EP FINANCIAL+MANAGERIAL ACCT. >CUSTOM<

5th Edition

ISBN: 9781323590287

Author: *ST.LEO UNIV.

Publisher: PEARSON C

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 19, Problem 34AP

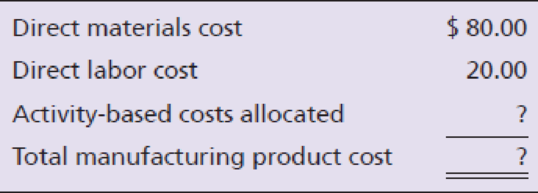

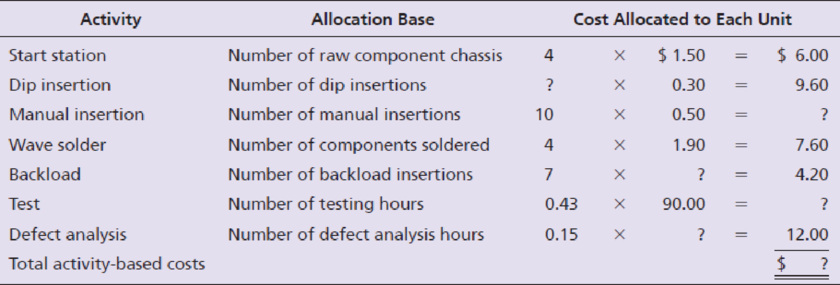

The Alright Manufacturing Company in Rochester, Minnesota, assembles and tests electronic components used in smartphones. Consider the following data regarding component T24 (amounts are per unit):

The activities required to build the component follow:

Requirements

- 1. Complete the missing items for the two tables.

- 2. Why might managers favor this ABC system instead of Alright’s older system, which allocated all

manufacturing overhead costs on the basis of direct labor hours?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Computing product costs in an ABC system

The Alright Manufacturing Company in Rochester, Minnesota, assembles and tests electronic components used in smartphones. Consider the following data regarding component T24 (amounts are per unit):

Requirements

Complete the missing items for the two tables.

Why might managers favor this ABC system instead of Alright’s older system, which allocated all manufacturing overhead costs on the basis of direct labor hours?

Computing product costs in an ABC system

The Alexander Manufacturing Company in Rochester, Minnesota, assembles and tests electronic components used in smartphones. Consider the following data regarding component T24 (amounts are per unit):

Requirements

Complete the missing items for the two tables.

Why might managers favor this ABC system instead of Alexander-’s older system, which allocated all manufacturing overhead costs on the basis of direct labor hours?

The Bangor Manufacturing Company makes mechanical toy robots that are typically produced in batches of 250 units. Prior to the current year, the company’s accountants used a standard cost system with a simplified method of assigning manufacturing support (i.e., overhead) costs to products: All such costs were allocated to outputs based on the standard machine hours allowed for output produced. You have recently joined the accounting team and are developing a proposal that the company adopt an ABC system for both product-costing and control purposes. To illustrate the benefit of such a system in terms of the latter, you decide to put together an analysis of batch-related overhead costs. You chose these costs because a previous investigation indicated that there is both a variable component to these costs (materials plus power) plus a fixed component (depreciation and salaries). Last year’s budget indicated that the variable overhead cost per setup hour was $20.00 and that the fixed…

Chapter 19 Solutions

EP FINANCIAL+MANAGERIAL ACCT. >CUSTOM<

Ch. 19 - The Santos Shirt Company manufactures shirts in...Ch. 19 - Prob. 2TICh. 19 - Prob. 3TICh. 19 - Prob. 4TICh. 19 - Prob. 5TICh. 19 - Prob. 6TICh. 19 - Prob. 7TICh. 19 - Prob. 8TICh. 19 - Prob. 9TICh. 19 - Prob. 10TI

