Concept explainers

Videos

Find Missing Data

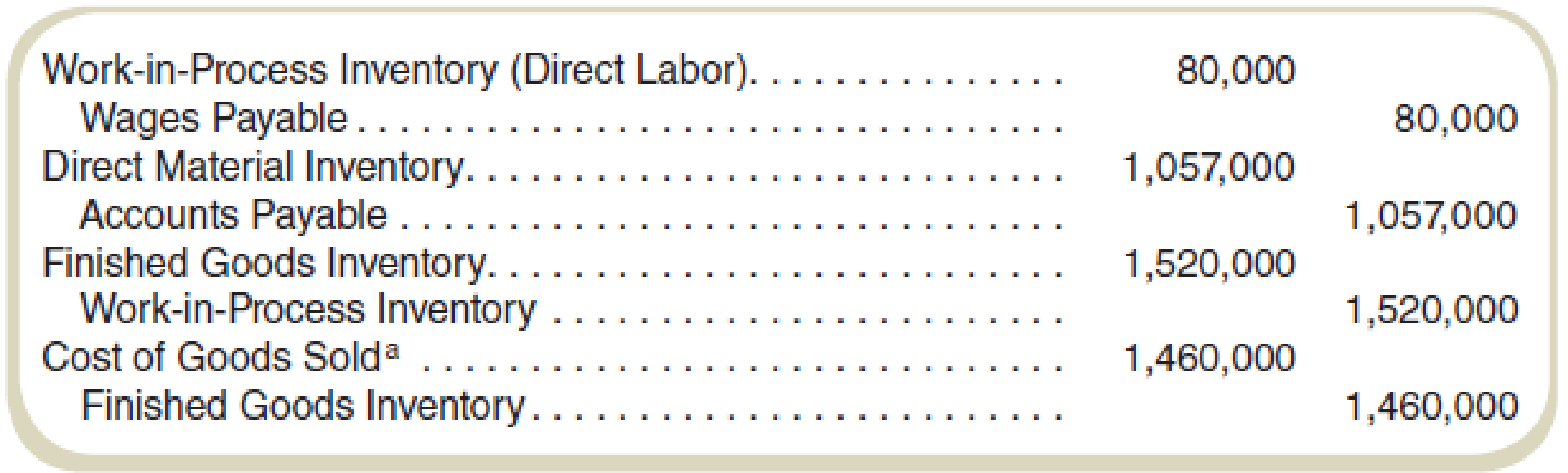

Accounting records for NIC Enterprises (NICE) for September show the following (each entry is the total of the actual entries for the account for the month):

a This entry does not include any over- or underapplied

The Work-in-Process ending account balance on September 30 was 125 percent of the beginning balance. The Direct Material ending inventory balance on September 30 was $25,000 less than the beginning balance. The Finished Goods beginning balance on September 1 was $148,000. The September income statement shows revenues of $2,300,000 and a gross profit of $850,000.

Required

- a. What was the Finished Goods inventory on September 30?

- b. How much manufacturing overhead was applied for September?

- c. What was the manufacturing overhead rate for September?

- d. How much manufacturing overhead was incurred for September?

- e. What was the Work-in-Process beginning inventory balance?

- f. What was the Work-in-Process ending inventory balance?

Want to see the full answer?

Check out a sample textbook solution

Chapter 7 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- The adjusted trial balance for Appleton Appliances, Ltd. on June 30, the end of its first month of operation, is as follows: The general ledger reveals the following additional data: a. There were no beginning inventories. b. Materials purchases during the period were 23,000. c. Direct labor cost was 18,500. d. Factory overhead costs were as follows: Required: 1. Prepare a statement of cost of goods manufactured for June. 2. Prepare an income statement for June. (Hint: Check to be sure that your figure for Cost of Goods Sold equals the amount given in the trial balance.) 3. Prepare a balance sheet as of June 30. (Hint: Do not forget Retained Earnings.)arrow_forwardOReilly Manufacturing Co.s cost of goods sold for the month ended July 31 was 345,000. The ending work in process inventory was 90% of the beginning work in process inventory. Factory overhead was 50% of the direct labor cost. No indirect materials were used during the period. Other information pertaining to OReillys inventories and production for July is as follows: Required: 1. Prepare a statement of cost of goods manufactured for the month of July. (Hint: Set up a statement of cost of goods manufactured, putting the given information in the appropriate spaces and solving for the unknown information. Start by using cost of goods sold to solve for the cost of goods manufactured.) 2. Prepare a schedule to compute the prime cost incurred during July. 3. Prepare a schedule to compute the conversion cost charged to Work in Process during July.arrow_forwardOn August 1, Cairle Companys work-in-process inventory consisted of three jobs with the following costs: During August, four more jobs were started. Information on costs added to the seven jobs during the month is as follows: Before the end of August, Jobs 70, 72, 73, and 75 were completed. On August 31, Jobs 72 and 75 were sold. Required: 1. Calculate the predetermined overhead rate based on direct labor cost. 2. Calculate the ending balance for each job as of August 31. 3. Calculate the ending balance of Work in Process as of August 31. 4. Calculate the cost of goods sold for August. 5. Assuming that Cairle prices its jobs at cost plus 20 percent, calculate Cairles sales revenue for August.arrow_forward

- Statement of cost of goods manufactured; income statement; balance sheet The adjusted trial balance for Rochester Electronics, Inc. on November 30, the end of its first month of operation, is as follows: The general ledger reveals the following additional data: a. There were no beginning inventories. b. Materials purchases during the period were 33,000. c. Direct labor cost was 18,500. d. Factory overhead costs were as follows: Required: 1. Prepare a statement of cost of goods manufactured for the month of November. 2. Prepare an income statement for the month of November. (Hint: Check to be sure that your figure for Cost of Goods Sold equals the amount given in the trial balance.) 3. Prepare a balance sheet as of November 30. (Hint: Do not forget Retained Earnings.)arrow_forwardNelson Fabrication Inc. had a remaining credit balance of $20,000 in its under- and overapplied factory overhead account at year-end. The balance was deemed to be large and, therefore, should be closed to Work in Process, Finished Goods, and Cost of Goods Sold. The year-end balances of these accounts, before adjustment, showed the following: Determine the prorated amount of the overapplied factory overhead that is chargeable to each of the accounts. Prepare the journal entry to close the credit balance in Under-and Overapplied Factory Overhead.arrow_forwardPhillips Products, Inc. had a remaining credit balance of $10,000 in its under- and overapplied factory overhead account at year-end. It also had year-end balances in the following accounts: Required: Prepare the closing entry for the $10,000 of overapplied overhead, assuming that the balance is not considered to be material. Prepare the closing entry for the $10,000 of overapplied overhead, assuming that the balance is considered to be material.arrow_forward

- On August 1, Cairle Companys work-in-process inventory consisted of three jobs with the following costs: During August, four more jobs were started. Information on costs added to the seven jobs during the month is as follows: Before the end of August, Jobs 70, 72, 73, and 75 were completed. On August 31, Jobs 72 and 75 were sold. Cairles selling and administrative expenses for August were 1,200. Required: Prepare an income statement for Cairle Company for August.arrow_forwardNathan Industries had a remaining debit balance of $20,000 in its under- and overapplied factory overhead account at year-end. It also had year-end balances in the following accounts: Required: Prepare the closing entry for the $20,000 of underapplied overhead, assuming that the balance is not considered to be material. Prepare the closing entry for the $20,000 of underapplied overhead, assuming that the balance is considered to be material.arrow_forwardDuring August, Skyler Company worked on three jobs. Data relating to these three jobs follow: Overhead is assigned on the basis of direct labor hours at a rate of 2.30 per direct labor hour. During August, Jobs 39 and 40 were completed and transferred to Finished Goods Inventory. Job 40 was sold by the end of the month. Job 41 was the only unfinished job at the end of the month. Required: 1. Calculate the per-unit cost of Jobs 39 and 40. (Round unit costs to nearest cent.) 2. Compute the ending balance in the work-in-process inventory account. 3. Prepare the journal entries reflecting the completion of Jobs 39 and 40 and the sale of Job 40. The selling price is 140 percent of cost.arrow_forward

- If the factory overhead control account has a credit balance of 2,000 at the end of the first month of the fiscal year, has the overhead been under- or overapplied for the month? What are some probable causes for the credit balance?arrow_forwardThe books of Petry Products Co. revealed that the following general journal entry had been made at the end of the current accounting period: The total direct materials cost for the period was $40,000. The total direct labor cost, at an average rate of $10 per hour for direct labor, was one and one-half times the direct materials cost. Factory overhead was applied on the basis of $4 per direct labor hour. What was the total actual factory overhead incurred for the period? (Hint: First solve for direct labor cost and then for direct labor hours.)arrow_forwardHousley Paints Co. had a remaining debit balance of $25,000 in its under- and overapplied factory overhead account at year-end. The balance was deemed to be large and, therefore, should be closed to Work in Process, Finished Goods, and Cost of Goods Sold. The year-end balances of these accounts, before adjustment, showed the following: Determine the prorated amount of the underapplied factory overhead that is chargeable to each of the accounts. Prepare the journal entry to close the debit balance in Under-and Overapplied Factory Overhead.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,