Videos

Two months (July and August) have passed since Ms. Valli has seen the financial statements for All About You Spa. It is time to begin their preparation. Several accounts need adjusting. These include the accounts you adjusted in Chapter 4 as well as any accounts involved with merchandising.

Adjusting Entry Information

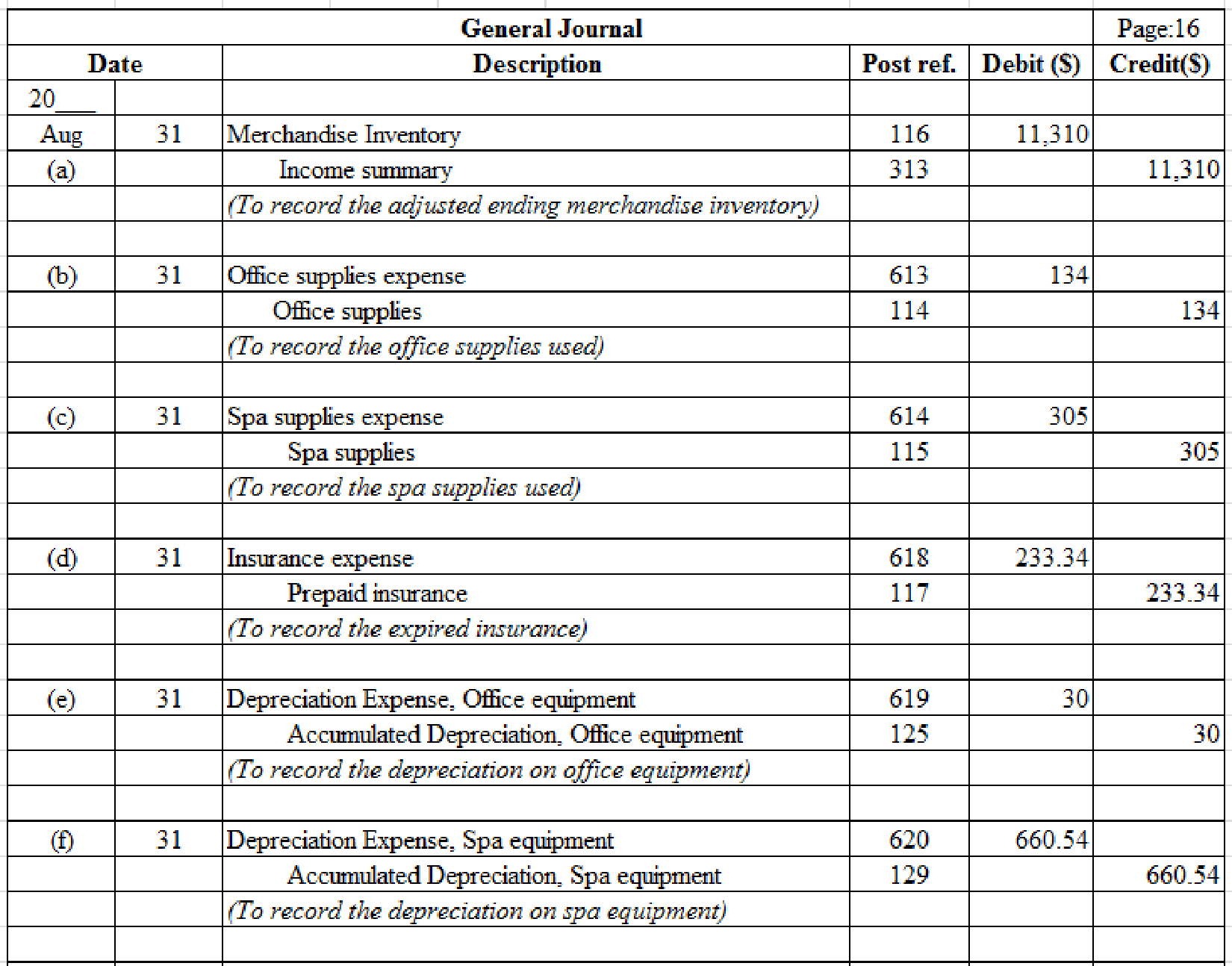

Merchandise Inventory Adjustment (a)

A physical count of inventory was taken, and the inventory was valued at $11,310.