Ch. 19 - Prob. 11TICh. 19 - Prob. 12TICh. 19 - Which statement is false? a. Using a single...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It uses activity-based costing. Two of...Ch. 19 - Compute It can use ABC information for what...Ch. 19 - Prob. 6QCCh. 19 - Companies enjoy many benefits from using JIT....Ch. 19 - Which account is not used in JIT costing? a....Ch. 19 - The cost of lost future sales after a customer...Ch. 19 - Spending on testing a product before shipment to...Ch. 19 - What is the formula to compute the predetermined...Ch. 19 - How is the predetermined overhead allocation rate...Ch. 19 - Describe how a single plantwide overhead...Ch. 19 - Why is using a single plantwide overhead...Ch. 19 - Why is the use of departmental overhead allocation...Ch. 19 - What is activity-based management? How is it...Ch. 19 - How many cost pools are in an activity-based...Ch. 19 - What are the four steps to developing an...Ch. 19 - Why is ABC usually considered more accurate than...Ch. 19 - List two ways managers can use ABM to make...Ch. 19 - Define value engineering. How is it used to...Ch. 19 - Explain the difference between target price and...Ch. 19 - How can ABM be used by service companies?Ch. 19 - What is a just-in-time management system?Ch. 19 - Explain how the work cell manufacturing layout...Ch. 19 - What are the inventory accounts used in JIT...Ch. 19 - How is the Conversion Costs account used in JIT...Ch. 19 - Prob. 18RQCh. 19 - Which accounts are adjusted for the underallocated...Ch. 19 - Prob. 20RQCh. 19 - Prob. 21RQCh. 19 - Prevention is much cheaper than external failure....Ch. 19 - What are quality improvement programs?Ch. 19 - Prob. 24RQCh. 19 - Prob. 1SECh. 19 - The Oakman (Company (see Short Exercise S19-1) has...Ch. 19 - Activity-based costing requires four steps. List...Ch. 19 - Prob. 4SECh. 19 - Darby Corp. is considering the use of...Ch. 19 - The following information is provided for Orbit...Ch. 19 - Jaunkas Corp. manufactures mid-fi and hi-fi stereo...Ch. 19 - Spectrum Corp. makes two products: C and D. The...Ch. 19 - Refer to Short Exercise S19-8. Spectrum Corp....Ch. 19 - Haworth Company is a management consulting firm....Ch. 19 - Refer to Short Exercise S19-10. Haworth desires a...Ch. 19 - Prob. 12SECh. 19 - Prime Products uses a JIT management system to...Ch. 19 - Stegall, Inc. manufactures motor scooters. For...Ch. 19 - Koehler makes handheld calculators in two models:...Ch. 19 - Koehler (see Exercise E19-15) makes handheld...Ch. 19 - Koehler (see Exercise E19-15 and Exercise E19-16)...Ch. 19 - Franklin, Inc. uses activity-based costing to...Ch. 19 - Turbo Champs Corp. uses activity-based costing to...Ch. 19 - Eason Company manufactures wheel rims. The...Ch. 19 - Refer to Exercise E19-20. For 2019, Easons...Ch. 19 - Refer to Exercises E19-20 and E19-21. Controller...Ch. 19 - Treat Dog Collars uses activity-based costing....Ch. 19 - Western, Inc. is a technology consulting firm...Ch. 19 - Refer to Exercise E19-24. The president of Western...Ch. 19 - Prob. 26ECh. 19 - Refer to Exercise E19-26. Western desires a 20%...Ch. 19 - Lally, Inc. produces universal remote controls....Ch. 19 - Prob. 29ECh. 19 - Darrel Co. makes electronic components. Chris...Ch. 19 - Prob. 31ECh. 19 - Prob. 32ECh. 19 - Willitte Pharmaceuticals manufactures an...Ch. 19 - The Alright Manufacturing Company in Rochester,...Ch. 19 - Oscar, Inc. manufactures bookcases and uses an...Ch. 19 - Blanchette Plant Service completed a special...Ch. 19 - Low Range produces fleece jackets. The company...Ch. 19 - Stella, Inc. is using a costs-of-quality approach...Ch. 19 - Harcourt Pharmaceuticals manufactures an...Ch. 19 - The Alexander Manufacturing Company in Rochester,...Ch. 19 - Martin, Inc. manufactures bookcases and uses an...Ch. 19 - Rennie Plant Service completed a special...Ch. 19 - High Mountain produces fleece jackets. The company...Ch. 19 - Roxi, Inc. is using a costs-of-quality approach to...Ch. 19 - Download an Excel template for this problem online...Ch. 19 - This problem continues the Piedmont Computer...Ch. 19 - Prob. 1TIATCCh. 19 - Harris Systems specializes in servers for...Ch. 19 - Harris Systems has decided to adopt ABC. To remain...Ch. 19 - Prob. 1EICh. 19 - Anu Ghai was a new production analyst at RHI,...

Additional Business Textbook Solutions

Find more solutions based on key concepts

How would the decision to dispose of a segment of operations using a split-off rather than a spin-off impact th...

