Concept explainers

Videos

Show Flow of Costs to Jobs

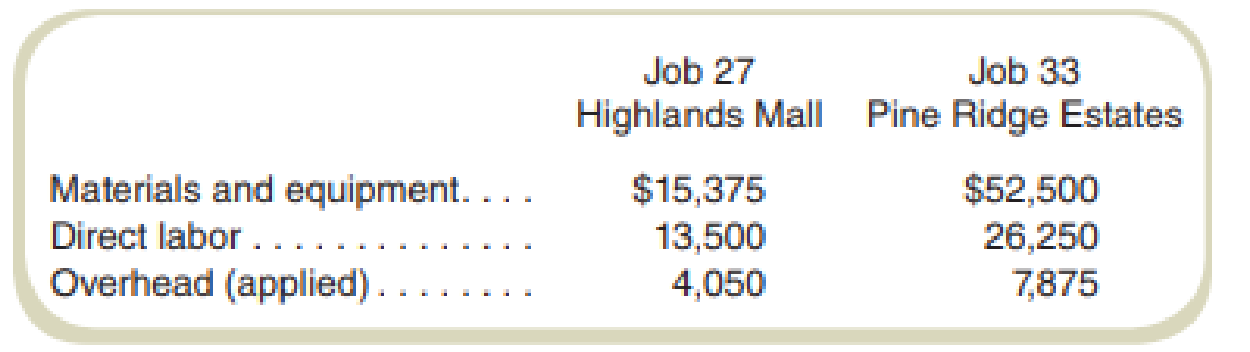

Kim’s Asphalt does driveway and parking lot resurfacing work for large commercial clients as well as small residential clients. An inventory of materials and equipment is on hand at all times so that work can start as quickly as possible. Special equipment is ordered as required. On May 1, the Materials and Equipment Inventory account had a balance of $36,000. The Work-in-Process Inventory account is maintained to record costs of work not yet complete. There were two such jobs on May 1 with the following costs:

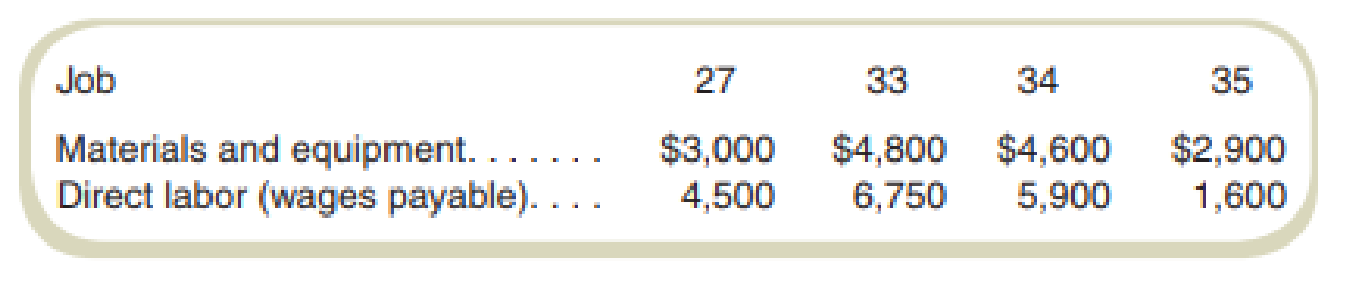

During May, Kim’s Asphalt started two new jobs. Additional work was carried out on Jobs 27 and 33, with the latter completed and billed to Pine Ridge Estates. Details on the costs incurred on jobs during May follow:

Other May Events

- 1. Received $12,500 payment on Job 24 delivered to customer in April.

- 2. Purchased materials and equipment for $9,400.

- 3. Billed Pine Ridge Estates $130,000 and received payment for $75,000 of that amount.

- 4. Determined that payroll for indirect labor personnel totaled $650.

- 5. Issued supplies and incidental materials for current

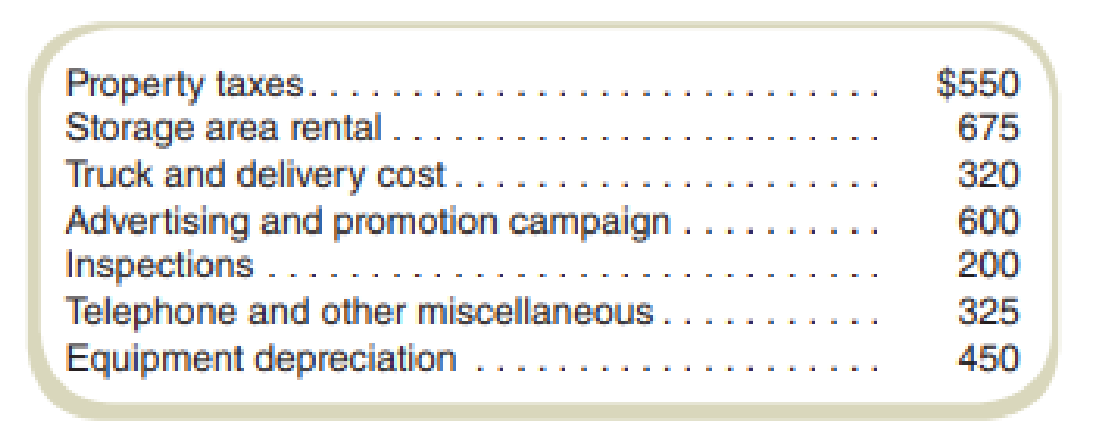

jobs costing $155. - 6. Recorded overhead and advertising costs for the operation as follows (all cash except equipment

depreciation ):

Required

- a. Prepare

journal entries to record the flow of costs for operations during May. - b. Calculate the amount of over- or underapplied overhead for the month. This amount is debited or credited to Cost of Goods Sold.

- c. Determine inventory balances for Materials and Equipment Inventory and Work-in-Process Inventory.

Want to see the full answer?

Check out a sample textbook solution

Chapter 7 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Overhead Assignment: Actual and Normal Activity Compared Reynolds Printing Company specializes in wedding announcements. Reynolds uses an actual job-order costing system. An actual overhead rate is calculated at the end of each month using actual direct labor hours and overhead for the month. Once the actual cost of a job is determined, the customer is billed at actual cost plus 50%. During April, Mrs. Lucky, a good friend of owner Jane Reynolds, ordered three sets of wedding announcements to be delivered May 10, June 10, and July 10, respectively. Reynolds scheduled production for each order on May 7, June 7, and July 7, respectively. The orders were assigned job numbers 115, 116, and 117, respectively. Reynolds assured Mrs. Lucky that she would attend each of her daughters weddings. Out of sympathy and friendship, she also offered a lower price. Instead of cost plus 50%, she gave her a special price of cost plus 25%. Additionally, she agreed to wait until the final wedding to bill for the three jobs. On August 15, Reynolds asked her accountant to bring her the completed job-order cost sheets for Jobs 115, 116, and 117. She also gave instructions to lower the price as had been agreed upon. The cost sheets revealed the following information: Reynolds could not understand why the overhead costs assigned to Jobs 116 and 117 were so much higher than those for Job 115. She asked for an overhead cost summary sheet for the months of May, June, and July, which showed that actual overhead costs were 20,000 each month. She also discovered that direct labor hours worked on all jobs were 500 hours in May and 250 hours each in June and July. Required: 1. How do you think Mrs. Lucky will feel when she receives the bill for the three sets of wedding announcements? 2. Explain how the overhead costs were assigned to each job. 3. Assume that Reynoldss average activity is 500 hours per month and that the company usually experiences overhead costs of 240,000 each year. Can you recommend a better way to assign overhead costs to jobs? Recompute the cost of each job and its price, given your method of overhead cost assignment. Which method do you think is best? Why?arrow_forwardSource Documents For each of the following independent situations, give the source document that would be referred to for the necessary information. Required: 1. Direct materials costing 460 are requisitioned for use on a job. 2. Greiners Garage uses a job-order costing system. Overhead is applied to jobs based on direct labor hours. Which source document gives the number of direct labor hours worked on Job 2004-276? 3. Pasilla Investigative Services bills clients on a monthly basis for costs to date. Job 3-48 involved an investigator following the clients business partner for a week by automobile. Mileage is billed at number of miles times 0.75. 4. The foreman on the Jackson job wonders what the actual direct materials cost was for that job.arrow_forwardVentana Window and Wall Treatments Company provides draperies, shades, and various window treatments. Ventana works with the customer to design the appropriate window treatment, places the order, and installs the finished product. Direct materials and direct labor costs are easy to trace to the jobs. Ventanas income statement for last year is as follows: Ventana wants to find a markup on cost of goods sold that will allow them to earn about the same amount of profit on each job as was earned last year. Required: 1. What is the markup on cost of goods sold (COGS) that will maintain the same profit as last year? (Round the percentage to two significant digits.) 2. A customer orders draperies and shades for a remodeling job. The job will have the following costs: What is the price that Ventana will quote given the markup percentage calculated in Requirement 1? (Round the price to the nearest dollar.) 3. What if Ventana wants to calculate a markup on direct materials cost, since it is the largest cost of doing business? What is the markup on direct materials cost that will maintain the same profit as last year? (Round the percentage to two significant digits.) What is the bid price Ventana will use for the job given in Requirement 2 if the markup percentage is calculated on the basis of direct materials cost? (Round to the nearest dollar.)arrow_forward

- Brady Furniture Company manufactures wooden oak furniture. The company employs a job cost system to trace manufacturing costs to jobs. Each job represents a batch of furniture of the same type. Information regarding direct materials on selected jobs throughout the year is as follows: Dining tables are the most difficult furniture item in Bradys catalog to manufacture. Thus, the most skilled employees are scheduled to make dining tables, unless they are required for other jobs. a. Determine the material cost per unit for each job. b. Use the January material cost per unit for each type of furniture as the base material cost. For each month and each type of furniture, determine the unit material cost as a percent of the base unit material cost. Round percent to one decimal place. Use the following table format: c. Develop a line chart of the percent of unit material cost to the base unit material cost. Place the months on the horizontal axis and use three lines for the three different types of furniture. d. Interpret the chart. What is happening to the dining tables?arrow_forwardJOB ORDER COSTING WITH UNDER- AND OVERAPPLIED FACTORY OVERHEAD M. Evans Sons manufactures parts for radios. For each job order, it maintains ledger sheets on which it records direct labor, direct materials, and factory overhead applied. The factory overhead control account contains postings of actual overhead costs. At the end of the month, the under- or over applied factory overhead is charged to the cost of goods sold account. Factory overhead is applied on the basis of direct labor hours. For Job Nos. 101, 102,103, and 104, direct labor hours are 12, 000, 10,000, 11, 000, and 18,000, respectively. The overhead application rate is 1.20/direct labor hour. (a) Purchased raw materials on account, 50,000. (b) Issued direct materials: (c) Issued indirect materials to production, 8,000. (d) Incurred direct labor costs: (e) Charged indirect labor to production, 15,000. (f) Paid electricity bill, taxes, and repair fees for the factory and charged to production, 8,000. (g) Depreciation expense on factory equipment, 30,000. (h) Applied factory overhead to Job Nos. 101104 using the predetermined factory overhead rate (see above). (i) Finished Job Nos. 101103 and transferred to the finished goods inventory account as products N, O, and P. (j) Sold products N and for 50,000 and 45,400, respectively. (k) Transferred under- or over applied factory overhead balance to the cost of goods sold account. REQUIRED 1. Prepare general journal entries to record transactions (a) through (k). 2. Post the entries to the work in process and finished goods accounts only and determine the ending balances in these accounts. 3. Compute the balance in the job cost ledger and verify that this balance agrees with that in the work in process control account.arrow_forwardThe Following events occurred during March for Ajax Company. Prepare a journal entry for each transaction. Materials were purchased on account for $5,429. Materials were requisitioned to begin work on Job C15 In the amount of $2,500. Direct labor expense for job C15 was $4,250. Actual overhead was incurred on account for $5,385. Factory overhead was charged w Job C15 at the rate of 200% direct labor. Job C15 was transferred to finished goods at $15,250. Job C15 was sold on account for $28,000.arrow_forward

- JOB ORDER COSTING WITH UNDER- AND OVERAPPLIED FACTORY OVERHEAD M Evans Sons manufactures parts for radios. For each job order, it maintains ledger sheets on which it records direct labor, direct materials, and factory overhead applied. The factory overhead control account contains postings of actual overhead costs. At the end of the month, the under- or overapplied factory overhead is charged to the cost of goods sold account. Factory overhead is applied on the basis of direct labor hours. For Job Nos. 101, 102, 103, and 104, direct labor hours are 12,000, 10,000, 11,000, and 18,000, respectively. The overhead application rate is 1.20/direct labor hour (a) Purchased raw materials on account, 50,000. (b) Issued direct materials: (c) Issued indirect materials to production, 8,000. (d) Incurred direct labor costs: (e) Charged indirect labor to production, 15,000. (f) Paid electricity bill, taxes, and repair fees for the factory and charged to production, 8,000. (g) Depreciation expense on factory equipment, 30,000. (h) Applied factory overhead to Job Nos. 101-104 using the predetermined factory overhead rare (see above). (i) Finished Job Nos. 101-103 and transferred to the finished goods inventory account as products N, O, and P. (j) Sold products N and O for 50,000 and 45,400, respectively. (k) Transferred under- or overapplied factory overhead balance to the cost of goods sold account. REQUIRED 1. Prepare general journal entries to record transactions (a) through (k). Make compound entries for (b), (d), and (h), with separate debits for each job. 2. Post the entries to the work in process and finished goods T accounts only and determine the ending balances in these accounts. 3. Compute the balance in the job cost ledger and verify that this balance agrees with that in the work in process control account.arrow_forwardA company manufactures a liquid product called Crystal. The basic ingredients are put into process in Department 1. In Department 2, other materials are added that increase the number of units being processed by 50%. The factory has only two departments. Calculate the following for each department: (a) unit cost for the month for materials, labor, and factory overhead, (b) cost of the units transferred, and (c) cost of the ending work in process.arrow_forwardSelected account balances and transactions of Titan Foundry Inc. follow: May Transactions: a. Purchased raw materials and factory supplies on account at costs of 45,000 and 10,000, respectively. (One inventory account is maintained.) b. Incurred wages during the month of 65,000 (15,000 was for indirect labor). c. Incurred factory overhead costs in the amount of 42,000 on account. d. Made adjusting entries to record 10,000 of factory overhead for items such as depreciation (credit Various Credits). Factory overhead was closed to Work in Process. Completed jobs were transferred to Finished Goods, and the cost of jobs sold was charged to Cost of Goods Sold. Required: Prepare journal entries for the following: 1. The purchase of raw materials and factory supplies. 2. The issuance of raw materials and supplies into production. (Hint: Be certain to consider the beginning and ending balances of raw materials and supplies as well as the amount of the purchases.) 3. The recording of the payroll. 4. The distribution of the payroll. 5. The payment of the payroll. 6. The recording of factory overhead incurred. 7. The adjusting entry for factory overhead. 8. The entry to transfer factory overhead costs to Work in Process. 9. The entry to transfer the cost of completed work to Finished Goods. (Hint: Be sure to consider the beginning and ending balances of Work in Process as well as the manufacturing costs added to Work in Process this period.) 10. The entry to record the cost of goods sold. (Hint: Be sure to consider the beginning and ending balances of Finished Goods as well as the cost of the goods finished during the month.)arrow_forward

- Use the following information for Brief Exercises 2-19 and 2-20: Slapshot Company makes ice hockey sticks. Last week, direct materials (wood, paint, Kevlar, and resin) costing 32,000 were put into production. Direct labor of 28,000 (10 workers 200 hours 14 per hour) was incurred. Manufacturing overhead equaled 60,000. By the end of the week, the company had manufactured 500 hockey sticks. Brief Exercise 2-20 Prime Cost and Conversion Cost Refer to the information for Slapshot Company on the previous page. Required: 1. Calculate the total prime cost for last week. 2. Calculate the per-unit prime cost. 3. Calculate the total conversion cost for last week. 4. Calculate the per-unit conversion cost.arrow_forwardRIRA Company makes attachments such as backhoes and grader and bulldozer blades for construction equipment. The company uses a job order cost system. Management is concerned about cost performance and evaluates the job cost sheets to learn more about the cost effectiveness of the operations. To facilitate a comparison, the job cost sheets for Job 206 (for 50 backhoe buckets completed in October) and Job 228 (for 75 backhoe buckets completed in December) were pulled and presented as follows: Management is concerned about the increase in unit costs over the months from October to December. To understand what has occurred, management interviewed the purchasing manager and quality manager. Purchasing Manager: Prices have been holding steady for our raw materials during the first half of the year. I found a new supplier for our bulk steel that was willing to offer a better price than we received in the past. I saw these lower steel prices and jumped on them, knowing that a reduction in steel prices would have a very favorable impact on our costs. Quality Manager: Something happened around mid-year. All of a sudden, we were experiencing problems with respect to the quality of our steel. As a result, weve been having all sorts of problems on the shop floor in our foundry and welding operation. a. Analyze the two job cost sheets and identify why the unit costs have changed for the backhoe buckets. Complete the following schedule to help in your analysis: b. How would you interpret what has happened in light of your analysis and the interviews?arrow_forwardCost flow relationships The following information is available for the first month of operations of Bahadir Company, a manufacturer of mechanical pencils: Using the information given, determine the following missing amounts: A. Cost of goods sold B. Finished goods inventory at the end of the month C. Direct materials cost D. Direct labor cost E. Work in process inventory at the end of the montharrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning