Concept explainers

Videos

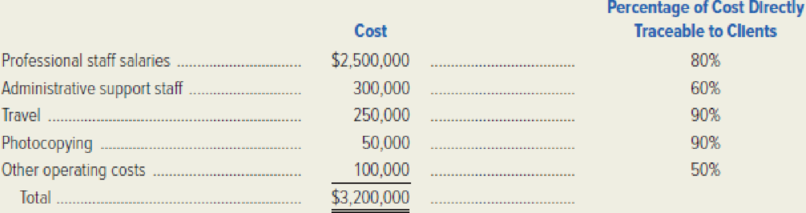

JLR Enterprises provides consulting services throughout California and uses a

JLR’s director of cost management, Brent Dean, anticipates the following costs for the upcoming year:

The firm’s partners desire to make a $640,000 profit for the firm and plan to add a percentage markup on total cost to achieve that figure.

On March 10, JLR completed work on a project for Martin Manufacturing. The following costs were incurred: professional staff salaries, $41,000; administrative support staff, $2,600; travel, $4,500; photocopying, $500; and other operating costs, $1,400.

Required:

- 1. Determine JLR’s total traceable costs for the upcoming year and the firm’s total anticipated overhead.

- 2. Calculate the predetermined overhead rate. The rate is based on total costs traceable to client jobs.

- 3. What percentage of cost will JLR add to each job to achieve its profit target?

- 4. Determine the total cost of the Martin Manufacturing project. How much would Martin be billed for services performed?

- 5. Notice that only 50 percent of JLR’s other operating cost is directly traceable to specific client projects. Cite several costs that would be included in this category and difficult to trace to clients.

- 6. Notice that 80 percent of the professional staff cost is directly traceable to specific client projects. Cite several reasons that would explain why this figure isn’t 100 percent.

Want to see the full answer?

Check out a sample textbook solution

Chapter 3 Solutions

Managerial Accounting: Creating Value in a Dynamic Business Environment

- The following describes the job responsibilities of two employees of Barney Manufacturing. Joan Dennison, Cost Accounting Manager. Joan is responsible for measuring and collecting costs associated with the manufacture of the garden hose product line. She is also responsible for preparing periodic reports that compare the actual costs with planned costs. These reports are provided to the production line managers and the plant manager. Joan helps to explain and interpret the reports. Steven Swasey, Production Manager. Steven is responsible for the manufacture of the high-quality garden hose. He supervises the line workers, helps to develop the production schedule, and is responsible for seeing that production quotas are met. He is also held accountable for controlling manufacturing costs. Required: CONCEPTUAL CONNECTION Identify Joan and Steven as line or staff and explain your reasons.arrow_forwardA manufacturing company has two service and two production departments. Human Resources and Machine Repair are the service departments. The production departments are Grinding and Polishing. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The human resources department services all departments of the company, and its costs are allocated using the numbers of employees within each department, while machine repair costs are allocable to Grinding and Polishing on the basis of machine hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardGeneva, Inc., makes two products, X and Y, that require allocation of indirect manufacturing costs. The following data were compiled by the accountants before making any allocations: The total cost of purchasing and receiving parts used in manufacturing is 60,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were 48,000 and 12,000 for X and Y, respectively. If an activity-based system is used, what would be the allocated costs for each product?arrow_forward

- A manufacturing company has two service and two production departments. Building Maintenance and Factory Office are the service departments. The production departments are Assembly and Machining. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The building maintenance department services all departments of the company, and its costs are allocated using floor space occupied, while factory office costs are allocable to Assembly and Machining on the basis of direct labor hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardWalsh & Coggins, a professional accounting firm, collects cost information about the services they provide to their clients. Describe the types of cost data they would collect and explain the importance of analyzing this cost data.arrow_forwardA CPA would recommend changing from plantwide overhead rate application to departmental rates under which of the following circumstances? a. The plant produces one product. b. The plant produces multiple products that may or may not pass through all producing departments. c. The plant produces multiple products that pass through all of the producing departments. d. The plant produces many different products that consume the same amount of resources in each producing department.arrow_forward

