Fundamentals Of Cost Accounting (6th Edition)

6th Edition

ISBN: 9781259969478

Author: WILLIAM LANEN, Shannon Anderson, Michael Maher

Publisher: McGraw Hill Education

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 11, Problem 63P

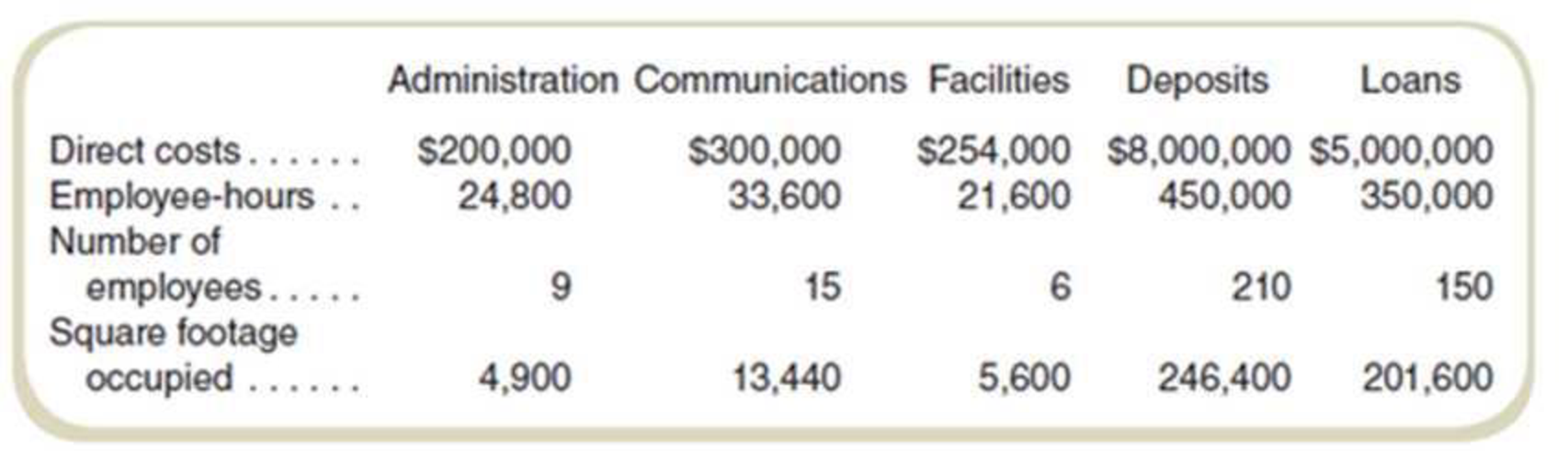

Allocate Service Department Costs: Direct and Step Methods

State Financial Corp. has three service departments (Administration, Communications, and Facilities), and two production departments (Deposits and Loans). A summary of costs and other data for each department prior to allocation of service department costs for the year ended December 31 follows:

The costs of the service departments are allocated on the following bases: Administration, employee-hours; Communications, number of employees; and Facilities, square footage occupied.

Required

Round all final calculations to the nearest dollar.

- a. Assume that the bank elects to distribute service department costs to production departments using the direct method. What amount of Communications Department costs is allocated to the IX*posits Department?

- b. Assume the same method of allocation as in requirement (a). What amount of Administration Department costs is allocated to the Loans Department?

- c. Assuming that the bank elects to distribute service department costs to other departments using the step method (starting with Facilities and then Communications), what amount of Facilities Department costs is allocated to the Communications Department?

- d. Assume the same method of allocation as in requirement (c). What amount of Communication Department costs is allocated to Facilities?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Chapter 11 Solutions

Fundamentals Of Cost Accounting (6th Edition)

Ch. 11 - Why do companies allocate costs? What are some of...Ch. 11 - What are the three methods of allocating service...Ch. 11 - What are the similarities and differences among...Ch. 11 - What criterion should be used to determine the...Ch. 11 - What is a limitation of the direct method of...Ch. 11 - What is a limitation of the step method of...Ch. 11 - Prob. 7RQCh. 11 - Why would a number of accountants express a...Ch. 11 - Prob. 9RQCh. 11 - What is the basic difference between the...

Ch. 11 - Prob. 11RQCh. 11 - If cost allocations arc arbitrary and potentially...Ch. 11 - Prob. 13CADQCh. 11 - Prob. 14CADQCh. 11 - Prob. 15CADQCh. 11 - Prob. 16CADQCh. 11 - Prob. 17CADQCh. 11 - Prob. 18CADQCh. 11 - What are some of the factors that a company needs...Ch. 11 - Prob. 20CADQCh. 11 - Prob. 21CADQCh. 11 - Prob. 22CADQCh. 11 - How is joint cost allocation like service...Ch. 11 - Prob. 24CADQCh. 11 - In what ways is joint cost allocation similar to...Ch. 11 - Why Are Costs Allocated?Ethical Issues You are the...Ch. 11 - Cost Allocation: Direct Method Caro Manufacturing...Ch. 11 - Allocating Service Department Costs First to...Ch. 11 - Cost Allwat ion: Direct Method University Printers...Ch. 11 - Prob. 30ECh. 11 - Cost Allocation: Step Method

Refer to the data for...Ch. 11 - Cost Allocation: Reciprocal Method

Refer to the...Ch. 11 - Cost Allocation: Reciprocal Method, Two Service...Ch. 11 - Cost Allocation: Reciprocal Method

Refer to the...Ch. 11 - Prob. 35ECh. 11 - Prob. 36ECh. 11 - Prob. 37ECh. 11 - Prob. 38ECh. 11 - Prob. 39ECh. 11 - Prob. 40ECh. 11 - Net Realizable Value Method: Multiple Choice

Oak...Ch. 11 - Sell or Process Further: Multiple Choice

Refer to...Ch. 11 - Net Realizable Value Method Euclid Corporation...Ch. 11 - Estimated Net Realizable Value Method Blasto,...Ch. 11 - Net Realizable Value Method to Solve for Unknowns...Ch. 11 - Net Realizable Value Method Bixel Components...Ch. 11 - Net Realizable Value Method with By-Products...Ch. 11 - Net Realizable Value Method Deming Sons...Ch. 11 - Physical Quantities Method

Refer to the facts in...Ch. 11 - Sell or Process Further

Refer to the facts in...Ch. 11 - Physical Quantities Method The following questions...Ch. 11 - Physical Quantities Method; Sell or Process...Ch. 11 - Physical Quantities Method with By-Product...Ch. 11 - Step Method with Three Service Departments Model,...Ch. 11 - Comparison of Allocation Methods BluStar Company...Ch. 11 - Solve for Unknowns: Direct Method Franks Foods has...Ch. 11 - Solve for Unknowns: Step Method RT Renovations is...Ch. 11 - Cost Allocation: Step Method with Analysis and...Ch. 11 - Prob. 59PCh. 11 - Prob. 60PCh. 11 - Direct, Step, and Reciprocal Methods:...Ch. 11 - Cost Allocation: Step and Reciprocal Methods...Ch. 11 - Allocate Service Department Costs: Direct and Step...Ch. 11 - Prob. 64PCh. 11 - Prob. 65PCh. 11 - Prob. 66PCh. 11 - Prob. 67PCh. 11 - Prob. 68PCh. 11 - Fletcher Fabrication, Inc., produces three...Ch. 11 - Findina Missing Data: Net Realizable Value Spartan...Ch. 11 - Finding Missing Data: Net Realizable Value Blaine,...Ch. 11 - Joint Costing in a Process Costing Context:...Ch. 11 - Find Maximum Input Price: Estimated Net Realizable...Ch. 11 - Effect of By-Product versus Joint Cost Accounting...Ch. 11 - Prob. 75PCh. 11 - Prob. 76P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Service department charges In divisional income statements prepared for Demopolis Company, the Payroll Department costs are charged back to user divisions on the basis of the number of payroll distributions, and the Purchasing Department costs are charged back on the basis of the number of purchase requisitions. The Payroll Department had expenses of 64,560, and the Purchasing Department had expenses of 40,000 for the year. The following annual data for Residential, Commercial, and Government Contract divisions were obtained from corporate records: A. Determine the total amount of payroll checks and purchase requisitions processed per year by the company and each division. B. Using the cost driver information in (A), determine the annual amount of payroll and purchasing costs allocated to the Residential, Commercial, and Government Contract divisions from payroll and purchasing services. C. Why does the Residential Division have a larger support department allocation than the other two divisions, even though its sales are lower?arrow_forwardA manufacturing company has two service and two production departments. Human Resources and Machine Repair are the service departments. The production departments are Grinding and Polishing. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The human resources department services all departments of the company, and its costs are allocated using the numbers of employees within each department, while machine repair costs are allocable to Grinding and Polishing on the basis of machine hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardRefer to the data in Exercise 7.22. The support departments are ranked in order of highest cost to lowest cost. Required: 1. Allocate the costs of the support departments using the sequential method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.) 2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)arrow_forward

- A manufacturing company has two service and two production departments. Building Maintenance and Factory Office are the service departments. The production departments are Assembly and Machining. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The building maintenance department services all departments of the company, and its costs are allocated using floor space occupied, while factory office costs are allocable to Assembly and Machining on the basis of direct labor hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardRefer to the data in Exercise 7.22. The company has decided to simplify its method of allocating support service costs by switching to the direct method. Required: 1. Allocate the costs of the support departments to the producing departments using the direct method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.) 2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)arrow_forwardA company uses charging rates to allocate service department costs to the using departments. The accountant compiled the following information on one of the service departments: If Department K plans to use 1,350 hours of the service departments service in the coming year, how much of the service departments cost is allocated to Department K? a. 3,375 b. 27,300 c. 26,325 d. 23,950arrow_forward

- Refer to Cornerstone Exercise 7.3. Now assume that Valron Company uses the sequential method to allocate support department costs. The support departments are ranked in order of highest cost to lowest cost. Required: 1. Calculate the allocation ratios (rounded to four significant digits) for the four departments using the sequential method. 2. Using the sequential method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments. (Round all allocated costs to the nearest dollar.) 3. What if the allocation ratios in Requirement 1 were rounded to six significant digits rather than four? How would that affect any rounding error in the allocation of costs?arrow_forwardDistribution of service department costs to production departments using the sequential distribution method Required: Using the information in P4-6, prepare a schedule showing the distribution of the service departments’ expenses using the sequential distribution method in the order of number of other departments served. (Hint: First distribute the service department that services the greater number of other departments.)arrow_forwardRefer to the data in Exercise 7.18. When the capacity of the HR Department was originally established, the normal usage expected for each department was 20,000 direct labor hours. This usage is also the amount of activity planned for the two departments in Year 1 and Year 2. Required: 1. Allocate the costs of the HR Department using the direct method and assuming that the purpose is product costing. 2. Allocate the costs of the HR Department using the direct method and assuming that the purpose is to evaluate performance.arrow_forward

- Refer to Cornerstone Exercise 7.3. Now assume that Valron Company uses the reciprocal method to allocate support department costs. Required: 1. Calculate the allocation ratios (rounded to four significant digits) for the four departments using the reciprocal method. 2. Develop a simultaneous equations system of total costs for the support departments. Solve for the total reciprocated costs of each support department. (Round reciprocated total costs to the nearest dollar.) 3. Using the reciprocal method, allocate the costs of the Human Resources and General Factory departments to the Fabricating and Assembly departments. (Round all allocated costs to the nearest dollar.) 4. What if the square footage in Fabricating were 13,300 and the square footage in Assembly were 5,700. How would that affect the allocation of support department costs?arrow_forward(Appendix 4B) Sequential Method of Support Department Cost Allocation Refer to Exercise 4-51 for data. Now assume that Stevenson uses the sequential method to allocate support department costs to the operating divisions. General Factory is allocated first in the sequential method for the company. Required: 1. Calculate the allocation ratios for Power and General Factory. (Note: Carry these calculations out to four decimal places.) 2. Allocate the support service costs to the operating divisions. (Note: Round all amounts to the nearest dollar.) 3. Assume divisional overhead rates are based on direct labor hours. Calculate the overhead rate for the Battery Division and for the Small Motors Division. (Note: Round overhead rates to the nearest cent.)arrow_forwardLonsdale Inc. manufactures entry and dining room lighting fixtures. Five activities are used in manufacturing the fixtures. These activities and their associated budgeted activity costs and activity bases are as follows: Corporate records were obtained to estimate the amount of activity to be used by the two products. The estimated activity-base usage quantities and units produced follow: a. Determine the activity rate for each activity. b. Use the activity rates in (a) to determine the total and per-unit activity costs associated with each product. Round to the nearest cent.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

What is Cost Allocation? Definition & Process; Author: FloQast;https://www.youtube.com/watch?v=hLhvvHvZ3JM;License: Standard Youtube License