INTERMEDIATE ACCT VOL.2>CUSTOM<

9th Edition

ISBN: 9781307165067

Author: SPICELAND

Publisher: MCG/CREATE

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 12, Problem 12.7BYP

Real World Case 12–7

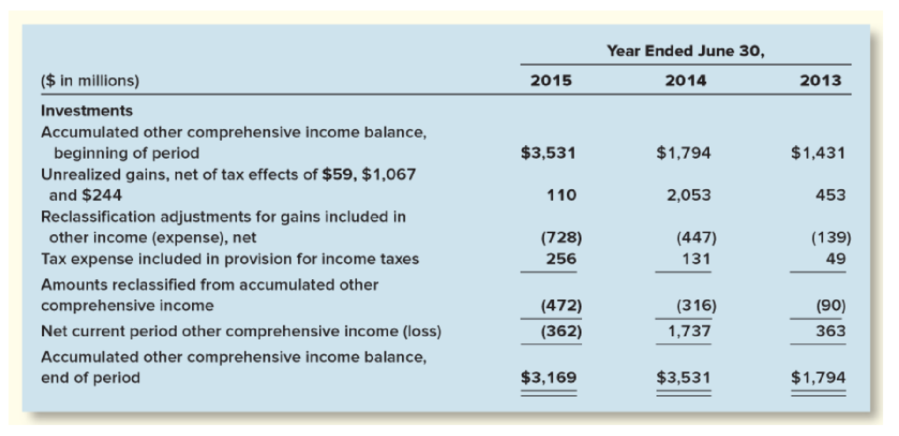

Comprehensive income —Microsoft

• LO12-4

Microsoft’s 2015 10-K includes the following information in Note 20—Accumulated Other Comprehensive Income relevant to its available-for-sale investments:

Required:

1. Prepare a

2. Prepare a journal entry to record Microsoft’s reclassification adjustment for 2015.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

7.8.25

Use table 7.13 to answer the following questions.

a) compute the tax due in 2014 on a net taxable income of $80k. show your work.

b) compute the effective tax rate for that income.

c) check your answers with those in the spreadsheet graduatedtax.xlsx

d) compute the effective tax rate a second time, as a weighted average of the rates in the various brackets, using as weights the amount of income subject to tax at each rate. you should get the same answer.

Intermediate Accounting ll ch 16

7. At the end of 2023, Payne Industries had a deferred tax asset account with a balance of $25 million attributable to a temporary book-tax difference of $100 million in a liability for estimated expenses. At the end of 2024, the temporary difference is $64 million. Payne has no other temporary differences and no valuation allowance for the deferred tax asset. Taxable income for 2024 is $180 million and the tax rate is 25%.

Required:

Prepare the journal entry(s) to record Payne’s income taxes for 2024, assuming it is more likely than not that the deferred tax asset will be realized in full.

Prepare the journal entry(s) to record Payne’s income taxes for 2024, assuming it is more likely than not that only one-fourth of the deferred tax asset ultimately will be realized.

Required 1

Record 2024 income taxes

Transaction

General Journal

Debit

Credit

1

Record…

Required information

Problem 12-51 (LO 12-3) (Algo)

Skip to question

[The following information applies to the questions displayed below.]

Sandra would like to organize LAB as either an LLC (taxed as a sole proprietorship) or a C corporation. In either form, the entity is expected to generate an 13 percent annual before-tax return on a $660,000 investment. Sandra’s marginal income tax rate is 37 percent, and her tax rate on dividends and capital gains is 23.8 percent (including the 3.8 percent net investment income tax). If Sandra organizes LAB as an LLC, she will be required to pay an additional 2.9 percent for self-employment tax and an additional 0.9 percent for the additional Medicare tax. LAB’s income is not qualified business income (QBI) so Sandra is not allowed to claim the QBI deduction. Assume that LAB will distribute all of its after-tax earnings every year as a dividend if it is formed as a C corporation. (Round your intermediate computations to the nearest whole dollar…

Chapter 12 Solutions

INTERMEDIATE ACCT VOL.2>CUSTOM<

Ch. 12 - All investments in debt securities are classified...Ch. 12 - When market rates of interest rise after a...Ch. 12 - Does GAAP distinguish between fair values that are...Ch. 12 - When a debt investment is acquired to be held for...Ch. 12 - Prob. 12.5QCh. 12 - What is comprehensive income? Its composition...Ch. 12 - Why are holding gains and losses treated...Ch. 12 - Prob. 12.8QCh. 12 - Prob. 12.9QCh. 12 - Prob. 12.10Q

Ch. 12 - Under IFRS No. 9, which reporting categories are...Ch. 12 - Prob. 12.12QCh. 12 - Do U.S. GAAP and IFRS differ in the amount of...Ch. 12 - Under what circumstances is the equity method used...Ch. 12 - The equity method has been referred to as a...Ch. 12 - In the application of the equity method, how...Ch. 12 - Prob. 12.17QCh. 12 - Prob. 12.18QCh. 12 - Prob. 12.19QCh. 12 - How does IFRS differ from U.S. GAAP with respect...Ch. 12 - What is the effect of a company electing the fair...Ch. 12 - Define a financial instrument. Provide three...Ch. 12 - Some financial instruments are called derivatives....Ch. 12 - (Based on Appendix 12A) Northwest Carburetor...Ch. 12 - Prob. 12.25QCh. 12 - Prob. 12.26QCh. 12 - (Based on Appendix 12B) Reporting an investment at...Ch. 12 - Prob. 12.28QCh. 12 - Explain how the CECL model (introduced in ASU No....Ch. 12 - Prob. 12.30QCh. 12 - Prob. 12.1BECh. 12 - Prob. 12.2BECh. 12 - Trading securities LO12-3 For the Coca-Cola bonds...Ch. 12 - Available -for-sale securities LO12-4 SL...Ch. 12 - Available -for-sale securities LO12-4 For the...Ch. 12 - Prob. 12.6BECh. 12 - Prob. 12.7BECh. 12 - Prob. 12.8BECh. 12 - Prob. 12.9BECh. 12 - Prob. 12.10BECh. 12 - Equity investments and dividends LO12-5 Turner...Ch. 12 - Prob. 12.12BECh. 12 - Prob. 12.13BECh. 12 - Equity method investments LO12-6, LO12-9 Kim...Ch. 12 - Change in principle; change to the equity method ...Ch. 12 - Fair value option; equity method investments ...Ch. 12 - Prob. 12.17BECh. 12 - Impairments (AFS Credit Loss Model) (Appendix 12B)...Ch. 12 - Prob. 12.19BECh. 12 - Prob. 12.20BECh. 12 - Prob. 12.1ECh. 12 - Prob. 12.2ECh. 12 - Securities held-to-maturity LO12-1 FFT...Ch. 12 - Prob. 12.4ECh. 12 - Prob. 12.5ECh. 12 - Trading securities LO12-1 [This is a variation of...Ch. 12 - Various transactions relating to trading...Ch. 12 - Prob. 12.8ECh. 12 - Securities available-for-sale; adjusting entries ...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Classification of securities; adjusting entries ...Ch. 12 - Prob. 12.14ECh. 12 - Equity investments; fair value through net income ...Ch. 12 - Equity investments; fair value through net income ...Ch. 12 - Prob. 12.17ECh. 12 - Equity investments; fair value through net income ...Ch. 12 - Investment securities and equity method...Ch. 12 - Equity method; purchase; investee income;...Ch. 12 - Error corrections; equity method investment ...Ch. 12 - Prob. 12.22ECh. 12 - Prob. 12.23ECh. 12 - Prob. 12.24ECh. 12 - Prob. 12.25ECh. 12 - Prob. 12.26ECh. 12 - Prob. 12.27ECh. 12 - Prob. 12.28ECh. 12 - Prob. 12.29ECh. 12 - Prob. 12.30ECh. 12 - Prob. 12.31ECh. 12 - Prob. 12.32ECh. 12 - Accounting for impairments under IFRS (Appendix...Ch. 12 - Prob. 12.1PCh. 12 - Prob. 12.2PCh. 12 - Securities available-for-sale; bond investment;...Ch. 12 - Prob. 12.4PCh. 12 - Various transactions related to trading securities...Ch. 12 - Various transactions related to securities...Ch. 12 - Prob. 12.7PCh. 12 - Various transactions relating to trading...Ch. 12 - Securities held-to-maturity; securities available...Ch. 12 - Investment securities and equity method...Ch. 12 - Prob. 12.11PCh. 12 - Prob. 12.12PCh. 12 - Prob. 12.13PCh. 12 - Equity method LO12-6, LO12-7 On January 2, 2018,...Ch. 12 - Prob. 12.15PCh. 12 - Prob. 12.16PCh. 12 - Accounting for debt and equity investments ...Ch. 12 - Prob. 12.18PCh. 12 - Real World Case 121 Intels investments LO12-4 The...Ch. 12 - Prob. 12.2BYPCh. 12 - Prob. 12.4BYPCh. 12 - Prob. 12.6BYPCh. 12 - Real World Case 127 Comprehensive income Microsoft...Ch. 12 - Continuing Cases Target Case LO12-4, LO12-6...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Problem 11-5 (Algorithmic)Special Deductions and Limitations (LO 11.3) Fisafolia Corporation has gross income from operations of $423,000 and operating expenses of $359,550 for 2021. The corporation also has $42,300 in dividends from publicly-traded domestic corporations in which the ownership percentage was 45 percent. Below is the Dividends Received Deduction table to use for this problem.arrow_forwardImmediate Accounting ll Ch 16 3. During 2024, its first year of operations, Baginski Steel Corporation reported a net operating loss of $360,000 for financial reporting and tax purposes. The enacted tax rate is 25%. Required: Prepare the journal entry to recognize the income tax benefit of the net operating loss. Assume the weight of available evidence suggests that future taxable income will be sufficient to benefit from future deductible amounts arising from the net operating loss carryforward. Show the lower portion of the 2024 income statement that reports the income tax benefit of the net operating loss. Required 1 Record 2024 income tax benefit from operating loss Transaction General Journal Debit Credit 1arrow_forwardProblem 11-5Special Deductions and Limitations (LO 11.3) Fisafolia Corporation has gross income from operations of $210,000 and operating expenses of $160,000 for 2021. The corporation also has $30,000 in dividends from publicly-traded domestic corporations in which the ownership percentage was 45 percent. Below is the Dividends Received Deduction table to use for this problem.arrow_forward

- Rr.12. 1.) Calculate taxable income for 20X2 answer: 139,000 2.) Calculate taxes payable for 20X2 answer: 20,850 3.) Determine the current deferred tax liability at 12/31/X2 answer: 37200 4.) calculate total income tax expense for 20X2 answer: 58,050 5.) Compute net income after taxes for 20X2 answer: 328,950 6.) Calculate taxable income for 20X3 answer: 213,027 7.) The entry required at the end of 20X3 requires answer: debit DTL for 26,040 8.) Compute net income after taxes for 20X3 answer: ??? 9.) Calculate taxable income for 20X4 answer: 196,800 10.) Compute net income after taxes for 20X4 answer: ??? Using the information above, solve for parts 8 and 10arrow_forwardProblem 16-7 (Algo) Multiple differences; calculate taxable income; balance sheet classification [LO16-2, 16-3, 16-5, 16-8] Sherrod, Inc., reported pretax accounting income of $92 million for 2021. The following information relates to differences between pretax accounting income and taxable income: Income from installment sales of properties included in pretax accounting income in 2021 exceeded that reported for tax purposes by $6 million. The installment receivable account at year-end 2021 had a balance of $8 million (representing portions of 2020 and 2021 installment sales), expected to be collected equally in 2022 and 2023. Sherrod was assessed a penalty of $3 million by the Environmental Protection Agency for violation of a federal law in 2021. The fine is to be paid in equal amounts in 2021 and 2022. Sherrod rents its operating facilities but owns one asset acquired in 2020 at a cost of $104 million. Depreciation is reported by the straight-line method, assuming a four-year…arrow_forwardProblem 6-55 (LO. 3) For 2021, MSU Corporation has $500,000 of adjusted taxable income, $22,000 of business interest income, and $120,000 of business interest expense. It has average annual gross receipts of more than $26,000,000 over the prior three taxable years. a. What is MSU's interest expense deduction for 2021?$fill in the blank 1 b. How much interest expense can be deducted for 2021 if MSU's adjusted taxable income is $300,000?$fill in the blank 2arrow_forward

- NOPAT 8250000 EBITDA 17725000 Net Income 5050000 Capital Expenditures 6820000 After tax capital costs 6820000 Tax rate 40%Calculate the interest expense and EVAarrow_forwardPROBLEM 2 Complex Company reported the following information relating to income before the 30% tax for accounting purposes: 2021 P 2,000,000 2022 3,000,000 2023 4,000,000 2024 5,000,000 In 2021, Complex Company recognized doubtful accounts of P100,000. Such accounts were considered worthless or uncollectible in 2022, P40,000 and 2023, P60,000. Analysis of the tax and book records disclosed P120,000 in unearned rent income on December 31, 2021 that has been recognized as taxable income in 2021 when the cash was received. Also, on December 31, 2021, estimated warranty cost of P300,000 had been recognized as expense on the books in 2021 when the product sales were made but is not deductible for tax purposes until paid. The unearned rent income on December 31, 2021 is realized and the actual warranty payments were made as follows: Rent income per books Actual warrant payments 2022 P 40,000 P…arrow_forwardInvestment reporting O'Brien Industries Inc. is a hook publisher. The comparative unclassified balance sheets for December 31, Year 2 and Year 1 follow. Selected missing balances are shown by letters. Brien Industries Inc. Balance Sheet December 31, Year 2 and Year 1 Dec. 31, Year 2 Dec 31, Year 1 cash 233,000 220,000 Accounts receivable (net) 136,530 138,000 Available for sale investments (at cost)Note 1 a 103,770 Less valuation allowance for available-for-sale investments b. 2,500 Available for-sale investments (fair value) c 101,270 Interest receivable d Investment in Jolly Roger Co. stockNote 2 e. 77,000 Office equipment (net) 115,000 130,000 Total assets f. 666,270 Accounts payable 69.400 65,000 Common stock 70.000 70,000 Excess of issue price over par 225,000 225,000 Retained earnings g 308,770 Unrealized gain (loss) on available for-sale investments h. (2,500) Total liabilities and Stockholders equity i. 666,270 Note 1. Investments are classified as available for sale. The investments at cost and fair value on December 31, Year 1, are as follows: No. of Shares Cost per Share Total Cost Total Fair Value Bernard Co. stock 2,250 17 38,250 37,500 Chadwick Co. stock 1,260 52 65,520 63,770 103,770 101,270 Note 2. The investment in Jolly Roger Co. stock is an equity method investment representing 30% of the outstanding .shares of Jolly Roger Co. The following selected investment transactions occurred during Year 2: May 5. Purchased 3,080 shares of Gozar Inc. at 30 per share including brokerage commission. Gozar Inc. is classified as an available-for-sale security. Oct. 1. Purchased 40,000 of Nightline co. 6%, 10-Year bonds at 100. The bonds are classified as available for sale. The bonds pay interest on October 1 and April 1. 9. Dividends of 12,500 are received on the Jolly Roger co. investment. Dec. 31 Jolly Roger co. reported a total net income of 112,000 for year 2. O'Brien industries Inc. recorded equity earnings for its share of Jolly Roger co. net income. 31. Accrued three months of interest on the Nightline bonds. 31. Adjusted the available-for-sale investment portfolio to fair value, using the following fair value per-share amounts: Available-for-Sale Investments Fair Value Bernard Co. stock 15,40 per share Chadwick Co. stock 46,00 per share Gozar Inc. stock 32,00 per share Nightline Co. bonds 98 per 100 of face amount Dec. 31. Closed the OBrien Industries Inc. net income of 146,230. O'Brien Industries Inc. paid no dividends during the year. Instructions Determine the missing letters in the unclassified balance sheet. Provide appropriate supporting calculations.arrow_forward

- Nineteen measures of solvency and profitability The comparative financial statements of Bettancort Inc. are as follows. The market price of Bettancort Inc. common stock was 71.25 on December 31, 2016. Bettancort Inc. Comparative Retained Earnings Statement For the Years Ended December 31, 2016 and 2015 2016 2015 Retained earnings. January 1......................................... 2,655,000 2,400,000 Add net income for year............................................. 300,000 280,000 Total............................................................... 2,955,000 2,680,000 Deduct dividends: On preferred stock................................................ 15,000 15,000 On common stock................................................. 10,000 10,000 Total........................................................... 25,000 25,000 Retained earnings. December 31..................................... 2,930,000 2,655,000 Bettancort Inc. Comparative Retained Earnings Statement For the Years Ended December 31, 2016 and 2015 2016 2015 Sales...................... 1,200,000 1,000,000 Cost of goods sold............ 500,000 475,000 Gross profit............... 700,000 525,000 Selling expenses.......... 240,000 200,000 Administrative expenses...... 180,000 150,000 Total operating expenses.. 420,000 350,000 Income from operations.. 280,000 175,000 Other income............. 166,000 225,000 446,000 400,000 Other expense (Interest)... 66,000 60,000 Income before income tax 380,000 340,000 Income tax expense....... 80,000 60,000 Net income............... 300,000 280,000 Bettancort Inc. Comparative Retained Earnings Statement For the Years Ended December 31, 2016 and 2015 Dec.31, 2016 Dec. 31, 2015 Assets Current Assets: Cash.................................... 450,000 400,000 Marketable securities.................... 300,000 260,000 Accounts receivable (net)................. 130,000 110,000 Inventories.............................. 67,000 58,000 Prepaid expenses........................ 153,000 139,000 Total current assets..................... 1,100,000 967,000 Long-term investments.................... 2,350,000 2,200,000 Property, plant and equipment (net)....... 1,320,000 1,118,000 Total assets............................... 4,770,000 4,355,000 Liabilities Current liabilities.......................... 440,000 400,000 Long-term liabilities: Mortgage note payable, 8.8%, due 2021... 100,000 0 Bonds payable, 9%, due 2017............. 1,000,000 1,000,000 Total long term liabilities............... 1,100,000 1,000,000 Total liabilities............................ 1,540,000 1,400,000 Stockholders' equity Preferred stock 0.90, 10 par.. 200,000 200,000 Common stock. 5 par..................... 100,000 100,000 Retained earnings......................... 2,930,000 2,665,000 Total stockholders equity............... 3,230,000 2,955,000 Total liabilities and stockholders' equity..... 4,770,000 4,355,000 Instructions Determine the following measures for 2016, rounding to one decimal place: 1. Working capital 2. Current ratio 3. Quick ratio 4. Accounts receivable turnover 5. Number of days' sales in receivables 6. Inventory turnover 7. Number of days' sales in inventory 8. Ratio of fixed assets to long-term liabilities 9. Ratio of liabilities to stockholders equity 10. Number of times interest charges are earned 11. Number of times preferred dividends are earned 12. Ratio of sales to assets 13. Rate earned on total assets 14. Rate earned on stockholders' equity 15. Rate earned on common stockholders' equity 16. Earnings per share on common stock 17. Price-earnings ratio 18. Dividends per share of common stock 19. Dividend yieldarrow_forwardRequired information Problem 8-50 (LO 8-1) (Static) [The following information applies to the questions displayed below.] Lacy is a single taxpayer. In 2021, her taxable income is $42,000. What is her tax liability in each of the following alternative situations? Use Tax Rate Schedule, Dividends and Capital Gains Tax Rates for reference. (Do not round intermediate calculations. Round your answer to 2 decimal places.) c. Her $42,000 of taxable income includes $5,000 of qualified dividends.arrow_forward7.8.26 a),b) Use the spreadsheet federalindividualratehistory.xlsx to answer the questions. It contains a complete history of income tax brackets and rates from the inception of the income tax in 1913 through 2013, in both dollars current in each year and adjusted for inflation (2012 dollars) a) compute the tax due in 2003 for a single taxpayer with a net taxable income of $30k. what is her effective tax rate? b) suppose the taxpayer received raises each year that kept up with inflation. use an inflation calculator to calculate her net taxable income in 2013.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)

Accounting

ISBN:9781285743615

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Financial & Managerial Accounting

Accounting

ISBN:9781285866307

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Chapter 19 Accounting for Income Taxes Part 1; Author: Vicki Stewart;https://www.youtube.com/watch?v=FMjwcdZhLoE;License: Standard Youtube License