- Cynthia Rogers, the cost accountant for Sanford Manufacturing, is preparing a management report that must include an allocation of overhead. The budgeted overhead for each department and the data for one job are as follows: Using the departmental overhead application rates, and allocating overhead on the basis of direct labor hours, overhead applied to Job 231 in the Tooling Department would be: a. 44.00. b. 197.50. c. 241.50. d. 501.00.arrow_forwardWhat factors would you consider in deciding whether to use direct labor dollars or direct labor hours in charging overhead to jobs in a service firm?arrow_forwardRandy Harris, controller, has been given the charge to implement an advanced cost management system. As part of this process, he needs to identify activity drivers for the activities of the firm. During the past four months, Randy has spent considerable effort identifying activities, their associated costs, and possible drivers for the activities costs. Initially, Randy made his selections based on his own judgment using his experience and input from employees who perform the activities. Later, he used regression analysis to confirm his judgment. Randy prefers to use one driver per activity, provided that an R2 of at least 80 percent can be produced. Otherwise, multiple drivers will be used, based on evidence provided by multiple regression analysis. For example, the activity of inspecting finished goods produced an R2 of less than 80 percent for any single activity driver. Randy believes, however, that a satisfactory cost formula can be developed using two activity drivers: the number of batches and the number of inspection hours. Data collected for a 14-month period are as follows: Required: 1. Calculate the cost formula for inspection costs using the two drivers, inspection hours and number of batches. Are both activity drivers useful? What does the R2 indicate about the formula? 2. Using the formula developed in Requirement 1, calculate the inspection cost when 300 inspection hours are used and 30 batches are produced. Prepare a 90 percent confidence interval for this prediction.arrow_forward

- John Sheng, a cost accountant at Starlet Company, is developing departmental factory overhead application rates for the companys Tooling and Fabricating departments. The budgeted overhead for each department and the data for one job are as follows: Using the departmental overhead application rates, total overhead applied to Job 231 in the Tooling and Fabricating departments will be: a. 225. b. 303. c. 537. d. 671.arrow_forwardDarnell Poston, owner of Poston Manufacturing, Inc., wants to determine the cost behavior of labor and overhead. Darnell pays his workers a salary; during busy times, everyone works to get the orders out. Temps (temporary workers hired through an agency) may be hired to pack and prepare completed orders for shipment. During slower times, Darnell catches up on bookkeeping and administrative tasks while the salaried workers do preventive maintenance, clean the lines and building, etc. Temps are not hired during slow times. Darnell found that workers salaries, temp agency payments, rentals, utilities, and plant and equipment depreciation are the largest dollar accounts. He believes that workers salaries and plant and equipment depreciation are fixed, temp agency payments are associated with the number of orders (since temp workers are used to pack and prepare completed orders for shipment), and electricity is associated with the number of machine hours. When the number of different parts stored by Poston exceeds the space in the materials storeroom, Darnell rents nearby warehouse space. He can rent as much or as little space as he wants on a month-to-month basis. Therefore, he believes warehouse rental payments are variable with the number of parts purchased and stored. The account balances for the past six months as well as the six-month total are as follows: Information on number of machine hours, orders, and parts for the six-month period follows: Required: 1. Calculate the monthly average account balance for each account. Calculate the average monthly amount for each of the three drivers. 2. Calculate fixed monthly cost and the variable rates for temp agency payments, warehouse rent, and electricity. Express the results in the form of an equation for total cost. 3. In July, Darnell predicts there will be 420 orders, 250 parts, and 5,900 machine hours. What is the total labor and overhead cost for July? 4. What if Darnell buys a new machine in July for 24,000? The machine is expected to last 10 years and will have no salvage value at the end of that time. What part of the cost equation will be affected? How? What is the new expected cost in July?arrow_forwardBounce Back Insurance Company carries three major lines of insurance: auto, workers compensation, and homeowners. The company has prepared the following report: Management is concerned that the administrative expenses may make some of the insurance lines unprofitable. However, the administrative expenses have not been allocated to the insurance lines. The controller has suggested that the administrative expenses could be assigned to the insurance lines using activity-based costing. The administrative expenses are comprised of five activities. The activities and their rates are as follows: Activity-base usage data for each line of insurance were retrieved from the corporate records as follows: a. Complete the product profitability report through the administrative activities. Determine the operating income as a percent of premium revenue, rounded to the nearest whole percent. b. Interpret the report.arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning