INTERMEDIATE ACCT VOL.2>CUSTOM<

9th Edition

ISBN: 9781307165067

Author: SPICELAND

Publisher: MCG/CREATE

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 12, Problem 12.9E

Securities available-for-sale;

• LO12-4

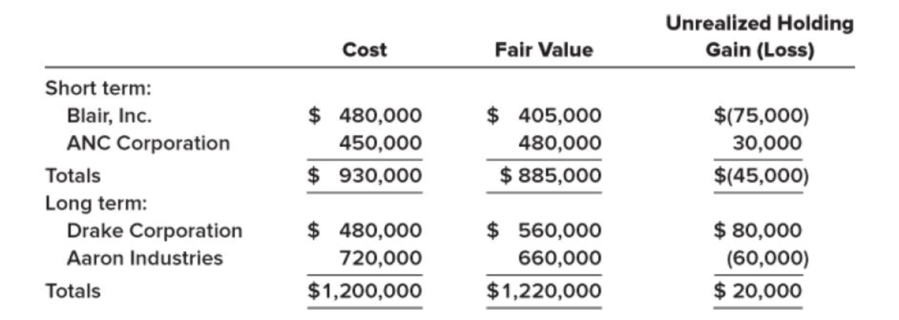

Loreal-American Corporation purchased several marketable securities during 2018. At December 31, 2018, the company had the investments in bonds listed below. None was held at the last reporting date, December 31, 2017, and all are considered securities available-for-sale.

Required:

1. Prepare appropriate adjusting entries at December 31, 2018.

2. What amounts would be reported in the income statement at December 31, 2018, as a result of these adjusting entries?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

E17.6 (LO1) (HFCS Debt Securities Entries and Financial Statement Presentation) At December 31, 2019, the held-for-collection and selling debt portfolio for Steffi Graf SA is as follows.

Security Amortized Cost Fair Value Unrealized Gain (Loss)

A €17,500 €15,000 (€2,500)

B 12,500 14,000 1,500

C 23,000 25,500 2,500

Total €53,000 €54,500 1,500

Previous fair value adjustment balance-Dr. 400

Fair value adjustment-Dr. €1,100 On January 20, 2020, Steffi Graf SA sold security A for €15,100. The sale proceeds are net of brokerage fees.

Instructions

a. Prepare the adjusting entry at December 31, 2019, to report the portfolio at fair value.

b. Show the statement of financial…

On December 31, 2021, Kona purchased debt securities as trading securities. Pertinent data are as follows:\\n Fair Value\\nSecurity Cost At 12/31/22\\nA $225,000 $215,000\\nB 200,000 210,000\\nC 230,000 210,000\\nOn December 31, 2022, Kona transferred its investment in security C from trading to available‐for‐sale\\nbecause Kona intends to retain security C as a long‐term investment. What total amount of gain or loss on\\nits securities should be included in Kona's income statement for the year ended December 31, 2022?

#6 answer only SUB PARTS

Recording Entries for TS—Effective Interest Method

Adjust FVA at Year-End

On July 1, 2020, West Company purchased for cash, twelve $10,000 bonds of North Corporation at a market rate of 6%. The bonds pay 5% interest, payable on a semiannual basis each July 1 and January 1, and mature on July 1, 2023. The bonds are classified as trading securities. The annual reporting period ends December 31. Assume the effective interest method of amortization of any discounts or premiums. Ignore income taxes.

a. Prepare a bond amortization schedule for the life of the bonds using the effective interest method.

Note: Round each amount entered into the schedule to the nearest whole dollar. Use the rounded amount for later calculations in the schedule. Adjust market interest in the final year of the bond term for any net rounding difference.

