EP FINANCIAL+MANAGERIAL ACCT. >CUSTOM<

5th Edition

ISBN: 9781323590287

Author: *ST.LEO UNIV.

Publisher: PEARSON C

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 19, Problem 38AP

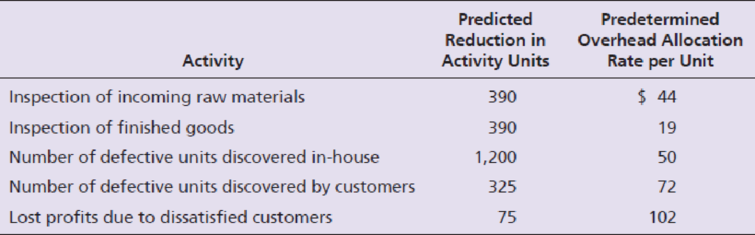

Stella, Inc. is using a costs-of-quality approach to evaluate design engineering efforts for a new skateboard. Stella’s senior managers expect the engineering work to reduce appraisal, internal failure, and external failure activities. The predicted reductions in activities over the two-year life of the skateboards follow. Also shown are the predetermined overhead allocation rates for each activity.

Requirements

- 1. Calculate the predicted quality cost savings from the design engineering work.

- 2. Stella spent $103,000 on design engineering for the new skateboard. What is the net benefit of this “preventive” quality activity?

- 3. What major difficulty would Stella’s managers have in implementing this costs-of-quality approach? What alternative approach could they use to measure quality improvement?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Chapter 19 Solutions

EP FINANCIAL+MANAGERIAL ACCT. >CUSTOM<

Ch. 19 - The Santos Shirt Company manufactures shirts in...Ch. 19 - Prob. 2TICh. 19 - Prob. 3TICh. 19 - Prob. 4TICh. 19 - Prob. 5TICh. 19 - Prob. 6TICh. 19 - Prob. 7TICh. 19 - Prob. 8TICh. 19 - Prob. 9TICh. 19 - Prob. 10TI

Ch. 19 - Prob. 11TICh. 19 - Prob. 12TICh. 19 - Which statement is false? a. Using a single...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It can use ABC information for what...Ch. 19 - Prob. 6QCCh. 19 - Companies enjoy many benefits from using JIT....Ch. 19 - Which account is not used in JIT costing? a....Ch. 19 - The cost of lost future sales after a customer...Ch. 19 - Spending on testing a product before shipment to...Ch. 19 - What is the formula to compute the predetermined...Ch. 19 - How is the predetermined overhead allocation rate...Ch. 19 - Describe how a single plantwide overhead...Ch. 19 - Why is using a single plantwide overhead...Ch. 19 - Why is the use of departmental overhead allocation...Ch. 19 - What is activity-based management? How is it...Ch. 19 - How many cost pools are in an activity-based...Ch. 19 - What are the four steps to developing an...Ch. 19 - Why is ABC usually considered more accurate than...Ch. 19 - List two ways managers can use ABM to make...Ch. 19 - Define value engineering. How is it used to...Ch. 19 - Explain the difference between target price and...Ch. 19 - How can ABM be used by service companies?Ch. 19 - What is a just-in-time management system?Ch. 19 - Explain how the work cell manufacturing layout...Ch. 19 - What are the inventory accounts used in JIT...Ch. 19 - How is the Conversion Costs account used in JIT...Ch. 19 - Prob. 18RQCh. 19 - Which accounts are adjusted for the underallocated...Ch. 19 - Prob. 20RQCh. 19 - Prob. 21RQCh. 19 - Prevention is much cheaper than external failure....Ch. 19 - What are quality improvement programs?Ch. 19 - Prob. 24RQCh. 19 - Prob. 1SECh. 19 - The Oakman (Company (see Short Exercise S19-1) has...Ch. 19 - Activity-based costing requires four steps. List...Ch. 19 - Prob. 4SECh. 19 - Darby Corp. is considering the use of...Ch. 19 - The following information is provided for Orbit...Ch. 19 - Jaunkas Corp. manufactures mid-fi and hi-fi stereo...Ch. 19 - Spectrum Corp. makes two products: C and D. The...Ch. 19 - Refer to Short Exercise S19-8. Spectrum Corp....Ch. 19 - Haworth Company is a management consulting firm....Ch. 19 - Refer to Short Exercise S19-10. Haworth desires a...Ch. 19 - Prob. 12SECh. 19 - Prime Products uses a JIT management system to...Ch. 19 - Stegall, Inc. manufactures motor scooters. For...Ch. 19 - Koehler makes handheld calculators in two models:...Ch. 19 - Koehler (see Exercise E19-15) makes handheld...Ch. 19 - Koehler (see Exercise E19-15 and Exercise E19-16)...Ch. 19 - Franklin, Inc. uses activity-based costing to...Ch. 19 - Turbo Champs Corp. uses activity-based costing to...Ch. 19 - Eason Company manufactures wheel rims. The...Ch. 19 - Refer to Exercise E19-20. For 2019, Easons...Ch. 19 - Refer to Exercises E19-20 and E19-21. Controller...Ch. 19 - Treat Dog Collars uses activity-based costing....Ch. 19 - Western, Inc. is a technology consulting firm...Ch. 19 - Refer to Exercise E19-24. The president of Western...Ch. 19 - Prob. 26ECh. 19 - Refer to Exercise E19-26. Western desires a 20%...Ch. 19 - Lally, Inc. produces universal remote controls....Ch. 19 - Prob. 29ECh. 19 - Darrel Co. makes electronic components. Chris...Ch. 19 - Prob. 31ECh. 19 - Prob. 32ECh. 19 - Willitte Pharmaceuticals manufactures an...Ch. 19 - The Alright Manufacturing Company in Rochester,...Ch. 19 - Oscar, Inc. manufactures bookcases and uses an...Ch. 19 - Blanchette Plant Service completed a special...Ch. 19 - Low Range produces fleece jackets. The company...Ch. 19 - Stella, Inc. is using a costs-of-quality approach...Ch. 19 - Harcourt Pharmaceuticals manufactures an...Ch. 19 - The Alexander Manufacturing Company in Rochester,...Ch. 19 - Martin, Inc. manufactures bookcases and uses an...Ch. 19 - Rennie Plant Service completed a special...Ch. 19 - High Mountain produces fleece jackets. The company...Ch. 19 - Roxi, Inc. is using a costs-of-quality approach to...Ch. 19 - Download an Excel template for this problem online...Ch. 19 - This problem continues the Piedmont Computer...Ch. 19 - Prob. 1TIATCCh. 19 - Harris Systems specializes in servers for...Ch. 19 - Harris Systems has decided to adopt ABC. To remain...Ch. 19 - Prob. 1EICh. 19 - Anu Ghai was a new production analyst at RHI,...

Additional Business Textbook Solutions

Find more solutions based on key concepts

List five asset accounts, three liability accounts, and five expense accounts included in the acquisition and p...

Auditing and Assurance Services (16th Edition)

Assume you are a CFO of a company that is attempting to race additional capital to finance an expansion of its ...

Financial Accounting, Student Value Edition (4th Edition)

The amount that should be recorded by Company R for building under historical cost principle.

Financial Accounting (11th Edition)

1. For Frank’s Funky Sounds, straight-line depreciation on the trucks is a

Learning Objective 1

a. variable cos...

Horngren's Accounting (12th Edition)

List five asset accounts, three liability accounts, and five expense accounts included in the acquisition and p...

Auditing And Assurance Services

Calculating certain information using the direct method (Learning Objective 4) 20-25 min. Trudeaus Marine, Inc....

Financial Accounting, Student Value Edition (5th Edition)

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Pinter Company had the following environmental activities and product information: 1. Environmental activity costs 2. Driver data 3. Other production data Required: 1. Calculate the activity rates that will be used to assign environmental costs to products. 2. Determine the unit environmental and unit costs of each product using ABC. 3. What if the design costs increased to 360,000 and the cost of toxic waste decreased to 750,000? Assume that Solvent Y uses 6,000 out of 12,000 design hours. Also assume that waste is cut by 50 percent and that Solvent Y is responsible for 14,250 of 15,000 pounds of toxic waste. What is the new environmental cost for Solvent Y?arrow_forwardSilven Company has identified the following overhead activities, costs, and activity drivers for the coming year: Silven produces two models of cell phones with the following expected activity demands: 1. Determine the total overhead assigned to each product using the four activity drivers. 2. Determine the total overhead assigned to each model using the two most expensive activities. The costs of the two relatively inexpensive activities are allocated to the two expensive activities in proportion to their costs. 3. Using ABC as the benchmark, calculate the percentage error and comment on the accuracy of the reduced system. Explain why this approach may be desirable.arrow_forwardRecently, Ulrich Company received a report from an external consulting group on its quality costs. The consultants reported that the companys quality costs total about 21 percent of its sales revenues. Somewhat shocked by the magnitude of the costs, Rob Rustin, president of Ulrich Company, decided to launch a major quality improvement program. For the coming year, management decided to reduce quality costs to 17 percent of sales revenues. Although the amount of reduction was ambitious, most company officials believed that the goal could be realized. To improve the monitoring of the quality improvement program, Rob directed Pamela Golding, the controller, to prepare monthly performance reports comparing budgeted and actual quality costs. Budgeted costs and sales for the first two months of the year are as follows: The following actual sales and actual quality costs were reported for January: Required: 1. Reorganize the monthly budgets so that quality costs are grouped in one of four categories: appraisal, prevention, internal failure, or external failure. (Essentially, prepare a budgeted cost of quality report.) Also, identify each cost as variable (V) or fixed (F). (Assume that no costs are mixed.) 2. Prepare a performance report for January that compares actual costs with budgeted costs. Comment on the companys progress in improving quality and reducing its quality costs.arrow_forward

- Nabors Company had actual quality costs for the year ended June 30, 20x5, as given below. At the zero-defect state, Nabors expects to spend 375,000 on quality engineering, 75,000 on vendor certification, and 50,000 on packaging inspection. Assume sales to be 25,000,000. Required: 1. Prepare a long-range performance report for 20x5. What does this report tell the management of Nabors? 2. Explain why quality costs still are present for the zero-defect state. 3. What if Nabors achieves the zero-defect state reflected in the report? What are some of the implications of this achievement?arrow_forwardIn 20X1, Don Blackburn, president of Price Electronics, received a report indicating that quality costs were 31% of sales. Faced with increasing pressures from imported goods. Don resolved to take measures to improve the overall quality of the companys products. After hiring a consultant in 20X1, the company began an aggressive program of total quality control. At the end of 20X5, Don requested an analysis of the progress the company had made in reducing and controlling quality costs. The accounting department assembled the following data: Required: 1. Compute the quality costs as a percentage of sales by category and in total for each year. 2. Prepare a multiple-year trend graph for quality costs, both by total costs and by category. Using the graph, assess the progress made in reducing and controlling quality costs. Does the graph provide evidence that quality has improved? Explain. 3. Using the 20X1 quality cost relationships (assume all costs are variable), calculate the quality costs that would have prevailed in 20X4. By how much did profits increase in 20X4 because of the quality improvement program? Repeat for 20X5.arrow_forwardLindell Manufacturing embarked on an ambitious quality program that is centered on continual improvement. This improvement is operationalized by declining quality costs from year to year. Lindell rewards plant managers, production supervisors, and workers with bonuses ranging from 1,000 to 10,000 if their factory meets its annual quality cost goals. Len Smith, manager of Lindells Boise plant, felt obligated to do everything he could to provide this increase to his employees. Accordingly, he has decided to take the following actions during the last quarter of the year to meet the plants budgeted quality cost targets: a. Decrease inspections of the process and final product by 50% and transfer inspectors temporarily to quality training programs. Len believes this move will increase the inspectors awareness of the importance of quality; also, decreasing inspection will produce significantly less downtime and less rework. By increasing the output and decreasing the costs of internal failure, the plant can meet the budgeted reductions for internal failure costs. Also, by showing an increase in the costs of quality training, the budgeted level for prevention costs can be met. b. Delay replacing and repairing defective products until the beginning of the following year. While this may increase customer dissatisfaction somewhat, Len believes that most customers expect some inconvenience. Besides, the policy of promptly dealing with customers who are dissatisfied could be reinstated in 3 months. In the meantime, the action would significantly reduce the costs of external failure, allowing the plant to meet its budgeted target. c. Cancel scheduled worker visits to customers plants. This program, which has been very well received by customers, enables Lindell workers to see just how the machinery they make is used by the customer and also gives them first-hand information on any remaining problems with the machinery. Workers who went on previous customer site visits came back enthusiastic and committed to Lindells quality program. Lindells quality program staff believes that these visits will reduce defects during the following year. Required: 1. Evaluate Lens ethical behavior. In this evaluation, consider his concern for his employees. Was he justified in taking the actions described? If not, what should he have done? 2. Assume that the company views Lens behavior as undesirable. What can the company do to discourage it? 3. Assume that Len is a CMA and a member of the IMA. Refer to the ethical code for management accountants in Chapter 1. Were any of these ethical standards violated?arrow_forward

- Jolene Askew, manager of Feagan Company, has committed her company to a strategically sound cost reduction program. Emphasizing life-cycle cost management is a major part of this effort. Jolene is convinced that production costs can be reduced by paying more attention to the relationships between design and manufacturing. Design engineers need to know what causes manufacturing costs. She instructed her controller to develop a manufacturing cost formula for a newly proposed product. Marketing had already projected sales of 25,000 units for the new product. (The life cycle was estimated to be 18 months. The company expected to have 50 percent of the market and priced its product to achieve this goal.) The projected selling price was 20 per unit. The following cost formula was developed: Y=200,000+10X1 where X1=Machinehours(Theproductisexpectedtouseonemachinehourforeveryunitproduced.) Upon seeing the cost formula, Jolene quickly calculated the projected gross profit to be 50,000. This produced a gross profit of 2 per unit, well below the targeted gross profit of 4 per unit. Jolene then sent a memo to the Engineering Department, instructing them to search for a new design that would lower the costs of production by at least 50,000 so that the target profit could be met. Within two days, the Engineering Department proposed a new design that would reduce unit-variable cost from 10 per machine hour to 8 per machine hour (Design Z). The chief engineer, upon reviewing the design, questioned the validity of the controllers cost formula. He suggested a more careful assessment of the proposed designs effect on activities other than machining. Based on this suggestion, the following revised cost formula was developed. This cost formula reflected the cost relationships of the most recent design (Design Z). Y=140,000+8X1+5,000X2+2,000X3 where X1=MachinehoursX2=NumberofbatchesX3=Numberofengineeringchangeorders Based on scheduling and inventory considerations, the product would be produced in batches of 1,000; thus, 25 batches would be needed over the products life cycle. Furthermore, based on past experience, the product would likely generate about 20 engineering change orders. This new insight into the linkage of the product with its underlying activities led to a different design (Design W). This second design also lowered the unit-level cost by 2 per unit but decreased the number of design support requirements from 20 orders to 10 orders. Attention was also given to the setup activity, and the design engineer assigned to the product created a design that reduced setup time and lowered variable setup costs from 5,000 to 3,000 per setup. Furthermore, Design W also creates excess activity capacity for the setup activity, and resource spending for setup activity capacity can be decreased by 40,000, reducing the fixed cost component in the equation by this amount. Design W was recommended and accepted. As prototypes of the design were tested, an additional benefit emerged. Based on test results, the post-purchase costs dropped from an estimated 0.70 per unit sold to 0.40 per unit sold. Using this information, the Marketing Department revised the projected market share upward from 50 percent to 60 percent (with no price decrease). Required: 1. Calculate the expected gross profit per unit for Design Z using the controllers original cost formula. According to this outcome, does Design Z reach the targeted unit profit? Repeat, using the engineers revised cost formula. Explain why Design Z failed to meet the targeted profit. What does this say about the use of unit-based costing for life-cycle cost management? 2. Calculate the expected profit per unit using Design W. Comment on the value of activity information for life-cycle cost management. 3. The benefit of the post-purchase cost reduction of Design W was discovered in testing. What direct benefit did it create for Feagan Company (in dollars)? Reducing post-purchase costs was not a specific design objective. Should it have been? Are there any other design objectives that should have been considered?arrow_forwardJavier Company has sales of 8 million and quality costs of 1,600,000. The company is embarking on a major quality improvement program. During the next three years, Javier intends to attack failure costs by increasing its appraisal and prevention costs. The right prevention activities will be selected, and appraisal costs will be reduced according to the results achieved. For the coming year, management is considering six specific activities: quality training, process control, product inspection, supplier evaluation, prototype testing, and redesign of two major products. To encourage managers to focus on reducing non-value-added quality costs and select the right activities, a bonus pool is established relating to reduction of quality costs. The bonus pool is equal to 10 percent of the total reduction in quality costs. Current quality costs and the costs of these six activities are given in the following table. Each activity is added sequentially so that its effect on the cost categories can be assessed. For example, after quality training is added, the control costs increase to 320,000, and the failure costs drop to 1,040,000. Even though the activities are presented sequentially, they are totally independent of each other. Thus, only beneficial activities need be selected. Required: 1. Identify the control activities that should be implemented, and calculate the total quality costs associated with this selection. Assume that an activity is selected only if it increases the bonus pool. 2. Given the activities selected in Requirement 1, calculate the following: a. The reduction in total quality costs b. The percentage distribution for control and failure costs c. The amount for this years bonus pool 3. Suppose that a quality engineer complained about the gainsharing incentive system. Basically, he argued that the bonus should be based only on reductions of failure and appraisal costs. In this way, investment in prevention activities would be encouraged, and eventually, failure and appraisal costs would be eliminated. After eliminating the non-value-added costs, focus could then be placed on the level of prevention costs. If this approach were adopted, what activities would be selected? Do you agree or disagree with this approach? Explain.arrow_forwardMabbut Company has the following departmental manufacturing layout for one of its plants: A consulting firm recommended a value stream with the following manufacturing cell: Required: 1. Calculate the total time it takes to produce a batch of 10 units using the traditional departmental manufacturing layout. 2. Using cellular manufacturing, how much time is saved producing the same batch of 10 units? Assuming the cell operates continuously, what is the production rate? Which process controls this production rate? 3. Assume the processing time of Welding is reduced to 6 minutes, while the times of the other processes stay the same. What is the production rate now, and how long will it take to produce a batch of 10 units if the cell is in a continuous production mode?arrow_forward

- The controller for Muir Companys Salem plant is analyzing overhead in order to determine appropriate drivers for use in flexible budgeting. She decided to concentrate on the past 12 months since that time period was one in which there was little important change in technology, product lines, and so on. Data on overhead costs, number of machine hours, number of setups, and number of purchase orders are in the following table. Required: 1. Calculate an overhead rate based on machine hours using the total overhead cost and total machine hours. (Round the overhead rate to the nearest cent and predicted overhead to the nearest dollar.) Use this rate to predict overhead for each of the 12 months. 2. Run a regression equation using only machine hours as the independent variable. Prepare a flexible budget for overhead for the 12 months using the results of this regression equation. (Round the intercept and x-coefficient to the nearest cent and predicted overhead to the nearest dollar.) Is this flexible budget better than the budget in Requirement 1? Why or why not?arrow_forwardAndresen Company had the following quality costs for the years ended June 30, 20X1 and 20X2: At the end of 20X1, management decided to increase its investment in control costs by 50% for each categorys items, with the expectation that failure costs would decrease by 20% for each item of the failure categories. Sales were 6,000,000 for both 20X1 and 20X2. Required: 1. Calculate the budgeted costs for 20X2, and prepare an interim quality performance report. 2. Comment on the significance of the report. How much progress has Andresen made?arrow_forwardGagnon Company reported the following sales and quality costs for the past four years. Assume that all quality costs are variable and that all changes in the quality cost ratios are due to a quality improvement program. Required: 1. Compute the quality costs for all four years. By how much did net income increase from Year 1 to Year 2 because of quality improvements? From Year 2 to Year 3? From Year 3 to Year 4? 2. The management of Gagnon Company believes it is possible to reduce quality costs to 2.5 percent of sales. Assuming sales will continue at the Year 4 level, calculate the additional profit potential facing Gagnon. Is the expectation of improving quality and reducing costs to 2.5 percent of sales realistic? Explain. 3. Assume that Gagnon produces one type of product, which is sold on a bid basis. In Years 1 and 2, the average bid was 400. In Year 1, total variable costs were 250 per unit. In Year 3, competition forced the bid to drop to 380. Compute the total contribution margin in Year 3 assuming the same quality costs as in Year 1. Now, compute the total contribution margin in Year 3 using the actual quality costs for Year 3. What is the increase in profitability resulting from the quality improvements made from Year 1 to Year 3?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Excel Applications for Accounting Principles

Accounting

ISBN:9781111581565

Author:Gaylord N. Smith

Publisher:Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

Cost Classifications - Managerial Accounting- Fixed Costs Variable Costs Direct & Indirect Costs; Author: Accounting Instruction, Help, & How To;https://www.youtube.com/watch?v=QQd1_gEF1yM;License: Standard Youtube License