Concept explainers

Videos

Cost of production report

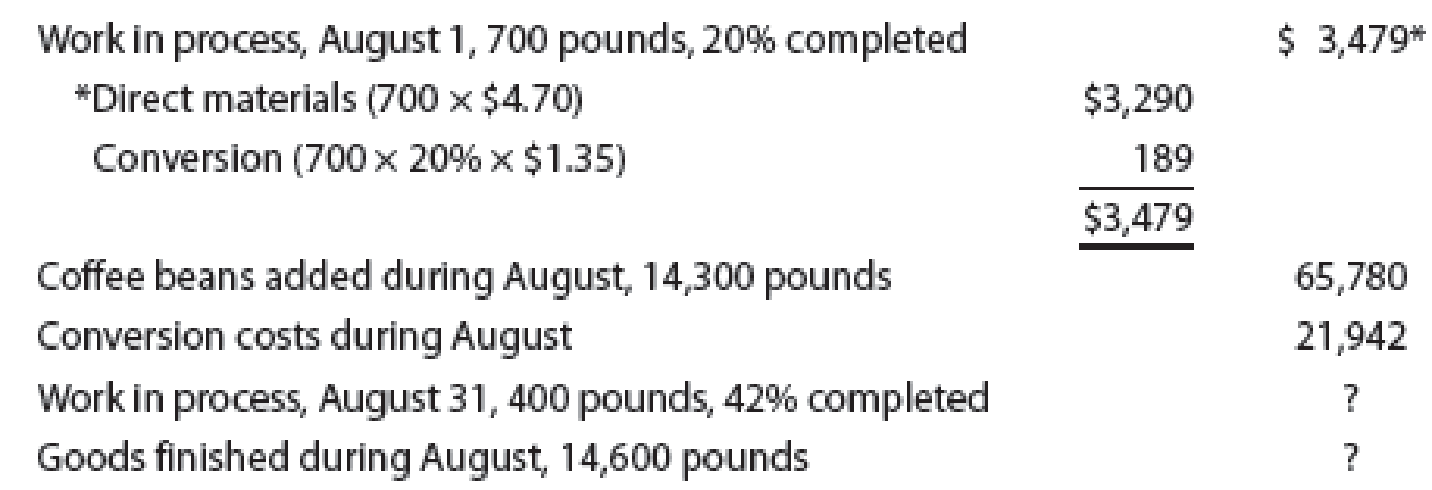

The debits to Work in Process—Roasting Department for Morning Brew Coffee Company for August, together with information concerning production, are as follows:

All direct materials are placed in process at the beginning of production.

- A. Prepare a cost of production report, presenting the following computations:

- 1. Direct materials and conversion equivalent units of production for August

- 2. Direct materials and conversion costs per equivalent unit for August

- 3. Cost of goods finished during August

- 4. Cost of work in process at August 31

- B. Compute and evaluate the change in cost per equivalent unit for direct materials and conversion from the previous month (July).

A. (1)

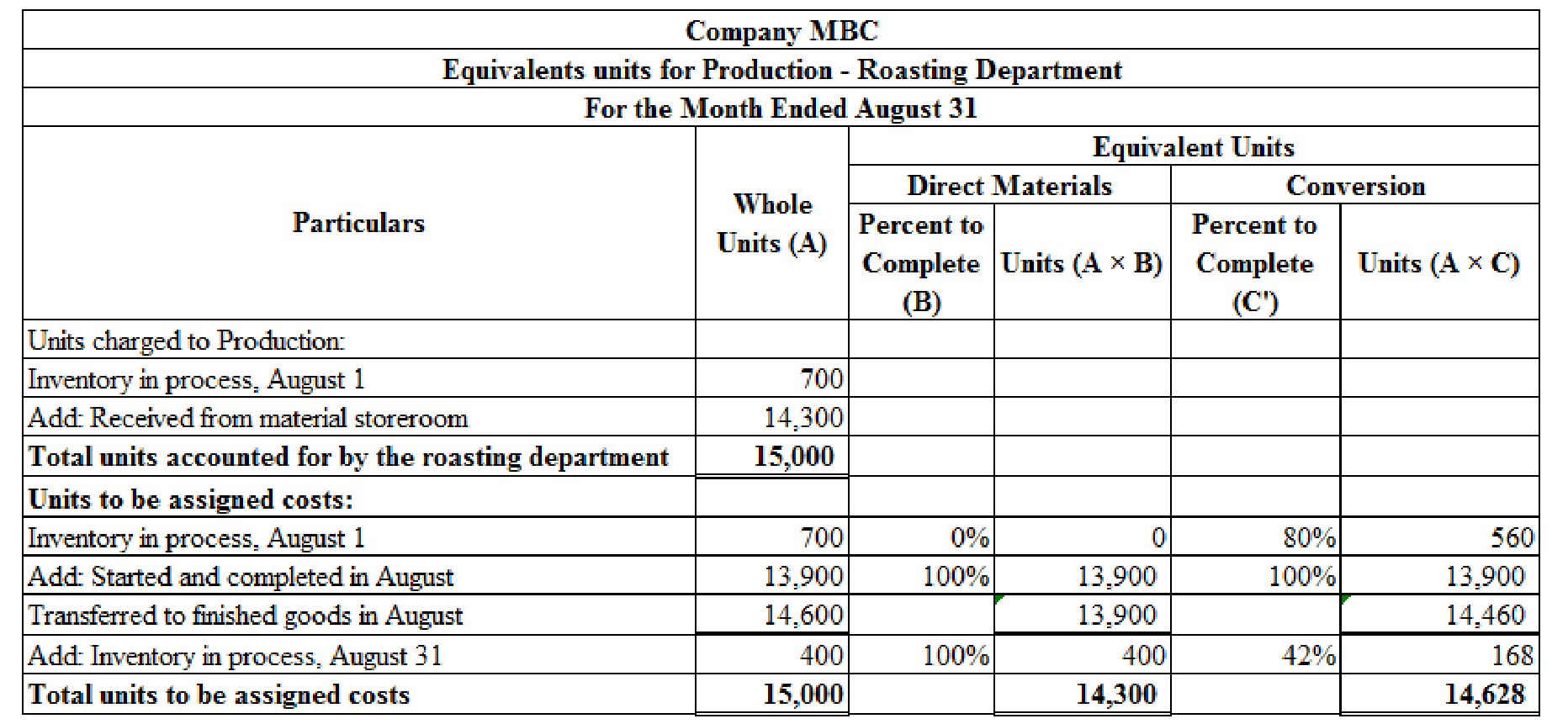

Calculate the equivalents units for production of direct materials and conversion costs for the month of August for Company MBC.

Explanation of Solution

Process costs

It is a method of cost accounting, which is used where the production is continuous, and the product needs various processes to complete. This method is used to ascertain the cost of the product at each process or stage of production.

Equivalents units for production

The activity of a processing department in terms of fully completed units is known as equivalent units. It includes the completed units of direct materials and conversion cost of beginning work in process, units completed and transferred out, and ending work in process.

Production cost report

A production cost report is a comprehensive report prepared for each department separately at the end of a particular period, which represents the physical flow and cost flow of product for the concerned department.

Calculate the equivalents units for production of direct materials and conversion costs for the month of August for Company MBC as shown below:

Figure (1)

Working note (1):

Calculate opening work in process inventory for conversion costs as shown below:

Working note (2):

Calculate units started and completed in August as shown below:

Working note (3):

Calculate ending work in process inventory for conversion costs as shown below:

Equivalent units for production is calculated by adding units of opening work in process inventory, transferred to finished goods in august, and units for ending work in process inventory. Therefore, an equivalents unit for production for direct materials is 14,300 units and equivalent units for production for conversion costs is 14,628 units.

A. (2)

Calculate the direct materials and conversion cost equivalent cost per unit for August.

Explanation of Solution

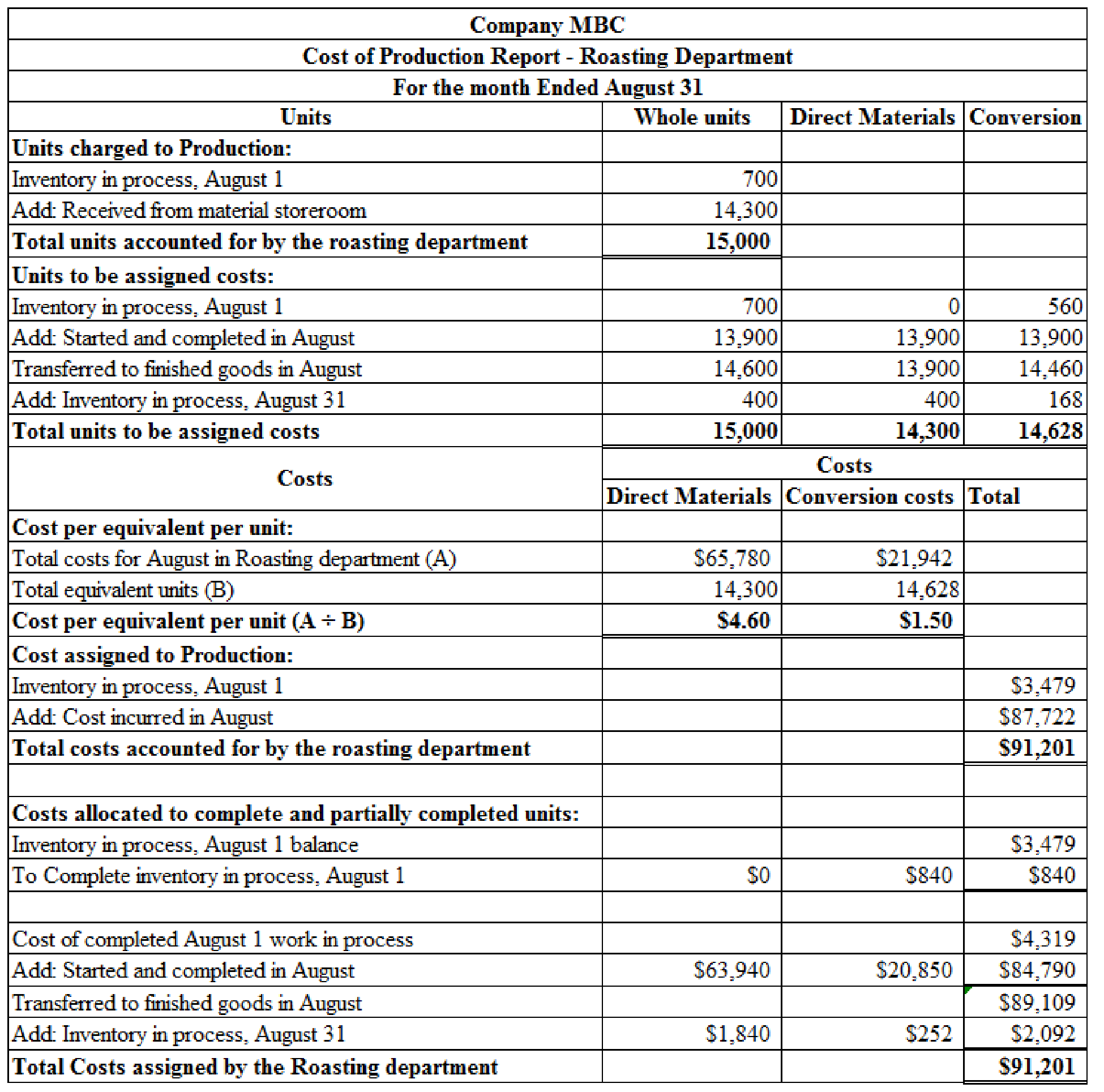

Calculate direct materials and conversion cost equivalent cost per unit for August as shown below:

Direct material cost per unit is calculated by dividing total direct materials cost by equivalent units for direct materials. Hence, direct material cost per unit is $4.60 per unit. Conversion cost per unit is calculated by dividing total conversion costs by equivalent units for conversion. Hence, conversion cost per unit is $1.50 per unit.

A. (3)

Calculate the cost of goods finished during the month of august.

Explanation of Solution

Calculate the cost of goods finished during the month of August as shown below:

| Particulars | Units (A) | Per unit (B) | Amount (A × B) |

| Inventory in process, August 1 balance | $3,479 | ||

| Add: Cost of completed August 1, Work in process | |||

| Direct materials | 0 | $4.60 | $0 |

| Conversion | 560 | $1.50 | $840 |

| Add: Transferred to finished goods in August: | |||

| Direct materials | 13,900 | $4.60 | $63,940 |

| Conversion | 13,900 | $1.50 | $20,850 |

| Cost of Goods finished during August | $89,109 |

Table (1)

Cost of goods finished during the month of august is calculated by adding opening inventory balance, cost of opening work in process inventory, and transferred to finished goods during the period of August. Therefore, cost of goods finished during the august is $89,109.

A. (4)

Calculate the cost of ending work in process inventory during the month of August.

Explanation of Solution

Calculate the cost of ending work in process inventory during the month of August as shown below:

| Particulars | Units (A) | Per unit (B) | Amount (A × B) |

| Inventory in process, August 31, balance | |||

| Direct materials | 400 | $4.60 | $1,840 |

| Conversion | 168 | $1.50 | $252 |

| Cost of ending work in process inventory | $2,092 |

Table (2)

Cost of ending work in process inventory is calculated by adding ending work in process inventory for both direct materials and conversion costs. Hence, cost of ending work in process inventory is $2,092.

Cost of production report for Company MBC as shown below:

Figure (2)

B.

Calculate the change in cost per equivalent unit for direct material and conversion cost comparing with July month.

Explanation of Solution

Calculate change in cost per equivalent unit for direct material and conversion cost during the month of July as shown below:

| Particulars | Per unit |

| Cost per unit for August | $4.60 |

| Less: Cost per unit for July | $4.70 |

| Decrease in direct material per unit | ($0.10) |

Table (3)

| Particulars | Per unit |

| Cost per unit for August | $1.50 |

| Less: Cost per unit for July | $1.35 |

| Increase in conversion cost per unit | $0.15 |

Table (4)

Change in cost per equivalent unit is calculated by deducting previous month cost per unit from current month cost per unit. Direct material is decreased by $0.10. Conversion cost per unit is increased by $0.15 per unit. Company MBC might be asking to scrutinize the reasons for the rise in the conversion cost in the current month.

Want to see more full solutions like this?

Chapter 3 Solutions

Managerial Accounting

- The following information concerns production in the Finishing Department for May. The Finishing Department uses the weighted average method. a. Determine the number of units in work in process inventory at the end of the month. b. Determine the number of whole units to be accounted for and to be assigned costs and the equivalent units of production for May. Assume that direct materials are placed in process during production.arrow_forwardThe following information concerns production in the Baking Department for December. All direct materials are placed in process at the beginning of production. a. Determine the number of units in work in process inventory at December 31. b. Determine the equivalent units of production for direct materials and conversion costs in December.arrow_forwardTanaka Manufacturing Co. uses the process cost system. The following information for the month of December was obtained from the company’s books and from the production reports submitted by the department heads: Required: Prepare cost of production summaries for the Mixing, Blending, and Bottling (Hint: You must calculate the adjusted unit cost from Blending.) departments. Prepare a departmental cost work sheet. Draft the journal entries required to record the month’s operations. Prepare a statement of cost of goods manufactured for December. (Hint: Goods finished but not transferred to finished goods are considered part of work in process inventory.)arrow_forward

- Dublin Brewing Co. uses the process cost system. The following data, taken from the organizations books, reflect the results of manufacturing operations during October: Production Costs Work in process, beginning of period: Costs incurred during month: Production Data: 13,000 units finished and transferred to stockroom Work in process, end of period, 2,000 units one-half completed Required: Prepare a cost of production summary for October.arrow_forwardProduction Report Refer to the information for Alfombra Inc. on the previous page. The owner of Alfombra insisted on a formal report that provided all the details of the weighted average method. In the manufacturing process, all materials are added uniformly throughout the process. Required: Prepare a production report for the throw rug department for August using the weighted average method.arrow_forwardCalculating unit costs; units lost in production Gray Brothers Products Inc. manufactures a liquid product in one department. Due to the nature of the product and the process, units are regularly lost at the beginning of production. Materials and labor and overhead costs are added evenly throughout the process. The following summaries were prepared for the month of January: Calculate the unit cost for materials, labor, and factory overhead for January and show the costs of units transferred to finished goods and of the ending work in process inventory.arrow_forward

- Prepare a cost of production report for the Cutting Department of Dalton Carpet Company for January. Assuming that direct materials are placed in process during production, use the weighted average method with the following data:arrow_forwardBasic Cost Flows Linsenmeyer Company produces a common machine component for industrial equipment in three departments: molding, grinding, and finishing. The following data are available for September: During September, 18,000 components were completed. There is no beginning or ending WIP in any department. Required: 1. Prepare a schedule showing, for each department, the cost of direct materials, direct labor, applied overhead, product transferred in from a prior department, and total manufacturing cost. 2. Calculate the unit cost. (Note: Round the unit cost to two decimal places.)arrow_forwardConte Chemical Co. uses the weighted average cost method. All materials are added at the start of the production process. Labor and overhead are added evenly at the same rate throughout the process. Contes records indicate the following data for May: Ending work in process, on May 31, is 75% completed as to labor and factory overhead. Make the following calculations: a. Equivalent units for direct materials b. Equivalent units for labor and overhead (Hint: first determine the ending units in work in process.)arrow_forward

- Work in process account data for two months; cost of production reports Hearty Soup Co. uses a process cost system to record the costs of processing soup, which requires the cooking and filling processes. Materials are entered from the cooking process at the beginning of the filling process. The inventory of Work in ProcessFilling on April 1 and debits to the account during April were as follows: During April, 800 units in process on April 1 were completed, and of the 7,800 units entering the department, all were completed except 550 units that were 90% completed. Charges to Work in ProcessFilling for May were as follows: During May, the units in process at the beginning of the month were completed, and of the 9,600 units entering the department, all were completed except 300 units that were 35% completed. Instructions 1. Enter the balance as of April 1, in a four-column account for Work in ProcessFilling. Record the debits and the credits in the account for April. Construct a cost of production report, and present computations for determining (A) equivalent units of production for materials and conversion, B) costs per equivalent unit, (C) cost of goods finished, differentiating between units started in the prior period and units started and finished in April, and (d) work in process inventory. 2. Provide the same information for May by recording the May transactions in the four-column work in process account. Construct a cost of production report, and present the May computations (A through D) listed in part (1). 3. Comment on the change in costs per equivalent unit for March through May for direct materials and conversion costs.arrow_forwardSeacrest Company uses a process-costing system. The company manufactures a product that is processed in two departments: A and B. As work is completed, it is transferred out. All inputs are added uniformly in Department A. The following summarizes the production activity and costs for November: Required: 1. Using the weighted average method, prepare the following for Department A: (a) a physical flow schedule, (b) an equivalent unit calculation, (c) calculation of unit costs (Note: Round to four decimal places.), (d) cost of EWIP and cost of goods transferred out, and (e) a cost reconciliation. 2. CONCEPTUAL CONNECTION Prepare journal entries that show the flow of manufacturing costs for Department A. Use a conversion cost control account for conversion costs. Many firms are now combining direct labor and overhead costs into one category. They are not tracking direct labor separately. Offer some reasons for this practice.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College