Concept explainers

Videos

A. (1)

Prepare

A. (1)

Explanation of Solution

Equivalents units for production

The activity of a processing department in terms of fully completed units is known as equivalent units. It includes the completed units of direct materials and conversion cost of beginning work in process, units completed and transferred out, and ending work in process.

Cost per unit

Total unit cost is the cost incurred by the company to produce one unit of product. The unit cost is calculated by dividing the units produced with the total cost.

Prepare the journal entry to record material charged to production for casting department of Incorporation AC as shown below:

| Account title and Explanation | Debit | Credit |

| work in process - Casting Department | $350,000 | |

| Materials - Alloy | $350,000 | |

| (To record the materials used in production) |

Table (1)

- • Work in process inventory – Casting department is a current asset, and increased. Therefore, debit work in process inventory – casting department account for $350,000.

- • Materials – Alloy is a current asset, and decreased. Therefore, credit materials – Alloy account for $350,000.

A. (2)

Prepare journal entry to record conversion costs charged to production for casting department of Incorporation AC.

A. (2)

Explanation of Solution

Prepare the journal entry to record conversion costs charged to production for casting department of Incorporation AC as shown below:

| Account title and Explanation | Debit | Credit |

| work in process - Casting Department | $49,600 | |

| Wages payable | $19,840 | |

| Factory overhead | $29,760 | |

| (To record the conversion costs used in production) |

Table (2)

- • Work in process inventory – Casting department is a current asset, and increased. Therefore, debit work in process inventory – casting department account for $49,600.

- • Wages payable is a current liability and increased. Therefore, credit wages payable account for $19,840.

- • Factory overhead is a component of

stockholders’ equity and decreased it. Therefore, credit factory overhead account for $29,760.

Working note (1):

Calculate

A. (3)

Prepare journal entry to record transferred out to Machining department of Incorporation AC.

A. (3)

Explanation of Solution

Prepare the journal entry to record transferred out to Machining department of Incorporation AC as shown below:

| Account title and Explanation | Debit | Credit |

| Work in process – Machining Department | $402,684 | |

| Work in process – Casting department (5) | $402,684 | |

| (To record completed production transferred from casting department to Machining department ) |

Table (3)

- • Work in process inventory – Machining department is a current asset, and increased. Therefore, debit work in process inventory – machining department account for $402,684.

- • Work in process inventory – Casting department is a current asset, and decreased. Therefore, credit work in process inventory – Casting department account for $402,684.

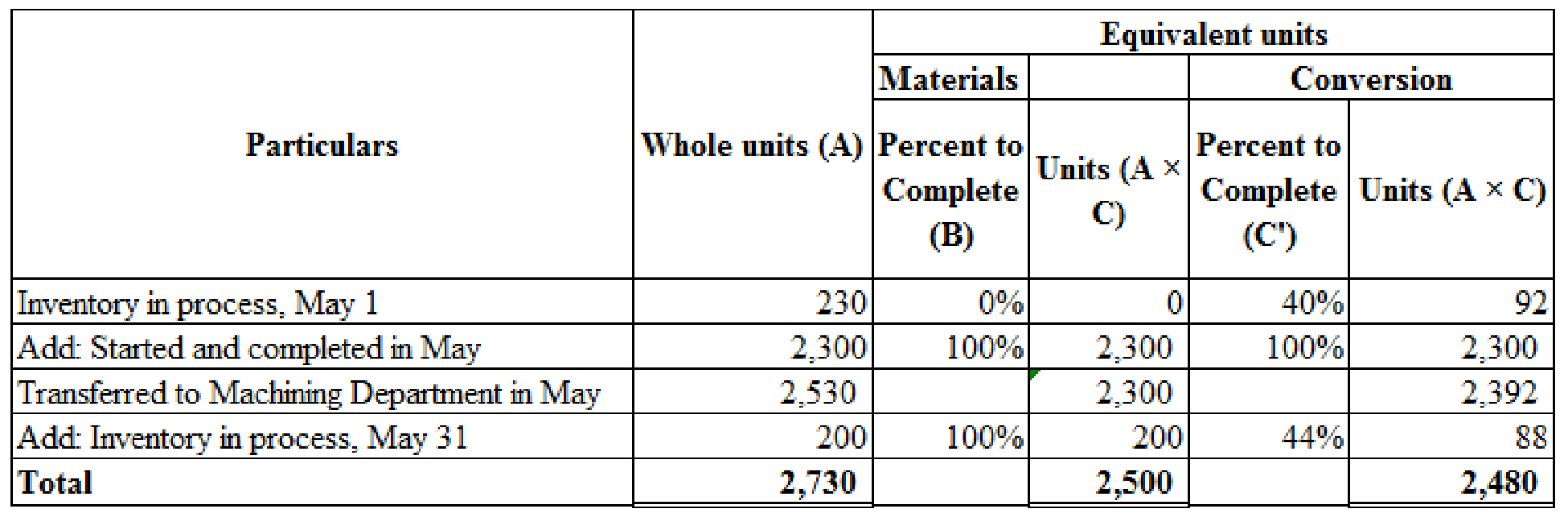

Working note (2):

Calculate equivalent units for production of casting department as shown below:

Figure (1)

Hints:

- 1. Opening work in process inventory units for conversion costs is calculated by multiplying whole units of opening work in process inventory with percent to complete.

- 2. A started and completed unit in May is calculated by deducting opening work in process inventory whole units from Transferred units to machining department.

- 3. Ending work in process inventory whole units is calculated by adding units produced during the period of May, and opening work in process inventory whole units and then deduct with transferred to machining department in May.

- 4. Ending work in process inventory units for conversion costs is calculated by multiplying whole units of ending work in process inventory with percentage completed during the period of May.

Working note (3):

Calculate equivalent cost per unit for direct materials as shown below:

Working note (4):

Calculate equivalent cost per unit for conversion costs as shown below:

Working note (5):

Calculate cost transferred out costs to Machining department as shown below:

| Particulars | Pounds (A) | Per pound (B) | Amount (A × B) |

| Cost of 2,530 transferred out pounds: | |||

| Materials | 230 | $132 | $30,360 |

| Conversion | 138 | $18 | $2,484 |

| Add: Cost to complete, May 1: | |||

| Materials | 0 | $140 | $0 |

| Conversion | 92 | $20 | $1,840 |

| Add: Pounds started and completed in May: | |||

| Materials | 2,300 | $140 | $322,000 |

| Conversion | 2,300 | $20 | $46,000 |

| Transferred costs to Machining Department | $402,684 |

Table (4)

B.

Calculate the ending work in process balance for casting department of Incorporation AC.

B.

Explanation of Solution

Calculate the ending work in process balance for casting department of Incorporation AC as shown below:

| Particulars | Pounds (A) | Per pound (B) | Amount (A × B) |

| Ending work in process inventory: | |||

| Direct materials | 200 | $140 | $28,000 |

| Conversion costs | 88 | $20 | $1,760 |

| Total ending work in process inventory | $29,760 |

Table (5)

Therefore, ending work in process inventory balance for casting department of Incorporation AC is $29,760.

C.

Evaluate the changes in equivalent cost per unit of direct materials and conversion costs comparing with previous month.

C.

Explanation of Solution

Calculate the changes in equivalent cost per unit of direct materials and conversion costs comparing with previous month as shown below:

| Particulars | Per pound |

| Cost per unit for May | $140 |

| Less: Cost per unit for April | $132 |

| Increase in Direct material cost per unit | $8 |

Table (6)

| Particulars | Per pound |

| Cost per unit for May | $20 |

| Less: Cost per unit for April | $18 |

| Increase in Conversion cost per unit | $2 |

Table (7)

Change in equivalent cost per unit for direct material is $8 per pound ($140 – $132). Hence, equivalent cost per unit for direct materials is increased by $8 per pound. A change in equivalent cost per unit for conversion cost is $2 per pound ($20 – $18). Hence, equivalent cost per unit for conversion cost is increased by $2 per pound. Incorporation AC might to scrutinize the reasons for increasing in direct material cost per unit and conversion cost per unit.

Want to see more full solutions like this?

Chapter 3 Solutions

Managerial Accounting

- Chavez Concrete Inc. has two production departments. Blending had 1,000 units in process at the beginning of the period, two-fifths complete. During the period 7,800 units were received from Mixing, 8,200 units were transferred to the finished goods storeroom, and 600 units were in process at the end of the period, 1/3 complete. The cost of the beginning work in process was: The costs during the month were: 1. Using the data in E5-15, prepare a cost of production summary for the month ended January 31, 2016. 2. Prepare a journal entry to transfer the cost of the completed units from Blending to the finished goods storeroom.arrow_forwardLarkin Company produces leather strips for western belts using three processes: cutting, design and coloring, and punching. The weighted average method is used for all three departments. The following information pertains to the Design and Coloring Department for the month of June: a. There was no beginning work in process. b. There were 400,000 units transferred in from the Cutting Department. c. Ending work in process, June 30: 50,000 strips, 80 percent complete with respect to conversion costs. d. Units completed and transferred out: 330,000 strips. The following costs were added during the month: a. Direct materials are added at the beginning of the process. b. Inspection takes place at the end of the process. All spoilage is considered normal. Required: 1. Calculate equivalent units of production for transferred-in materials, direct materials added, and conversion costs. 2. Calculate unit costs for the three categories of Requirement 1. 3. What is the total cost of units transferred out? What is the cost of ending work-in-process inventory? How is the cost of spoilage treated? 4. Assume that all spoilage is considered abnormal. Now, how is spoilage treated? Give the journal entry to account for the cost of the spoiled units. Some companies view all spoilage as abnormal. Explain why. 5. Assume that 80 percent of the units spoiled are abnormal and 20 percent are normal spoilage. Show the spoilage treatment for this scenario.arrow_forwardThe records of Stone Inc. reflect the following data: Work in process, beginning of month4,000 units one-fourth completed at a cost of 2,500 for materials, 1,400 for labor, and 1,800 for overhead. Production costs for the monthmaterials, 130,000; labor, 70,000; and factory overhead, 82,000. Units completed and transferred to stock45,000. Work in process, end of month5,000 units, one-half completed. Compute the months unit cost for each element of manufacturing cost and the total per unit cost. (Round unit costs to three decimal places.)arrow_forward

- Equivalent units and related costs; cost of production report; entries Dover Chemical Company manufactures specialty chemicals by a series of three processes, all materials being introduced in the Distilling Department. From the Distilling Department, the materials pass through the Reaction and Filling departments, emerging as finished chemicals. The balance in the account Work in ProcessFilling was as follows on January 1: The following costs were charged to Work in ProcessFilling during January: During January, 53,000 units of specialty chemicals were completed. Work in ProcessFilling Department on January 31 was 2,700 units, 30% completed. Instructions 1. Prepare a cost of production report for the Filling Department for January. 2. Journalize the entries for costs transferred from Reaction to Filling and the costs transferred from Filling to Finished Goods. 3. Determine the increase or decrease in the cost per equivalent unit from December to January for direct materials and conversion costs. 4. Discuss the uses of the cost of production report and the results of part (3).arrow_forwardAlgers Company produces dry fertilizer. At the beginning of the year, Algers had the following standard cost sheet: Algers computes its overhead rates using practical volume, which is 54,000 units. The actual results for the year are as follows: a. Units produced: 53,000 b. Direct materials purchased: 274,000 pounds at 2.50 per pound c. Direct materials used: 270,300 pounds d. Direct labor: 40,100 hours at 17.95 per hour e. Fixed overhead: 161,700 f. Variable overhead: 122,000 Required: 1. Compute price and usage variances for direct materials. 2. Compute the direct labor rate and labor efficiency variances. 3. Compute the fixed overhead spending and volume variances. Interpret the volume variance. 4. Compute the variable overhead spending and efficiency variances. 5. Prepare journal entries for the following: a. The purchase of direct materials b. The issuance of direct materials to production (Work in Process) c. The addition of direct labor to Work in Process d. The addition of overhead to Work in Process e. The incurrence of actual overhead costs f. Closing out of variances to Cost of Goods Soldarrow_forwardThe records of Burris Inc. reflect the following data: Work in process, beginning of month2,000 units one-half completed at a cost of 1,250 for materials, 675 for labor, and 950 for overhead. Production costs for the monthmaterials, 99,150; labor, 54,925; factory overhead, 75,050. Units completed and transferred to stock38,500. Work in process, end of month3,000 units, one-half completed. Compute the months unit cost for each element of manufacturing cost and the total per unit cost.arrow_forward

- Baxter Company has two processing departments: Assembly and Finishing. A predetermined overhead rate of 10 per DLH is used to assign overhead to production. The company experienced the following operating activity for April: a. Materials issued to Assembly, 24,000 b. Direct labor cost: Assembly, 500 hours at 9.20 per hour; Finishing, 400 hours at 8 per hour c. Overhead applied to production d. Goods transferred to Finishing, 32,500 e. Goods transferred to finished goods warehouse, 20,500 f. Actual overhead incurred, 10,000 Required: 1. Prepare the required journal entries for the preceding transactions. 2. Assuming Assembly and Finishing have no beginning work-in-process inventories, determine the cost of each departments ending work-in-process inventories.arrow_forwardHeap Company manufactures a product that passes through two processes: Fabrication and Assembly. The following information was obtained for the Fabrication Department for September: a. All materials are added at the beginning of the process. b. Beginning work in process had 80,000 units, 30 percent complete with respect to conversion costs. c. Ending work in process had 17,000 units, 25 percent complete with respect to conversion costs. d. Started in process, 95,000 units. Required: 1. Prepare a physical flow schedule. 2. Compute equivalent units using the weighted average method. 3. Compute equivalent units using the FIFO method.arrow_forwardFordman Company has a product that passes through two processes: Grinding and Polishing. During December, the Grinding Department transferred 20,000 units to the Polishing Department. The cost of the units transferred into the second department was 40,000. Direct materials are added uniformly in the second process. Units are measured the same way in both departments. The second department (Polishing) had the following physical flow schedule for December: Costs in beginning work in process for the Polishing Department were direct materials, 5,000; conversion costs, 6,000; and transferred in, 8,000. Costs added during the month: direct materials, 32,000; conversion costs, 50,000; and transferred in, 40,000. Required: 1. Assuming the use of the weighted average method, prepare a schedule of equivalent units. 2. Compute the unit cost for the month.arrow_forward

- SCHEDULE OF COST OF GOODS MANUFACTURED The following information is supplied for Sanchez Welding and Manufacturing Company. Prepare a schedule of cost of goods manufactured for the year ended December 31, 20--. Assume that all materials inventory items are direct materials. Work in process, January 1 20,500 Materials inventory, January 1 11,000 Materials purchases 12,000 Materials inventory, December 31 13,000 Direct labor 9,500 Overhead 5,500 Work in process, December 31 10,500arrow_forwardKraus Steel Company has two departments, Casting and Rolling. In the Rolling Department, ingots From the Casting Department are rolled into steel sheet. The Rolling Department received 4,000 tons from the Casting Department in October. During October, the Rolling Department completed 3,900 tons, including 200 tons of work in process on October 1. The ending work in process inventory on October 31 was 300 tons. How many tons were started and completed during October?arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,