Concept explainers

Videos

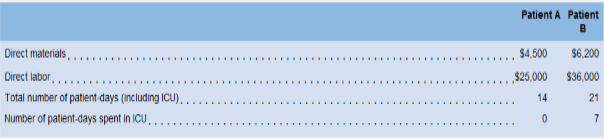

Plantwide versus Multiple Predetermined

Historically, McCullough has used one predetermined overhead rate based on the number of patient-days (each night that a patient spendsin the hospital counts as one patient-day) to allocate overhead costs to patients, Recently a member of the hospital’s accounting staff has suggested using two predetermined overhead rates (allocated based on the number of patient-days) to improve the accuracy of the costsallocated to patients. The first overhead rate would include all overhead costs within the Intensive Care Unit (ICU) and the second overheadrate would include all other overhead costs. Information pertaining to the hospital’s estimated number of patient-days, its estimated overheadcosts, and two of its patients—Patient A and Patient B—is provided below:

Required:

Assuming McCullough uses only one predetermined overhead rate, calculate:

a. The predetermined overhead rate.

b. The total cost, including direct materials, direct labor and applied overhead, assigned to Patient A and Patient B.

2. Assuming McCullough calculates two overhead rates as recommended by the staff accountant calculate:

a. The ICU and Other overhead rates.

b. The total cost, including direct materials, direct labor and applied overhead, assigned to Patient A and Patient B.

3. What insights are revealed by the staff accountant’s approach?

Want to see the full answer?

Check out a sample textbook solution

Chapter 2 Solutions

Introduction To Managerial Accounting

- Product costing and decision analysis for a service company Pleasant Stay Medical Inc. wishes to determine its product costs. Pleasant Stay offers a variety of medical procedures (operations) that are considered its products. The overhead has been separated into three major activities. The annual estimated activity costs and activity bases follow: Total patient days are determined by multiplying the number of patients by the average length of stay in the hospital. A weighted care unit (wcu) is a measure of nursing effort used to care for patients. There were 192,000 weighted care units estimated for the year. In addition, Pleasant Stay estimated 6,000 patients and 27,000 patient days for the year. (The average patient is expected to have a a little more than a four-day stay in the hospital.) During a portion of the year, Pleasant Stay collected patient information for three selected procedures, as follows: Private insurance reimburses the hospital for these activities at a fixed daily rate of 406 per patient day for all three procedures. Instructions Determine the activity rates. Determine the activity cost for each procedure. Determine the excess or deficiency of reimbursements to activity cost. Interpret your results.arrow_forwardOverhead Rates, Unit Costs Folsom Company manufactures specialty tools to customer order. There are three producing departments. Departmental information on budgeted overhead and various activity measures for the coming year is as follows: Currently, overhead is applied on the basis of machine hours using a plantwide rate. However, Janine, the controller, has been wondering whether it might be worthwhile to use departmental overhead rates. She has analyzed the overhead costs and drivers for the various departments and decided that Welding and Finishing should base their overhead rates on machine hours and that Assembly should base its overhead rate on direct labor hours. Janine has been asked to prepare bids for two jobs with the following information: The typical bid price includes a 35% markup over full manufacturing cost. Round all overhead rates to the nearest cent. Round all bid prices to the nearest dollar. Required: 1. Calculate a plantwide rate for Folsom Company based on machine hours. What is the bid price of each job using this rate? 2. Calculate departmental overhead rates for the producing departments. What is the bid price of each job using these rates?arrow_forwardSan Mateo Optics, Inc., specializes in manufacturing lenses for large telescopes and cameras used in space exploration. As the specifications for the lenses are determined by the customer and vary considerably, the company uses a job-order costing system. Manufacturing overhead is applied to jobs on the basis of direct labor hours, utilizing the absorption- or full-costing method. San Mateos predetermined overhead rates for 20x1 and 20x2 were based on the following estimates. Jim Cimino, San Mateos controller, would like to use variable (direct) costing for internal reporting purposes as he believes statements prepared using variable costing are more appropriate for making product decisions. In order to explain the benefits of variable costing to the other members of San Mateos management team, Cimino plans to convert the companys income statement from absorption costing to variable costing. He has gathered the following information for this purpose, along with a copy of San Mateos 20x1 and 20x2 comparative income statement. San Mateo Optics, Inc. Comparative Income Statement For the Years 20x1 and 20x2 San Mateos actual manufacturing data for the two years are as follows: The companys actual inventory balances were as follows: For both years, all administrative expenses were fixed, while a portion of the selling expenses resulting from an 8 percent commission on net sales was variable. San Mateo reports any over-or underapplied overhead as an adjustment to the cost of goods sold. Required: 1. For the year ended December 31, 20x2, prepare the revised income statement for San Mateo Optics, Inc., utilizing the variable-costing method. Be sure to include the contribution margin on the revised income statement. 2. Describe two advantages of using variable costing rather than absorption costing. (CMA adapted)arrow_forward

- Pelder Products Company manufactures two types of engineering diagnostic equipment used in construction. The two products are based upon different technologies, X-ray and ultrasound, but are manufactured in the same factory. Pelder has computed the manufacturing cost of the X-ray and ultrasound products by adding together direct materials, direct labor, and overhead cost applied based on the number of direct labor hours. The factory has three overhead departments that support the single production line that makes both products. Budgeted overhead spending for the departments is as follows: Pelders budgeted manufacturing activities and costs for the period are as follows: The budgeted cost to manufacture one ultrasound machine using the activity-based costing method is: a. 225. b. 264. c. 293. d. 305.arrow_forwardBounce Back Insurance Company carries three major lines of insurance: auto, workers compensation, and homeowners. The company has prepared the following report: Management is concerned that the administrative expenses may make some of the insurance lines unprofitable. However, the administrative expenses have not been allocated to the insurance lines. The controller has suggested that the administrative expenses could be assigned to the insurance lines using activity-based costing. The administrative expenses are comprised of five activities. The activities and their rates are as follows: Activity-base usage data for each line of insurance were retrieved from the corporate records as follows: a. Complete the product profitability report through the administrative activities. Determine the operating income as a percent of premium revenue, rounded to the nearest whole percent. b. Interpret the report.arrow_forwardActivity-based department rate product costing and product cost distortions Big Sound Inc. manufactures two products: receivers and loudspeakers. The factory overhead incurred is as follows: The activity base associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: The activity-base usage quantities and units produced for the two products follow: Instructions Determine the factory overhead rates under the multiple production department rate method. Assume that indirect labor is associated with the production departments, so that the total factory overhead is 420,000 and 294,000 for the Subassembly and Final Assembly departments, respectively. Determine the total and per-unit factory overhead costs allocated to each product, using the multiple production department overhead rates in (1). Determine the activity rates, assuming that the indirect labor is associated with activities rather than with the production departments. Determine the total and per-unit cost assigned to each product under activity-based costing. Explain the difference in the per-unit overhead allocated to each product under the multiple production department factory overhead rate and activity-based costing methods. production department factory overhead rate and activity-based costing methods.arrow_forward

- A CPA would recommend changing from plantwide overhead rate application to departmental rates under which of the following circumstances? a. The plant produces one product. b. The plant produces multiple products that may or may not pass through all producing departments. c. The plant produces multiple products that pass through all of the producing departments. d. The plant produces many different products that consume the same amount of resources in each producing department.arrow_forwardLansing. Inc., provided the following data for its two producing departments: Machine hours are used to assign the overhead of the Molding Department, and direct labor hours are used to assign the overhead of the Polishing Department. There are 30,000 units of Form A produced and sold and 50,000 of Form B. Required: 1. Calculate the overhead rates for each department. 2. Using departmental rates, assign overhead to live two products and calculate the overhead cost per unit. How does this compare with the plantwide rate unit cost, using direct labor hours? 3. What if the machine hours in Molding were 1,200 for Form A and 3,800 for Form B and the direct labor hours used in Polishing were 5,000 and 15,000, respectively? Calculate the overhead cost per unit for each product using departmental rates, and compare with the plantwide rate unit costs calculated in Requirement 2. What can you conclude from this outcome?arrow_forwardJournalizing the distribution of service department costs to production departments Required: Using your solution to P4-7, prepare journal entries for the following: The distribution of the total factory overhead of $79,400 to the individual production and service departments where it originated. The distribution of the Building Maintenance overhead to the appropriate other departments. The distribution of the Factory Office overhead to the appropriate other departments.arrow_forward

- The management of Gwinnett County Chrome Company, described in Problem 1A, now plans to use the multiple production department factory overhead rate method. The total factory overhead associated with each department is as follows: Instructions 1. Determine the multiple production department factory overhead rates, using direct labor hours for the Stamping Department and machine hours for the Plating Department. 2. Determine the product factory overhead costs, using the multiple production department rates in (1).arrow_forwardJob-Order Costing versus Process Costing a. Hospital services b. Custom cabinet making c. Toy manufacturing d. Soft-drink bottling e. Airplane manufacturing (e.g., 767s) f. Personal computer assembly g. Furniture making (e.g., computer desks sold at discount stores) h. Custom furniture making i. Dental services j. Paper manufacturing k. Nut and bolt manufacturing l. Auto repair m. Architectural services n. Landscape design services o. Flashlight manufacturing Required: Identify each of these preceding types of businesses as using either job-order or process costing.arrow_forwardA manufacturing company has two service and two production departments. Human Resources and Machine Repair are the service departments. The production departments are Grinding and Polishing. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The human resources department services all departments of the company, and its costs are allocated using the numbers of employees within each department, while machine repair costs are allocable to Grinding and Polishing on the basis of machine hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,