Advanced Financial Accounting

Bank loan; accrued interest LO132 On October 1, Eder Fabrication borrowed 60 million and issued a nine-month, ...

Intermediate Accounting

18. What is the calculation for return on assets (ROA)? Explain what ROA measures.

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

Discussion Analysis A13-41 Discussion Questions 1. How do managers use the statement of cash flows? 2. Describ...

Managerial Accounting (4th Edition)

Analysis of inventory errors A2 Hallam Company’s financial statements show the following. The company recently ...

FINANCIAL ACCT.FUND.(LOOSELEAF)

List five asset accounts, three liability accounts, and five expense accounts included in the acquisition and p...

Auditing and Assurance Services (16th Edition)

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Evans, Inc., has a unit-based costing system. Evanss Miami plant produces 10 different electronic products. The demand for each product is about the same. Although they differ in complexity, each product uses about the same labor time and materials. The plant has used direct labor hours for years to assign overhead to products. To help design engineers understand the assumed cost relationships, the Cost Accounting Department developed the following cost equation. (The equation describes the relationship between total manufacturing costs and direct labor hours; the equation is supported by a coefficient of determination of 60 percent.) Y=5,000,000+30X,whereX=directlaborhours The variable rate of 30 is broken down as follows: Because of competitive pressures, product engineering was given the charge to redesign products to reduce the total cost of manufacturing. Using the above cost relationships, product engineering adopted the strategy of redesigning to reduce direct labor content. As each design was completed, an engineering change order was cut, triggering a series of events such as design approval, vendor selection, bill of materials update, redrawing of schematic, test runs, changes in setup procedures, development of new inspection procedures, and so on. After one year of design changes, the normal volume of direct labor was reduced from 250,000 hours to 200,000 hours, with the same number of products being produced. Although each product differs in its labor content, the redesign efforts reduced the labor content for all products. On average, the labor content per unit of product dropped from 1.25 hours per unit to one hour per unit. Fixed overhead, however, increased from 5,000,000 to 6,600,000 per year. Suppose that a consultant was hired to explain the increase in fixed overhead costs. The consultants study revealed that the 30 per hour rate captured the unit-level variable costs; however, the cost behavior of other activities was quite different. For example, setting up equipment is a step-fixed cost, where each step is 2,000 setup hours, costing 90,000. The study also revealed that the cost of receiving goods is a function of the number of different components. This activity has a variable cost of 2,000 per component type and a fixed cost that follows a step-cost pattern. The step is defined by 20 components with a cost of 50,000 per step. Assume also that the consultant indicated that the design adopted by the engineers increased the demand for setups from 20,000 setup hours to 40,000 setup hours and the number of different components from 100 to 250. The demand for other non-unit-level activities remained unchanged. The consultant also recommended that management take a look at a rejected design for its products. This rejected design increased direct labor content from 250,000 hours to 260,000 hours, decreased the demand for setups from 20,000 hours to 10,000 hours, and decreased the demand for purchasing from 100 component types to 75 component types, while the demand for all other activities remained unchanged. Required: 1. Using normal volume, compute the manufacturing cost per labor hour before the year of design changes. What is the cost per unit of an average product? 2. Using normal volume after the one year of design changes, compute the manufacturing cost per hour. What is the cost per unit of an average product? 3. Before considering the consultants study, what do you think is the most likely explanation for the failure of the design changes to reduce manufacturing costs? Now use the information from the consultants study to explain the increase in the average cost per unit of product. What changes would you suggest to improve Evanss efforts to reduce costs? 4. Explain why the consultant recommended a second look at a rejected design. Provide computational support. What does this tell you about the strategic importance of cost management?arrow_forwardThe management of Wheeler Company has decided to develop cost formulas for its major overhead activities. Wheeler uses a highly automated manufacturing process, and power costs are a significant manufacturing cost. Cost analysts have decided that power costs are mixed; thus, they must be broken into their fixed and variable elements so that the cost behavior of the power usage activity can be properly described. Machine hours have been selected as the activity driver for power costs. The following data for the past eight quarters have been collected: Required: 1. Prepare a scattergraph by plotting power costs against machine hours. Does the scatter-graph show a linear relationship between machine hours and power cost? 2. Using the high and low points, compute a power cost formula. 3. Use the method of least squares to compute a power cost formula. Evaluate the coefficient of determination. 4. Rerun the regression and drop the point (20,000; 26,000) as an outlier. Compare the results from this regression to those for the regression in Requirement 3. Which is better?arrow_forwardSilven Company has identified the following overhead activities, costs, and activity drivers for the coming year: Silven produces two models of cell phones with the following expected activity demands: 1. Determine the total overhead assigned to each product using the four activity drivers. 2. Determine the total overhead assigned to each model using the two most expensive activities. The costs of the two relatively inexpensive activities are allocated to the two expensive activities in proportion to their costs. 3. Using ABC as the benchmark, calculate the percentage error and comment on the accuracy of the reduced system. Explain why this approach may be desirable.arrow_forward

- Southward Company has implemented a JIT flexible manufacturing system. John Richins, controller of the company, has decided to reduce the accounting requirements given the expectation of lower inventories. For one thing, he has decided to treat direct labor cost as a part of overhead and to discontinue the detailed direct labor accounting of the past. The company has created two manufacturing cells, each capable of producing a family of products: the radiator cell and the water pump cell. The output of both cells is sold to a sister division and to customers who use the radiators and water pumps for repair activity. Product-level overhead costs outside the cells are assigned to each cell using appropriate drivers. Facility-level costs are allocated to each cell on the basis of square footage. The budgeted direct labor and overhead costs are as follows: The predetermined conversion cost rate is based on available production hours in each cell. The radiator cell has 45,000 hours available for production, and the water pump cell has 27,000 hours. Conversion costs are applied to the units produced by multiplying the conversion rate by the actual time required to produce the units. The radiator cell produced 81,000 units, taking 0.5 hour to produce one unit of product (on average). The water pump cell produced 90,000 units, taking 0.25 hour to produce one unit of product (on average). Other actual results for the year are as follows: All units produced were sold. Any conversion cost variance is closed to Cost of Goods Sold. Required: 1. Calculate the predetermined conversion cost rates for each cell. 2. Prepare journal entries using backflush accounting. Assume two trigger points, with completion of goods as the second trigger point. 3. Repeat Requirement 2, assuming that the second trigger point is the sale of the goods. 4. Explain why there is no need to have a work-in-process inventory account. 5. Two variants of backflush costing were presented in which each used two trigger points, with the second trigger point differing. Suppose that the only trigger point for recognizing manufacturing costs occurs when the goods are sold. How would the entries be listed here? When would this backflush variant be considered appropriate?arrow_forwardBrees, Inc., a manufacturer of golf carts, has just received an offer from a supplier to provide 2,600 units of a component used in its main product. The component is a track assembly that is currently produced internally. The supplier has offered to sell the track assembly for 66 per unit. Brees is currently using a traditional, unit-based costing system that assigns overhead to jobs on the basis of direct labor hours. The estimated traditional full cost of producing the track assembly is as follows: Prior to making a decision, the companys CEO commissioned a special study to see whether there would be any decrease in the fixed overhead costs. The results of the study revealed the following: 3 setups1,160 each (The setups would be avoided, and total spending could be reduced by 1,160 per setup.) One half-time inspector is needed. The company already uses part-time inspectors hired through a temporary employment agency. The yearly cost of the part-time inspectors for the track assembly operation is 12,300 and could be totally avoided if the part were purchased. Engineering work: 470 hours, 45/hour. (Although the work decreases by 470 hours, the engineer assigned to the track assembly line also spends time on other products, and there would be no reduction in his salary.) 75 fewer material moves at 30 per move. Required: 1. Ignore the special study, and determine whether the track assembly should be produced internally or purchased from the supplier. 2. Now, using the special study data, repeat the analysis. 3. Discuss the qualitative factors that would affect the decision, including strategic implications. 4. After reviewing the special study, the controller made the following remark: This study ignores the additional activity demands that purchasing would cause. For example, although the demand for inspecting the part on the production floor decreases, we may need to inspect the incoming parts in the receiving area. Will we actually save any inspection costs? Is the controller right?arrow_forwardGeneva, Inc., makes two products, X and Y, that require allocation of indirect manufacturing costs. The following data were compiled by the accountants before making any allocations: The total cost of purchasing and receiving parts used in manufacturing is 60,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were 48,000 and 12,000 for X and Y, respectively. If an activity-based system is used, what would be the allocated costs for each product?arrow_forward

- Bumblebee Mobiles manufactures a line of cell phones. The management has identified the following overhead costs and related cost drivers for the coming year. The following were incurred in manufacturing two of their cell phones, Bubble and Burst, during the first quarter. REQUIREMENT Review the worksheet called ABC that follows these requirements. You have been asked to determine the cost of each product using an activity-based cost system. Note that the problem information is already entered into the Data Section of the ABC worksheet.arrow_forwardRandy Harris, controller, has been given the charge to implement an advanced cost management system. As part of this process, he needs to identify activity drivers for the activities of the firm. During the past four months, Randy has spent considerable effort identifying activities, their associated costs, and possible drivers for the activities costs. Initially, Randy made his selections based on his own judgment using his experience and input from employees who perform the activities. Later, he used regression analysis to confirm his judgment. Randy prefers to use one driver per activity, provided that an R2 of at least 80 percent can be produced. Otherwise, multiple drivers will be used, based on evidence provided by multiple regression analysis. For example, the activity of inspecting finished goods produced an R2 of less than 80 percent for any single activity driver. Randy believes, however, that a satisfactory cost formula can be developed using two activity drivers: the number of batches and the number of inspection hours. Data collected for a 14-month period are as follows: Required: 1. Calculate the cost formula for inspection costs using the two drivers, inspection hours and number of batches. Are both activity drivers useful? What does the R2 indicate about the formula? 2. Using the formula developed in Requirement 1, calculate the inspection cost when 300 inspection hours are used and 30 batches are produced. Prepare a 90 percent confidence interval for this prediction.arrow_forwardBig Mikes, a large hardware store, has gathered data on its overhead activities and associated costs for the past 10 months. Nizam Sanjay, a member of the controllers department, believes that overhead activities and costs should be classified into groups that have the same driver. He has decided that unloading incoming goods, counting goods, and inspecting goods can be grouped together as a more general receiving activity, since these three activities are all driven by the number of receiving orders. The 10 months of data shown below have been gathered for the receiving activity. Required: 1. Prepare a scattergraph, plotting the receiving costs against the number of purchase orders. Use the vertical axis for costs and the horizontal axis for orders. 2. Select two points that make the best fit, and compute a cost formula for receiving costs. 3. Using the high-low method, prepare a cost formula for the receiving activity. 4. Using the method of least squares, prepare a cost formula for the receiving activity. What is the coefficient of determination?arrow_forward

- Anderson Company has the following departmental manufacturing structure for one of its products: After some study, the production manager of Anderson recommended the following revised cellular manufacturing approach: Required: 1. Calculate the total time it takes to produce a batch of 20 units using Andersons traditional departmental structure. 2. Using cellular manufacturing, how much time is saved producing the same batch of 20 units? Assuming the cell operates continuously, what is the production rate? Which process controls this production rate? 3. What if the processing times of molding, welding, and assembly are all reduced to six minutes each? What is the production rate now, and how long will it take to produce a batch of 20 units?arrow_forwardThe PC Works assembles custom computers from components supplied by various manufacturers. The company is very small and its assembly shop and retail sales store are housed in a single facility in a Redmond, Washington, industrial park. Listed below are some of the costs that are incurred at the company. Required: For each cost, indicate whether it would most likely be classified as direct labor, direct materials ,manufacturing overhead, selling, or an administrative cost. The cost of a hard drive installed in a computer. The cost of advertising in the Puget Sound Computer User newspaper. The wages of employees who assemble computers from components. Sales commissions paid to the company’s salespeople. The wages of the assembly shop’s supervisor. The wages of the company’s accountant. Depreciation on equipment used to test assembled computers before release to customers. 8. Rent on the facility in the industrial park.arrow_forwardThe PC Works assembles custom computers from components supplied by various manufacturers. The company is very small and its assembly shop and retail sales store are housed in a single facility in a Redmond, Washington, industrial park. Listed below are some of the costs that are incurred at the company.Required:For each cost, indicate whether it would most likely be classified as direct materials, direct labor, manufacturing overhead, selling, or an administrative cost.1. The cost of a hard drive installed in a computer.2. The cost of advertising in the Puget Sound Computer User newspaper.3. The wages of employees who assemble computers from components.4. Sales commissions paid to the company’s salespeople.5. The salary of the assembly shop’s supervisor.6. The salary of the company’s accountant.7. Depreciation on equipment used to test assembled computers before release to customers.8. Rent on the facility in the industrial park.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Excel Applications for Accounting Principles

Accounting

ISBN:9781111581565

Author:Gaylord N. Smith

Publisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Cost Accounting - Definition, Purpose, Types, How it Works?; Author: WallStreetMojo;https://www.youtube.com/watch?v=AwrwUf8vYEY;License: Standard YouTube License, CC-BY