Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN: 9781337788281

Author: James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 22, Problem 8E

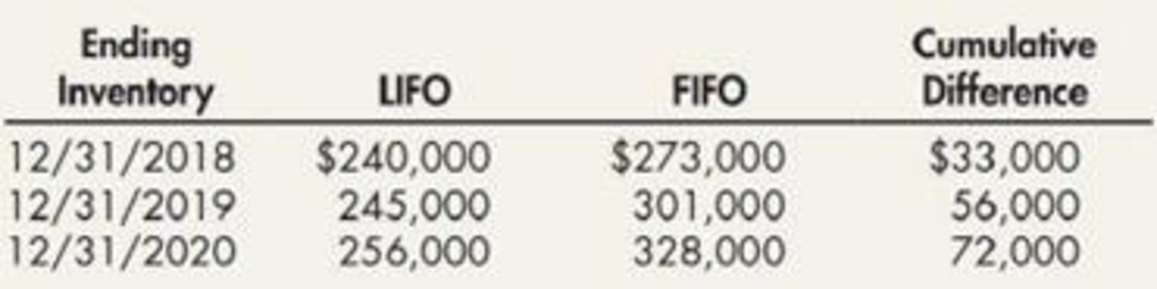

In 2020, Frost Company, which began operations in 2018, decided to change from LIFO to FIFO because management believed that FIFO belter represented the flow of their inventory. Management prepared the following analysis showing the effect of this change:

Frost reported net income of $2,500,000, $2,400,000, and $2,100,000 in 2018, 2019, and 2020, respectively. The tax rate is 21%.

Required:

- 1. Prepare the

journal entry necessary to record the change. - 2. What amount of net income would Frost report in 2018, 2019, and 2020?

- 3. If Frost’s employees received a bonus of 10% of income before deducting the bonus and income taxes in 2018 and 2019, what would be the effect on net income for 2018, 2019, and 2020?

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Now assume that Syer does account for its NOL under the CARES Act. Prepare the appropriate journal entry to record Syer’s 2020 income taxes, and indicate Syer’s 2020 net income(loss).

Syer Company reports net operating income (loss) for financial reporting and tax purposes in each year as follows ($ in millions):

2016

2017

2018

2019

2020

$ 330)

$ 130

$ 0

$0

$ (660)

Syer’s 2020 NOL is driven by an unfortunate obsolescence of its primary product. Given great uncertainty in Syer’s future profitability, Syer’s management does not believe it is more likely than not that it will be able to realize deferred tax assets in future years. Syer’s federal tax rate decreased from 35% to 21% starting in 2018.

Kucing Garong Construction Company decided at the beginning of 2020 to change from the cost recovery method to the percentage-of-completion method for financial reporting purposes. The company will continue to use the cost-recovery method for tax purposes. For years prior to 2020, pretax income under the two methods was as follows: percentage-of-completion £144,000, and cost-recovery £114,000. The tax rate is 35%. Kucing Garong has a profit-sharing plan, which pays all employees a bonus at year-end based on 1.5% of pretax income. What is the amount of the indirect effect of Kucing Garong’s change in accounting policy that will be reported in the 2020 income statement, assuming that the profit-sharing contract explicitly requires adjustment for changes in income numbers?

Jacob, Inc., changed from the average cost to the FIFO cost flow assumption in 2019. The increase in the prior year's income before taxes is €1,100,000. The tax rate is 35%. Jacob's 2019 journal entry to record the change in accounting policy will include. a. a debit to Retained Earnings for €1,100,000. b. a credit to Retained Earnings for €1,100,000. a debit to Inventory for €715,000. C. a credit to Deferred Tax Liability for €385,000

Chapter 22 Solutions

Intermediate Accounting: Reporting And Analysis

Ch. 22 - Prob. 1GICh. 22 - Prob. 2GICh. 22 - Prob. 3GICh. 22 - What steps are necessary to apply the...Ch. 22 - Prob. 5GICh. 22 - Prob. 6GICh. 22 - Prob. 7GICh. 22 - Prob. 8GICh. 22 - Define a change in estimate. What is the proper...Ch. 22 - Prob. 10GI

Ch. 22 - How is a change in depreciation method accounted...Ch. 22 - Describe a change in a reporting entity. How does...Ch. 22 - Prob. 13GICh. 22 - Prob. 14GICh. 22 - Prob. 15GICh. 22 - Prob. 16GICh. 22 - Prob. 17GICh. 22 - Prob. 18GICh. 22 - Prob. 19GICh. 22 - Prob. 20GICh. 22 - The cumulative effect of an accounting change...Ch. 22 - When a change in accounting principle is made...Ch. 22 - Prob. 3MCCh. 22 - A change in the expected service life of an asset...Ch. 22 - During 2019, White Company determined that...Ch. 22 - Generally, how should a change in accounting...Ch. 22 - On January 2, 2017, Garr Company acquired...Ch. 22 - A company has included in its consolidated...Ch. 22 - Shannon Corporation began operations on January 1,...Ch. 22 - Shannon Corporation began operations on January 1,...Ch. 22 - Prob. 1RECh. 22 - Heller Company began operations in 2019 and used...Ch. 22 - Refer to RE22-2. Assume the pretax cumulative...Ch. 22 - Refer to RE22-2. Assume Heller Company had sales...Ch. 22 - Bloom Company had beginning unadjusted retained...Ch. 22 - Suppose that Blake Companys total pretax...Ch. 22 - Bliss Company owns an asset with an estimated life...Ch. 22 - At the end of 2019, Framber Company received 8,000...Ch. 22 - At the end of 2019, Cortex Company failed to...Ch. 22 - At the end of 2019, Jayrad Company paid 6,000 for...Ch. 22 - At the end of 2019, Manny Company recorded its...Ch. 22 - Abrat Company failed to accrue an allowance for...Ch. 22 - The following are independent events: a. Changed...Ch. 22 - Prob. 2ECh. 22 - The following are independent events: a. A...Ch. 22 - Change in Inventory Cost Flow Assumption At the...Ch. 22 - Fava Company began operations in 2018 and used the...Ch. 22 - Berg Company began operations on January 1, 2019,...Ch. 22 - Prob. 7ECh. 22 - In 2020, Frost Company, which began operations in...Ch. 22 - Gundrum Company purchased equipment on January 1,...Ch. 22 - Prob. 10ECh. 22 - On January 1, 2014, Klinefelter Company purchased...Ch. 22 - The following are independent errors made by a...Ch. 22 - The following are independent errors made by a...Ch. 22 - Refer to the information in E22-13. Required:...Ch. 22 - The following are independent errors: a. In...Ch. 22 - Dudley Company failed to recognize the following...Ch. 22 - Prob. 1PCh. 22 - Prob. 2PCh. 22 - Koopman Company began operations on January 1,...Ch. 22 - Schmidt Company began operations on January 1,...Ch. 22 - Prob. 5PCh. 22 - Kraft Manufacturing Company manufactures two...Ch. 22 - Jackson Company has decided to issue common stock...Ch. 22 - At the beginning of 2020, Holden Companys...Ch. 22 - At the end of 2020, while auditing Sandlin...Ch. 22 - At the beginning of 2020, Tanham Company...Ch. 22 - A review of Anderson Corporations books indicates...Ch. 22 - Prob. 12PCh. 22 - Gray Companys financial statements showed income...Ch. 22 - Prob. 14PCh. 22 - There are three types of accounting changes:...Ch. 22 - Prob. 2CCh. 22 - Berkeley Company, a manufacturer of many different...Ch. 22 - When the FASB issues a new generally accepted...Ch. 22 - It is important in accounting theory to be able to...Ch. 22 - Prob. 6CCh. 22 - Prob. 7CCh. 22 - Prob. 8CCh. 22 - Prob. 9CCh. 22 - Sometimes a business entity may change its method...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Heller Company began operations in 2019 and used the LIFO method to compute its 300,000 cost of goods sold for that year. At the beginning of 2020, Heller changed to the FIFO method. Heller determined that its cost of goods sold under FIFO would have been 250,000 in 2019. For 2020, Hellers cost of goods sold under FIFO was 360,000, while it would have been 410,000 under LIFO. Heller is subject to a 21% income tax rate. Compute the cumulative effect of the retrospective adjustment on prior years income (net of taxes) that Heller would report on its retained earnings statement for 2020.arrow_forwardBerg Company began operations on January 1, 2019, and uses the FIFO method in costing its raw materials inventory. During 2020, management is contemplating a change to the LIFO method and is interested in determining what effect such a change will have on net income. Accordingly, the following information has been developed: Required: What is the effect on income before income taxes in 2020 of a change to the LIFO method?arrow_forwardFava Company began operations in 2018 and used the LIFO inventory method for both financial reporting and income taxes. At the beginning of 2019, the anticipated cost trends in the industry had changed, so that it adopted the FIFO method for both financial reporting and income taxes. Fava reported revenues of 300,000 and 270,000 in 2019 and 2018, respectively. Fava reported expenses (excluding income tax expense) of 125,000 and 120,000 in 2019 and 2018, which included cost of goods sold of 55,000 and 45,000, respectively. An analysis indicates that the FIFO cost of goods sold would have been lower by 8,000 in 2018. The tax rate is 21%. Fava has a simple capital structure with 15,000 shares of common stock outstanding during 2018 and 2019. It paid no dividends in either year. Required: 1. Prepare the journal entry to reflect the change. 2. At the end of 2019, prepare the comparative income statements for 2019 and 2018. Notes to the financial statements are not necessary. 3. At the end of 2019, prepare the comparative retained earnings statements for 2019 and 2018.arrow_forward

- Schmidt Company began operations on January 1, 2018, and used the LIFO inventory method for both financial reporting and income taxes. However, at the beginning of 2020, Schmidt decided to switch to the average cost inventory method for financial and income tax reporting. It had previously reported the following financial statement information for 2019: An analysis of the accounting records discloses the following cost of goods sold under the LIFO and average cost inventory methods: There are no indirect effects of the change in inventory method. Revenues for 2020 total 130,000; operating expenses for 2020 total 30,000. Schmidt is subject to a 21% income tax rate in all years; it pays all income taxes payable in the next quarter. Assume that any deferred tax liability was paid in the subsequent year. Schmidt had 10,000 shares of common stock outstanding during all years; it paid dividends of 1 per share in 2020. At the end of 2020, Schmidt had cash of 15,600, inventory of 34,000, other assets of 76,000, income taxes payable of 4,200, and accounts payable of 3,000. It desires to show financial statements for the current year and previous year in its 2020 annual report. Required: 1. Prepare the journal entry to reflect the change in method at the beginning of 2020. Show supporting calculations. 2. Prepare the 2020 financial statements. Notes to the financial statements are not necessary. Show supporting calculations.arrow_forwardKoopman Company began operations on January 1, 2018, and uses they FIFO inventory method for financial reporting and the average cost inventory method for income taxes. At the beginning of 2020, Koopman decided to switch to the average cost inventory method for financial reporting. It had previously reported the following financial statement information for 2019: An analysis of the accounting records discloses the following cost of goods sold under the FIFO and average cost inventory methods: There are no indirect effects of the change in inventory method. Revenues for 2020 total 130,000; operating expenses for 2020 total 30,000. Koopman is subject to a 21% income tax rate in all years; it pays the income taxes payable of a current year in the first quarter of the next year. Koopman had 10,000 shares of common stock outstanding during all years; it paid dividends of 1 per share in 2020. At the end of 2020, Koopman had cash of 10,000, inventory of 24,000, other assets of 70,800, accounts payable of 4,500, and income taxes payable of 6,000. It desires to show financial statements for the current year and previous year in its 2020 annual report. Required: 1. Prepare the journal entry to reflect the change in methods at the beginning of 2020. Show supporting calculations. 2. Prepare the 2020 financial statements. Notes to the financial statements are not necessary. Show supporting calculations.arrow_forwardAt the end of 2019, Manny Company recorded its ending inventory at 350,000 based on a physical count. During 2020, the company discovered that the correct inventory value at the end of 2019 should have been 400,000 because it made a counting error. Upon discovery of this error in 2020, what correcting journal entry will Manny make? Ignore income taxes.arrow_forward

- Brooks Company reported a prior period adjustment of 512,000 in pretax financial "income" and taxable income for 2020. The prior period adjustment was the result of an error in calculating bad debt expense for 2019. The current tax rate is 30%, and no change in the tax rate has been enacted for future years. When the company applies intraperiod income tax allocation, the prior period adjustment will be shown on the: a. income statement at 12,000 b. income statement at 8,400 (net of 3,600 income taxes) c. retained earnings statement at 12,000 d. retained earnings statement at 8,400 (net of 3,600 income taxes)arrow_forwardKraft Manufacturing Company manufactures two products: Mult and Tran. At December 31, 2019, Kraft used the FIFO inventory method. Effective January 1, 2020, Kraft changed to the LIFO inventory method. The cumulative effect of this change is not determinable, and, as a result, the ending inventory of 2019, for which the FIFO method was used, is also the beginning inventory for 2020 for the LIFO method. Any layers added during 2020 should be costed by reference to the first acquisitions of 2020, and any layers liquidated during 2020 should be considered a permanent liquidation. The following information was available from Krafts inventory records for the two most recent years: Required: Compute the effect on income before income taxes for the year ended December 31, 2020, resulting from the change from the FIFO to the LIFO inventory method.arrow_forwardPierce Corporation has the following gross profits for 2018 and 2019: Sales = 2019 - P810,000; 2018 - P792,000. Cost of sales = 2019 - 480,000; 2018 - 464,000. Gross profit = 2019 - P330,000; 2018 - P328,000. Sales price was 10% lower during 2019. The percent of increase (decrease) in cost price must be: The owners would like to know what reasons caused the current performance of the company and ask your opinion. Through review of the complete records you were able to obtain this additional information: (1) The selling price for every unit is P7.20 during 2018 and; (2) The marketing department did a tremendous job and was able to increase sales units by 20% during 2019. The increase (decrease) in gross profit because of the change in sales price is: a. P900 b. P1,080 c. (P4,320) d. P15,480arrow_forward

- Pierce Corporation has the following gross profits for 2018 and 2019: Sales = 2019 - P810,000; 2018 - P792,000. Cost of sales = 2019 - 480,000; 2018 - 464,000. Gross profit = 2019 - P330,000; 2018 - P328,000. Sales price was 10% lower during 2019. The percent of increase (decrease) in cost price must be: The owners would like to know what reasons caused the current performance of the company and ask your opinion. Through review of the complete records you were able to obtain this additional information: (1) The selling price for every unit is P7.20 during 2018 and; (2) The marketing department did a tremendous job and was able to increase sales units by 20% during 2019. The increase (decrease) in gross profit because of the change in unit cost is: a. (P19,000) b. P10,800 c. (P10,800) d. P9,000arrow_forwardIn its proposed 2020 income statement, Hrabik Corporation reports income before income taxes $ 505,000, income taxes $ 146,450 (not including unusual items), loss on operation of discontinued music division $ 58,000, gain on disposal of discontinued music division $ 40,000, and unrealized loss on available-for-sale securities $ 150,000. The income tax rate is 29%.Prepare a correct statement of comprehensive income, beginning with income before income taxesarrow_forwardAt Carla Vista Co., events and transactions during 2020 included the following. The tax rate for all items is 20%.(1) Depreciation for 2018 was found to be understated by $120500.(2) A strike by the employees of a supplier resulted in a loss of $100800.(3) The inventory at December 31, 2018 was overstated by $169800.(4) A disposal of a component of the business resulted in a $1985000 loss.The effect of these events and transactions on 2020 net income net of tax would bearrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Individual Income Taxes

Accounting

ISBN:9780357109731

Author:Hoffman

Publisher:CENGAGE LEARNING - CONSIGNMENT

Accounting Changes and Error Analysis: Intermediate Accounting Chapter 22; Author: Finally Learn;https://www.youtube.com/watch?v=c2uQdN53MV4;License: Standard Youtube License