Date

StatedInterest

MarketInterest

DiscountAmortization

BondAmortized Cost

Jul. 1, 2020

Answer

Jan. 1, 2021

Answer

Answer…

Chapter 12 Solutions

INTERMEDIATE ACCT VOL.2>CUSTOM<

Ch. 12 - All investments in debt securities are classified...Ch. 12 - When market rates of interest rise after a...Ch. 12 - Does GAAP distinguish between fair values that are...Ch. 12 - When a debt investment is acquired to be held for...Ch. 12 - Prob. 12.5QCh. 12 - What is comprehensive income? Its composition...Ch. 12 - Why are holding gains and losses treated...Ch. 12 - Prob. 12.8QCh. 12 - Prob. 12.9QCh. 12 - Prob. 12.10Q

Ch. 12 - Under IFRS No. 9, which reporting categories are...Ch. 12 - Prob. 12.12QCh. 12 - Do U.S. GAAP and IFRS differ in the amount of...Ch. 12 - Under what circumstances is the equity method used...Ch. 12 - The equity method has been referred to as a...Ch. 12 - In the application of the equity method, how...Ch. 12 - Prob. 12.17QCh. 12 - Prob. 12.18QCh. 12 - Prob. 12.19QCh. 12 - How does IFRS differ from U.S. GAAP with respect...Ch. 12 - What is the effect of a company electing the fair...Ch. 12 - Define a financial instrument. Provide three...Ch. 12 - Some financial instruments are called derivatives....Ch. 12 - (Based on Appendix 12A) Northwest Carburetor...Ch. 12 - Prob. 12.25QCh. 12 - Prob. 12.26QCh. 12 - (Based on Appendix 12B) Reporting an investment at...Ch. 12 - Prob. 12.28QCh. 12 - Explain how the CECL model (introduced in ASU No....Ch. 12 - Prob. 12.30QCh. 12 - Prob. 12.1BECh. 12 - Prob. 12.2BECh. 12 - Trading securities LO12-3 For the Coca-Cola bonds...Ch. 12 - Available -for-sale securities LO12-4 SL...Ch. 12 - Available -for-sale securities LO12-4 For the...Ch. 12 - Prob. 12.6BECh. 12 - Prob. 12.7BECh. 12 - Prob. 12.8BECh. 12 - Prob. 12.9BECh. 12 - Prob. 12.10BECh. 12 - Equity investments and dividends LO12-5 Turner...Ch. 12 - Prob. 12.12BECh. 12 - Prob. 12.13BECh. 12 - Equity method investments LO12-6, LO12-9 Kim...Ch. 12 - Change in principle; change to the equity method ...Ch. 12 - Fair value option; equity method investments ...Ch. 12 - Prob. 12.17BECh. 12 - Impairments (AFS Credit Loss Model) (Appendix 12B)...Ch. 12 - Prob. 12.19BECh. 12 - Prob. 12.20BECh. 12 - Prob. 12.1ECh. 12 - Prob. 12.2ECh. 12 - Securities held-to-maturity LO12-1 FFT...Ch. 12 - Prob. 12.4ECh. 12 - Prob. 12.5ECh. 12 - Trading securities LO12-1 [This is a variation of...Ch. 12 - Various transactions relating to trading...Ch. 12 - Prob. 12.8ECh. 12 - Securities available-for-sale; adjusting entries ...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Classification of securities; adjusting entries ...Ch. 12 - Prob. 12.14ECh. 12 - Equity investments; fair value through net income ...Ch. 12 - Equity investments; fair value through net income ...Ch. 12 - Prob. 12.17ECh. 12 - Equity investments; fair value through net income ...Ch. 12 - Investment securities and equity method...Ch. 12 - Equity method; purchase; investee income;...Ch. 12 - Error corrections; equity method investment ...Ch. 12 - Prob. 12.22ECh. 12 - Prob. 12.23ECh. 12 - Prob. 12.24ECh. 12 - Prob. 12.25ECh. 12 - Prob. 12.26ECh. 12 - Prob. 12.27ECh. 12 - Prob. 12.28ECh. 12 - Prob. 12.29ECh. 12 - Prob. 12.30ECh. 12 - Prob. 12.31ECh. 12 - Prob. 12.32ECh. 12 - Accounting for impairments under IFRS (Appendix...Ch. 12 - Prob. 12.1PCh. 12 - Prob. 12.2PCh. 12 - Securities available-for-sale; bond investment;...Ch. 12 - Prob. 12.4PCh. 12 - Various transactions related to trading securities...Ch. 12 - Various transactions related to securities...Ch. 12 - Prob. 12.7PCh. 12 - Various transactions relating to trading...Ch. 12 - Securities held-to-maturity; securities available...Ch. 12 - Investment securities and equity method...Ch. 12 - Prob. 12.11PCh. 12 - Prob. 12.12PCh. 12 - Prob. 12.13PCh. 12 - Equity method LO12-6, LO12-7 On January 2, 2018,...Ch. 12 - Prob. 12.15PCh. 12 - Prob. 12.16PCh. 12 - Accounting for debt and equity investments ...Ch. 12 - Prob. 12.18PCh. 12 - Real World Case 121 Intels investments LO12-4 The...Ch. 12 - Prob. 12.2BYPCh. 12 - Prob. 12.4BYPCh. 12 - Prob. 12.6BYPCh. 12 - Real World Case 127 Comprehensive income Microsoft...Ch. 12 - Continuing Cases Target Case LO12-4, LO12-6...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Transfer between Categories On December 31, 2018, Leslie Company held an investment in bonds of Kaufmann Company which it categorized as being held to maturity. At that time, the 8%, 100,000 face value bonds had a carrying value of 107,023.56 and were being amortized using the effective interest method based on a market rate of 7%. Interest on these bonds is paid annually each December 31. On December 31, 2019, after recording the interest earned, Leslie decided to reclassify the Kaufmann bonds to its available-for-sale category in anticipation of a major restructuring. At that time, the ending quoted market price for the bonds was 105,000. Required: Prepare the journal entries on December 31, 2019, to record the interest earned and the reclassification.arrow_forwardTrading Securities Pear Investments began operations in 2020 and invests in securities classified as trading securities. During 2020, it entered into the following trading security transactions: Purchased 20,000 shares of ABC common stock at $38 per share Purchased 32,000 shares of XYZ common stock at $17 per share At December 31, 2020, ABC common stock was trading at $39.50 per share and XYZ common stock was trading at $16.50 per share. Required: 1. Prepare the necessary adjusting entry to value the trading securities at fair market value. 2. CONCEPTUAL CONNECTION What is the income statement effect of this adjusting entry?arrow_forward5. On May 1, 2019, Ed Company purchased a short-term P2.000.000 face value, 9% debt instruments for P1,860,000 including the accrued interest and classified it as a trading security. The debt instruments mature on January 1, 2022, and pay interest semi-annually on January 1 and July1. On December 31, the fair market value of the instruments is 98. On March 2, 2020, Ed sold the trading securities for P1,980,000. How much should Ed report the investment on December 31, 2019? 1,960,000 1,800,000 1,860,000 1,980,000 6. On October 1, 2019, Kite Corporation purchased a debt security having a face value of P3,000,000 with an interest rate of 10% for P3,200,000 inclusive of the accrued interest to be held as financial assets at amortized cost. A total of P50,000 was incurred and paid by Kite in relation to the acquisition of the debt instrument. The bonds mature on January 1, 2024, and pay interest semi-annually on January 1 and July 1. On December 31, 2019, the bonds had a market value of…arrow_forward

