Concept explainers

Videos

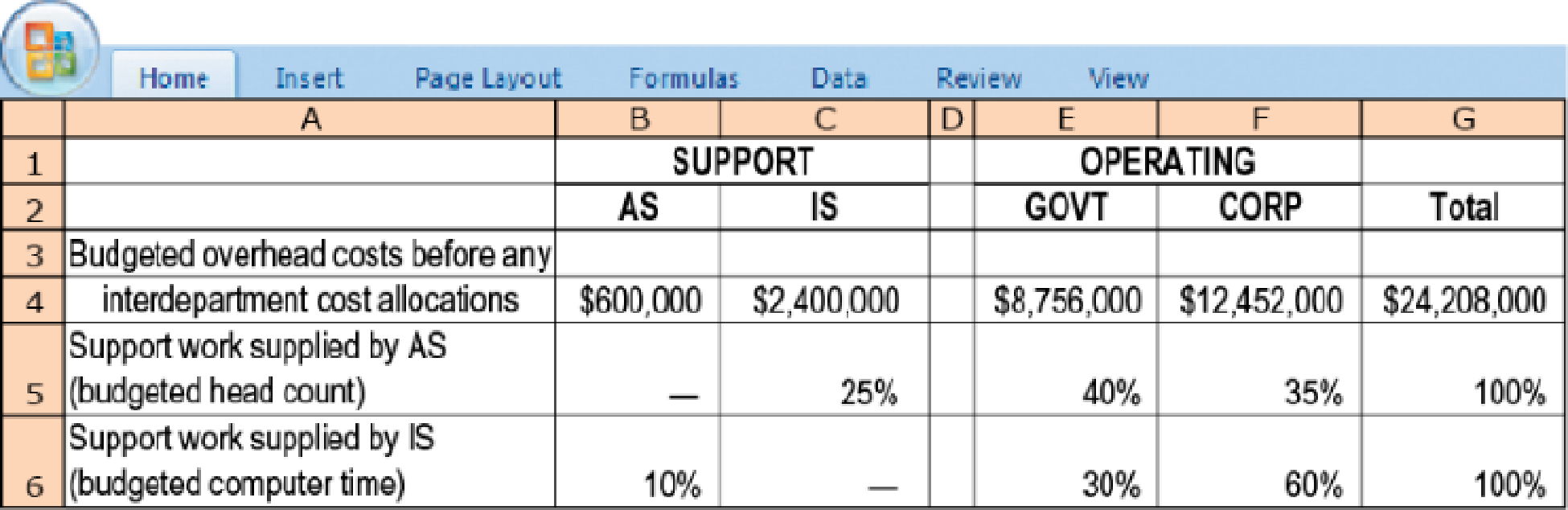

Support-department cost allocation; direct and step-down methods. Phoenix Partners provides management consulting services to government and corporate clients. Phoenix has two support departments—administrative services (AS) and information systems (IS)—and two operating departments—government consulting (GOVT) and corporate consulting (CORP). For the first quarter of 2017, Phoenix’s cost records indicate the following:

- 1. Allocate the two support departments’ costs to the two operating departments using the following methods:

Required

- a. Direct method

- b. Step-down method (allocate AS first)

- c. Step-down method (allocate IS first)

- 2. Compare and explain differences in the support-department costs allocated to each operating department.

- 3. What approaches might be used to decide the sequence in which to allocate support departments when using the step-down method?

Learn your wayIncludes step-by-step video

Chapter 15 Solutions

COST ACCOUNTING

Additional Business Textbook Solutions

Principles of Accounting Volume 1

Financial Accounting (11th Edition)

Intermediate Accounting (2nd Edition)

Financial Accounting, Student Value Edition (5th Edition)

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Cost Accounting (15th Edition)

- A manufacturing company has two service and two production departments. Human Resources and Machine Repair are the service departments. The production departments are Grinding and Polishing. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The human resources department services all departments of the company, and its costs are allocated using the numbers of employees within each department, while machine repair costs are allocable to Grinding and Polishing on the basis of machine hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardA manufacturing company has two service and two production departments. Building Maintenance and Factory Office are the service departments. The production departments are Assembly and Machining. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The building maintenance department services all departments of the company, and its costs are allocated using floor space occupied, while factory office costs are allocable to Assembly and Machining on the basis of direct labor hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardRefer to the data in Exercise 7.18. When the capacity of the HR Department was originally established, the normal usage expected for each department was 20,000 direct labor hours. This usage is also the amount of activity planned for the two departments in Year 1 and Year 2. Required: 1. Allocate the costs of the HR Department using the direct method and assuming that the purpose is product costing. 2. Allocate the costs of the HR Department using the direct method and assuming that the purpose is to evaluate performance.arrow_forward

- A company uses charging rates to allocate service department costs to the using departments. The accountant compiled the following information on one of the service departments: If Department K plans to use 1,350 hours of the service departments service in the coming year, how much of the service departments cost is allocated to Department K? a. 3,375 b. 27,300 c. 26,325 d. 23,950arrow_forwardComprehensive support department allocationsManagement at C. Pier Press has decided to allocate costs of the paper’s two support departments (administration and human resources) to the two revenue-generating departments (advertising and circulation). Administration costs are to be allocated on the basis of dollars of assets employed; human resources costs are to be allocated on the basis of number of employees. The following costs and allocation bases are available: Department Direct Costs Number of Employees Assets Employed Administration $1,094,100 14 $541,940 Human resources 689,780 11 408,380 Advertising 1,340,920 17 1,067,360 Circulation 1,893,640 36 2,618,420 Totals $5,018,440 78 $4,636,100 c. Assuming that the benefits-provided ranking is the order shown in the table, use the step method to allocate the support department costs to the revenue-generating departments.Note: Round your final answers only to the nearest whole dollar. Amount…arrow_forwardComprehensive support department allocationsManagement at C. Pier Press has decided to allocate costs of the paper’s two support departments (administration and human resources) to the two revenue-generating departments (advertising and circulation). Administration costs are to be allocated on the basis of dollars of assets employed; human resources costs are to be allocated on the basis of number of employees. The following costs and allocation bases are available: Department Direct Costs Number of Employees Assets Employed Administration $1,094,100 14 $541,940 Human resources 689,780 11 408,380 Advertising 1,340,920 17 1,067,360 Circulation 1,893,640 36 2,618,420 Totals $5,018,440 78 $4,636,100 e. Using the algebraic method, allocate the support department costs to the revenue-generating departments. Note: Round percentages in your calculation to the nearest whole percent (for example, round 34.5% to 35%). Note: Round your final answer to the nearest…arrow_forward

- Comprehensive support department allocationsManagement at C. Pier Press has decided to allocate costs of the paper’s two support departments (administration and human resources) to the two revenue-generating departments (advertising and circulation). Administration costs are to be allocated on the basis of dollars of assets employed; human resources costs are to be allocated on the basis of number of employees. The following costs and allocation bases are available: Department Direct Costs Number of Employees Assets Employed Administration $1,094,100 14 $541,940 Human resources 689,780 11 408,380 Advertising 1,340,920 17 1,067,360 Circulation 1,893,640 36 2,618,420 Totals $5,018,440 78 $4,636,100 c. Assuming that the benefits-provided ranking is the order shown in the table, use the step method to allocate the support department costs to the revenue-generating departments.Note: Round your final answers only to the nearest whole dollar. Amount allocated…arrow_forwardComprehensive support department allocationsManagement at C. Pier Press has decided to allocate costs of the paper’s two support departments (administration and human resources) to the two revenue-generating departments (advertising and circulation). Administration costs are to be allocated on the basis of dollars of assets employed; human resources costs are to be allocated on the basis of number of employees. The following costs and allocation bases are available: Department Direct Costs Number of Employees Assets Employed Administration $1,094,100 14 $541,940 Human resources 689,780 11 408,380 Advertising 1,340,920 17 1,067,360 Circulation 1,893,640 36 2,618,420 Totals $5,018,440 78 $4,636,100 c. Assuming that the benefits-provided ranking is the order shown in the table, use the step method to allocate the support department costs to the revenue-generating departments.Note: Round your final answers only to the nearest whole dollar. Amount allocated…arrow_forwardManagement of XYZ Media has decided to allocate the costs of the paper's two service/support departments (administration and human resources) to the two revenue generating/producing departments (advertising and circulation.) Administration costs are to be allocated on the Pesos of Assets Employed. ; Human Resources costs are to be allocated on the basis of Number of Employees. The following costs and allocated bases are available. (Convert the fractions on the allocated bases into percentages rounded to the whole number). Department - Administration: Direct Costs - P781,500 Number of Employees - 10 Pesos of Assets Employed - P387,100 Department - Human Resources: Direct Costs - P492,700 Number of Employees - 7 Pesos of Assets Employed - P291,700 Department - Advertising: Direct Costs - P957,800 Number of Employees - 12 Pesos of Assets Employed - P762,400 Department - Circulation: Direct Costs - P1,352,600 Number of Employees - 25 Pesos of Assets Employed - P1,870,300…arrow_forward

- Comprehensive support department allocations Management at C. Pier Press has decided to allocate costs of the paper’s two support departments (administration and human resources) to the two revenue-generating departments (advertising and circulation). Administration costs are to be allocated on the basis of dollars of assets employed; human resources costs are to be allocated on the basis of number of employees. The following costs and allocation bases are available: Department Direct Costs Number of Employees Assets Employed Administration $390,750 5 $193,550 Human resources 246,350 4 145,850 Advertising 478,900 6 381,200 Circulation 676,300 13 935,150 Totals $1,792,300 28 $1,655,750 a. Using the direct method, allocate the support department costs to the revenue-generating departments.Note: Round percentages in your calculation to the nearest whole percent (for example, round 34.5% to 35%).Note: Round your final answer to the nearest whole dollar.Total…arrow_forwardData Performance, a computer software consulting company, has three major functional areas: computer programming, information systems consulting, and software training. Carol Bingham, a pricing analyst, has been asked to develop total costs for the functional areas. These costs will be used as a guide in pricing a new contract. In computing these costs, Carol is considering three different methods of the departmental allocation approach to allocate overhead costs: the direct method, the step method, and the reciprocal method. She assembled the following data from the two service departments, information systems and facilities: Service Departments Production Departments Information Systems Facilities Computer Programming Information Systems Consulting Software Training Total Budgeted overhead (base) $ 368,000 $ 184,000 $ 736,000 $ 874,000 $ 575,000 $ 2,737,000 Information Systems (computer hours) 600 1,200 300 900 3,000 Facilities (square feet) 240 960 600 600…arrow_forwardMiddler Corporation, a manufacturer of electronics and communications systems, uses a service department charge system to charge profit centers with Computing and Communications Services (CCS) service department costs. The following table identifies an abbreviated list of service categories and activity bases used by the CCS department. The table also includes some assumed cost and activity base quantity information for each service for October. CCS ServiceCategory Activity Base Budgeted Cost Budgeted ActivityBase Quantity Help desk Number of calls $55,660 2,200 Network center Number of devices monitored 668,100 10,200 Electronic mail Number of user accounts 57,500 5,750 Handheld technology support Number of handheld devices issued 153,600 9,600 One of the profit centers for Middler Corporation is the Communication Systems (COMM) sector. Assume the following information for the COMM sector: The sector has 1,000 employees, of whom 50% are office employees.…arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,