Supplies Adjustments (b) and (c)

A physical count has been taken of the two supplies accounts. The values of the remaining inventories of supplies are as follows:

Prepaid Insurance Adjustment (d)

A review of the insurance records determined that $233.34 in liability insurance coverage had been used during the last two months.

Estimated depreciation amounts for the two equipment accounts are as follows:

Wages Expense/Wages Payable Adjustment

There is no need for a Wages Expense/Wages Payable adjustment because the end of the fiscal period did not come in the middle of a pay period.

Required

- 1. Complete a work sheet (if required by your instructor). Ignore this step if using CLGL.

- 2. Journalize the adjusting entries in the general journal.

- If you are preparing the adjusting entries with Working Papers, enter your transactions beginning on page 16.

- 3. Post the adjusting entries to the general ledger accounts.

- Ignore this step if you are using CLGL.

- 4. Prepare an adjusted

trial balance as of August 31, 20--.

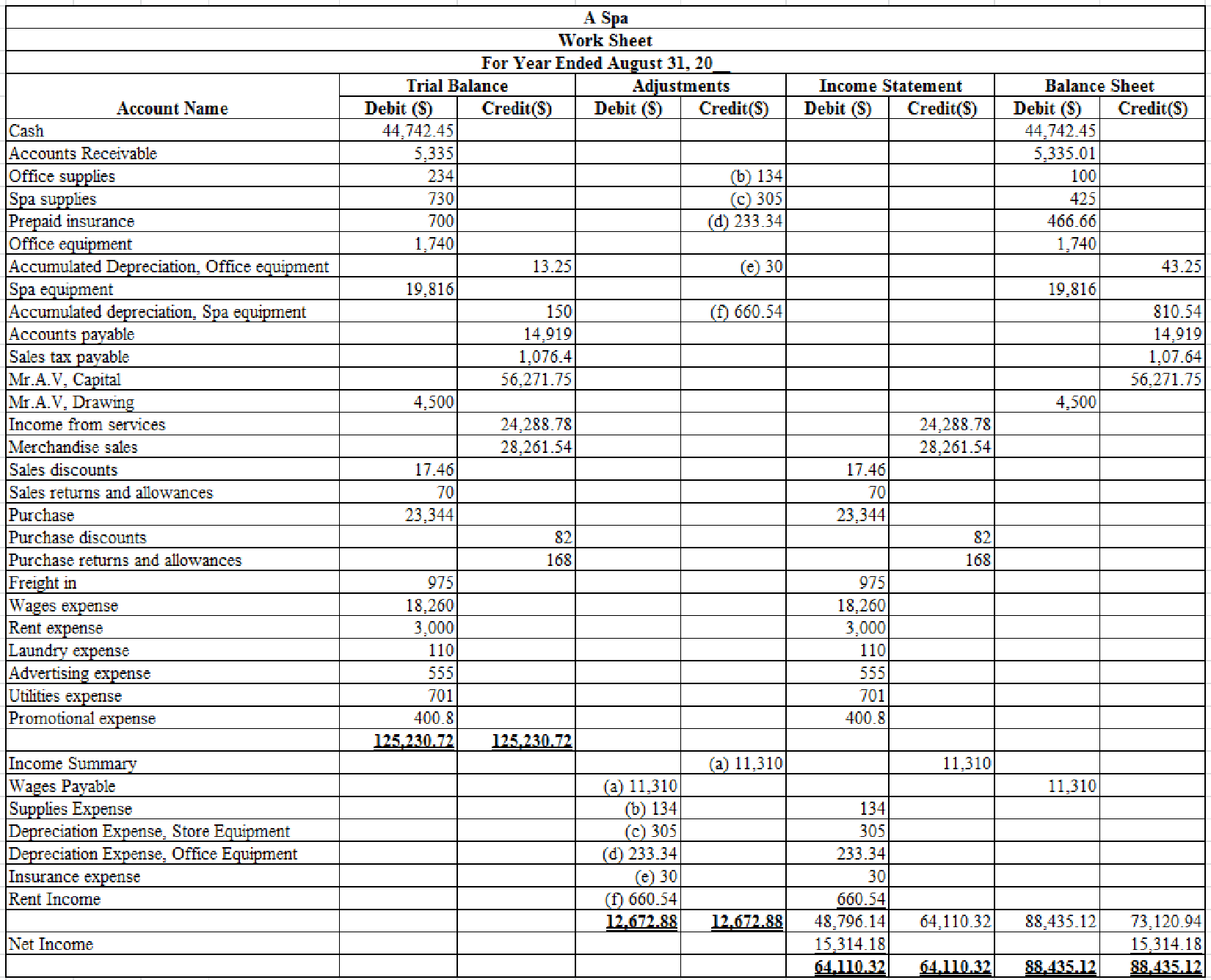

1.

Prepare worksheet for A Spa as of August.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Balance sheet: This financial statement reports a company’s resources (assets) and claims of creditors (liabilities) and stockholders (stockholders’ equity) over those resources. The resources of the company are assets which include money contributed by stockholders and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and stockholders’ equity.

Worksheet: A worksheet is a spreadsheet used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Prepare worksheet for A Spa.

Table (1)

2.

Journalize the adjusting entries in the general journal

Explanation of Solution

Adjusting entries: Adjusting entries are those entries which are recorded at the end of the year, to update the income statement accounts (revenue and expenses) and balance sheet accounts (assets, liabilities, and stockholders’ equity) to maintain the records according to accrual basis principle.

General journal: This is a journal used to record infrequent transactions like adjusting entries, closing entries, accounting errors, sale of assets, or bad debts expense.

Journalize the adjusting entries.

Table (2)

Description:

- a) Merchandise Inventory is an asset (current) account and it is increased. Therefore, debit the merchandise inventory. Income summary is a temporary account and it is closed. Therefore, credit the income summary.

- b) Office supplies expense is an expense account and it is increased. Therefore, debit the Office supplies expense. Office supplies are a liability account and it is increased. Therefore, credit the Office supplies.

- c) Spa supplies expense is revenue account and it is increased. Therefore, debit the Spa supplies expense. Spa supplies (on hand) are an asset (current) account and it is decreased. Therefore, credit the Spa supplies (on hand).

- d) Insurance expense is an expense (operating) account and it is increased. Therefore, debit the insurance expense. Prepaid insurance is an asset (current) account and it is decreased. Therefore, credit the prepaid insurance.

- e) Depreciation expense (on office equipment) is an expense account and it is increased. Therefore, debit the depreciation expense. Accumulated depreciation (on office equipment) is a contra asset account and it is decreased. Therefore, credit the accumulated depreciation.

- f) Depreciation expense (on spa equipment) is an expense account and it is increased. Therefore, debit the depreciation expense. Accumulated depreciation (on spa equipment) is a contra asset account and it is decreased. Therefore, credit the accumulated depreciation.

3.

Post the adjusting entries in general ledger.

Explanation of Solution

Posting of transaction: The process of transferring the journalized transactions into the accounts of the ledger is known as posting of transaction.

Post the prepared journals to the general ledger:

| General ledger | |||||||

| Account: Cash | Account No: 111 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 44,742.45 | ||||

| Account: Accounts receivable | Account No: 113 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 5,335.01 | ||||

| Account: Office supplies | Account No: 114 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 234 | ||||

| Adjusting | J16 | 134 | 100 | ||||

| Account: Spa supplies | Account No: 115 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 730 | ||||

| Adjusting | J16 | 305 | 425 | ||||

| Account: Merchandise inventory | Account No: 116 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Adjusting | J16 | 11,310 | 11,310 | ||

| Account: Prepaid insurance | Account No: 117 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 700 | ||||

| Adjusting | J16 | 233.34 | 466.66 | ||||

| Account: Office equipment | Account No: 124 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 1,740 | ||||

| Account: Accumulated depreciation, Office equipment | Account No: 125 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 13.25 | ||||

| Adjusting | J11 | 30 | 43.25 | ||||

| Account: Spa equipment | Account No: 128 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 19,816 | ||||

| Account: Accumulated depreciation, Spa equipment | Account No: 129 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 150 | ||||

| Adjusting | J16 | 660.54 | 810.54 | ||||

| Account: Accounts payable | Account No: 211 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 14,919 | ||||

| Account: Wages payable | Account No: 212 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | ||||||

| Account: sales tax payable | Account No: 215 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 1,076.4 | ||||

| Account: Mr. A.V, capital | Account No: 311 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 56,271.75 | ||||

| Account: Mr. A.V, Drawing | Account No: 115 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 4,500 | ||||

| Account: Income summary | Account No: 313 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Adjusting | J16 | 11,310 | 11,310 | ||

| Account: Income from services | Account No: 411 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 24,288.78 | ||||

| Account: Merchandise sales | Account No: 412 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 28,261.54 | ||||

| Account: Sales discount | Account No: 413 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 17.46 | ||||

| Account: Sales returns and allowances | Account No: 414 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 70 | ||||

| Account: Purchase | Account No: 511 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 23,344 | ||||

| Account: Purchase discount | Account No: 512 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 82 | ||||

| Account: Purchase returns and allowances | Account No: 513 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 168 | ||||

| Account: Freight in | Account No: 515 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 975 | ||||

| Account: Wages expense | Account No: 611 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 18,260 | ||||

| Account: Rent expense | Account No: 612 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 3,000 | ||||

| Account: Office supplies expense | Account No: 613 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Adjusting | J16 | 134 | 134 | ||

| Account: Spa supplies expense | Account No: 614 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Adjusting | J16 | 305 | 305 | ||

| Account: Laundry expense | Account No: 615 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 110 | ||||

| Account: Advertising expense | Account No: 616 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 555 | ||||

| Account: Utilities expense | Account No: 617 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 701 | ||||

| Account: Insurance expense | Account No: 618 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Adjusting | J16 | 233.34 | 233.34 | ||

| Account: Depreciation expense, Office equipment | Account No: 619 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Adjusting | J16 | 30 | 30 | ||

| Account: Depreciation expense, Spa equipment | Account No: 620 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Adjusting | J16 | 660.54 | 660.54 | ||

| Account: Promotional expense | Account No: 630 | ||||||

| Date | Item | Post ref | Debit | Credit | Balance | ||

| 20___ | ($) | ($) | Debit ($) | Credit($) | |||

| Aug. | 31 | Balance | 400.8 | ||||

Table (3)

4.

Prepare a trail balance for 31st August.

Explanation of Solution

Trial balance: Trial balance is a summary of all the ledger accounts balances presented in a tabular form with two column, debit and credit. It checks the mathematical accuracy of the ledger postings and helps preparing the final accounts.

Prepare a trial balance.

| A Spa | ||

| Trail balance (Adjusted) | ||

| August 31, 20__ | ||

| Account name | Debit ($) | Credit($) |

| Cash | 44,742.45 | |

| Accounts receivable | 5,335 | |

| Office supplies | 100 | |

| Spa supplies | 425 | |

| Merchandise inventory | 11,310 | |

| Prepaid insurance | 466.66 | |

| Office equipment | 1,740 | |

| Accumulated depreciation, office equipment | 43.25 | |

| Spa equipment | 19,816 | |

| Accumulated depreciation, spa equipment | 810.54 | |

| Accounts payable | 14,919 | |

| Sales tax payable | 1,076.4 | |

| Mr. A.V, capital | 56,271.75 | |

| Mr. A.V, drawings | 4,500 | |

| Income summary | 11,310 | |

| Income from services | 24,288.78 | |

| Merchandise sales | 28,261.54 | |

| Sales discounts | 17.46 | |

| Sales returns and allowances | 70 | |

| Purchases | 23,344 | |

| Purchases discounts | 82 | |

| Purchases returns and allowances | 168 | |

| Freight in | 975 | |

| Wages expense | 18,260 | |

| Rent expense | 3,000 | |

| Office supplies expense | 134 | |

| Spa supplies expense | 305 | |

| Laundry expense | 110 | |

| Advertising expense | 555 | |

| Utilities expense | 701 | |

| Insurance expense | 233.34 | |

| Depreciation expense, office equipment | 30 | |

| Depreciation expense, spa equipment | 660.54 | |

| Promotional expense | 400.8 | |

| 137,231.26 | 137,231.26 | |

Table (4)

Want to see more full solutions like this?

Chapter 11 Solutions

College Accounting (Book Only): A Career Approach

Additional Business Textbook Solutions

Financial Accounting, Student Value Edition (4th Edition)

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Managerial Accounting (5th Edition)

Principles Of Taxation For Business And Investment Planning 2020 Edition

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

Principles of Accounting Volume 1

- Journalize the required adjusting entries for the year ended December 31 for Butler Spa and Pool Accessories. Butler Spa and Pool Accessories uses the periodic inventory system. ab. On December 31, a physical count of inventory was taken. The physical count amounted to 22,624. The Merchandise Inventory account shows a balance of 21,696. c. On July 1 of this year, 2,400 was paid for a one-year insurance policy. d. On November 1 of this year, 420 was paid for three months of advertising. e. As of December 31, the balance of the Unearned Membership Fees account is 15,600. Of this amount, 9,200 has been earned. f. Equipment purchased on May 1 of this year for 8,000 is expected to have a useful life of five years with a trade-in value of 500. All other equipment has been fully depreciated. The straight-line method is used. g. As of December 31, three days wages at 250 per day had accrued. h. As of December 31, the balance of the supplies account is 4,200. A physical inventory of the supplies was taken, with an amount of 1,650 determined to be on hand.arrow_forwardEND-OF-PERIOD SPREADSHEET, ADJUSTING, CLOSING, AND REVERSING ENTRIES Vickis Fabric Store shows the trial balance on page 601 as of December 31, 20-1. At the end of the year, the following adjustments need to be made: (a, b)Merchandise inventory as of December 31, 31,600. (c, d, e)Vicki estimates that customers will be granted 2,500 in refunds of this years sales next year and the merchandise expected to be returned will have a cost of 1,800. (f)Unused supplies on hand, 350. (g)Insurance expired, 2,400. (h)Depreciation expense for the year on building, 20,000. (i)Depreciation expense for the year on equipment, 4,000. (j)Wages earned but not paid (Wages Payable), 520. (k)Unearned revenue on December 31, 20-1, 1,200. PROBLEM 15-10A CONT. REQUIRED 1. Prepare an end-of-period spreadsheet. 2. Prepare adjusting entries and post adjusting entries to an Income Summary T account. 3. Prepare closing entries and post to a Capital T account. There were no additional investments this year. 4. Prepare a post-closing trial balance. 5. Prepare reversing entry(ies).arrow_forwardThe trial balance of Jillson Company as of December 31, the end of its current fiscal year, is as follows: Here are the data for the adjustments. ab. Merchandise Inventory at December 31, 54,845.00. c. Store supplies inventory (on hand), 488.50. d. Insurance expired, 680. e. Salaries accrued, 692. f. Depreciation of store equipment, 3,760. Required Complete the work sheet after entering the account names and balances onto the work sheet.arrow_forward

- Here are the accounts in the ledger of Mishas Jewel Box, with the balances as of December 31, the end of its fiscal year. Here are the data for the adjustments. Assume that Mishas Jewel Box uses the perpetual inventory system. a. Merchandise Inventory at December 31, 124,630. b. Insurance expired during the year, 1,294. c. Depreciation of building, 3,300. d. Depreciation of store equipment, 6,470. e. Salaries accrued at December 31, 2,470. f. Store supplies inventory (on hand) at December 31, 1,959. Required 1. Complete the work sheet after entering the account names and balances onto the work sheet. Ignore this step if using CLGL. 2. Journalize the adjusting entries. If using manual working papers, record adjusting entries on journal page 63.arrow_forwardThe trial balance of Hadden Company as of December 31, the end of its current fiscal year, is as follows: Here are the data for the adjustments. ab.Merchandise Inventory at December 31, 64,742.80. c.Store supplies inventory (on hand), 420.20. d.Insurance expired, 738. e.Salaries accrued, 684.50. f.Depreciation of store equipment, 3,620. Required Complete the work sheet after entering the account names and balances onto the work sheet.arrow_forwardADJUSTING. CLOSING. AND REVERSING ENTRIES A 6-column spreadsheet for Baldwin Company is shown on the next page. Data for adjusting the accounts are as follows: REQUIRED 1. Prepare the December 31 adjusting journal entries for Baldwin Company. 2. Prepare the December 31 closing journal entries for Baldwin Company. 3. Prepare the reversing journal entries as of January 1,20-2, for Baldwin Company. PROBLEM 27-8Aarrow_forward

- Office Supplies Somerville Corp. purchases office supplies once a month and prepares monthly financial statements. The asset account Office Supplies on Hand has a balance of $1,450 on May 1. Purchases of supplies during May amount to $1,100. Supplies on hand at May 31 amount to $920. Prepare the necessary adjusting entry on Somervilles books on May 31. What will be the effect on net income for May if this entry is not recorded?arrow_forwardOn December 31, the end of the year, the accountant for Fireside Magazine was called away suddenly because of an emergency. However, before leaving, the accountant jotted down a few notes pertaining to the adjustments. Journalize the necessary adjusting entries. Assume that Fireside Magazine uses the periodic inventory system. ab. A physical count of inventory revealed a balance of 199,830. The Merchandise Inventory account shows a balance of 202,839. c. Subscriptions received in advance amounting to 156,200 were recorded as Unearned Subscriptions. At year-end, 103,120 has been earned. d. Depreciation of equipment for the year is 12,300. e. The amount of expired insurance for the year is 1,612. f. The balance of Prepaid Rent is 2,400, representing four months rent. Three months rent has expired. g. Three days salaries will be unpaid at the end of the year; total weekly (five days) salaries are 4,000. h. As of December 31, the balance of the supplies account is 1,800. A physical inventory of the supplies was taken, with an amount of 920 determined to be on hand.arrow_forwardCOMPLETION OF A WORK SHEET SHOWING A NET INCOME The trial balance for the Venice Beach Kite Shop, a business owned by Molly Young k shown on page 550. Year-end adjustment information is as follows: (a and b)Merchandise inventory costing 35,000 is on hand as of December .31, 20--. (The periodic inventory system is used.) (c)Supplies remaining at the end of the year, 3,300. (d)Unexpired insurance on December 31, S3,800. (e)Depreciation expense on the building foe 20--, 2,500. (f)Depreciation expense on the store equipment for 20--, 3,500. (g)Unearned rent revenue as of December 31, 4,00. (h)Wages earned but not paid as of December 31, 800. 1. Complete the Adjustments columns, identifying each adjustment with its corresponding letter. 2. Complete the work sheet. 3. Enter the adjustments m a general journal.arrow_forward

- The following accounts appear in the ledger of Celso and Company as of June 30, the end of this fiscal year. The data needed for the adjustments on June 30 are as follows: ab.Merchandise inventory, June 30, 54,600. c.Insurance expired for the year, 475. d.Depreciation for the year, 4,380. e.Accrued wages on June 30, 1,492. f.Supplies on hand at the end of the year, 100. Required 1. Prepare a work sheet for the fiscal year ended June 30. Ignore this step if using CLGL. 2. Prepare an income statement. 3. Prepare a statement of owners equity. No additional investments were made during the year. 4. Prepare a balance sheet. 5. Journalize the adjusting entries. 6. Journalize the closing entries. 7. Journalize the reversing entry as of July 1, for the wages that were accrued in the June adjusting entry. Check Figure Net income, 14,066arrow_forwardThe following accounts appear in the ledger of Sheldon Company on January 31, the end of this fiscal year. The data needed for adjustments on January 31 are as follows: ab.Merchandise inventory, January 31, 55,750. c.Insurance expired for the year, 1,285. d.Depreciation for the year, 5,482. e.Accrued wages on January 31, 1,556. f.Supplies used during the year 1,503. Required 1. Prepare a work sheet for the fiscal year ended January 31. Ignore this step if using QuickBooks or general ledger. 2. Prepare an income statement. 3. Prepare a statement of owners equity. No additional investments were made during the year. Ignore this step if using CLGL. 4. Prepare a balance sheet. 5. Journalize the adjusting entries. 6. Journalize the closing entries. Check Figure Net loss, 1,737arrow_forwardThe Supplies account has a 1,400 balance. A physical inventory is taken at the end of the fiscal year, and the amount on hand is determined to be 300. What adjusting entry is required to record the supplies used? a. Supplies 300 DR, Cash 300 CR b. Supplies Expense 1,400 DR, Supplies 1,400 CR c. Supplies 1,100 DR, Supplies Expense 1,100 CR d. Supplies Expense 1,100 DR, Supplies 1,100 CR e. None of the abovearrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage