Concept explainers

Videos

Comprehensive cycle problem: Perpetual system

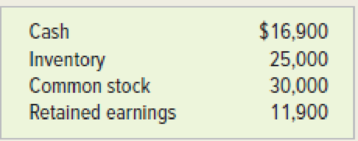

At the beginning of 2018, the Redd Company had the following balances in its accounts:

During 2018, the company experienced the following events:

1. Purchased inventory that cost $15,200 on account from Ross Company under terms 1/10, n/30. The merchandise was delivered FOB shipping point. Freight costs of $200 were paid in cash.

2. Returned $800 of the inventory that it had purchased because the inventory was damaged in transit. The seller agreed to pay the return freight cost.

3. Paid the amount due on its account payable to Ross Company within the cash discount period.

4. Sold inventory that had cost $18,000 for $32,000 on account, under terms 2/10, n/45.

5. Received merchandise returned from a customer. The merchandise originally cost $800 and was sold to the customer for $1,500 cash. The customer was paid $1,500 cash for the returned merchandise.

6. Delivered goods FOB destination in Event 4. Freight costs of $140 were paid in cash.

7. Collected the amount due on the

8. Took a physical count indicating that $21,100 of inventory was on hand at the end of the accounting period.

Required

a. Identify these events as asset source (AS), asset use (AU), asset exchange (AE), or claims exchange (CE).

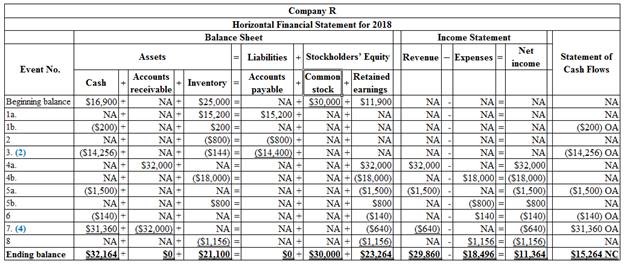

b. Record each event in a statements model like the following one.

c. Prepare a multistep income statement, a statement of changes in stockholders’ equity, a

a.

Identify the events as asset source (AS), asset use (AU), asset exchange (AE), or claims exchange (CE).

Explanation of Solution

Identify the events as asset source (AS), asset use (AU), asset exchange (AE), or claims exchange (CE).

| Event No. | Event type |

| 1a. | AS |

| 1b. | AE |

| 2. | AU |

| 3. | AU |

| 4a. | AS |

| 4b. | AU |

| 5a. | AU |

| 5b. | AS |

| 6. | AU |

| 7. | AU |

| 8. | AU |

Table (1)

- Asset source: All the transactions which increase assets either by borrowing from creditors (increase liabilities), or by earning operating revenues (increase in stockholders’ equity) are referred to as asset source transactions.

- Asset use: All the transactions which decrease assets either by paying off liabilities (decrease in liabilities), or by paying operating expenses (decrease in stockholders’ equity) are referred to as asset use transactions.

- Asset exchange: All the transactions which increase assets and decrease assets simultaneously, with no effect on the total assets value are referred to as asset exchange transactions.

- Claims exchange: All the transactions which include exchange of liabilities for equity are referred to as claims exchange transactions.

b.

Record each event in a statements model.

Explanation of Solution

Horizontal statements model: The model that represents all the financial statements, balance sheet, income statement, and statement of cash flows in one table in a horizontal form, is referred to as, horizontal statements model.

Record each event in a statements model.

Table (2)

Working Note:

(1) Compute purchase discount.

(2) Compute the cash paid for inventory purchased.

(3) Compute sales discount.

(4) Compute cash received.

c.

Prepare a multistep income statement, statement of stockholders’ equity, balance sheet, and statement of cash flows for Company R.

Explanation of Solution

Multi-step income statement: The income statement represented in multi-steps with several subtotals, to report the income from principal operations, and separate the other expenses and revenues which affect net income, is referred to as multi-step income statement.

Prepare a multistep income statement for Company R for the year ended December 31, 2018.

| Company R | ||

| Income Statement | ||

| For the Year Ended December 31, 2018 | ||

| Net sales | $29,860 | |

| Cost of goods sold (5) | ($18,356) | |

| Gross margin | $11,504 | |

| Operating expenses: | ||

| Transportation-out | ($140) | |

| Net income | $11,364 | |

Table (3)

Working Note:

(5) Determine the amount of cost of goods sold.

Statement of stockholders’ equity: The statement which reports the changes in stock, paid-in capital, retained earnings, and treasury stock, during the year is referred to as statement of stockholders’ equity.

Prepare a statement of stockholders’ equity for Company R for the year ended December 31, 2018.

| Company R | ||

| Statement of Stockholders’ Equity | ||

| For the Year Ended December 31, 2018 | ||

| Beginning common stock | $30,000 | |

| Add: Stock issued | $0 | |

| Ending common stock | $30,000 | |

| Beginning retained earnings | $11,900 | |

| Add: Net income | $11,364 | |

| Ending retained earnings | $23,264 | |

| Total stockholders’ equity | $53,264 | |

Table (4)

Balance sheet: This financial statement reports a company’s resources (assets) and claims of creditors (liabilities) and stockholders (stockholders’ equity) over those resources. The resources of the company are assets which include money contributed by stockholders and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and stockholders’ equity.

Prepare the balance sheet for Company R as at December 31, 2018.

| Company R | ||

| Balance Sheet | ||

| December 31, 2018 | ||

| Assets | ||

| Cash | $32,164 | |

| Merchandise inventory | $21,100 | |

| Total assets | $53,264 | |

| Liabilities | $0 | |

| Stockholders’ equity | ||

| Common stock | $30,000 | |

| Retained earnings | $23,264 | |

| Total stockholders’ equity | $53,264 | |

| Total liabilities and stockholders’ equity | $53,264 | |

Table (5)

Statement of cash flows: Statement of cash flows reports all the cash transactions which are responsible for inflow and outflow of cash and the result of these transactions is reported as ending balance of cash at the end of reported period.

Prepare the statement of cash flows for Company R for the year ended December 31, 2018.

| Company R | ||

| Statement of Cash Flows | ||

| For the Year Ended December 31, 2018 | ||

| Cash flows from operating activities: | ||

| Inflow from customers (6) | $29,860 | |

| Outflow for inventory (7) | ($14,456) | |

| Outflow for expenses | ($140) | |

| Net cash flow from operating activities | $15,624 | |

| Cash flows from investing activities | $0 | |

| Cash flows from financing activities | $0 | |

| Net change in cash | $15,624 | |

| Add: Beginning cash balance | $16,900 | |

| Ending cash balance | $31,164 | |

Table (6)

Working note:

(6) Determine the cash inflow from customers.

(7) Determine the cash outflow for inventory.

Want to see more full solutions like this?

Chapter 3 Solutions

Survey Of Accounting

- Continuing problem Palisade Creek Co. is a merchandising business that uses the perpetual inventory system. The account Balances for Palisade Creek Co. as of May 1, 2016 (unless otherwise indicated), are as follows: 110 Cash 83,600 112 Accounts Receivable 233,900 115 Merchandise Inventory 624,400 116 Estimated Returns Inventory 28,000 117 Prepaid Insurance 16,800 118 Store Supplies 11,400 123 Store Equipment 569,500 124 Accumulated DepreciationStore Equipment 56,700 210 Accounts Payable 96,600 211 Salaries Payable 212 Customers Refunds Payable 50,000 310 Common Stock 100,000 311 Retained Earnings 585,300 312 Dividends 135,000 313 Income Summary 410 Sales 5,069,000 510 Cost of Merchandise Sold 2,823,000 520 Sales Salaries Expense 664,800 521 Advertising Expense 281,000 522 Depreciation Expense 523 Store Supplies Expense 529 Miscellaneous Selling Expense 12,600 530 Office Salaries Expense 382,100 531 Rent Expense 83,700 532 Insurance Expense 539 Miscellaneous Administrative Expense 7,800 During May, the last month of the fiscal year, the following transactions were completed: May 1. Paid rent for May, 5,000. 3. Purchased merchandise on account from Martin Co. terms 2/10t n/30, FOB shipping point, 36,000. 4. Paid freight on purchase of May 3, 600. 6. Sold merchandise on account to Korman Co., terms 2/10, n/30, FOB shipping point, 68,500. The cost of the merchandise sold was 41,000. 7. Received 22,300 cash from Halstad Co. on account. 10. Sold merchandise for cash, 54,000. The cost of the merchandise sold was 32,000. 13. Paid for merchandise purchased on May 3- 15. Paid advertising expense for last half of May, 11,000. 16. Received cash from sale of May 6. 19. Purchased merchandise for cash, 18,700. 19. Paid 33,450 to Buttons Co. on account 20. Paid Korman Co. a cash refund of 13,230 for returned merchandise from sale of May 6. The invoice amount of the returned merchandise was 13,500 and the cost of the returned merchandise was 8,000. Record the following transactions on Page 21 of the journal: 20. Sold merchandise on account to Crescent Co., terms 1/10, n/30, FOB shipping point, 110,000. The cost of the merchandise sold was 70,000. 21. For the convenience of Crescent Co., paid freight on sale of May 20. 2,300. 21. Received 42,900 cash from Gee Co. on account. May 21. Purchased merchandise on account from Osterman Co., terms 1/10, n/30, FOB destination. 88,000. 24. Returned of damaged merchandise purchased on May 21, receiving a credit memo from the seller for 5,000. 26. Refunded cash on sales made for cash. 7,500. The cost of the merchandise returned was 4,800. 28. Paid sales salaries of 56,000 and office salaries of 29,000. 29. Purchased store supplies for cash, 2,400. 30. Sold merchandise on account to Turner Co., terms 2/10, n/30, FOB shipping point, 78,750. The cost of the merchandise sold was 47,000. 30. Received cash from sale of May 20 plus freight paid on May 21. 31. Paid for purchase of May 21. less return of May 24. Instructions 1. Enter the balances of each of the accounts in the appropriate balance column of a four-column account. Write Balance in the item section, and place a check mark () in the Posting Reference column. Journalize the transactions for July, starting on Page 20 of the journal. 2. Post the journal to the general ledger, extending the month-end balances to the appropriate balance columns after all posting is completed. In this problem, you are not required to update or post to the accounts receivable and accounts payable subsidiary ledgers. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete (5) and (6). a. Merchandise inventory on May 31 570,000 b. Insurance expired during the year 12,000 c. Store supplies on hand on May 31 4,000 d. Depreciation for the current year 14,000 e. Accrued salaries on May 31: Sales salaries 7,000 Office salaries 6,600 13,600 f. The adjustment for customer returns and allowances is 60,000 for sales and 35,000 for cost of merchandise sold. 5. (Optional) Enter the unadjusted trial balance on a 10-column end-of-period spreadsheet (work sheet), and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 22 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a retained earnings statement, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 23 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. Insert the new balance in the retained earnings account. 10. Prepare a post-closing trial balance.arrow_forwardAnalyzing the Accounts Casey Company uses a perpetual inventory system and engaged in the following transactions: a. Made credit sales of $825,000. The cost of the merchandise sold was $560,000. b. Collected accounts receivable in the amount of $752,600. c. Purchased goods on credit in the amount of $574,300. d. Paid accounts payable in the amount of $536,200. Required: Prepare the journal entries necessary to record the transactions. Indicate whether each transaction increased cash, decreased cash, or had no effect on cash.arrow_forwardWorksheet, Including Inventory Surian Motors Company prepared a trial balance on the following partially completed worksheet for the year ended December 31, 2019: Additional information: (a) The equipment is being depreciated on a straight-line basis over a 10-year life, with no residual value; (b) salaries accrued but nor recorded total 500; (c) on January 1, 2019, the company had paid 3 years rent in advance at 100 per month; (d) bad debts are expected to be 1% of total sales; (e) interest of 400 has accrued on the note payable; and (f) the income tax rate is 40% on current income and will be paid in the first quarter of 2020. Required: 1. Complete the worksheet. 2. Prepare financial statements for 2019. 3. Prepare closing entries in the general journal.arrow_forward

- Effects of an Inventory Error The income statements for Graul Corporation for the 3 years ending in 2019 appear below. During 2019, Graul discovered that the 2017 ending inventory had been misstated due to the following two transactions being recorded incorrectly. a. A purchase return of inventory costing $42,000 was recorded twice. b. A credit purchase of inventory' made on December 20 for $28,500 was not recorded. The goods were shipped F.O.B. shipping point and were shipped on December 22, 2017. Required: 1. Was ending inventory for 2017 overstated or understated? By how much? 2. Prepare correct income statements for all 3 years. 3. CONCEPTUAL CONNECTION Did the error in 2017 affect cumulative net income for the 3-year period? Explain your response. 4. CONCEPTUAL CONNECTION Why was the 2019 net income unaffected?arrow_forwardPalisade Creek Co. is a merchandising business that uses the perpetual inventory system. The account balances for Palisade Creek Co. as of May 1, 2016 (unless otherwise indicated), are as follows: During May, the last month of the fiscal year, the following transactions were completed: May 1. Paid rent for May, 5,000. 3. Purchased merchandise on account from Martin Co., terms 2/10, n/30, FOB shipping point, 36,000. 4. Paid freight on purchase of May 3, 600. 6. Sold merchandise on account to Korman Co., terms 2/10, n/30, FOB shipping point, 68,500. The cost of the merchandise sold was 41,000. 7. Received 22,300 cash from Halstad Co. on account. 10. Sold merchandise for cash, 54,000. The cost of the merchandise sold was 32,000. 13. Paid for merchandise purchased on May 3. 15. Paid advertising expense for last half of May, 11,000. 16. Received cash from sale of May 6. 19. Purchased merchandise for cash, 18,700. 19. Paid 33,450 to Buttons Co. on account. 20. Paid Korman Co. a cash refund of 13,230 for returned merchandise from sale of May 6. The invoice amount of the returned merchandise was 13,500 and the cost of the returned merchandise was 8,000. Record the following transactions on Page 21 of the journal: 20. Sold merchandise on account to Crescent Co., terms 1/10, n/30, FOB shipping point, 110,000. The cost of the merchandise sold was 70,000. 21. For the convenience of Crescent Co., paid freight on sale of May 20, 2,300. 21. Received 42,900 cash from Gee Co. on account. May 21. Purchased merchandise on account from Osterman Co., terms 1/10, n/30, FOB destination, 88,000. 24. Returned of damaged merchandise purchased on May 21, receiving a credit memo from the seller for 5,000. 26. Refunded cash on sales made for cash, 7,500. The cost of the merchandise returned was 4,800. 28. Paid sales salaries of 56,000 and office salaries of 29, 000. 29. Purchased store supplies for cash, 2,400. 30. Sold merchandise on account to Turner Co., terms 2/10, n/30, FOB shipping point, 78,750. The cost of the merchandise sold was 47,000. 30. Received cash from sale of May 20 plus freight paid on May 21. 31. Paid for purchase of May 21, less return of May 24. Instructions 1. Enter the balances of each of the accounts in the appropriate balance column of a four-column account. Write Balance in the item section, and place a check mark () in the Posting Reference column. Journalize the transactions for July, starting on Page 20 of the journal. 2. Post the journal to the general ledger, extending the month-end balances to the appropriate balance columns after all posting is completed. In this problem, you are not required to update or post to the accounts receivable and accounts payable subsidiary ledgers. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete (5) and (6). f. The adjustment for customer returns and allowances is 60,000 for sales and 35,000 for cost of merchandise sold. 5. (Optional) Enter the unadjusted trial balance on a IO-column end-of-period spreadsheet (work sheet), and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 22 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of owners equity, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 23 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. Insert the new balance in the owners capital account. 10. Prepare a post-closing trial balance.arrow_forwardRescue Sequences LLC purchased inventory by issuing a 30,000, 10%, 60-day note on October 1. Prepare the journal entries for Rescue Sequences to record the purchase and payment assuming it uses a perpetual inventory system and a 360-day calendar fiscal year. Rescue Sequences LLC uses a perpetual inventory system.arrow_forward

- Refer to the information in E22-13. Required: Prepare the correcting journal entries if the company discovers each error 2 years after it is made and it has closed the books for the second year. Ignore income taxes. E22-13: The following are independent errors made by a company that uses the periodic inventory system: a. Goods in transit, purchased on credit and shipped FOB destination, 10,000, were included in purchases but not in the physical count of ending inventory. b. Purchase of a machine for 2,000 was expensed. The machine has a 4-vear life, no residual value, and straight-line depreciation is used. c. Wages payable of 2,000 were not accrued. d. Payment of next years rent, 4,000, was recorded as rent expense. e. Allowance for doubtful accounts of 5,000 was not recorded. The company normally uses the aging method. f. Equipment with a book value of 70,000 and a fair value of 100,000 was sold at the beginning of the year. A 2-year, non-interest-bearing note for 129,960 was received and recorded at its face value, and a gain of 59,960 was recognized. No interest revenue was recorded and 14% is a fair rate of interest.arrow_forward( Appendices 6A and 6B) Inventory Costing Methods Edwards Company began operations in February 2019. Edwards accounting records provide the following data for the remainder of 2019 for one of the items the company sells: Â Edwards uses a periodic inventory system. All purchases and sales were for cash. Required: 1. Compute cost of goods sold and the cost of ending inventory using FIFO. 2. Compute cost of goods sold and the cost of ending inventory using LIFO. 3. Compute cost of goods sold and the cost of ending inventory using the average cost method. ( Note: Use four decimal places for per-unit calculations and round all other numbers to the nearest dollar.) 4. Prepare the journal entries to record these transactions assuming Edwards chooses to use the FIFO method. 5. CONCEPTUAL CONNECTION Which method would result in the lowest amount paid for taxes? 6. CONCEPTUAL CONNECTION Refer to Problem 6-67B and compare your results. What are the differences? Be sure to explain why the differences occurred.arrow_forwardRecording Sale and Purchase Transactions Alpharack Company sells a line of tennis equipment to retailers. Alpharack uses the perpetual inventory system and engaged in the following transactions during April 2019, its first month of operations: a. On April 2, Alpharack purchased, on credit, 360 Wilbur T-100 tennis rackets with credit terms of 2/10, n/30. The rackets were purchased at a cost of S30 each. Alpharack paid Barker Trucking $195 to transport the tennis rackets from the manufacturer to Alpharacks warehouse, shipping terms were F.O.B. shipping point, and the items were shipped on April 2. b. On April 3, Alpharack purchased, for cash, 115 packs of tennis balls for $10 per pack. c. On April 4, Alpharack purchased tennis clothing, on credit, from Designer Tennis Wear. The cost of the clothing was $8,250. Credit terms were 2/10, n/25. d. On April 10, Alpharack paid for the purchase of the tennis rackets in Transaction a. e. On April 15, Alpharack determined that $325 of the tennis clothing was defective. Alpharack returned the defective merchandise to Designer Tennis Wear. f. On April 20, Alpharack sold 1 18 tennis rackets at $90 each, 92 packs of tennis balls at $12 per pack, and $5,380 of tennis clothing. All sales were for cash. The cost of the merchandise sold was $7,580 and no sales returns are expected. g. On April 23, customers returned $860 of the merchandise purchased on April 20. The cost of the merchandise returned was $450. h. On April 25, Alpharack sold another 55 tennis rackets, on credit, for $90 each and 15 packs of tennis balls at $12 per pack, for cash. The cost of the merchandise sold was $1,800. i. On April 29, Alpharack paid Designer Tennis Wear for the clothing purchased on April 4 minus the return on April 15. j. On April 30, Alpharack purchased 20 tennis bags, on credit, from Bag Designs for $320. The bags were shipped F.O.B. destination and arrived at Alpharack on May 3. Required: 1. Prepare the journal entries to record the sale and purchase transactions for Alpharack during April 2019. 2. Assuming operating expenses of $8,500 and income taxes of $1,180, prepare Alpharacks income statement for April 2019.arrow_forward

- Transaction Analysis Pollys Cards $ Gifts Shop had the following transactions during the year: Pollys purchased inventory on account from a supplier for $8,000. Assume that Pollys uses a periodic inventory system. On May 1, land was purchased for $44,500. A 20% down payment was made, and an 18-month, 8% note was signed for the remainder. Pollys returned $450 worth of inventory purchased in (a), which was found broken when the inventory was received. Pollys paid the balance due on the purchase of inventory. On June 1, Polly signed a one-year, $15,000 note to First State Bank and received $13,800. Pollys sold 200 gift certificates for $25 each for cash. Sales of gift certificates are recorded as a liability. At year-end, 35% of the gift certificates had been redeemed. Sales for the year were $120,000, of which 90% were for cash. State sales tax of 6% applied to all sales must be remitted to the state by January 31. Required Record all necessary journal entries relating to these transactions. Assume that Pollys accounting year ends on December 31. Prepare any necessary adjusting journal entries. What is the total of the current liabilities at the end of the year?arrow_forwardGoods in Transit Gravais Company made two purchases on December 29, 2019. One purchase for 3,000 was shipped FOB destination, and the second for 4,000 was shipped FOB shipping point. Neither purchase had been received nor paid for on December 31, 2019. Required: Which of these purchases, if either, does Gravais include in inventory on December 31, 2019? What is the cost?arrow_forwardRefer to RE22-2. Assume Heller Company had sales revenue of 510,000 in 2019 and 650,000 in 2020. Prepare Hellers partial income statements (through gross profit) for 2019 and 2020. RE22-2 Heller Company began operations in 2019 and used the LIFO method to compute its 300,000 cost of goods sold for that year. At the beginning of 2020, Heller changed to the FIFO method. Heller determined that its cost of goods sold under FIFO would have been 250,000 in 2019. For 2020, Hellers cost of goods sold under FIFO was 360,000, while it would have been 410,000 under LIFO. Heller is subject to a 21% income tax rate. Compute the cumulative effect of the retrospective adjustment on prior years income (net of taxes) that Heller would report on its retained earnings statement for 2020.arrow_forward

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning