by changes in direct materials or direct labor inputs or by changes in the manufacturing process, are recognized as they occur by the inclusion of planned variances in Tracers monthly operating budgets. The following direct labor standard was established for one of Tracers products, effective June 1, 2012, the beginning of the fiscal year: The standard was based on the direct labor being performed by a team consisting of five persons with Assembler A skills, three persons with Assembler B skills, and two persons with machinist skills; this team represents the most efficient use of the companys skilled employees. The standard also assumed that the quality of direct materials that had been used in prior years would be available for the coming year. For the first seven months of the fiscal year, actual manufacturing costs at Tracer have been within the standards established. However, the company has received a significant increase in orders, and there is an insufficient number of skilled workers to meet the increased production. Therefore, beginning in January, the production teams will consist of eight persons with Assembler A skills, one person with Assembler B skills, and one person with machinist skills. The reorganized teams will work more slowly than the normal teams, and as a result, only 80 units will be produced in the same time period in which 100 units would normally be produced. Faulty work has never been a cause for units to be rejected in the final inspection process, and it is not expected to be a cause for rejection with the reorganized teams. Furthermore, Tracer has been notified by its direct materials supplier that lower-quality direct materials will be supplied beginning January 1. Normally, one unit of direct materials is required for each good unit produced, and no units are lost due to defective direct materials. Tracer estimates that 6 percent of the units manufactured after January 1 will be rejected in the final inspection process due to defective direct materials. Required: 1. Determine the number of units of lower quality direct materials that Tracer Company must enter into production in order to produce 47,000 good finished units. 2. How many hours of each class of direct labor must be used to manufacture 47,000 good finished units? 3. Determine the amount that should be included in Tracers January operating budget for the planned direct labor variance caused by the reorganization of the direct labor teams and the lower quality direct materials. (CMA adapted)arrow_forwardThe management of Golding Company has determined that the cost to investigate a variance produced by its standard cost system ranges from 2,000 to 3,000. If a problem is discovered, the average benefit from taking corrective action usually outweighs the cost of investigation. Past experience from the investigation of variances has revealed that corrective action is rarely needed for deviations within 8% of the standard cost. Golding produces a single product, which has the following standards for materials and labor: Actual production for the past 3 months follows, with the associated actual usage and costs for materials and labor. There were no beginning or ending raw materials inventories. Required: 1. What upper and lower control limits would you use for materials variances? For labor variances? 2. Compute the materials and labor variances for April, May, and June. Identify those that would require investigation by comparing each variance to the amount of the limit computed in Requirement 1. Compute the actual percentage deviation from standard. Round all unit costs to four decimal places. Round variances to the nearest dollar. Round variance rates to three decimal places so that percentages will show to one decimal place. 3. CONCEPTUAL CONNECTION Let the horizontal axis be time and the vertical axis be variances measured as a percentage deviation from standard. Draw horizontal lines that identify upper and lower control limits. Plot the labor and material variances for April, May, and June. Prepare a separate graph for each type of variance. Explain how you would use these graphs (called control charts) to assist your analysis of variances.arrow_forward

- Refer to Cornerstone Exercise 8.13. In March, Nashler Company produced 163,200 units and had the following actual costs: Required: 1. Prepare a performance report for Nashler Company comparing actual costs with the flexible budget for actual units produced. 2. What if Nashler Companys actual direct materials cost were 1,175,040? How would that affect the variance for direct materials? The total cost variance?arrow_forwardGeorgia Gasket Co. budgets 8,000 direct labor hours for the year. The total overhead budget is expected to amount to 20,000. The standard cost for a unit of the companys product estimates the variable overhead as follows: The actual data for the period follow: Using the four-variance method, calculate the overhead variances. (Hint: First compute the budgeted fixed overhead rate.)arrow_forwardUSD Inc. has established the following standard cost per unit: Although 10,000 units were budgeted, 12,000 units were produced. The Purchasing department bought 50,000 lb of materials at a cost of $237,500. Actual pounds of materials used were 46,000. Direct labor cost was $287,500 for 25,000 hours worked. Required: Make journal entries to record the materials transactions, assuming that the materials price variance was recorded at the time of purchase. Make journal entries to record the labor variances.arrow_forward

- Flexible budgeting and variance analysis Im Really Cold Coat Company makes womens and mens coats. Both products require filler and lining material. The following planning information has been made available: Im Really Cold Coat Company does not expect there to be any beginning or ending inventories of filler and lining material. At the end of the budget year, Im Really Cold Coat Company experienced the following actual results: The expected beginning inventory and desired ending inventory were realized. Instructions 1. Prepare the following variance analyses for both coats and the total, based on the actual results and production levels at the end of the budget year: A. Direct materials price, quantity, and total variance. B. Direct labor rate, time, and total variance. 2. Why are the standard amounts in part (1) based on the actual production at the end of the year instead of the planned production at the beginning of the year?arrow_forwardIn all of the exercises involving variances, use F and U to designate favorable and unfavorable variances, respectively. E8-1 through E8-5 use the following data: The standard operating capacity of Tecate Manufacturing Co. is 1,000 units. A detailed study of the manufacturing data relating to the standard production cost of one product revealed the following: 1. Two pounds of materials are needed to produce one unit. 2. Standard unit cost of materials is 8 per pound. 3. It takes one hour of labor to produce one unit. 4. Standard labor rate is 10 per hour. 5. Standard overhead (all variable) for this volume is 4,000. Each case in E8-1 through E8-5 requires the following: a. Set up a standard cost summary showing the standard unit cost. b. Analyze the variances for materials and labor. c. Make journal entries to record the transfer to Work in Process of: 1. Materials costs 2. Labor costs 3. Overhead costs (When making these entries, include the variances.) d. Prepare the journal entry to record the transfer of costs to the finished goods account. Standard unit cost; variance analysis; journal entries 1,000 units were started and finished. Case 1: All prices and quantities for the cost elements are standard, except for materials cost, which is 8.50 per pound. Case 2: All prices and quantities for the cost elements are standard, except that 1,900 lb of materials were used.arrow_forwardCarlo Lee Corp. has established the following standard cost per unit: Although 10,000 units were budgeted, only 8,800 units were produced. The purchasing department bought 55,000 lb of materials at a cost of $123,750. Actual pounds of materials used were 54,305. Direct labor cost was $186,550 for 18,200 hours worked. Required: Make journal entries to record the materials transactions, assuming that the materials price variance was recorded at the time of purchase. Make journal entries to record the labor variances.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Responsibility Accounting| Responsibility Centers and Segments| US CMA Part 1| US CMA course; Master Budget and Responsibility Accounting-Intro to Managerial Accounting- Su. 2013-Prof. Gershberg; Author: Mera Skill; Rutgers Accounting Web;https://www.youtube.com/watch?v=SYQ4u1BP24g;License: Standard YouTube License, CC-BY