- No investments were sold during 2018. All securities except Security D and Security F are considered shortterm investments. None of the fair value changes is considered permanent.Required:Determine the following amounts at December 31, 2018.1. Investments reported as current assets2. Investments reported as noncurrent assets3. Unrealized gain (or loss) component of income before taxes4. Unrealized gain (or loss) component of accumulated other comprehensive income in shareholders’ equityarrow_forwardOn February 18, 2018, Union Corporation purchased $1,139,000 of IBM bonds. Union will hold the bonds indefinitely, and may sell them if their increases sufficiently. On December 31, 2018, and December 31, 2019, the market value of the bonds was $1,105,000 and $1,156,000, respectfully. Prepare the adjusting entry for December 31, 2018 and 2019. The answer they have is: Dec 31,2018 Unrealized holding gain 34,000 Fair value adjustment 34,000 Dec 31,2019 Fair value adjustment 51,000 Unrealized holding gain 51,000 Please show me the calculation steps for the answer: $51,000. How do you get this number?arrow_forwardIn 2019, Edward Company purchased equity securities as a trading investment. For the year ended December 31, 2019, the entity recognized an unrealized holding loss of P230,000. There were no security transactions during 2020. Pertinent information on December 31, 2020 is as follows: Security Cost Market Value A 2,450,000 2,300,000 B 1,800,000 1,820,000 4,250,000 4,120,000 In the 2020 income statement, what amount should be reported as unrealized holding gain or loss?arrow_forward

- Please avoid solution in an image format thanku On January 1, 2016, Hyde Corporation purchased bonds with a face value of $300,000 for $308,373.53. The bonds are due June 30, 2019, carry a 13% stated interest rate, and were purchased to yield 12%. Interest is payable semiannually on June 30 and December 31. On March 31, 2017, in contemplation of a major acquisition, the company sold one-half the bonds for $159,500 including accrued interest; the remainder were held until maturity. Required: Prepare the journal entries to record the purchase of the bonds, each interest payment, the partial sale of the investment on March 31, 2017, and the retirement of the bond issue on June 30, 2019.arrow_forwardI ONLY NEED ANSWER OF 16,17 &18 PLEASE KINDLY ANSWER Problem 3:On June 1, 2021, VIXEN Company received ₱1,077,200 plus accrued interest for 12% bonds with face amount of ₱1,000,000. The bonds were sold to yield 10%. Interest is payable semiannually every July 1 and December 31. The entity elected the fair value option for measuring financial liabilities. On December 31, 2020, the fair value of the bonds is at 108. The change in fair value of the bonds is attributable to market factors.Requirements:E. Prepare all necessary entries for calendar year 2021.F. Compute or provide the answers for the following:14. How much is initial valuation of the bonds?15. How much cash was received upon the sale of the bonds?16. How much is the interest expense for the year ended December 31, 2021?17. How much is the gain or loss from change in fair value of the bonds for 2021? (In the google form, if loss, put a negative sign before the numerical figure.)18. What is the carrying amount of the…arrow_forward(a) Assuming no Fair Value Adjustment account balance at the beginning of the year, prepare the adjusting entry at the end of the year if Laura Company's available-for-sale debt securities have a fair value $60,000 below cost. (b) Assume the same information as part (a), except that Laura Company has a debit balance in its Fair Value Adjustment account of $10,000 at the beginning of the year. Prepare the adjusting entry at year-end.arrow_forward

- Recording Entries for Impairment of Investments—AFS Atlanta Inc. holds an AFS bond investment in Falcons Corporation. The amortized cost of the investment is $351,250 on December 31, 2020. Atlanta Inc. estimates the fair value of the bonds to be $325,000. The unrealized loss of $26,250 is partially due to a credit loss of $20,000, with the remaining portion due to other factors. The company adjusted the AFS bonds to fair value through OCI on December 31, 2020. a. Record the impairment loss on December 31, 2020, assuming that the company does not intend to sell the investment and does not believe it is more likely than not that it will be required to sell the investment before recovery of any unrealized loss.b. Record the impairment loss on December 31, 2020, now assuming that the company intends to sell the investment. Note: List multiple debits or credits (when applicable) in alphabetical order. Date Account Name Dr. Cr. a. Dec. 31, 2020 Answer Answer…arrow_forwardHobson Company bought the securities listed below during 2020. These securities were classified as trading securities. In its December 31, 2020, income statement Hobson reported a net unrealized holding loss of $16,000 on these securities. Pertinent data at the end of June 2021 is as follows: Security Cost Fair Value X $ 381,500 $ 344,000 Y 185,500 162,700 Z 424,000 408,200 What amount of unrealized holding loss on these securities should Hobson include in its income statement for the six months ended June 30, 2021? $76,100. $16,000. $0. $60,100.arrow_forwardI need help with requried 2 please Colah Company purchased $2,000,000 of Jackson, Inc., 6% bonds at par on July 1, 2021, with interest paid semi-annually. Colah determined that it should account for the bonds as an available-for-sale investment. At December 31, 2021, the Jackson bonds had a fair value of $2,300,000. Colah sold the Jackson bonds on July 1, 2022 for $1,800,000. Required:1. Prepare Colah’s journal entries for the following transactions: The purchase of the Jackson bonds on July 1. Interest revenue for the last half of 2021. Any year-end 2021 adjusting entries. Interest revenue for the first half of 2022. Any entries necessary upon sale of the Jackson bonds on July 1, 2022, including updating the fair-value adjustment, recording any reclassification adjustment, and recording the sale. 2. Complete the following table to show the effect of the Jackson bonds on Colah’s net income, other comprehensive income, and comprehensive income for 2021, 2022, and cumulatively over…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Financial instruments products; Author: fi-compass;https://www.youtube.com/watch?v=gvxozM3TUIg;License: Standard Youtube License